I’m STILL watching TLINE which inches down from 2.856 to 2.85% as does the 50dMA which comes in today at 2.976% … momentum offering very little but does appear to be leaning towards a bit (more)of a concession, at least early on here this morning. There is somewhat more on LEVELS TO WATCH, just below …

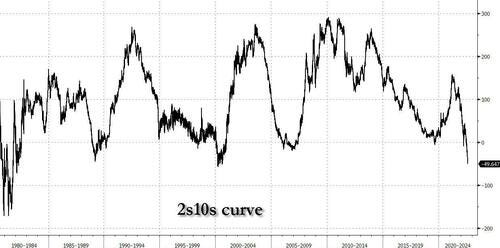

I WILL say that while the Fed continues to get put into a corner and may be forced to tighten MORE than currently priced in to markets, especially given rate CUT expectations (which have eased a touch as of late), the search or ‘quest’ for duration may just be starting. Curve FLATTENERS then still make some amount of common sense and here is ZeroHedge with some thoughts by Ven Ram (@ven_word)

The inversion in a key segment of the US yield curve may deepen to levels not seen since the 1980s as competing concerns about higher policy rates and their economic impact play out in the markets.

Ten-year Treasuries now offer a yield of around 2.78%, compared with about 3.28% on two-year maturities, leading to a differential of minus 50 basis points. That spread may invert further to minus 65 basis points, and beyond, in the coming months as front-end bonds sell off more than longer maturities.

Employers stunned economists by adding more than half a million jobs in July. That print is likely to add to the Fed’s conviction about the economy’s resilience. Chair Jerome Powell remarked before the report that the “strong labor market makes us question the GDP data” that pointed to a recession …

… Indeed, the 10-year maturity is now trading at a premium of almost 68 basis points over its implied value of 3.4792% based on realized inflation and the Fed’s benchmark rate. While the 10-year yield may climb in sympathy with a higher Fed funds rate, I expect the security to still trade at a premium.

Those factors will mean that the spread between 10- and two-year yields may become the most inverted since the early 1980s, when then Chair Paul Volcker was wrestling with mammoth inflation by raising rates successively.

While a search for duration would have proved to be a failure earlier in the current cycle, now may be the time to get set for a meaningful quest.

… here is a snapshot OF USTs as of 7a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are mixed with the curve pivoting steeper around a little-changed belly ahead of US CPI this morning. DXY is lower (-0.25%) while front WTI futures are too (-1.3%) as oil prices hover just above key range support near $88.50 (see attachments). Asian stocks were mostly/modestly lower, EU and UK share markets are little changed while ES futures are showing +0.17% here at 6:50am. Our overnight US rates flows saw another dead-quiet Asian session (~60% of ave volumes) with some interest to buy the front end and 30yrs seen from real$. During London's AM hours Treasuries were bid with EU bank treasury's buying original-issue 30yrs in the 20y sector on ASW and outright. We also saw Asian real$ demand for T-Bills out to intermediates with a series of TU block buys supporting the front end too. Overnight Treasury volume improved to ~85% of average this morning.

… US news: San Fran Fed research : "Given the large increase in short-term inflation expectations in the past year, our results point to an important upside risk to inflation, as workers demand higher wages that businesses could pass on to consumers by raising prices..." FRBSF Bullard: "We may see some relief in the headline CPI tomorrow [today] but the reason we tend to track core PCE inflation is exactly because we ignore the energy price movement on the way up but also on the way down." FXLUS online prices post first annual drop in over 2yrs as pandemic demand cools BBG Dreaded 'down rounds' shave billions off start- up valuations RTRS Investors watch for cracks in the consumer loan market FT Bad news: equity analysts are ecstatic again FT Chipmakers expect slowdown to expand beyond PC's and smartphones WSJ

… Further out the still steadily flattening curve, Treasury 5yr yields are going into CPI pressing up against their similarly-constructed bull trend today; a presumed support that comes in at 2.98% this session.

And even further out, our next picture shows the 5y5y OIS rate sitting/idling in the middle of its well-defined bull channel off the mid-June rate peak. To wit: there's something for everyone, depending on which part of the curve you traffic in.

… and for some MORE of the news you can use » IGMs Press Picks for today (10 Aug) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the brightest bulbs on Wall St, some of the most respected 2-handed economists out there, a few things I’d like to share.

First up from the group who recently suggested DISINFLATION AHEAD comes,

… We expect core PCE goods inflation to fall from 5.5% year-on-year to 3.2% in December, subtracting 0.6pp from overall core PCE inflation. This is meaningful, but we expect it to leave core PCE inflation at a sequential run rate well above 2% through the end of this year and at 4.5% year-on-year in December. A more sizeable disinflationary impulse from core goods will likely have to wait until 2023.

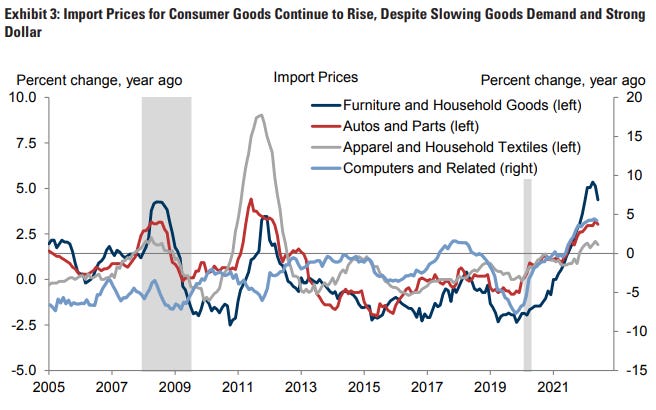

… as shown in Exhibit 3, year-on-year import price inflation for most consumer goods is only starting to peak now, despite the appreciation of the dollar and the slowdown in US and global goods demand.3 Together this suggests upward pressure on base pricing for consumer goods during the back-to-school shopping season—and likely into Q4 as well. We do, however, continue to expect the strong dollar and easing supply chain constraints to weigh on import prices later this year, and in turn on consumer goods prices by the first half of 2023.

Next up is a timely bit of narrative for the elite global climatologists on Global Wall St

Policies to effect the transition to net zero carbon emissions will contribute to global inflationary pressures, in our view.

The key stagflation risk we see is a delayed transition requiring steep rises in carbon prices.

The large increase in global energy prices caused by the war in Ukraine is likely to accelerate the transition.

We think DM central banks will ensure that a 1970s-style outcome remains a worst-case scenario.

In the transition, EU energy markets are likely to remain tight and prices volatile, with pressure to the upside.

Rates: Inflationary pressures and price volatility arising from climate change and the necessary transition should see inflation risk premia rise and nominal rates curves remain at relatively flat levels.

FX: Implications for currencies go beyond the inflation channel alone. G10 commodity exporters appear likely to outperform, though, and a reflationary environment might see the USD broadly weaken, but perhaps by less than history would suggest.

HERE are some weekly multi-asset macro charts / themes for those into technicals where I’d highlight this one ahead of today’s 10yr auction

10yr US Bond Yields rose last week with the market now oscillating around the “neckline” to its “head and shoulders” top. With a top still in place for now, we see the risks to yields as skewed to the downside over the next 1-3 months from a technical perspective.

ANOTHER CHART for those interested in today’s CPI as it relates TO FedFunds pricing which ultimately will show up in the front end of the UST curve, yesterday

US2YR: Is trading higher after bouncing off two-month descending former resistance now support at 3.18%. A close above 3.27% today, if seen, would complete a bullish outside day as well as a double bottom formation that targets 3.75% with interim resistance at 3.45% (2022 high). We still believe that the 2YR yield has more room to head higher given that the peak in the 2YR, historically, is quite close to what the terminal fed funds rate will be. Considering current headline inflation is at 9.1% YoY and Citi Econ expects a print of 8.8% YoY tomorrow as well as Core CPI to rise from 5.9% to 6.1%, the Fed clearly has more work to do to combat inflation which, by definition, would mean that the 2YR will likely break new highs…

I’m sure it’s ALL nothing. It is fine … I’ll NOT insert THAT MEME but instead, will advance this oldy but goody … where I’m reminded of an economic pillar of the US (largely consumption based, am I right?)

NOTHING without a consequence and … THAT is all for now. Off to the day job…

{kind=link}

{kind=link}

{kind=link}