while WE slept: ; "CAPU - At Recessionary Levels", WDL record low, a rising UR ... #HIMCO remains BULLISH bonds; 'all tenant repeat rent (ATRR) supports this

… readthru is questionable nowadays with DJT2.0 making waves at Davos…

CNBC: Treasury yields dip as investors consider Trump’s latest comments

U.S. Treasury yields dipped on Friday as investors reacted to President Donald Trump’s latest comments and anticipated further economic data.

At 4:30 a.m. ET, The 10-year Treasury yield fell by more than one basis point to 4.6235%. The 2-year Treasury yield slipped by more than two basis points to 4.2612%.

One basis point is equal to 0.01% and yields and prices move in opposite directions.

Investors watched as Trump addressed global leaders at the World Economic Forum in Davos, Switzerland, via video on Thursday. The newly inaugurated president took a swipe at the Federal Reserve regarding interest rates.

“I’ll demand that interest rates drop immediately,” Trump said. “And likewise, they should be dropping all over the world. Interest rates should follow us all over.”

Those comments come ahead of the Federal Open Market Committee meeting on Jan. 28-29, where interest rate decisions will be made. Markets are pricing in an almost 0% chance that the Fed will lower interest rates at its next meeting, per the CME Group data…

Truthfully, though, this AND BOJs rate hike o/n …

BBG: Japan Hikes Rates, Solidifying Exit From Rock-Bottom Borrowing Costs

(Bloomberg) -- The Bank of Japan raised its key policy rate Friday to the highest level since 2008 and took a more bullish view on the strength of inflation, fueling expectations for more rate hikes and supporting the yen…

… don’t matter as much to ME (or markets, frankly, as they are aggressively UNCH) and today’s the day … Woke up to commentary on TV ‘bout this note — the latest from Dr. Lacy HUNT of HIMCO.

Agree or NOT (and I always find it hard to disagree with him), feast your eyes on his latest (and yes, still quit BULLISH BONDS) note HERE …

The Global Capacity Glut Factories across the world are growing increasingly idle. Global industrial capacity utilization (CAPU) has fallen significantly, and a rising unemployment rate has followed suit, signaling that the available factors of production globally are progressively more redundant. The reason this is relevant is that since 1990, this thirty-four year correlation is consistent with the U.S. experience where data has been available for seven decades. As such, CAPU appears to be the dominant supply-side variable in determining inflation in the United States, China, Japan, U.K. and the EU.

… CAPU - At Recessionary Levels In the United States, CAPU has plummeted to levels lower than at the start of all of the cyclical recessions since 1967 (Chart 1). This vividly reflects a significant underutilization of resources, a circumstance which has historically led to moderating economic growth. Based on nearly complete fourth quarter 2024 data, the U.S. CAPU is estimated to have been 76.9%, a significant 3.2 percentage points lower than the post-1967 average and 6 percentage points below the historical level of 82.9%, which is the average entry level for the cyclical recessions. This surplus capacity reflects an irregular cyclical decline in industrial production from the fall of 2022…

… Inflation and Bond Yields Historically, on an annual basis, there has been a high correlation between the thirty-year Treasury bond yield and the inflation rate. That relationship did not hold in the past two years when the long bond yields rose even though the inflation rate moved downward. Despite this recent divergence, inflation and the long bond yield moved in the same direction for 71% of the years since 1954, when Treasury bond yields started trading freely. Historically, such divergences have been brief.

The previously discussed fundamental determinants of inflation indicate the prospects for slower price increases are even more significant than in any year since the late 1990s. In addition to the growing factory capacity glut and rising UR, the percent decline in modernized world dollar liquidity (WDL) reached another record low in the fourth quarter. The accelerating decline in WDL will intensify the liquidity/money squeeze domestically and globally. We estimate the trend adjusted real M2 declined further in the fourth quarter. Since the Fed's first reduction in the policy rate in September, critical consumer and small business borrowing rates have remained unchanged or increased. Such considerations argue that lower inflation will lead to a surprising drop in thirty-year Treasury bond yields in 2025.

newsquawk US Market Open: DXY pressured by Trump remarks, EZ PMIs lift the EUR, BoJ hike as expected … USTs a little firmer, Bunds pressured by EZ PMIs and BoJ Governor Ueda spurs JGB action .. USTs are moving in tandem with JGBs, Bunds and Gilts thus far. However, USTs remain just about in the green at the low end of a 108-09+ to 108-19+ band. US Flash PMIs due later.

Reuters Morning Bid: Dollar swoons as BOJ hikes, euro zone grows, yuan relieved

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

On CLAIMS (NFP survey week) hitting before DJT h’lines …

BMO: IJC Rise to 6-week High of 223k, Continuing Claims Disappoint; UST Bounce

Initial Jobless Claims printed at a 6-week high of 223k in the week of Jan. 18 (NFP survey week). This was 3k above the 220k consensus, and a 6k increase from the prior week's 217k. As a result, the 4-week moving-average ticked up to 213.5k vs. 212.75k prior. Continuing Claims jumped to 1899k in the week of January 11th -- the highest in over 3 years. This was 33k higher than the 1866k consensus, and a 46k gain from the prior week's 1853k.

Before the data, Treasuries were modestly weaker on solid volumes and 10-year yields reached a new, post-inauguration high of 4.646%. Since the headlines, Treasuries have bounced off the session lows; albeit 10-year yields remain slightly higher on the day. From here, attention will shift toward Trump's speech at the World Economic Forum (11am EST) for any fresh insight on the President’s tariff agenda.

We expect the FOMC to keep rates on hold next week, with a largely unchanged statement. The press conference will likely see an effort to retain optionality amid continued policy uncertainty.

We view current US economic data as signaling little urgency to ease further, with caution underpinned by doubt about the policy rate’s neutral level as well as inflation risks from Trump administration tariff and immigration policies.

Fed Chair Powell will probably be asked about the tail risk of rate hikes at the press conference. We expect him to reply cautiously by indicating they are less likely, but could come into view if needed to secure a soft landing for inflation and growth.

… The second of the above concerns – an excessively restrictive policy stance – now seems like less of a worry, owing to an increasingly widespread belief that the neutral interest rate has risen sharply since 2020. Looking across a range of models, our estimate of the nominal neutral rate is now 3.75%, which suggests policy is merely slightly restrictive and only a few cuts remain to reach a neutral stance. While policymakers recorded a much lower estimate in the December SEP, the frequency with which they express uncertainty about the neutral rate suggests they are taking this estimate with a large grain of salt.

Why the neutral rate has risen so significantly since the pandemic isn’t especially clear…

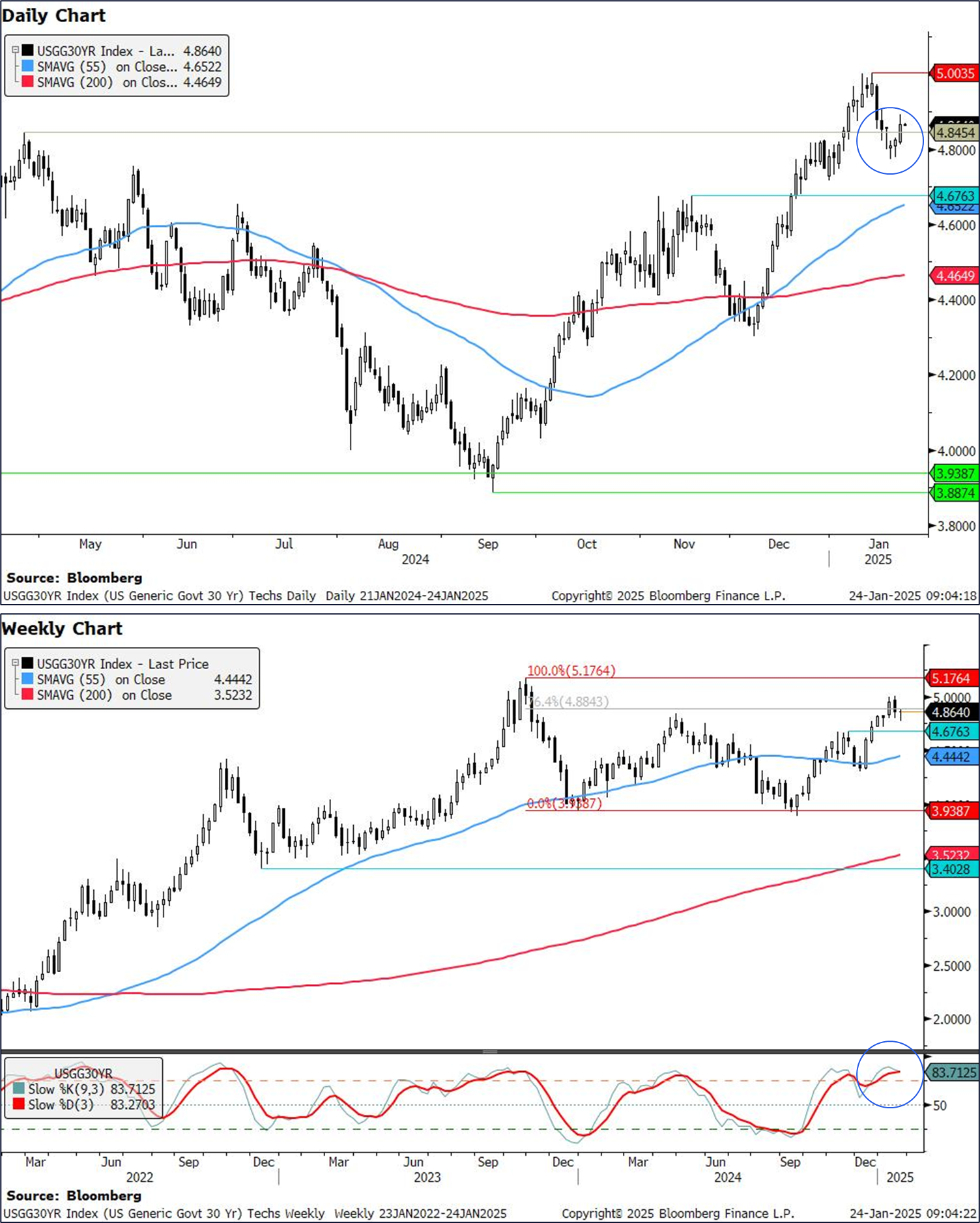

Interrupting FOMC precaps to bring you some techAmentals from best in that biz …

Short-term, daily indicators in US 5y, 10y, and 30y yields implies we could see higher yields. However, weekly momentum continues to suggest trend exhaustion. We detail these in our note below. As a summary:

US 2y yields: Strong resistance at 4.37% (55w MA). Triple momentum divergence in weekly charts suggests trend exhaustion. Short term, we see support at 4.20% (Jan low)

US 5y yields: Daily morning star formation off support at 4.31% suggests we could see higher yields short term. Resistance at 4.62-4.65% (Jan 2025 high, May 29th high).

US 10y yields: Look likely to hold in a short term range between 4.50% (July 2024 high, November 2024 high and psychological level) and 4.81% (Jan 2025 high).

US 30y yields: Two hammer candlesticks on the daily chart suggests we could see higher yields in the short term. Resistance is at 5.00% (psychological level, Jan high), Support is likely at 4.65-4.67% (55d MA, November high).

… as was widely expected the BoJ have raised rates by 25bps this morning to 0.5%, the first since July when their unexpected hike seemed to kick start a huge but brief global sell-off. This follows CPI ex fresh food coming in at 3%, also inline with expectation but the first time since August 2023 that this measure had hit 3%. All other measures were inline. The BoJ have upgraded their inflation forecasts with the hike which is a bit hawkish but have also cited many uncertainties concerning the outlook. Much will depend on where the emphasis is in Ueda's press conference that starts just before this will hit inboxes…

… Trump was speaking virtually before the World Economic Forum’s meeting at Davos, where remarks covered a lot of ground. Aside from the oil comments, a big one from a market perspective was “I’ll demand that interest rates drop immediately”. The Fed independence angle got further attention after the US close, as Trump questioned the Fed Chair’s decision making on interest rates in comments to reporters, saying “I think I know interest rates much better than they do, and I think I know it certainly much better than the one who’s primarily in charge of making that decision” and adding that he planned to speak to the Fed Chair “at the right time”. Otherwise, Trump said he wanted to cut corporate taxes further, saying that “we’re going to bring it down from 21 to 15% if there’s a big if, if you make your product in the US”. And there were also critical remarks towards the EU, saying that “From the standpoint of America, the EU treats us very, very unfairly, very badly” and denouncing EU cases against US tech giants as “a form of taxation”.

With oil prices moving lower, that added some growing confidence that the Fed would be cutting rates this year. For instance, the amount of cuts priced in by the December meeting inched up +0.9bps on the day to 40bps. That saw 2yr Treasury yields fall also by -0.9bps on the day to 4.29%, having been on track to closer higher before Trump’s remarks. However, long-end yields weren’t affected as much, with the 10yr yield ticking up +3.3bps to 4.64%, which in turn led to the sharpest daily steeping of the 2s10s curve so far this year …

Same German shop with (dis)INFLATION OPTIMISM …

DB: Data DBrief: ATRR gives reasons for cautious optimism

Yesterday’s Q4 All Tenant Repeat Rent (ATRR) data point towards continued rental disinflation in the CPI. The 0.65% quarter-over-quarter change in Q4 is consistent with upcoming (NSA) prints for primary rents in the CPI in the 20-30bps range.

The data also showed meaningful revisions to previous quarters’ data, smoothing out some of the volatility in the Q2 and Q3 data. These revisions now see the ATRR data much more consistent with how primary rents have evolved over 2024. However, these data are subject to large revisions, so some caution is warranted

Thinkin’ extended pause, yer not alone. Some further context …

After 100bp of rate cuts the Fed has signalled it needs evidence of economic weakness and more subdued inflation prints to justify further policy loosening. President Trump’s low tax, light-touch regulation policies should be good news for growth, while immigration controls and trade tariffs provide upside risk for prices, suggesting we could have a long wait for the next cut …

Fed funds target rate mid-point and market expectations for the path forward (%). September 2024 versus latest pricing

For even MORE on coming trade wars, same firm …

ING: The path to avoid a more destructive US-China trade war is a narrow one

Donald Trump already has China in his sights as far as trade is concerned. There is some room for cooperation in the early days of China-US negotiations. But perhaps markets are overlooking the strength of China’s response if it’s pushed into a corner

For a few words on BoJ hike …

ING: Bank of Japan hikes interest rates by 25bp as markets focus on timing of next hike

As widely expected, the BoJ raised its target rate to 0.5% today. The surprise came from its latest inflation outlook, which was revised sharply higher throughout 2026. If the spring wage negotiations bring another solid wage increase, we expect the BoJ to deliver a 25 hike in May

Lookin’ for an FOMC mtg (next week) preview? Today’s yer luck day …

MS: Optimistic on Inflation, Cautious on Policy Outlook | January FOMC Preview

We expect the Fed to stay on hold but retain its easing bias. Chair Powell is likely to sound confident on disinflation given recent inflation outturns, keeping a March rate cut on the table. Our strategists stay long UST duration via 5-year notes, and maintain long MBS basis.

Key expectations

The Fed stays on hold, but retains its easing bias. Chair Powell is likely to sound confident on disinflation, but cautious on potential policy changes.

Inflation data has been favorable. If tariffs are gradually phased in across 2025, it leaves room for rate cuts in March and June. The path to cuts is there, but it's narrow.

We expect a meaningful discussion about balance sheet runoff and the end to quantitative tightening. We think QT ends in March, with risk to June or September.

Our rates strategists suggest investors stay long US Treasury duration via 5-year notes and remain positioned for a 25bp rate cut at the March FOMC meeting.

… Trade idea: Maintain UST 5y notes at 4.43%, with a target of 3.75% and stop of 4.50%.

Our FX strategists expect the FOMC meeting to be USD-negative, and recommend short USD positions against EUR, JPY, and GBP.

On agency MBS, our strategists remain long the mortgage basis.

… stay LONG, young man, stay long …

Back TO upcoming FOMC meeting, though, another precap…

The FOMC announcement is on Wednesday, January 29. The only communication following the meeting will be the policy statement and Chair Powell’s press conference. The statement will be released at 2:00pm (EST) and the press conference begins at 2:30pm (EST).

The main takeaways we expect include:

No change in interest rates (target funds range 4.25%-4.50%)

Limited changes to policy statement

Powell to emphasize uncertainty & data dependency

For a couple / few words on BoJ and the setting of rates …

The Bank of Japan raised interest rates a quarter point, as had been signaled in the media in advance. The BoJ appears to have confidence in rising wages, and like other central banks is following the trend of inflation (the difference is that Japan’s trend is rising). We expect one further rate increase this year.

ECB President Lagarde is speaking, which is not unusual. The remarks are being made at the World Economic Forum in Davos which may add media attention. Investors are confident in their expectation that rate cuts are coming.

US President Trump declared they knew interest rates better than the Federal Reserve. This omniscience may be undermined by Trump also declaring the recent inflation was probably the highest in US history. US inflation was higher four times during Trump’s lifetime (in the 1940s, 1950s, 1970s, and 1980s). Economists believe inflation is important to understanding interest rates.

At Davos, Trump seemed to imply a universal tax on US consumers of any imported goods (a universal tariff). Universal tariffs cannot legally be avoided, while supply chain rerouting can escape selective tariffs (as happens with up to a third of China’s exports to the US). Trump then said they were reluctant to further tax US consumers of goods from China.

AND as a visual learner, this next one caught my eye …

WELLS FARGO Charting the Course: U.S. Trade in 12 Charts

Summary Since taking office on Monday, President Trump has yet to impose new tariffs, though he has directed agencies to investigate current trade agreements. Tariffs remain very much in play. He has mentioned the administration may impose a 25% tariff on imports from Mexico and Canada and levy a 10% tariff on goods from China as soon as February, while also commenting that the European Union will see tariffs as well. If President Trump's first term is any guide, trade policy will remain a key item on the agenda over the next four years. With that in mind, we present a visual guide to the current state of U.S. international trade.

Finally, from Dr. Bond Vigilante …

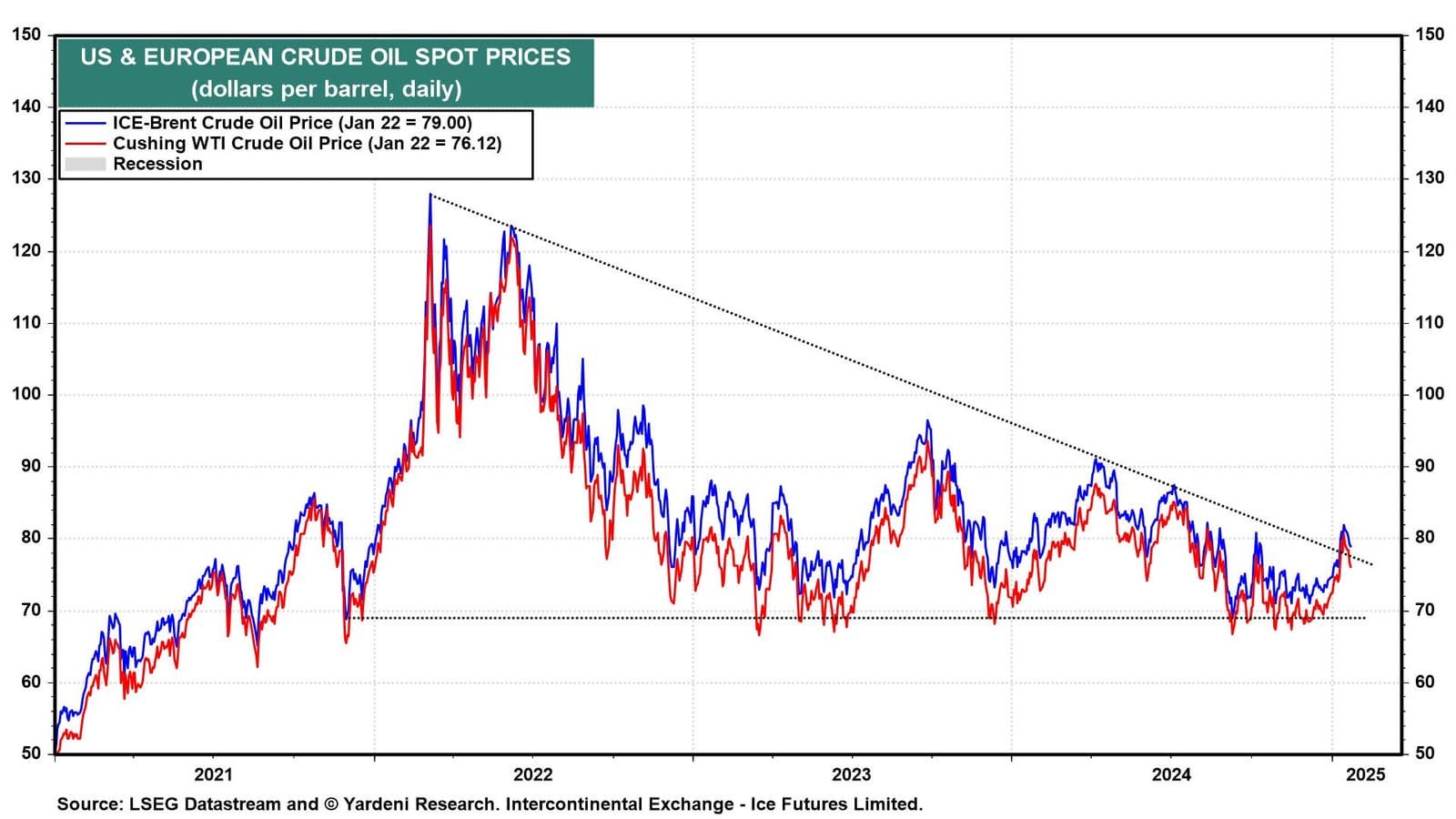

YARDENI: Take Down These Interest Rates And Oil Prices Too!

President Donald Trump invoked his inner President Ronald Reagan today in a virtual speech at the World Economic Forum in Davos, Switzerland. But his asks amounted to a taller order than just "tear down this wall." During his address, Trump demanded lower interest rates (not just in the US, but globally), called on OPEC to lower oil prices, and urged that the Russia-Ukraine war must end as soon as possible. He also warned that foreign companies either produce in America or pay tariffs.

During Trump 1.0, the President also demanded that the Fed lower interest rates. Perhaps it gives dovish Fed Governor Christopher Waller a bump in his shadow campaign for Fed Chair, 2026. The stock market took the comments in stride, as the S&P 500 reached a new record high of 6,118. But the biggest impact of Trump 2.0 so far has been in the oil market. A barrel of WTI crude is down from $80 on January 15 to $75 today, erasing its gains from the Biden administration's last-minute added sanctions on Russia (chart). We think there's room for crude prices to fall further.

Shifting from Davos to the US, today's economic data were positive on balance. Here's more:

… And from the Global Wall Street inbox TO the WWW … a few curated links …

Trump and RATES … a view …

Bloomberg: Will the dog that barked in the nighttime also bite? Markets are getting the idea that Trump 2.0 doesn’t have the leeway to follow through on pronouncements.

… Rates

Apparently referring to Federal Reserve Chair Jerome Powell (appointed by Trump in his first term), Trump told reporters:

I think I know interest rates much better than they do, and I think I know it certainly much better than the one who’s primarily in charge of making that decision. If I disagree, I will let it be known.

It’s true that oil prices and yields tend to move together, with big drops in oil accompanied by falling rates. However, this is often because of a crisis (when both fall together), and both tend to be a function of the broader macro economy. When times are good, both oil and yields will tend to rise. It’s not obvious that attacking the oil price in itself will bring down yields, although the case of 2014, when a breakdown in Opec discipline caused a crash in the oil price, is interesting. That time, with the economy not in notably bad shape, yields came tumbling:

Trump would not be the first president to put pressure on the Fed, but his choice of words suggests a looming conflict. Powell’s mandate ends in 2026, and the process of replacing him will get underway later this year. For now, Powell can’t say much in response. It’s also hard for the Fed to set monetary policy without clarity on what’s coming from the administration. A growth agenda should make it harder to cut rates, but the central bank can’t say that out loud. Vincent Reinhart, chief economist of BNY Wealth and a long-time senior Fed official, put it this way:

It’s a trapeze-artist problem. You don’t leave your platform until your partner has also left their platform. You can’t assume political actions that might change policy until they actually happen, because they might not… A politic or cautious Federal Reserve isn’t going to raise its head in DC.

He added that the word “Trump” appears twice in all the transcripts from the two FOMC meetings held since the election. Both times, his name came up from journalists asking questions. It’s unlikely the name will come up at next week’s meeting either, as Powell will keep his head down. But the risk of a confrontation later this year, which markets would hate, is obvious…

… THAT is all for now. Off to the day job…back over the weekend b4 the games…