while WE slept: bonds build on gains (UK gilts lead, CPI); HOPE springs eternal (BAML FMS on growth expectations); and a shop moves neutral small vs large caps

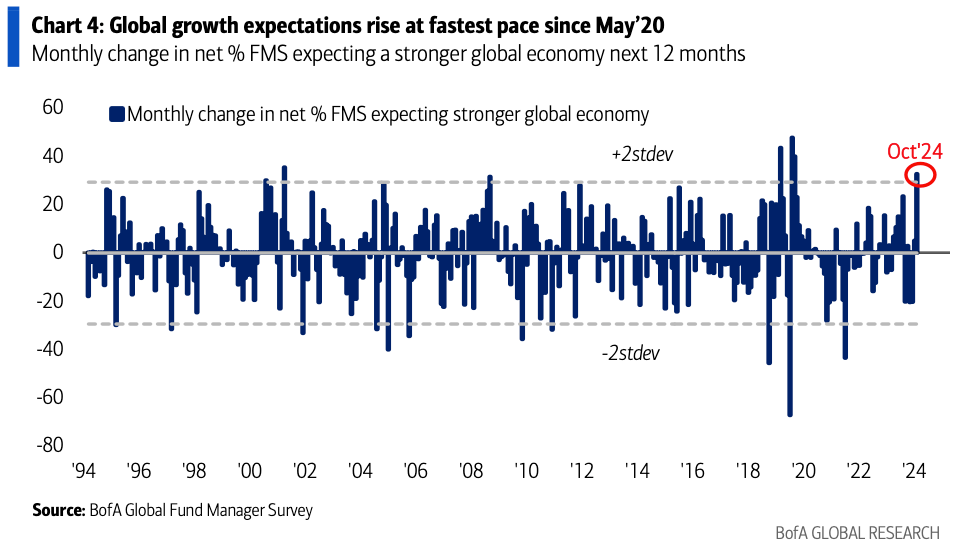

Good morning … I’ll lead with a chart from BAMLs latest Global Fund Manager Survey (which I’ve yet to stumble on — and when I do, i’ll pass along) via the intertubes as it summarizes a view quite nicely …

Global growth expectations rose from -47% to -10%...the 5th largest jump since 1994 ... on the back of 50bps Fed cut, +250k payroll print, and China stimulus.

… and one might assume these fund managers surveyed are, in fact, putting their (our) money where their mouths are … hate to assume, we know how that goes but with that good bit of optimism and HOPE in mind …

ZH: Empire Fed Manufacturing Crashes From 30-Month High To 5-Month Low...

… HOPE meeting reality or HOPE as a lagging indicator … good times, good times … unless of course, you mfg something in / around the NY (aka the Empire State) area?

Moving on / away from The Empire State to, well … ok we’re not going to stray far off the reservation with this next point of data and ray of light ALSO from NY area …

ZH: Stagflation Odds Jump In Latest NY Fed Survey As Inflation Expectations Rise, Delinquency Fears Hit 4 Year High

… HOPE springs eternally and with little else to add, here is a snapshot OF USTs as of 658a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Sentiment hit by poor tech and luxury earnings; Gilts fuelled by softer CPI … Bonds continue to build on the prior day’s gains, with upside also fuelled by the aforementioned UK CPI report, which has led to clear outperformance in Gilts … USTs are holding in the green, taking the lead from the above but yet to extend much further with US specifics light. USTs are just off a 112-20 peak, resistance at 112-21 from last week and thereafter 112-24 and 112-28+.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

… elections continue to garner global attn …

ABNAmro: For every new regulation we’ll scrap two, no, ten! | Insights newsletter

Regulation and enforcement will be kept in place or strengthened under Harris, it will be weakened under Trump. The ability to change regulation will depend on congress’ makeup. Trump is better positioned to circumvent legislation and bypass congress.

… from bonds yesterday, this techAmentalist offering views on rates and these are likely ‘joined at the hip’ with bonds …

CitiFX Oil: Choppy, with a chance of finding support

…WTI futures (CL1): It is a similar set of technicals for WTI. In this case, WTI has tested resistance at 77.35-79.27 (200d MA, 55w MA and 200w MA). The price has broken below initial support at 72.79 (55d MA), and is on track to post an evening star formation on the weekly chart.

For WTI, the key level to watch is 67.71 (Dec 2023 low), which we have held on a weekly basis. IF we see a weekly break below, it would open the door to a move towards 63.43-63.64 (2023 low and Dec 2021 low). Resistance is at 77.35-79.27.

…Even with the tech sell-off, in some ways the most important move yesterday was the decline in oil prices, with Brent crude (-4.14%) down for a third consecutive day to $74.25/bbl. That followed the Washington Post report we mentioned yesterday, saying that Israel would strike military infrastructure in Iran, and not oil or nuclear facilities. So that took out some of the geopolitical risk premium from oil prices, but there remains significant concern about an escalatory spiral and the potential for a wider conflict, as Iran have said that they would respond to any Israeli attack.

That decline in oil prices meant investors became more relaxed about inflationary pressures, which have moved increasingly onto the radar over recent weeks. In fact, the 5yr US inflation swap fell by -4.1bps yesterday to 2.48%, marking its biggest daily decline in over a month. And in turn, investors dialled up the likelihood of rate cuts over the months ahead, with the rate priced in for the Fed’s June 2025 meeting falling -2.8bps to 3.62%. That also came as the New York Fed’s latest Survey of Consumer Expectations showed that debt delinquency expectations moved higher once again, with the mean probability of not being able to make a minimum debt payment over the next 3 months rising to 14.2%, which is the highest since April 2020 at the height of the pandemic.

With rate cut expectations moving higher again, that led to a sovereign bond rally on both sides of the Atlantic. In the US, that meant the 10yr Treasury fell -6.7bps to 4.03%, although the 2yr yield was down by a smaller -0.9bps to 3.95%. The decline was most pronounced at the long-end, with 30yr yields (-9.1bps) seeing their sharpest decline since the vol shock on August 2…

DB: Monthly charts: November air brings election risks to the outlook

This monthly chartbook highlights our top charts for understanding the current state of the US economy and the outlook for 2024-26. In this edition, we feature a deep dive into the labor market, drivers of the near-term outlook, an assessment of consumer fundamentals, our outlook for inflation, and our expectations for Fed policy. We also detail recent polling for the US election and summarize the economic implications of different policy proposals (see more here: "Election outcomes: Growth and deficit impacts").

… Fed expectations: DB, market and Fed now mostly aligned on path ahead

..Real monetary policy stance has reached elevated levels from a historical perspective

… a few words on small caps …

MS IDEA: US Equity Strategy: Small Caps, Are We There Yet?

We are neutral on Small vs Large caps and prefer Quality and Value within the Small cap universe. At the sector/industry level, Financials, Industrials, Biotech, and Software look attractive within Small Caps. We present screens for stock selection in today's report.

… and finally from everyone’s fav UK economist pontificating on ‘bout US situation …

Former US President Trump suggested tariffs of up to 2,000% on cars imported from Mexico (an unconventional interpretation of NAFTA). US and European investors have viewed proposed tariffs as a bargaining device, not to be taken seriously. The random suggestion of numbers like 2,000% does suggest more rhetoric than rigorous policy analysis. However, the repeated theme of trade taxes implies the policy is important.

The proposed universal tariff of 20% paid by US consumers of any imported product would be disruptive. The US imports more now than did in 1971 (the last universal tariff). It uses more imports to manufacture exports, risking a competitive disadvantage. A tariff is applied to the import price, not consumer prices, so a 20% tariff should raise consumer prices for imported goods less than 10%. Retailers may use the narrative of a 20% tax to raise their prices more than the tariff cost alone, however.

Media reports suggest Israel has reassured the US that it will not target Iranian oil facilities. This has reduced the risk premium in the oil price…

… And from Global Wall Street inbox TO the WWW,

First up an official siting of (or at least search for) … canaries in the coalmine?

Chicago Fed: Searching for “Inflation Canaries” in Household Surveys

…Conclusion Identifying inflation canaries, or people who reliably signal a change in inflation via their expectations, is not an easy task. Current household surveys of inflation expectations are not designed for this. To do this well, one would need samples that are both larger in scale and broader in scope than existing surveys.

In particular, to properly identify inflation canaries, a long panel of responses is necessary so that one could compare multiple assessments of inflation expectations for a given individual to realized inflation. While it is standard to ask individuals more than once to predict inflation over the next 12 months, current survey panels are still too short to effectively use the insights from individuals with accurate expectations in forecasting, because individuals are out of the sample by the time the accuracy of their predictions can be checked. In addition, respondents appear to take several months to learn how to properly answer questions about inflation expectations.

Interviewing a greater number of respondents over longer, staggered time periods—for example, using a 6in-6out-6in sample design—would greatly increase the potential to identify inflation canaries. Our analysis suggests that this change in survey design, combined with focusing on changes in expectations rather than levels, is a promising path forward in the search for inflation canaries. Larger and longer surveys would naturally be more expensive, but given the potential of these investments to improve inflation forecasts, they seem worthy of exploration.

We are currently at a stage where many macro assets seem overextended and are likely to reverse their trends, in my view.

The US dollar and 2-year yields are prime examples of this.

Just as short-term rates experienced a steep decline from May to September, they have now surged to significantly overbought levels in the past two weeks.

This trend seems entirely unsustainable to me and is likely to clash with the government’s increasing struggle to manage the rising cost of servicing its debt.

Notice how 2-year yields are significantly elevated compared to the much lower historical support seen today.

Consequentially, I believe that a decline in short-term rates could substantially affect the US dollar, especially given that the DXY index is currently overbought, with the 9-day RSI approaching 80.

If you don't already sub DC-Daily Chartbook Lite on the Stack he gives 5 freebies daily (you've got to pay for the Full Monte 30 daily charts). Do note he's going on hiatus for about a wk, in his words "a baby chartbook is scheduled for delivery Oct 23rd" :)

If you don't already sub DC-Daily Chartbook Lite on the Stack he gives 5 freebies daily (you've got to pay for the Full Monte 30 daily charts). Do note he's going on hiatus for about a wk, in his words "a baby chartbook is scheduled for delivery Oct 23rd" :)

pavchartbook+dc-lite@substack.com