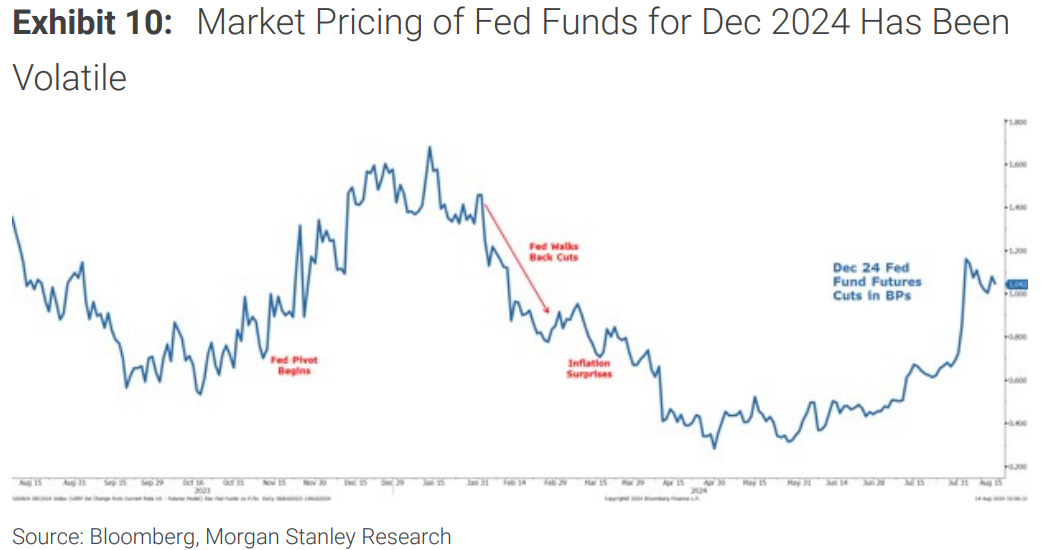

while WE slept: USTs bid (lag BUNDS); Daly supports cuts (FT); BIGger net short 10s; Goldilocks' updated (lower) recession call (and on Team 25bps ONLY)

Good morning … realize it’s early to be talkin’ ‘bout and thinking ahead TO Thurs/Friday (Jackson Hole confab kicks off and JPOW speech on Friday morning) I thought I’d lead with a look at the front end of the curve …

2yy: 4.135% is support and momentum (stochastics) may be a problem heading into rate CUT ? a head fake?

… and with 2s down a basis point this morning one COULD just write this off as statistical noise and nothing OR one might lean on things like this …

US rate-setter challenges fears of recession as global policymakers prepare for Jackson Hole meeting

… Daly, who votes on the Federal Open Market Committee, played down the need for a dramatic response to signs of a weakening labour market, saying the US economy was showing little evidence of heading for a deep downturn. The economy was “not in an urgent place”, she said.

“Gradualism is not weak, it’s not slow, it’s not behind, it’s just prudent,” she said, adding the that labour market — while slowing — was “not weak”…

… “After the first quarter of this year, inflation has just been making gradual progress towards 2 per cent,” Daly said, speaking on Thursday. “We are not there yet, but it’s clearly giving me more confidence that we are on our way to price stability.” …

… Daly said the Fed wanted to loosen the “restrictiveness” of its policy, while still maintaining some restraint to “fully get the job done” on inflation…

… And so, the lowering of rates then is NOT to ease policy restriction but rather to only reduce restriction (relative TO neutral which, not for nuthin’, has no REAL definition, but just made up GUESStimates by Global Wall and ivory tower cognoscenti) … here is a snapshot OF USTs as of 657a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Equities are mixed, DXY as low as 102.00, JPY bid & Crude lower; Fed's Waller due … Bonds are firmer to varying degrees, Bunds lead as Germany reaches a deal regarding its 2025 budget … USTs are bid, but not quite performing as well as Bunds are; holding at 113-09+ highs with resistance from Friday & Thursday at 113-12 & 113-23 respectively.

We expect Chair Powell to pave the way for a September rate cut in his Jackson Hole speech. While not ruling out a 50bp cut in September, we see the chair downplaying fears that the Fed is behind the curve. Our base case remains for a 25bp move.

We continue to favor 5s30s UST steepeners as, historically, the curve has steepened up to the first cut, though Powell’s likely push-back against the notion of imminent economic weakness presents some near-term risk to this view. The USD screens cheap vs. both the EUR and JPY, implying scope for it to outperform these currencies, should Powell push back on the need to cut by 50bp.

Fixed business investment has been a ballast to US growth through H1 and we see AI capex remaining a key theme this earnings season in US equities. We like playing this theme with call spreads on NVDA.

From a medium-term perspective, we think we are in a bond bull market.

But we would caution against going ‘all in’ at this stage because our analysis suggests the market has moved too far, too fast

… Through the lens of bond valuations

… At 3.92%, UST yields are already at their year-end fair value predicated in our base case. That said, fair value would drop further in 2025 (to 3.60% in a very shallow rate-cutting cycle), whereas if a recession were to eventually materialise, the magnitude of the rally could be much larger. For example, 3.60% could be reached fairly quickly should a Fed deliver 50bp cuts at each of its next three meetings. A further 10bp drop in inflation expectations than currently assumed would also lower fair value by an additional 20bp. Risks to bond yields therefore feel slightly more symmetric to us than a simple inspection of our fair value model would suggest.

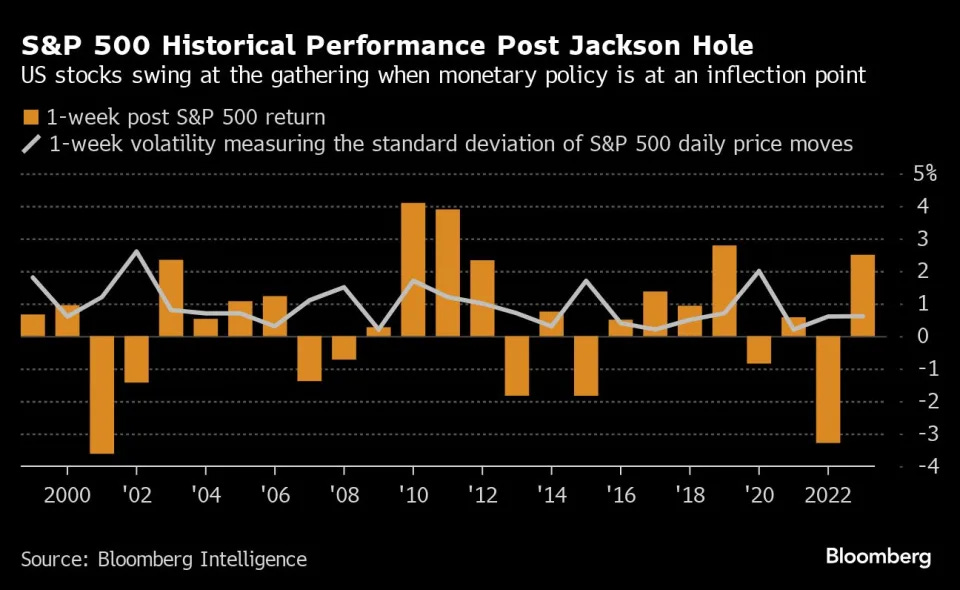

DATATREK: Jackson Hole “Drift”, Initial Claims, Fed Funds Odds

Topic #1: The “Jackson Hole Drift”. The Federal Reserve’s annual Jackson Hole Economic Policy Symposium is this week, running from August 22 – 24. Chair Powell will speak at 10 am East Coast Time on Friday morning, and markets will be looking for any hints regarding his thoughts on future monetary policy.

This got us to thinking about how equity markets have traded around prior Jackson Hole conferences. Despite its nominal purpose as a get together for central bankers and economists, the event has also long served as a chance for Fed Chairs to communicate during the summer hiatus of FOMC meetings. The committee does not usually meet in August, and Jackson Hole conveniently fills that gap.

The following table shows S&P 500 returns for the week leading up to a Fed Chair’s Jackson Hole speech, the week after the event, and the cumulative return over that 2-week period from 2010 through 2023. Fed Chairs don’t always attend, and we have noted those years.

Three thoughts on this data:

The S&P 500 has averaged a +0.9 percent return over the 2-week period around Jackson Hole since 2010, with returns weighted to the week after the meeting (+0.7 pct versus just +0.2 pct for the week before).

We consider 2022 an outlier year given the Fed’s aggressive monetary policy, so its -7.4 percent Jackson Hole “drift” is understandable in that context. Even then, Chair Powell’s “whatever is takes” speech surprised markets, with the S&P falling 5.5 percent in the week after the address. Exclude that year and average Jackson Hole returns since 2010 increase to 1.6 percent, with most of the move (1.1 points) still coming after the Chair’s comments.

Excluding 2022, the 2 worst years for US stock market returns around Jackson Hole weeks were when the then-current Fed Chair did not attend the conference (2013 and 2015, -1.4 and -4.2 pct). This speaks to the importance of the conference as a policy communication event. The average S&P 500 return in the 2 weeks around Jackson Hole excluding 2013, 2015, and 2022 is 2.3 percent, also skewed to the week after the Chair’s speech (1.6 points).

Takeaway: Market expectations for Fed rate cuts later this year are very high (more on this below), but Powell should be reassuring enough on the topic this Friday to see the typical “Jackson Hole Drift” higher over the next 2 weeks. Moreover, he knows markets are coming off a volatile few weeks and will therefore want to choose his words carefully. Finally, recent Initial Claims data suggests the US labor market is holding up pretty well, so he can also lean into a confident message about the American economy. Which brings us to our next point …

Topic #2: Last Thursday’s US Initial Claims for Unemployment Insurance report …

… Topic #3: Last week’s changes in the odds for Fed rate cuts later this year. The following CME FedWatch Tool (link below) chart shows the market-based probabilities for various Fed Funds rate scenarios just after the conclusion of the December 18th FOMC meeting. We have noted in red/green how these odds changed over the last week.

Takeaway: Last week, the odds of at least one 50 basis point cut in the next 4 months dropped from 75 to 59 percent. Much of that decline was due to Thursday’s better than expected Advanced Retail Sales (+1.0 percent versus expectations of +0.3 pct) and Initial Claims report, as discussed above. Even with these reassuring datapoints, however, Futures still give slightly better than 50:50 odds of at least one 50 basis point cut later this year. In good news for both Chair Powell ahead of his Friday speech and markets, Futures don’t think the September meeting will see that large a reduction in rates (odds of just 25 percent). The debate over 25 or 50 basis point cuts can wait until later this year…

DB Mapping Markets: Why was the turmoil so brief, and could it happen again?

Looking at markets, it's striking just how brief the recent turmoil was. In many respects, it's an even quicker version of what took place after SVB's collapse in March 2023, where volatility quickly spiked before subsiding again.

But, even as markets have stabilised, several of the fundamentals driving the sell-off haven't gone away. Data has been increasingly soft at a global level, falling inflation means that monetary policy is increasingly tight in real terms, geopolitical concerns are elevated, and we're heading into a tough period on a seasonal basis…

… Could this sell-off happen again? Although this has seemed like a brief episode that is fading into view, it's worth remembering that several of the catalysts for the sell-off are still in place:

1. Equity valuations are elevated by historical standards and positioning is overweight …

2. Economic data has been increasingly soft at a global level …

3. Monetary policy is becoming increasingly tight in real terms, with QT still going in the background…

4. We’re coming up to a tough period on a seasonal basis, and September has been a very bad month for markets in recent years…

5. Geopolitical tensions remain high right now …

…Conclusion Markets have just come through an eventful few weeks, but the volatility has quickly subsided, and the VIX index closed beneath 15 again on Friday.

However, even as the volatility has passed, many of the drivers of the sell-off haven't gone away. And it's worth noting that the moves were sparked by a jobs report where nonfarm payrolls were still up by +114k on the month, and not in contractionary territory. In addition, markets are pricing over 200bps of rate cuts from the Fed over the next 18 months, so it seems hard for much more than that to be priced unless the market prices even worse economic outcomes.

After the July jobs report released on August 2 triggered the “Sahm rule,” we raised our 12-month US recession probability from 15% to 25%. Now, we have moved it back down to 20% because the data released since August 2— including retail sales and jobless claims this week—shows no sign of recession.

Continued expansion would make the US look more similar to other G10 economies, where the Sahm rule has held less than 70% of the time. In the current cycle, several smaller economies—including Canada—have already seen sizable unemployment rate increases of 1pp+ without clearly falling into recession.

If the August jobs report released on September 6 looks reasonably good, we would probably cut our recession probability back to 15%, where it stood for almost a year before August 2.

We have become more confident in our forecast that the FOMC will cut the funds rate by just 25bp at its September 17-18 meeting, although another downside jobs surprise on September 6 could still trigger a 50bp move

MS US Equity Strategy: Weekly Warm-up: Stocks Rise on Better Macro Data; What's Next?

Equities continued to rally last week amid better than expected jobless claims and retail sales though the key barometer will be the August payrolls report. In the mean time, we skew toward quality and expect the week-to-week cadence of the data to dictate short-term market direction.

… As noted, last week brought "good" news on inflation with the PPI and CPI readings not exceeding consensus forecasts. While there were some conflicting signals in the data as usual, the conclusion is clear for most market participants—the Fed is expected to cut in September. At this point, the only debate is how much? Over the last year, market expectations around the Fed's rate path have been volatile. At the beginning of the year, there were ~7 cuts priced into the curve for 2024 which were then almost completely priced out of the market by April. Currently, we have close to 4 cuts priced into the curve for the rest of this year, but there has been quite a bit of movement in bond market pricing this month as to whether it will be a 25 or 50bp cut when the Fed begins. More recently, the rates market has sided with a 25bp cut post the better than expected growth and inflation data points last week.

MS: Sunday Start | What's Next in Global Macro: Derivative Thinking

All attention this week will be on Jackson Hole, where the conference has been aptly titled “Reassessing the Effectiveness and Transmission of Monetary Policy.” We expect Chair Powell to hold forth on the medium-term strategy for the Fed, particularly the fact that sustained disinflation means that it can focus on sustaining the expansion while still getting back to the 2% target. The FOMC has signaled the start of cutting, but Powell will likely note that even after cutting, policy will still be tight. Indeed, distinguishing between levels and changes may well be a theme. Economic activity is slowing, but it is not particularly weak. The job market has cooled, but even the 115k for July is not especially soft. Markets will have to decide what matters more – the level or the trend…

… Consumer spending – about 70% of the US economy – is another great example. US consumption spending soared well above its trend, so some reversion in levels back to fundamentals more aligned with income is in order. Tight monetary policy only reinforces that move. We think the process is under way, and last week's retail sales report suggests that the US consumer is alive and well.

Level versus trend is a critical distinction, and indeed markets will often trade the second derivative – that is, an acceleration or deceleration. I suspect Powell’s speech will at least implicitly highlight this distinction. The economy can slow from its unsustainably fast pace while still being healthy enough to escape recession. That distinction underpins our view that the Fed will cut by 25bp at successive meetings. Of course, we and the Fed could be wrong. State-level data imply that July payrolls were suppressed by a hurricane, but if August payrolls point to a slump, we expect a bigger rate cut. But that outcome would be a meaningful change in the trend.

As we emerge from the aftermath of the strong market reactions over the past weeks, we review the key risks across the world to pressure-test our baseline views.

As the dust settles following the market turmoil of the past couple of weeks, we huddled with our economists around the world to review the risks to our baseline call. The focus here is particularly outside of the US as we provided our US view in the Sunday Start that came out yesterday. We were lucky to be on the right side of the economic data of late, with our Japan economics team calling for a July hike and our US economics team maintaining a soft-landing view. Certainly, the non-farm payroll print was softer than our forecast, but the state-level data suggest it was a temporary hurricane effect, and the balance of the subsequent data suggest no slump is in the offing. But the respective journeys of the Yen, dollar, rates market, and credit markets prompt some pressure testing of views…

The data calendar today is so quiet even ECB President Lagarde does not appear to be speaking. The lack of economic data to guide investors might be troubling—but recent market swings were not based on rational economic analysis.

Politics dominates the near-term market landscape. US President Biden will open the Democratic National Convention in Chicago. The focus is less on Biden’s remarks and more on policy proposals from Vice-President Harris. Of course, markets do not necessarily assume campaign rhetoric will become policy reality (hence, investors’ reluctance to seriously price former US President Trump’s universal tariff proposals).

The issue of food retailers’ “price-gouging” (or profit-led inflation, in less emotive language) has been getting attention. US retailers’ profits-to-GDP ratio has risen from circa 14% before the pandemic to just under 22% today (wholesalers’ profit ratio remained around pre-pandemic levels, in contrast). Absolute price controls are generally regarded by economists as unhelpful. Enforcing competition and educating consumers can combat profit-led inflation.

The Federal Reserve’s summer camp for central bankers is at the end of the week, and we get minutes from the last Fed meeting mid-week. The summer camp is likely to be more of a focus. Fed President Daly was signaling a series of rate cuts are coming.

… Or will the Fed's talking heads favor swiftly cutting the federal funds rate (FFR) as inflation falls in order to loosen the restrictiveness of policy as measured by the real FFR (chart)? Might they hint at some concerns about the potential inflationary consequences of the next administration's policies as well as of unsettling geopolitical developments? Might they indicate that unwinding carry trades may limit their ability to cut interest rates quickly? If Fed officials confirm that they are likely to start cutting the FFR in September, might they signal a willingness to end quantitative tightening (QT) in the coming months?

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Global Bond Traders Are Seeking Protection From Inflation Threat

(Bloomberg) -- Just as bond traders grow more assured that inflation is finally under control, a camp of investors is quietly building up protection against the risk of a future spike in prices…

… Still, many investors think inflation gauges have fallen too far. Take the US five-year breakeven rate, the difference between inflation-linked and nominal yields of similar maturities and a proxy for the average rate of price rises over the period. It fell sharply in recent weeks as recession fears flared and is now trading around 2% for the first time since the start of 2021.

A near-term crunch point could come soon after the US presidential election should it result in a win for Republican Donald Trump. He is campaigning on a platform of tax cuts, tariff increases and immigration crackdowns — all of which are potentially inflationary.

Gareth Hill, a fund manager at Royal London Asset Management Ltd., has been adding US inflation exposure to his portfolios via five-year breakevens — essentially a bet that Treasury Inflation-Protected Securities (TIPS) will outperform five-year nominal bonds. Election aside, Hill still sees value in the trade, arguing that “the last mile in the battle against inflation is the hardest one.”

Bloomberg: Traders Need Fed’s Rate-Cut Signal to Keep Stocks Rallying

(Bloomberg) -- Wall Street is betting that Federal Reserve Chair Jerome Powell will confirm that interest-rate cuts are coming at the central bank’s annual confab in Jackson Hole, Wyoming. But as the debate shifts from “will they or won’t they?” to “how big will they go?” — stock traders may be left wanting.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (largest net short in 10s since Mid JAN record high…)

Investing.com: US recession risk easing, 'confident' Fed will cut by 25bps in Sept: Goldman Sachs

Goldman Sachs economists have revised their 12-month U.S. recession probability down from 25% to 20%, citing recent economic data that shows no signs of a downturn…

Sam Roi from TKer: The state of the American consumer in a single quote

Last week, we got such a perspective from Walmart CFO John David Rainey after the release of the company’s second quarter financial results. Via WSJ (emphasis added):

We continue to believe that customers are discerning, they are choiceful, they are focusing on essentials versus discretionary items, but we have not seen any incremental fraying of consumer health. … I wouldn’t say strength, but lack of weakness.

In other words, the American consumer isn’t spending as recklessly as they used to. But they aren’t falling apart.

… Walmart, America’s largest retailer, reported Q2 net sales that grew a healthy 4.8% year-over-year, fueled by 4.2% growth in U.S. same-store sales. Management even boosted its full year guidance, projecting 3.75% to 4.75% growth in fiscal 2025 (up from a range of 3.0% to 4.0%).

And this is not just a Walmart story.

According to national data released by the Census Bureau on Thursday, retail sales in July grew 2.7% year-over-year to a record $709.7 billion.

Retail sales are at record levels, but the growth trend has been plateauing. (Source: Census via FRED)

…finally, how the FOMC and it’s minions view capabilities of monetary policy …

… where lowering of rates then NOT to ease policy restriction but rather to only reduce restriction (relative TO neutral which, not for nuthin’, has no REAL definition, but just made up GUESStimates by Global Wall and ivory tower cognoscenti) … and from a REAL person perspective, the visual somewhat different …

My guess: Powell won't directly commit to September cut...but reiterate "data dependant" status.

Will give a slightly Dovish bias, but remain quite Balanced and Opaque....

Team 25, should get their wish....but not sure it's in September...

The 9 % Inflation Rate, has burned a scar into Mr Powell's Brain, that has not healed.....

But the markets are doing the Fed's work for it and if that continues the Fed will have to capitulate

and cut....

For now, I think Powell believes Time is on His Side....