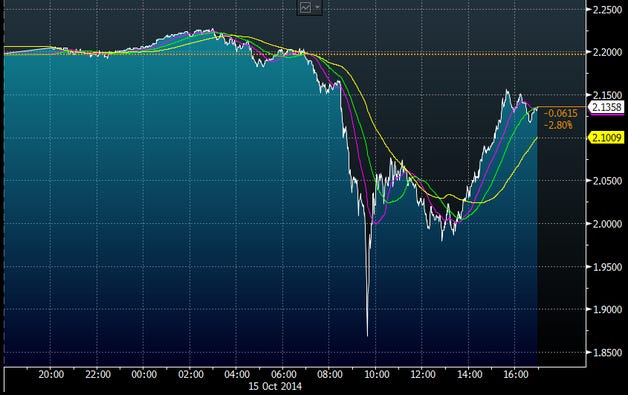

Good morning … happy Flash-Crash (yields)-A-versary (2014) …

Bloomberg: Bond Traders Fear Oct. 15-Style Volatility Could Repeat

… On Oct. 15, U.S. Treasury trading volume soared to record levels as yields on the 10-year note tumbled 0.34 percentage point to a low of 1.86 percent that day. Most of that drop occurred in a 10-minute span from 9:30 a.m. in New York, before yields ended the day at 2.14 percent….

CNBC: US officials: No single cause for 2014 bond market ‘flash crash’

… I will be looking for more evidence to support this outlook in the weeks and months to come. But, unfortunately, it won’t be easy to interpret the October jobs report to be released just before the next FOMC meeting. This report will most likely show a significant but temporary loss of jobs from the two recent hurricanes and the strike at Boeing. I expect these factors may reduce employment growth by more than 100,000 this month, and there may be a small effect on the unemployment rate, but I’m not sure it will be that visible. Since the jobs report will come during the usual blackout period for policymakers commenting on the economy, you won’t have any of us trying to put this low reading into perspective, though I hope others will…

… or perhaps some ‘good news’ out the Middle East …

WaPO: Netanyahu tells U.S. that Israel will strike Iranian military, not nuclear or oil, targets, officials say The signal is being seen in Washington as a sign of restraint after concerns that an Israeli strike on oil or nuclear facilities could trigger a wider war.

AND with this sign of restraint, well … some good news …

… dunno for sure but the bond market is back and bid. On THAT, here is a snapshot OF USTs as of 657a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bull-flattening alongside Gilts and EGBs after a strong 30y UK auction, sharply weaker Oil prices (-5%), and softer China markets (SHCOMP -2.5%) after limited stimulus relief and poor SEPT export data (see above). Our futures desk noted that fast$ short-covering in the long-end might be driving the duration rally after yesterday’s attempt at new local lows on thin holiday liquidity. Early-London block sellers of 4k FV and 3.35k UXY were well absorbed into the long-end outperformance, especially in the 20y point. Elsewhere, solid peripheral spread tightening is being seen (Italy -2bps to Gmy in 10y), while USDJPY is -0.4% and DXY -0.2%. The NKY (+0.8%) held in well overnight, while the DAX is showing +0.3% alongside a small positive bias for S&Ps this morning (+2pts here at 6:50am).

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Crude slumps after constructive geopolitical updates, US earnings ahead … Bonds are firmer, continuing the modest rebound seen in the prior session, but also deriving support from lower oil prices … USTs firmer with the above applying, at a 112-07+ peak; yield curve mixed (returning from holiday outages for cash) with the short end seemingly propped up by Fed’s Waller on Monday while the long-end slumps given energy.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

While all the news / views of China have been consumed and largely NOT passed along, the following was a writeup which caught MY attention and which I felt compelled to share …

China's export growth missed the consensus by a wide margin, with slowing exports to both EMs and DMs. Signs of headwinds to exports in H2 include a reversal in the global manufacturing upcycle, a slump in the exporter-oriented Caixin manufacturing PMI, and rising trade tensions with EMs.

September: 2.4% y/y for exports, and 0.3% y/y for imports (both in USD terms)

Bloomberg consensus (Barclays): 6.0% y/y (5.0%) for exports, and 0.8% y/y (0.3%) for imports

August: 8.7% y/y for exports, and 0.5% y/y for imports (both in USD terms)

… this same shop then offered some ‘creative thinking’ notes on weekend presser

BARCAP: China Stimulus: MOF press briefing: room for imagination

The MoF press briefing offered forward guidance but the scale of new stimulus may fall short of expectations. We examine the available details of the property and debt relief measures, and conclude it is not the 'whatever it takes' moment just yet.

… and as I see it and in my very unprofessional view, China still the mfg to the world and IF / when exports and the CB are signalling, we should attempt to make something OF said signals … This may be something for Team Rate CUT to consider (and may help bring November back in to the building?)

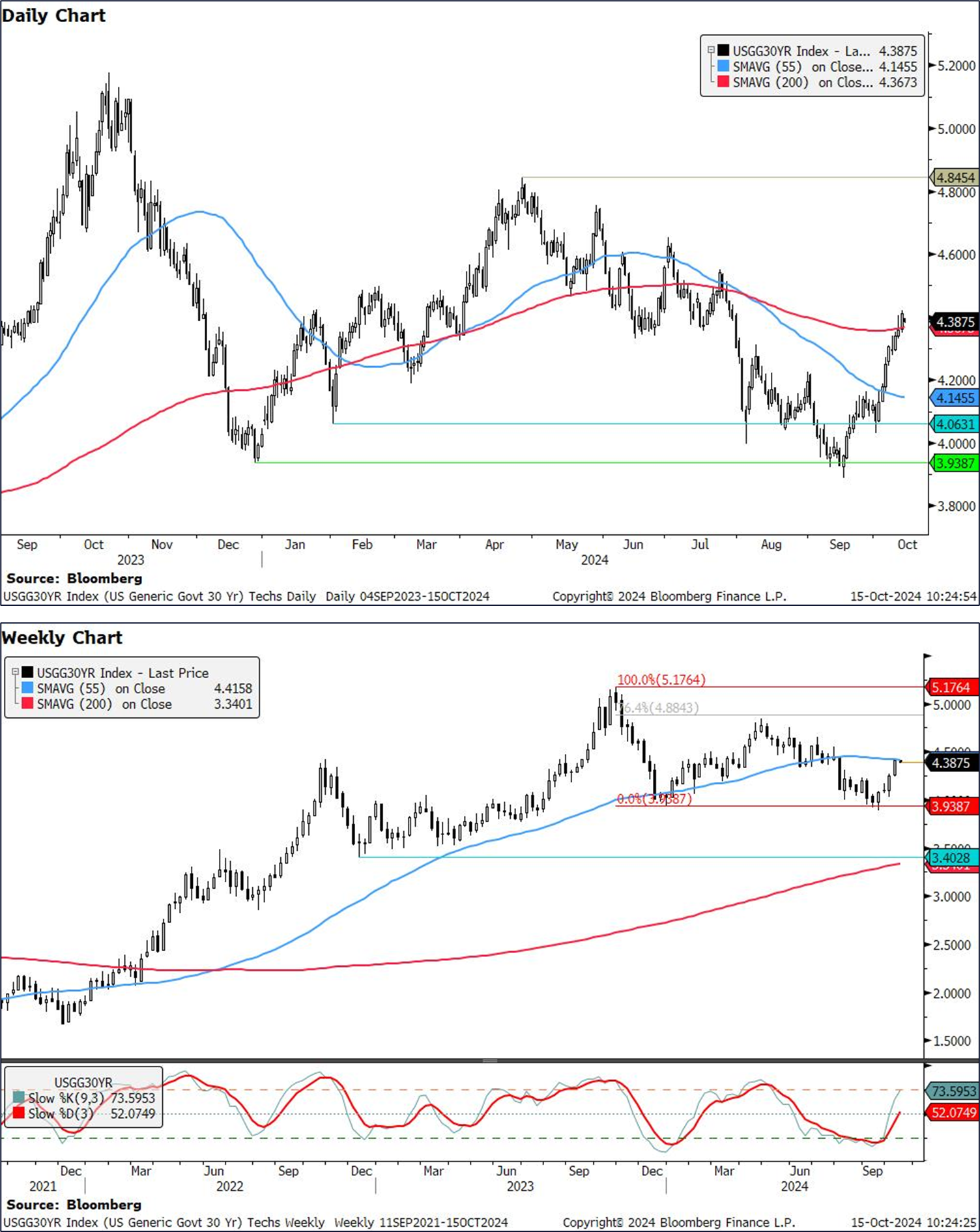

US rates are testing interesting resistance levels. While the momentum on yields suggests that we could see further upside, strong upcoming resistance could keep yields rangebound…

…US 30y yields: Yields are testing resistance at 4.42% (55w MA) and a significant level for 30y yields. IF we break above decisively on a weekly basis, we could see a move higher towards 4.65% (July high). This would be further supported by the move higher in weekly slow stochastics, which are showing no signs of crossing back lower.

For support, the key level remains 3.94% (Dec 2023 low), which we have not managed to close below on a weekly basis.

… Moving onto rates, it was an uneventful session thanks to the bond holiday in the US. But futures markets were open, and there were some indications that investors were becoming a bit more sceptical about rapid rate cuts from the Fed. For instance, the probability of a rate cut in November was dialled back slightly to 87%, having been at 89% at Friday’s close. And looking further out, the rate priced in by the Fed’s June 2025 meeting was up +3.2bps on the day to 3.65%. The moves came as Fed speakers continued to steer us away from expecting rapid easing, with Minneapolis Fed President Kashkari saying that “further modest reductions” would be appropriate over the quarters ahead, while Fed Governor Waller noted that “policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting”. The oil move over the last 36 hours may temper some of these more hawkish rate expectations today but Treasuries have reopened fairly flat in Asia hours after the holiday.

One reason that investors have been dialling back their expectations for rate cuts is a growing focus on inflation risk. Henry pointed out yesterday (link here) that the US 5yr inflation swap has now seen its biggest jump over five weeks since early March 2023, just before SVB’s collapse. That’s been driven by several factors, but it’s clear that inflationary pressures have been building, with commodities bouncing back thanks to China’s stimulus and developments in the Middle East, whilst central banks have engaged in faster easing than was expected only a few weeks earlier, not least with the Fed cutting by 50bps last month. So with the ECB widely expected to become the latest central bank to cut rates again this week, that’s one to keep an eye on…

… with change in the air, a quick recap of the ‘major’ happenings …

That was quite some move. In the space of a few weeks, bonds gave back a significant proportion of the gains of the previous six months, with both 2Y and 10Y yields settling back above 4.0%. US 10-year Treasury yields have risen 45bp from the trough of 3.62% (16 September) and stand at 4.07%, so that’s a 41% retracement of this year’s rally, which started with the yield peak of 4.71% on 25 April.

Let’s put some context around the recent move and then ask the question whether this is the start of a broader trend, or just a correction in what was turning out to be a good year for the bond market?

The bond sell-off has occurred since the Fed cut rates by a larger-than-expected 50bp on 18 September. This was the point when yields hit the low for the year, and rather than set the scene for a series of rate cuts, the new narrative appears to be that the move was large to make up for the inaction of July. What’s more, it was a divided decision. Inflation data supports looser policy, while the persistent strength in the real economy does not. Repricing from 50bp to steadier 25bp increments, at the upcoming FOMC meetings, explains the 49bp increase in the two-year segment that led this move higher in yields.

A week after the Fed’s 50bp rate cut, there was a September surprise from the PBoC, with easing and the promise of more to come, and extending from this, hope of a further uplift from fiscal policy. The boost to expectations was most evident in Chinese equities, with the CSI300 index surging 35% from the lows at one point (now 26%). This lift in confidence was felt across the globe, with stock markets reaching new highs, alleviating concerns of entrenched deflation in the world’s second-biggest economy. What’s good for the riskier asset classes, particularly equities, tends to be bad for bonds.

Amid all these moves there is still the backdrop of heightened geopolitical risk and, the elephant in the room, a US election just weeks away that’s too close to call. A Republican sweep, combined with an economy close to “no landing” mode, argues for higher Treasury yields on the basis that the Fed shouldn’t be easing. Most other scenarios point to something between today’s valuations and a return to lower yields. As the Fed will remind us, it all depends on the data.

Anyway, the above is all rather current and has not fully addressed the question: has something changed so that this is the start of a broader trend? We offer four key perspectives.

First, longer-term context matters …

Second, measures of longer-run equilibrium policy rates, those that forwards are doing their best to estimate, have high levels of global interconnectivity in developed economies1…

Third, extending the global angle, the rest of the world is in easing mode….

Fourth, cyclical versus structural drivers …

In summary, there is no new bull case for bonds to present here because the factors that were in place a few weeks ago still apply. The arguments that supported the decline in bond yields these past six months have not suddenly become invalid. The Bloomberg median forecast for the 10-year Treasury at the end of 2024 tells the story: it fell from 4.20% in July to 3.74% in September. Maybe the bond market just got over-extended, and investors now get the opportunity to invest at much better yields than a few weeks ago.

As always, there is a need to consider the near-term cyclical and political considerations in the US, along with longer-run structural trends, both at home and abroad. Plus ça change, plus c'est la même chose.

… soft / hard / NO landing debate continues and the good doctor weighs in …

Yardeni: DEEP DIVE: The Widely Feared Phantom Recession Is Over

This is an excerpt from our October 7, 2024 Yardeni Research Morning Briefing. It was written after the release of September's blowout employment report on Friday, October 4.

… And from Global Wall Street inbox TO the WWW … on markets and efficiency, there’s theory and practice … a few words …

AAM Viewpoints — Is the Market Efficiency Theory Working or is it Apathy?

As we have previously stated, perhaps more than any time in history, we are in a confirmation bias-type market, but that is not due to the somewhat extreme levels seen in various markets, but rather the deluge of data and interpretations that are offered to the average investor. While data proliferation is more commonly associated with the logistics of storing it, this is easily transferred to the consumer who is attempting to digest the same data that would have historically been delivered over weeks or months and is now condensed into seconds.

So, that brings us to a more pertinent question, “Are the levels of the current markets exhibiting a more elegant efficient market pricing mechanism of future events or is it more bluntly apathetic?”

To address this in more detail, let’s consider what is priced in relative to other points in history. Perhaps most importantly for the markets is the gauge of inflation and interest rates and where expectations are in the immediate future and further down the road. Many have pointed to the large reduction in inflation from abnormal highs as progress and moving back to “normal.” Currently the Consumer Price Index (CPI) is running at 2.50% on a year-over-year basis while the Personal Consumption Expenditure (PCE) core index is running at 2.7%. The PCE number is cut nearly in half from its high and significantly lower than the 65-year average of 3.24%. CPI has fallen over 70% from its recent high and similar to the PCE, is off its 65-year average of 3.7%.

Expectations have moved from the accepted Federal Reserve target of 2.00% to 2.5–2.8% depending upon which measure one references. So, we still see expectations higher than where we are at now and higher than the commonly accepted rate for the Federal Reserve, but interest rates are pricing in a more benign market. Could inflation expectations be set for a surprise?

… … At the max expectation, we were at nearly nine cuts being priced into the markets as evidenced by the chart below. However, this changed drastically as economic data came in stronger which caused expectations to become more timid, and why the 10-year Treasury yield has risen 40bps since September 16. However, consider that the chart below showed four fewer cuts next year, which equates to 100bps (4 x 25bps standard cut move). Does that mean the 10-year on a current level has another 60bps to move higher? Again, the debate of apathy or nuanced efficient market theory — which is more correct?

I wanted to share with you my latest Investment Outlook, titled “It’s a BullMarket You Know” after the line spoken by the “Turkey” character in the iconic“Reminiscences of a Stock Operator” book. Bottom line is I expect low butpositive investment returns over the balance of 2024. No bear market but it’snot the same bull market anymore. You know.

There was a reminder recently by Josh Brown, the excellent market strategist on CNBC, of a phrase in Jesse Livermore’s “Reminiscences of a Stock Operator” which told of an old sage called the “Turkey” who when asked about the stock market’s future characteristically proclaimed “it’s a bull market you know.” In the past few years it certainly has been. No wonder. Massive annual fiscal deficits of 2 trillion dollars leading to accelerating inflation beginning in 2021 in effect created monetary ease despite a Federal Reserve supposedly tightening credit as it raised Fed Funds to 5¼% in mid 2023. Ease? It wasn’t really a tight policy until mid 2023 — just a year ago, that an unbiased observer could claim that the cost of money was anywhere close to restrictive.

That and an obvious burst of AI investment spending, accompanied by a continuing GDP fiscal deficit of 7-8% have provided fuel for the Turkey’s mantra. It has been a bull market post Covid. But now? …

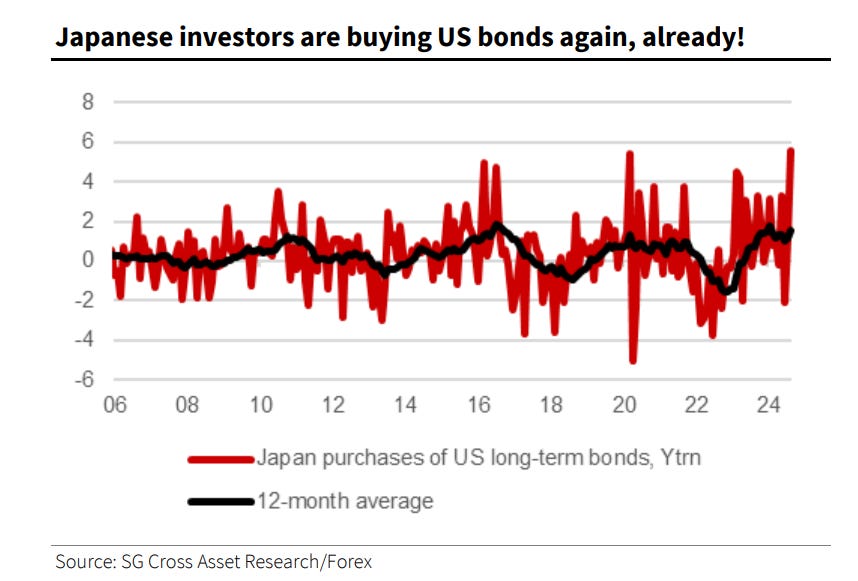

… Foreign investors have increased their net holdings of US assets by a staggering $40 trillion since 2020, with the dollar still close to a multi-decade high in real terms. Japanese investors’ enthusiasm for the dollar, Juckes adds, takes US exceptionalism to new levels:

A strong dollar has its pitfalls for Washington. Juckes argues that the US needs a large devaluation to restore the competitive position of its industry (a position also taken by presidential candidate Donald Trump), but inflows of capital make that increasingly difficult…

Tnx 🙏