Good morning … Everything is awesome, economy is fine, Fed has to NOT CUT …

CNBC: Target beats on earnings and revenue, but gives cautious sales outlook for the year

Yahoo: Target cut prices on 5,000 products. Now it's back with a big earnings beat.

… And so with Target earnings out and to be picked over I’ll leave that for those far better qualified … With fewer and fewer eyeballs around, I’ll spare you a look at an on the run UST yield and head right TO some of the clickbait and rhetoric which seems to be amping up quite a bit (hey, its not just at the DNC last night) …

ZH: Did Kam-unism Send Philly Fed Business Survey Crashing To COVID Lows?

… On a non-seasonally-adjusted basis (what exactly is a seasonally-adjusted 'sentiment'?), it was an even bigger collapse...

… Oh, and about that price-gouging stuff... for the last three years, businesses (at least in the Philly Fed region) have seen nothing but margin compression and pain as the prices paid for goods dominated the prices received for goods...

…Finally, today's Philly Fed survey joins a recent rash of 'soft' sentiment surveys that has reversed the rebound we saw in Q2...

… clickbait maybe but while I can’t say I (or friends, clients, traders I knew) ever put too much weight in Philly Fed index, the idea here is that it’s part of what is making up the current rate cut narrative.

We can see both hard and soft data back to / near March 2023 levels (hmmm, what happened back then?) and the ‘good’ news is the Fed may be closer now to a rate cut then it might / should have been then.

Couple things here which are conflicting. First, given how nothing has (yet) imploded from the March 2023 episode and second, well, don’t higher stock prices and ‘risk ON sentiment’ “… all else equal, argue against more aggressive action”?

Fact remains there are data points and risk sentiment moving ahead of perceived FOMC reaction and the markets moving are not just equities but bonds too.

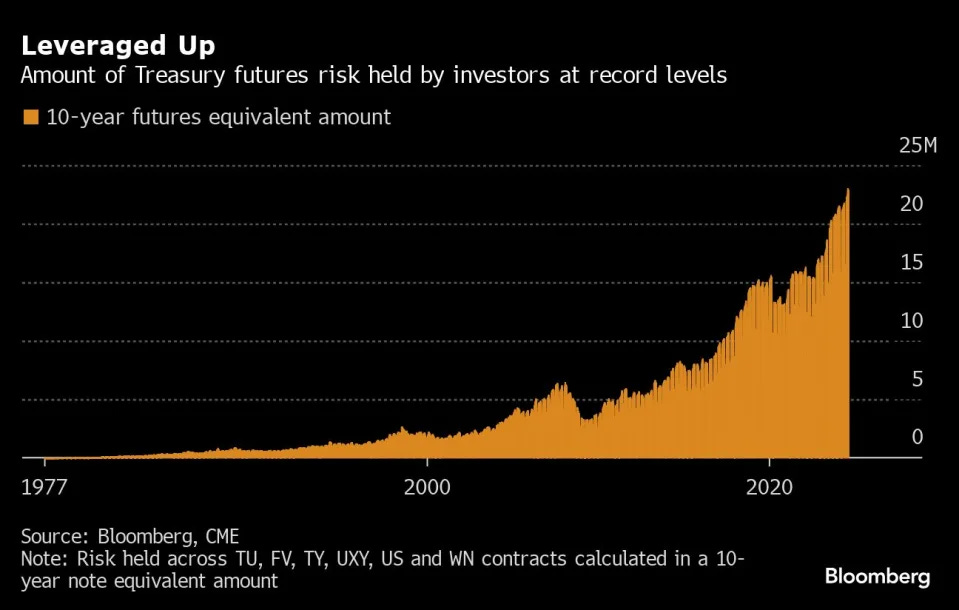

Here’s something for us to feast our eyes on — some POSITIONS related recon from none other than Edward Bolingbroke …

Bloomberg: Bond Traders Amassing Historic Level of Risk on Rate-Cut Bets

(Bloomberg) -- Bond traders are taking on a record amount of risk as they bet big on a Treasury market rally fueled by expectations the Federal Reserve will embark on its first interest-rate cut in more than four years.

The number of leveraged positions in Treasury futures has risen to an all-time high ahead of the central bank’s annual economic symposium in Jackson Hole, Wyoming, which will commence on Thursday. At the event, Fed Chair Jerome Powell will speak and provide more insights into the central bank’s monetary policy path for the rest of this year…

…The rise coincides with a ramp-up in bullish wagers over the past couple of weeks that call for aggressive rate cuts over this year and 2025. Asset managers extended net long positioning by roughly 120,000 10-year note futures equivalents, according to Commodity Futures Trading Commission data for the week ending Aug. 13…

… this is on heels of a large SHORT BASE (largest since middle January) from another subset of speculators, noted HERE…

make of it all whatever you will and I’ll simply move right along … here is a snapshot OF USTs as of 645a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities flat/firmer, Dollar gains & JPY underperforms; US Payroll Revisions & FOMC Minutes due … Bonds are flat with traders mindful of today’s key risk events … USTs are unchanged ahead of payroll revisions, and within a six tick range and holding in proximity to Tuesday's 113-20 peak. Significant downward revisions could spark a dovish move as it adds to the factors in favour of the Fed commencing the easing cycle in September.

… We have always held the view that the 2021 surge in prices was primarily driven by supply disruptions, and that inflation would inevitably fall as the world economy regained its post-pandemic composure – regardless of whether the Federal Reserve tightened policy or not.

Although inflation has indeed fallen sharply, disagreement over the equilibrium interest rate remains as big as ever. With the bond market becoming increasingly volatile, the need to know where the resting spot is for bond yields has only increased…

… All of this means that steady-state real interest rates, both at the short and long ends of the curve, should be higher than what prevailed in the 2010s and more in line with real economic growth.

Chart 11 provides another interesting perspective. It compares the nominal fed funds rate with U.S. nominal GDP growth: whenever the fed funds rate is higher than GDP growth, Fed policy is restrictive, and vice versa.

By this yardstick, a large portion of the rate hikes since 2022 should be considered as rate normalization, and that policy is only slightly restrictive today. However, the chart also highlights the need for the Fed to drop rates because falling inflation (and therefore nominal GDP growth) will make the current policy rate increasingly restrictive.

On balance, it seems that the steady-state Fed policy rate would be around 4.0% if the U.S. were a closed system, but inflows of foreign savings will likely compress the steady-state rate to 3.5%.

If so, the long end of the curve should be around 3.7-3.8%, assuming the term premium is small and at around 20-30 basis points. Our bond model also says the fair value for 10-year Treasury yields is at 3.7% (Chart 12)…

… If the “resting spot” for the long end of the curve indeed is 3.7-3.8%, investors should go long duration if bond yields are above that level, stay at the benchmark duration when yields are nearing their steady-state, but go short duration if yields fall far below the “resting spot”. This is why we cut our bond duration call to neutral from overweight on August 5 when 10-year Treasury yields dropped to 3.7%…

We initiate three trade ideas to position for upside in companies involved in the production of transition metals and copper in particular.

Soaring demand for AI data centres will significantly boost the need for copper in the medium to long term, putting upward pressure on an already-strained market. With supply struggling to keep pace, more companies will look to acquire copper assets inorganically. Amidst the global push for electrification, the metal’s importance will remain undiminished.

We have therefore constructed a basket offering exposure to copper and nickel-exposed liquid companies.

On a shorter time frame, we see current levels as attractive to own SXPP upside tactically as the sector lagged on the recovery over the past couple of weeks.

All eyes this week are on Chair Powell's remarks at Jackson Hole on Friday; our economists’ preview is here. The market will be looking for any clues as to how the FOMC will approach the timing, pace, and extent of rate cuts ahead, and any substantive signals could move markets materially.

For historical perspective on how market-moving Powell’s remarks might be, today’s chart looks at the impact of Fed Chairs’ Jackson Hole (JH) speeches over the past 25 years. The chart shows the change in the 10y nominal UST yield on the days of the remarks, with the moves expressed as a ratio to the average absolute daily change over the prior month. With this normalization for the prevailing rate volatility environment, a value of +/-1 means the 1-day change around Jackson Hole was the same in absolute value as the typical daily move over the preceding month….

… for the first dozen years the 10y reliably increased around Jackson Hole, moving up 10 of 12 years through 2010. But up until the GFC the moves were generally small relative to trailing volatility. Since 2011, Jackson Hole remarks have generally led rates to rally, with the 10y declining most years, and the moves have been a bit larger relative to prevailing vol. That is, the Chair’s remarks seem to have become a bigger driver of longer-term rates, though with values of 1-2 they still generally haven’t been a major market mover. (Incidentally, the reaction to Chair Powell's "there will be pain" remarks in 2022 is a good illustration of why judging the "dovishness" of a speech from the yield reaction can be misleading; equities fell over 3% in response to the hawkish reaction function conveyed in that speech, presumably limiting the extent of the yield increase.)

Extrapolating from the historical reactions and the realized volatility in the 10y over the past month would suggest a move on the order of +/- 5bp this Friday.

The US will be revising last year’s non-farm payrolls data. Markets have a heightened interest in the labor market, and these revisions are likely to be negative. However, this does not change anything about the economy. Making payrolls marginally less inaccurate is about spin, not substance. Consumers have been spending this year based on the labor market they experience, not the labour market that was reported.

The Federal Reserve minutes are due—with investors presuming that the period of policy error is about to end in September, with a rate cut. The Fed is late in cutting rates, but the relative stability of real borrowing rates means it is not a catastrophic error. The revisions to labor market data do emphasize the risks around Fed Chair Powell’s “data dependency” approach…

… And from Global Wall Street inbox TO the WWW,

ING Rates Spark: US payroll revisions could challenge recovered sentiment

Markets are moving cautiously in anticipation of today's US payroll revisions. Estimates vary, but chances are we'll see a significant downward revision of earlier payroll numbers. With risk sentiment still fragile, the balance of risk seems to be tilted towards lower yields and steeper curves

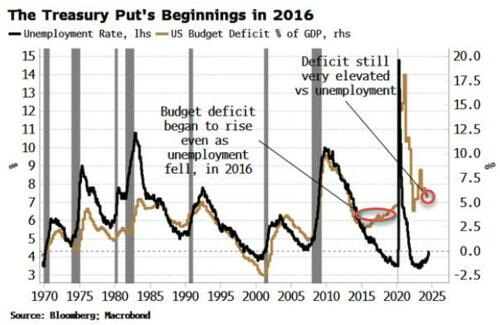

ZeroHedge: Forget The Fed, It's The 'Treasury Put' That Will Keep This Dream Alive 'Til November

The US Treasury has become a key driver of stocks and other asset markets through its pro-cyclical issuance of debt and the increasing depth and liquidity of repo markets. A pullback in fiscal spending now not only indirectly threatens markets through a weaker economy, but also more directly through a contraction of money-like liabilities and the forced deleveraging that it entails.

The year 2016 marked a sea change in US government policy. For the first time in the postwar period, fiscal spending significantly expanded outside of an economic downturn, in the beginnings of the Treasury put. Even more significantly for markets, that was also the precursor to the Treasury becoming the world’s largest de facto shadow bank, through its issuance of the debt which underpins the creation of trillions of dollars of money-like repo liabilities, allowing more leverage and boosting asset prices.

The chart below clearly indicates when fiscal spending and economic growth began to diverge. In 2016, the budget deficit continued to rise even as unemployment fell. An innocuous rise in the cap on discretionary spending in the Bipartisan Budget Act (BBA) nine years ago foreshadowed that unprecedented rupture in the postwar period. After the pandemic the deficit remains elevated — at its highest level outside of war or recession – while employment has been near historic lows.

The Affordable Care Act was implemented in the years prior to the BBA, leading to a rise in Medicaid spending, while Medicare spending also rose. Combined outlays for the two programs along with Social Security reached a record 48% of federal spending and 10% of GDP in 2016…

AND here’s MY view of how Global Wall is currently viewing national political conventions …

At least Seigel's been stuffed back into his hole, was Buffet wheeled out on BubbleVision 2 wks ago? It's not a REAL crash until that happens. As if you read my mind agree that at these 'market' levels any cuts seem silly, although so does the 10 yr IMHO. Nary a mention of Greenspan's measure of market liquidity & interest rates-Gold. By that measure, M2 is too high and rates are far too low. But why care about Gold when you can buy Digits in the sky aka Crypto smh

At least Seigel's been stuffed back into his hole, was Buffet wheeled out on BubbleVision 2 wks ago? It's not a REAL crash until that happens. As if you read my mind agree that at these 'market' levels any cuts seem silly, although so does the 10 yr IMHO. Nary a mention of Greenspan's measure of market liquidity & interest rates-Gold. By that measure, M2 is too high and rates are far too low. But why care about Gold when you can buy Digits in the sky aka Crypto smh