After the shitshow of Soft Survey data on the Manufacturing sector last week, analysts are hoping for some heroics from the Services sector. Amid the collapse in 'hard' data, soft survey data remains the last great hope for saving Bidenomics (with all hopes on a big rebound in ISM from last month's plunge)...

… AND so it’s NOT in fact, the end of the world as we know it (great song, less of a great Global Wall narrative shape-shift but …) and nobody cared, news at eleven … meanwhile as the day unfolded right up to / thru market recap …

CalculatedRISK: Fed Q2 SLOOS Survey: Banks reported Tighter Standards and Weaker Demand for almost All Loan Types

ZH: Monday Massacre Brought To You By Kazuo's Carry-Chaos, Kamalanomics, & Jump's Crypto Dump

… The Treasury market was chaotic today (but you'd barely notice if you were checking close to close). Yields collapsed by almost 20bps intraday... twice... before squeezing back higher and ending pratically unchanged. The long-end ended up outperforming on the day (30Y -4bps, 2Y +1bps)...

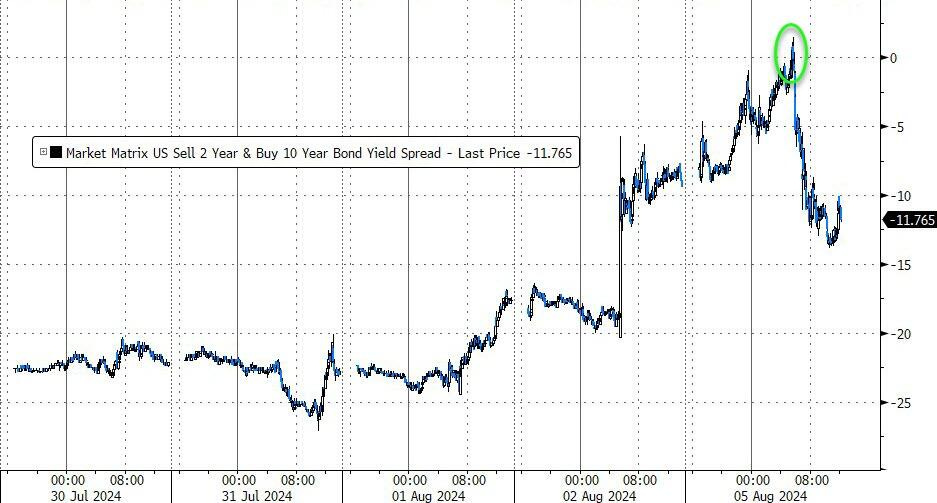

The yield curve (2s10s) briefly dis-inverted today for the first time since June 2022...

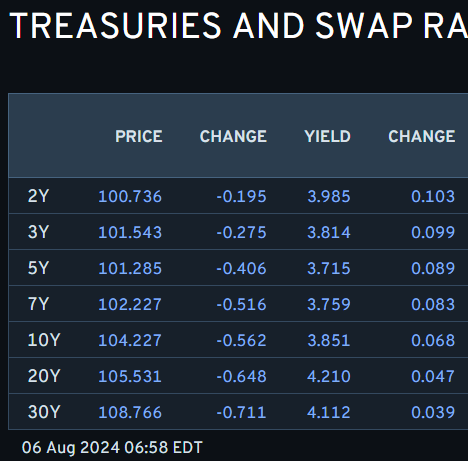

… AND … i’ll quit while I’m behind and head TO prices / yields snapshot as of 6:58a

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: APAC trade saw a reprieve from Monday's action, though this has faded in Europe … Fixed benchmarks spent the early morning under pressure but EGBs have lifted off lows following auctions/data; USTs remain pressured as Monday's dovish pricing eases from extremes … USTs holding just off 113-12 lows, which mark a new base for the week but markedly above Friday's 112-21 base. As such, market pricing has shifted to no longer entirely price in a 50bp cut in September, with the odds of that back down to circa. 75%.

Reuters Morning Bid: Rollercoaster markets, Nikkei rebounds 10% (VISUAL: VIX sees biggest 1d rise in history)

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: Is the US heading for recession? | Insights newsletter

Global Macro: US recession risk has risen but should stay contained, despite market worries. As the US economic slowdown has gathered momentum, and the BoJ brought an abrupt end to the yen carry trade last week with its surprise rate hike, global markets have entered much choppier waters. Equity markets have tumbled across advanced economies, and the VIX has shot to levels not seen since the onset of pandemic lockdowns in 2020. Against this backdrop, markets now price a much more aggressive rate cutting path by the Fed, with chatter of even an intermeeting rate cut. Are the fears over the US economy justified, and how likely is the Fed to follow through on market rate cut expectations? Moreover, what will all of this mean for Europe?

The ISM services PMI rebounded to 51.4 in July, returning to expansion territory, after plunging in June, supported by rebounds in the services employment, new orders, and business activity components. This suggests that the labor market may not cool as abruptly as feared following last Friday's July payroll report.

July's Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) showed readings similar to April's, with only a modest share of banks tightening lending standards and loan demand either unchanged or continuing to weaken, on net. In comparison to last year, lending standards eased for most categories.

BMO: ISM Services 51.4 July -- Solid Rebound from June

… Treasuries were rallying sharply this morning with the front-end leading the charge as there has been increased chatter about an intermeeting Fed cut. While we continue to see the bar for a cut before the September meeting as very high, we're sympathetic to investors' focus on the price action in equities as a potential trigger in the event the selloff significantly worsens. From here, we'll continue to watch the response in risk assets with a nod to the fact the ISM Services print has offered a moment of stability, if nothing else.

The market has sharply re-priced to reflect fears of a US growth slowdown.

The market’s pricing in of Fed rate cuts is now in line with what has been delivered on average over the past four recessions and is above the average seen over all recessions since 1973.

The USD typically strengthens while growth fears increase but before Fed cuts materialise, in contrast to the current weakening. While the price action is atypical, we think it is not unjustified.

… Figure 1 plots the average move in 3m T-bill yields during a recession (the recessions included are all NBER recessions since 1973 – so 1973, 1980, 1981, 1990, 2001, 2007, 2020), as well as the average DXY move.

… Figure 3 plots 3m T-bill yields versus 5y5y UST yields, for a very crude/approximate measure of how tight current policy is compared to market proxies of neutral. It is true that on this metric, policy appears a little tighter than in the past four recessions; but not meaningfully so…

BNP: Japan: Contextualizing the NKY’s second largest 1-day decline on record

KEY MESSAGES

The Nikkei 225’s second largest one-day decline on record (-12.4%) on Monday underscores the large portfolio liquidation pressure on Japanese equities as the bank sector has been the worst-performing sector in the past two days.

Three catalysts could provide some stability to Japanese equities near term, in our view: USDJPY, semiconductor stocks and domestic pensions.

We still prefer banks to autos in the medium term as BoJ governor Ueda acknowledged the potential for higher terminal interest rates in a press conference last week, while the auto sector is facing a multitude of headwinds.

… Fixed income was as equally wild as most equities yesterday as 2yr yields, for example, saw a 30bps range within a 4 hour period from late London lunchtime. During intraday trading, the 2yr yield briefly fell back -23.2bps, and the 10yr yield by -12.6bps. Off the back of this, the 2s10s curve briefly resteepened back to zero for the first time since July 2022. This was trimmed back over the course of the trading session, with 2yr and 10yr US yields closing +4.0bps higher and -0.2bps lower respectively. The 2s10s curve closed at -13.6bps, and actually flattened -4.2bps on the day after all the earlier savage steepening. Overnight, yields on 10yr USTs (+5.45bps) have continued to move higher, trading at 3.84%, while the 2yr yield is +3.9bps higher, trading at 3.96% as we go to print.

So yields are well off the lows of yesterday and the start of the turnaround seemed to coincide with comments from the Fed’s Goolsbee, who emphasised that last week’s jobs data was “not yet indicating recession”, and that the Fed “can wait for more data before (the) September meeting”. Following Goolsbee’s remarks, markets reversed some of their expectations for Fed rate cuts. The number of Fed cuts priced in by December was down by -2.1bps to 114bps by the close, having peaked as high as 138bps early in the US session. The 2024 Fed rate cut pricing has reversed a little more to 110bps overnight….

MS: US Economics: Some weak July data but we still expect a soft landing

Payrolls and manufacturing ISM were weak. We don’t think payrolls spells real weakening—could be weather, could be just noise.The Fed would need less than 100k in August payrolls to consider a 50bp cut. We survey recent indicators -- which are worrying and which are not…

… And the S&P manufacturing index casts some doubt on the ISM as it has been strengthening on net. ( Exhibit 6).

The services ISM index got attention in June for its decline and for weakness in its employment component. But the services ISM index rebounded to above 50 in July, and the employment component, at 51.1, rose to its highest level since last September. At little above 50, the levels of the index look consistent with slowing but not with a serious slump. And the ISM index has diverged from the S&P services measure, which did not show as much softness in June or July and has been trending up since 3Q last year. ( Exhibit 7 )

MS: US Banks: How Willing Is Your Bank to Pay Up for Deposits? July 2024

In line with commentary from 2Q24 earnings that deposit rates have stabilized, rates on new CD offers across all durations remained relatively unchanged in the month of July: During July the average highest rate and 1-12 month rates were both flat, and the highest 13-36 month rate increased 1 bp to 3.26%. Among the primarily online deposit gatherers (ALLY, AXP, COF, DFS, and SYF), the average highest CD rate increased 8 bps from 4.84% to 4.92%, the average online savings rate was flat at 4.56%.

The Japanese equity market is behaving with all the decorum and rationality of someone dancing the Hokey Cokey at a family wedding at two in the morning. Economic fundamentals are not driving equity prices—no economic data justified yesterday’s 12% plunge, nor today’s 10% rally.

The S&P 500 index is at early May levels. Fears of a negative wealth effect should be kept in perspective. For the overwhelming majority of US households, the family home is the most important asset and equities are something of an afterthought. The second quarter equity rally did not produce a positive wealth effect (savings rates were stable), so fears of the impact of the rally’s unwinding should be contained.

There are few economic data points today, but markets seem to be independent of real world economics. The Bank of Japan, the Japanese Ministry of Finance, and the Japanese financial regulator are reportedly meeting. It is hard to imagine what this will achieve—the Bank of Japan is very unlikely to take back its rate increase…

Wells Fargo: Service Sector Activity Returns to Expansion in July

Summary At a moment when global financial markets are selling off over concerns that the U.S. economy could be on thin ice, the ISM services index is a reminder that service-sector activity remains robust. The ISM Services Index rose back into expansion at 51.4 in July.

Bloomberg: Selloff's cruel summer looks more like 1998 than 2007 (Authers’ OpED)

But much will come down to whether appetite exists for a Fed Put. Is anyone too big to fail on the brink?

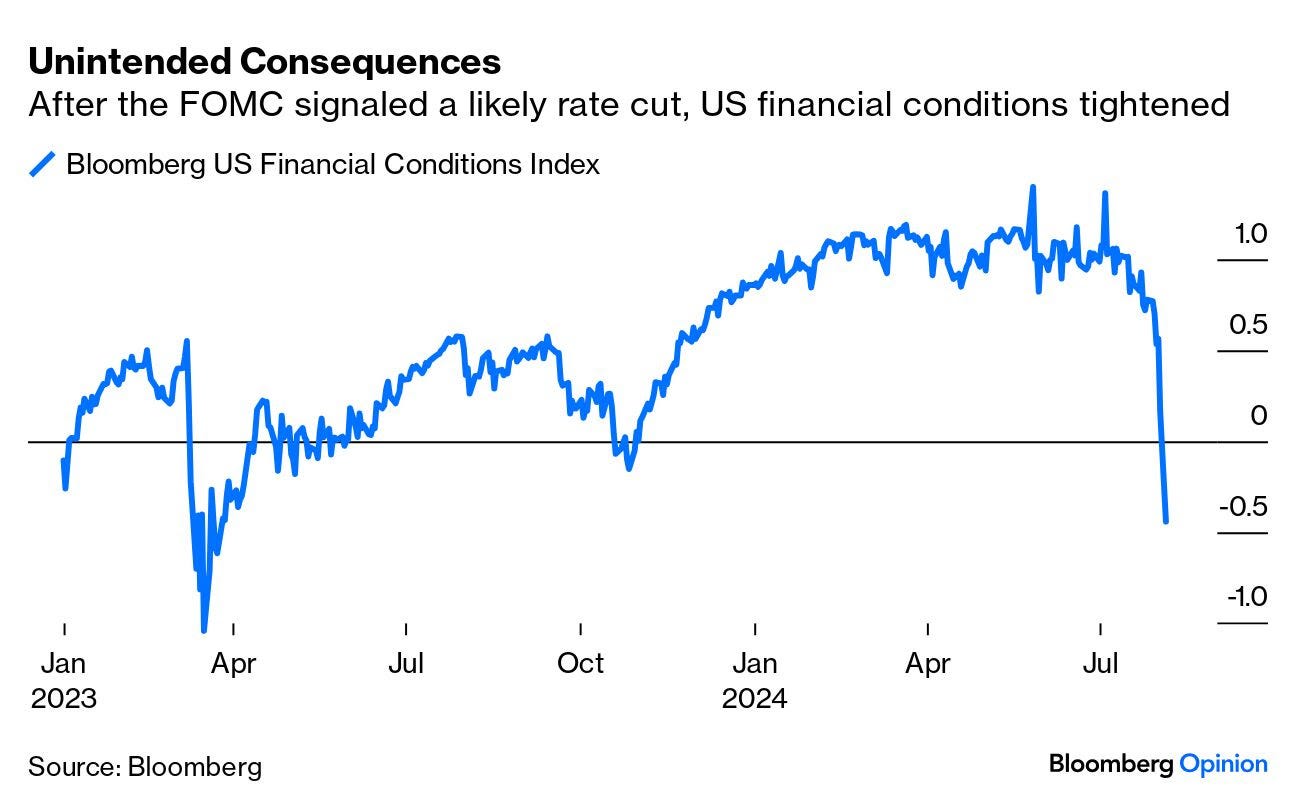

… Markets don’t move in a vacuum or merely respond to events. Instead, we should beware what George Soros calls reflexivity — the power of markets to create a new reality that we must all inhabit. Falling share prices make it harder for companies to raise funding. Investors feel poorer. Financial conditions tighten.Thus we have the irony that the Federal Reserve suggested last week that financial conditions were tight and that it might soon cut rates to make things easier — and since then, Blooomberg’s broad index of financial conditions has moved from easy to very tight. The shift is on a par with the sudden banking crisis that hit the US in the spring of 2023:

Bloomberg: The Fed Should Resist Placating Markets (El-Erian OpED)

The central bank needs to avoid being rushed into another policy mistake by making an emergency interest-rate cut.

FirstTrust: Monday Morning Outlook - The Lags are Over for Tighter Money

… Put it all together – decelerating inflation and decelerating growth, along with an abnormally slow rebound in M2 – and we have a strong case that the Federal Reserve has implemented tight money. In turn, given the lags between shifts in policy and its economic effects, the Fed now has room to shift to a monetary policy that is less tight…

…Instead, the Fed needs to start focusing on the money supply, particularly on M2. If the Fed cuts short-term rates but growth in the money supply remains weak because of tighter capital requirements on banks or because businesses and consumers expect even lower rates further ahead (which might lead them to temporary postpone economic activity) then it isn’t really making monetary policy less tight…

Hedgopia: Should Relief Rally Not Show Up On Time, Logical To Conclude This Selloff Is Different (funtertaining visuals … last one with S&P losing TLINE caught my eye)

… Several monthly indicators in particular have just begun to turn lower from overbought levels and can continue lower. Last Friday’s low just slightly breached horizontal support at 5320s, but was saved by close, as the index closed at 5347. Inability to defend 5320s will expose the index to another layer of support at 5260s. As I write this, futures are down 2.8 percent. If this sticks by close, then there is not much before the 200-day gets tested at 5008. A rising trendline from last October has already been breached (Chart 5)…

ING: Fed to step on the gas, but market pricing looks aggressive

The poor July jobs report has led to market fears of impending recession and the need for an aggressive Federal Reserve response. Yet the latest ISM services report suggests the situation looks ok with the economy growing, adding jobs and with inflation above target. We don't expect an inter-meeting Fed rate cut unless systemmic risk emerges

Following a weak jobs report, UST yields briefly hit 3.65% starting the new week, the lowest since the second quarter of 2023. The 10Y yield also dipped to 3.66%, causing a brief dis-inversion of the 2s10s curve. Despite lingering market concerns, we see no need for emergency Fed cuts, but the 50bp narrative may stick

During this selloff, bonds are behaving as expected.Recent movements in the rate market have pushed U.S. Treasury yields lower, with the 2-year and 10-year yields closer to parity with both trading below 3.7%. The market has fully priced in the odds of two 0.50% rate cuts over the next two Fed meetings and a subsequent 0.25% rate cut in December.

Long term, byDecember 2025, the market is anticipating over 2.5% in total rate cuts, which aligns with expectations for recessionary adjustments.

Despite the potential for a slight overreach in rate declines, high-quality bonds have effectively served their traditional role as portfolio diversifiers during market volatility. We would suggest continued emphasis on high-quality bonds in investor portfolios, as they offer the optionality of further portfolio protection in these uncertain times — something cash does not offer.

Technical Analysis Offers Some Key Potential Support Levels

Now that the S&P 500 Index has breached both its 20-day and 50-day moving averages (dma), key support levels to watch are 5,254 (March highs), 5,227 (a retracement level), and 5,011 (200-dma). Below the 200-dma, the next support level is at April’s lows at 4,954.

Currently, momentum indicators are bearish but not deeply oversold, suggesting there may still be some additional downside potential. This morning, the Relative Strength Index (RSI) touched oversold levels but has experienced a bounce midday.

Despite current volatility, the broader market's long-term uptrend remains intact, and most breadth metrics show minimal damage. Over two-thirds of S&P 500 stocks are still above their 200-dma. The market was also quite overbought as August began, particularly in the tech sector, where the correction has been more pronounced.

The extreme levels of the VIX measure of implied volatility reached this morning — at one point over 60 — have historically been associated with market capitulation. But remember bottoming is a process and usually takes some time. We’re following the charts closely.

Remember, corrections of 10% or more are a normal and healthy part of any bull market. On average, stocks correct 10% or more once per year — even in positive years. But that doesn’t mean the bull market is over.

Uptrend Still Intact as Stocks Near Oversold Levels

Source: LPL Research, Bloomberg 08/05/24 Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Bottom Line

Equities are nearing an attractive entry point, with the S&P 500 down about 8% from its July high (and the Nasdaq down 12%) as of 12:00 p.m. ET Monday. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities, while actively monitoring signs the bottoming process is playing out. We don’t think it’s quite time to buy this dip yet. We suggest staying invested, be patient, and most importantly, don’t panic.

In terms of potential catalysts for a stock market turnaround, consider the following:

A signal from the Fed that they will be more aggressive with rate cuts.

Evidence that the economy is holding up okay rather than falling off a cliff. Today’s ISM services data was a good start.

Some additional unwinding of trades by institutions that were caught off guard by these big moves. These include carry trades involving the yen currency and overly bullish and leveraged quantitative traders.

A refocus on corporate fundamentals, including the Magnificent Seven’s expected earnings growth near 30% and resilient overall estimates (even as some companies warn about consumer spending pressures).

Corporate buybacks could pick up now that most companies have reported results for the second quarter.

A successful test of the 200-dma on the S&P 500, currently at around 5,010 but rising, could encourage big market players to step in.

at RoyLMattox

$Vix printed 3rd highest level today since 1990. The Great Financial Crisis in 2008 and the 2020 Covid Pandemic are the only 2 times higher in 34 years. This is indeed how bottoms form but as always bottoms are processes.

Never before in my history studying the Federal Reserve (Fed) has the Fed’s policy come into question immediately following the Fed decision. Jerome Powell was asked at his press conference whether a 50-basis point (bp) rate cut was possible at the next meeting, and he was steadfast that this bold action was not currently contemplated. It should be—and it should be done without delay.

am now calling for more. The Fed should make an immediate 75 bp inter-meeting cut and follow that up with a 75 bp cut at the September meeting. The reasons are simple. The Fed says the long-term Fed Funds rate should be 2.8%. There are two variables that they look at to set the funds rate: unemployment and inflation. We have already blown beyond the Fed’s 4.2% long-term unemployment rate, and we are within 50 bps of the Fed’s inflation target. Why hasn’t the Fed lowered its very restricted 5.33% Funds rate at all! The funds rate should be 4% or less; at least….

WolfST: Despite the Recession-Emergency-Rate-Cut Buffoonery, the Services Sector Expands Strongly on Growth in New Orders & Employment. Inflation Pressures

What a bummer. Services are two-thirds of the economy; as long as they’re firm, the economy will plug along just fine, even as manufacturing stalled.

and from worst day to best day, i’ll present without further comment, the following tweet …

at TrendSpider

BREAKING: Japan's Nikkei Index triggers another circuit breaker, this time to the upside

Doin' the Hokey Cokey dats a good one! I declare team Pump the Brakes! Team Cuts became Team Big Fat Cuts or Team Gushing Gunshot wound. 150 bps between now & Sept FOMC is akin to the Fed's emergency Covid Cuts of 2020. I wonder who's crying UNCLE on Wall St....

{kind=link}

Doin' the Hokey Cokey dats a good one! I declare team Pump the Brakes! Team Cuts became Team Big Fat Cuts or Team Gushing Gunshot wound. 150 bps between now & Sept FOMC is akin to the Fed's emergency Covid Cuts of 2020. I wonder who's crying UNCLE on Wall St....