… and while the move is, in and of itself a bullish, ~30bps retreat from the recent highs, i’d note that as the move occurred, momentum has now moved from overSOLD to now overBOUGHT, which doesn’t suggest one buy here / now. Patience, perhaps, as time at a price can / will work off this overbought daily momentum …

Now in as far as WHY / how this price action has occurred, well, some news …

ZH: Job Openings Unexpectedly Crater By More Than 500K As Wheels Start To Fall Off The Job Market

Openings. CRATER. Jobs (ADP) day today and then again FRIDAY … to say much more here and now, would seem to be offering some idea that I’ve got a clue as to the whatever next.

I don’t.

I will then move right along … here is a snapshot OF USTs as of 642a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: USD lower and Bonds gain ahead of ISM Services, NQ hit as China mulls a probe into AAPL, GOOGL -7% post-earnings … Bonds bid as AAPL reports hit sentiment and into Bessent's first Quarterly Refunding … A morning of gains for USTs, upside was initially modest in nature and tempered by hawkish developments out of Japan via the largest wage data and remarks from former official Hayakawa around potentially hiking twice more in 2025. Further upside in the complex continued in the European session, with some impetus potentially stemming from reports that China could investigate Apple. Specifically, USTs lifted to a 109-15 session high over the course of 20-minutes. Ahead, US ADP National Employment, ISM Services, Quarterly Refunding Announcement and a slew of Fed speakers.

… before moving on TO narrative creators out there on Global Wall — views you can use, etc — I would like to take a moment and make sure one / all know of another of MY favorite ‘Stacks out there for daily macro morning recon as well as Global Wall insights … I don’t do this all the time (any / all you Yield HUNTERS know this) and so … HERE is a link to a blog / site …

… and you’ll note a metric TON of information and I’d specifically like to note / mention this one link to click here …

I’m always and forever about trying to save YOU time and effort and 1000s of hours is certainly just that. My humble effort has been in effort to highlight things below which institutional FI desks are talking about. In real time … and in some cases, paying for with hard or soft dollars.

I believe there’s value here and if you are one of the 30k subs, then you know this already. IF, by chance, you are not YET one of the 30k subs, well … you know what to do…

You’ll see this on MY ‘recommended list’ NOW … alrighty THEN … Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Ever hear that saying … different day, same sh!t? So too has this shop from across the pond …

BARCAP: December JOLTS: Different day, similar data

Job openings declined in December after growing in the prior two months, continuing a string of inconsistent readings. Hiring and separation rates held steady, showing some stabilization in labor market turnover. We see little in today's data to alter the course of Fed policy.

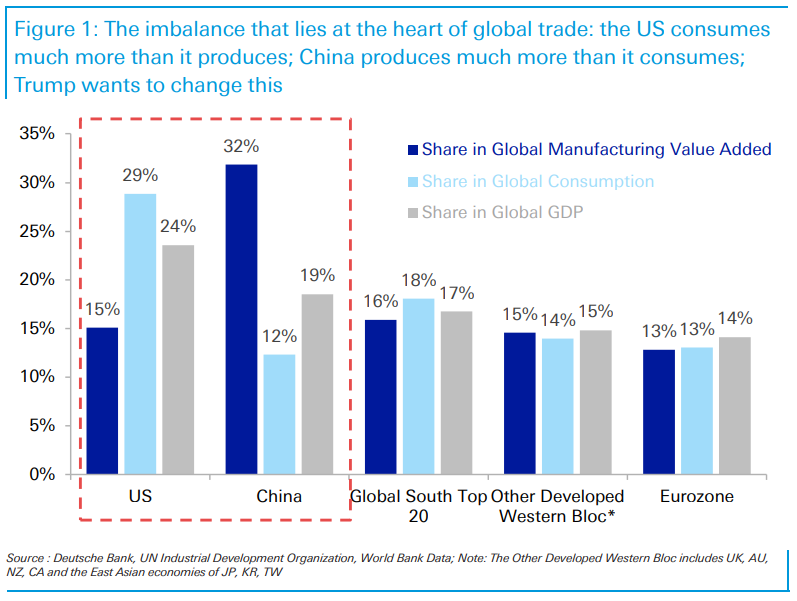

They say every opinion is created equally. They ALSO say that some opinions are more equal than others and along those lines, one mans view … Here’s a chart that is getting passed around (ZH and BBG specifically) quite a bit …

… While the US accounts for 29% of global consumption, it produces only 15% of the world's goods. Meanwhile, China accounts for 32% of global manufacturing but just 12% of consumption. Simplifying it, this imbalance shows up in a USD1tn Chinese trade surplus and a nearly equivalent US deficit.

China's economic development in recent years, instead of moving it towards a consumer-oriented economy, has moved in the direction of a more advanced manufacturing economy. This is now causing consternation in the West, with China making strides in many high-value added capital goods. While the US is still the second-largest goods producer, it has less than half of China's global share, with many US allies also seeing significant drops in their manufacturing share over the past 30 years. This may now have gone too far. Access to cheaper goods is no longer a good “trade” for the US given the loss of economic security over production supply chains and technologies to a competing power…

About that concept whereby supply creates its own demand …

We’ll see Wednesday whether Scott Bessent chooses to make a statement through material actions or words as his new department unveils the latest re-funding decision(s). The baseline view is for no surprises. If there are surprises, it's more likely to be negative for Treasuries than positive. For that reason, the smart money is for him not to rock the boat

… The key number of look for over the wires is $125bn for the upcoming 3yr, 10yr and 30yr auctions. Get that and we're on a similar track versus expectations. And the big numbers beyond that are $954bn in Coupons and $139bn in TIPS and FRNs …

When the facts change I change, what do you do, sir … bla bla blah … anytime Global Wall UPDATES A CALL, you pause and revel in the glory of the goal posts movin’ …

MS: Federal Reserve Monitor Tariff Uncertainty Raises the Hurdle for Fed Cuts

Tariffs on Canada and Mexico have been paused for a month, while 10% incremental tariffs on China took effect today. Onagain-off-again tariff uncertainty should raise the hurdle for Fed cuts, and we now tentatively look for only one rate cut this year in June.

Key Takeaways

Previously, we looked for 25bp cuts in March and June on the assumption that slow implementation of tariffs allowed inflation to come down through mid-year.

Imposing tariffs more quickly than we assumed would likely mean disinflation halts at a higher pace of inflation, blocking any near-term path to cuts.

Even if tariffs are avoided, we think their potential keeps uncertainty about PCE inflation elevated and keeps risks to PCE inflation tilted to the upside.

We now only look for one rate cut this year in June. The path for monetary policy in 2025 remains highly uncertain.

Lack of pressures in money markets make it unlikely the Fed will adjust its balance sheet policy just yet. We adjust our baseline view for QT to end to June.

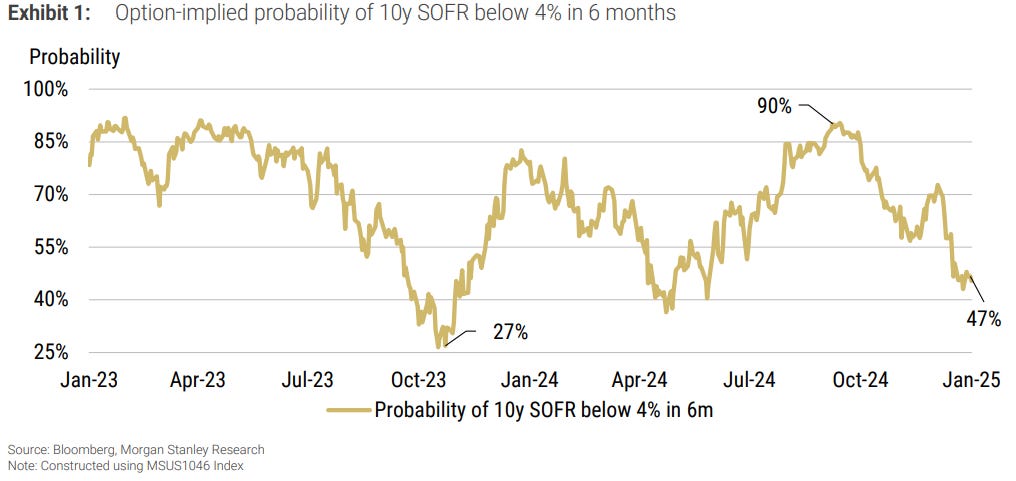

This note and a visual caught my eye …

MS: US Rates Strategy: Introducing Swaption-Implied Rate Distribution Probabilities

We calculate the market-implied probabilities of SOFR rates across the curve out to 12-month horizons. The results are available via 120 Bloomberg tickers. Our tests show that they provide information beyond widely-used rates and options data.

…A shiny new toy We introduce Bloomberg tickers to answer questions such as What is the market-implied probability of the 5-year term SOFR rate ending below 3.00% in 12 months' time? The series are daily and go back to January 2023.

To illustrate, Exhibit 1 displays the probability of 10y SOFR ending below 4% in 6 months (the MSUS1046 Index on Bloomberg). As of this writing, our models estimate the probability at ~47%, i.e., the market is pricing the outcome of 10y SOFR below 4% in July 2026 at roughly a coin toss.

Small but impactful? A short and thoughtful note …

The US postal service has stopped receiving parcels from mainland China and Hong Kong after US President Trump taxed buyers of goods from mainland China worth less than USD 800. Meanwhile, restaurants are surcharging egg-eaters. These are trivial issues, but they affect economic perceptions. Small parcels make up less than 5% of mainland China’s exports to the US, but individuals either do not receive those parcels or abruptly learn that tariffs are paid by consumers, not exporters. Egg prices were a key political issue, and some consumers (wrongly) use them as a measure of wider economic wellbeing.

Trivial issues can affect economic perceptions. The question for investors is whether perceptions then affect economic reality. Consumers had negative perceptions under US President Biden, but were better off in reality which kept them spending and supported the economy. The persistence of that perception-reality divorce matters to the economic outlook…

Job openings fall to 7.60 million in December Job openings fell 556K to 7.60 million in December, below consensus (8.00 million), leaving the series at the lower end of the 2024 range. We expect that the general direction of travel for job openings is a bumpy path downward, as it has been since early 2022 — but emphasis on the word "bumpy," as today's report was preceded by two back-to-back increases. The decline in December left the level down 1.29 million from twelve months prior…

…Also of note in the report today, the total industry quit rate remained at 2.0%. The series remains well below the 3% rate seen at recent peaks in 2022 and broadly consistent with mid-2010s levels, suggesting workers are still somewhat hesitant to voluntarily separate. As we have said in the past, while headline job openings look strong relative to the post-GFC expansion, the internals of the report do not look as strong…

This next note is near and dear to all waiting and watching this coming Sunday’s BIG game …

WELLS FARGO: The Economics of Super Bowl LIX Philadelphia Looks to Dethrone Kansas City

Summary Eagles vs. Chiefs in SBLVII Redux The Philadelphia Eagles will take on the Kansas City Chiefs in the Super Bowl this Sunday. You aren't experiencing déjà vu; the two teams last met in the league championship game two years ago in 2023. The Eagles will seek to avenge the loss with a new offensive weapon and a revamped defense loaded with young talent. The Philadelphia economy has also been flying high as of late, with the metro economy boasting low unemployment and solid job growth. Meanwhile, the Chiefs are aiming for their third straight championship, which would make them the first NFL team to achieve such a feat. The Chiefs franchise turnaround over the past decade echoes an economic renaissance in the Kansas City economy, which is now outperforming many of its Midwestern peers.

Summary A lot has happened since President Trump took office for his second term. In this report, we examine a few of the key takeaways from President Trump's first few weeks in office, including why the European Union could be Trump's next tariff target and why Trump has less leverage over China this time than during the first trade war. Tariffs and associated uncertainties should be consistent with a stronger U.S. dollar, although we acknowledge that “tariff fatigue” may set in and become less supportive of the greenback over time.

Google-parent Alphabet’s stock sank 7% after the closing bell today following its Q1 earnings report. That was partly because the company announced much higher 2025 capital expenditures than analysts anticipated. After spending $14.28 billion on CapEx in Q4-2024 (above the consensus estimate of $13.26 billion), Alphabet will spend $75 billion on CapEx during 2025, said CEO Sundar Pichai, mostly on building out its AI-related businesses. That's 29% more than the $59 billion expected by analysts. The company is clearly signaling that it disputes claims by Chinese AI lab DeepSeek that its AI is much cheaper and performs just as well as comparable US software programs. Microsoft is still aiming to spend $80 billion on AI infrastructure this year.

The initial reaction to Alphabet's earnings is similar to investors' flinch on the DeepSeek news just last week. Many have become skeptical that the returns on AI will justify big tech companies' massive outlays.

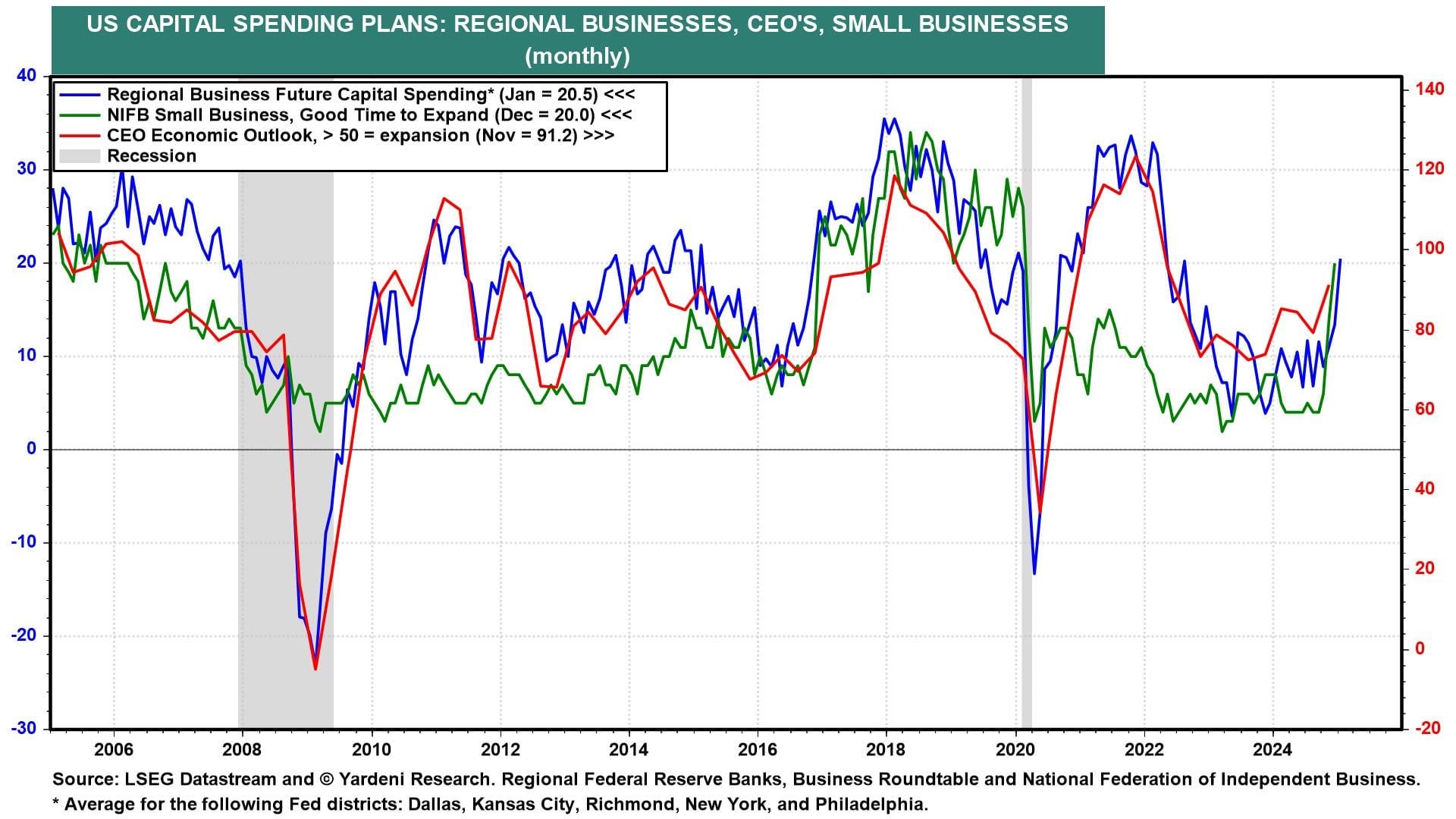

In any event, since the presidential election, small, medium, and large US enterprises alike have been saying they plan to expand their capacity sharply (chart). We expect they will also boost both productivity and employment. Animal spirits are back.

Today's economic data suggest the labor market is finding a balance at full employment, which supports our optimism around economic growth…

… And from the Global Wall Street inbox TO the WWW … a few curated links …

First up from The Terminal, an update on POSITIONS …

BLOOMBERG: Traders Turn More Neutral on US Bonds as Tariffs Cloud Outlook

Drop in US 2-year futures wagers is biggest since November

JPMorgan survey shows sharp pullback in bullish positions

Bond traders exited wagers in futures and cash Treasuries in the past week, turning more neutral as brinkmanship around tariffs clouded the outlook for the economy and the Federal Reserve and threatened to boost turbulence.

In Treasuries futures, traders unwound positions across shorter maturities on Monday by the most since November as the looming kickoff of President Donald Trump’s levies roiled markets. Meanwhile, investors in cash Treasuries have pulled back sharply from the biggest net long stance in almost 15 years, JPMorgan Chase & Co.’s latest client survey shows.

The start of this week showed the risk of carrying stretched positions around tariff deadlines. As traders braced for US levies to take effect Tuesday, short-dated Treasury yields surged and rates on longer maturities sank, signaling that investors were worried the levies would fuel inflation and slow the economy. Much of that move then reversed as the president agreed to pause tariffs on Mexico and Canada.

“You have to be super careful about whatever your story of the economy is — you’ve got to be careful about actually putting money to work behind it,” said Ed Al-Hussainy, a rates strategist at Columbia Threadneedle Investment. “A lot of people have become much more neutral on duration and not wanting to take that volatility.”

All the developments around tariffs left traders hedging various scenarios linked to the next Fed policy meeting, in March. In options linked to the Secured Overnight Financing Rate, which closely tracks the central bank’s policy path, Monday’s action was dominated by a mix of dovish and hawkish hedging for the March 19 rate announcement.

Swaps rates are currently pricing in just three basis points of easing into the meeting, or a bit more than a 10% chance of a cut, mirroring policymakers’ recent signals that they’re not in a rush to cut rates again as they monitor the policy mix of the new administration. However, elevated activity around the April SOFR options contracts signals that traders see the potential for the market outlook to shift in the coming weeks…

The St. Louis Fed Financial Stress Index has declined to -0.98, the lowest level this market stress index has seen in over 17 years.

Here’s the chart:

(right-click and open image in new tab to zoom in)

Let's break down what the chart shows:

The blue line represents the price of the S&P 500 index.

The greenand redline represent the St. Louis Fed Financial Stress Index (This data set has been inverted). When the line is green, it indicates that financial market stress is lower than normal. Conversely, when the line is red, it indicates that financial market stress is higher than normal.

The gray line represents the zero line for the St. Louis Fed Financial Stress Index, indicating normal financial market conditions.

The Takeaway: The St. Louis Fed Financial Stress Index measures financial stress in markets and is published by the Federal Reserve Bank of St. Louis. This index is constructed from 18 weekly data series: seven interest rate series, six yield spreads, and five other indicators. Each of these components provides insights into different aspects of financial stress.

The index is currently at its lowest level of market stress observed in the past 17 years. It has remained above the zero line for 96 consecutive weeks. During this period, the S&P 500 has experienced a gain of over 57%.

This is typical behavior of bull markets.

So, turn your attention to what the market data is actually telling us and not what they are saying on the mainstream financial media.

Are you stressed here?

The Wolf on JOLTS …

WOLFST: Underlying Job Market Dynamics Retighten as Fed Moves any Rate Cuts into Distance amid Accelerating Inflation

The low point was in September, which had spooked the Fed. But that’s over.

{kind=link}

Great article...

Is it really the fear of Tariff Effects that are driving the Bond Buyers ???

4.41% on the 10 year.....Wow !!!