Good morning … US economic data was somewhat LESS than good (more below). USA kills an Al Qaeda leader via drone (CNBC). And perhaps most importantly, Pelosi heads TO Taiwan SO, Chinese warplanes buzz the dividing line dividing Taiwan Straights (RTRS).

Here is a look at 20yy and I’ve attempted to highlight momentum (stochastics, bottom panel) which have gone from oversold - JUNE - to overbought, approaching ‘round number’ resistance (3.00%)for more on how bonds have gone from oversold to overbought, see JPMs comments HERE

… here is a snapshot OF USTs as of 725

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are higher and the curve flatter again (the 2s5s Tsy curve sits at its November 2000 low of -25bp this morning) ahead of today's auto sales and JOLTS prints and amid high tensions over House Speaker Pelosi's scheduled Taiwan visit tomorrow. DXY is modestly higher (+0.1%) while front WTI futures are lower (-0.7%). Asian stocks were paced mostly lower by Chinese markets (SHCOMP -2.26%, Hang Seng -2.36%), EU and UK share markets are all lower (SX5E -1.1%) while ES futures are showing -0.8% here just before 7am. Our overnight US rates flows were dominated by another FV block buying spree with 6 block buys(?) posted earlier this morning totaling ~$1.5mln/01. Color from the cash markets was unavailable but overnight Treasury volume was solid at ~190% of average.

… Yesterday's session finally saw Treasury 30yr yields join their intermediate brethren in breaking bullishly below range resistance levels. We show yesterday's crack and close through 30yrs' 2.94% range resistance with next resistance seen here at ~2.82%- a resistance that proved to be the foundation for the rise to above 3.40% in mid-June. We show yesterday's bullish break in 30yrs in today's first attachment and, perhaps predictably, it came on a day when front WTI futures also broke their month's-long range support near $94.09 yesterday too.

… and for some MORE of the news you can use check out Finviz.

Before I jump in to various narratives of Global Wall Street I’d like to bring this one from BBG forward, as it seems to me to be a big’ish deal.

Poor liquidity and economic uncertainty triggers yield swings

German bonds are their most volatile on record by some metrics

… From Sydney to Frankfurt to New York, market weaknesses long hidden by ultra-easy monetary policies are being exposed, stoking concern about potentially painful disruptions that could ricochet into other markets and the economy as a whole. Once-boring German bunds are jumping around by the most on record, while Australian bond futures are near the most volatile in 11 years. Japanese bankers are grappling with days when not a single benchmark bond trades.

But it’s in the $23 trillion US Treasuries market where the dislocations are causing the most trouble, fueling angst from investors and regulators alike about what can be done to shore up this crucial global financial linchpin.

With US Treasuries serving as the risk-free benchmark for more than $50 trillion of fixed-income assets, extreme volatility in their yields could make it tougher for private-sector companies to raise capital easily and at the lowest possible cost. The market gyrations also threaten to introduce chaos into what traditionally has been the preferred asset class for pension funds, retirees and others looking for the safest possible investment returns. And all of this in turn could pose risks for the broader economy that eventually may force central banks to change their plans…

Now in as far as Global Wall St goes, some NOT zerohedge data recapping by WFC where,

Here’s one for your inner techAmentalist from the CHARTS Department (and 1stBOS who is NEUTRAL on govies 3-6mo horizon).

Chart of the Day: 10yr US Bond Yields have fallen sharply for a break of major resistance at 2.715/705% as warned of in our recent spotlight for the completion of the flagged “head & shoulders” top. We look for this to clear the way for further strength to 2.555% initially and eventually the 38.2% retracement of the 2020/2022 upmove at 2.305%...

Which makes 1stBOS better buyer of dip (at support of 2.725%). Meanwhile they will STAY ‘tactically bullish’ 5yy from 2.905%. Check it out. Others sure are. HEREis another chart you’ll find noting the TREND (trend is your friend) on fintwit

@mark_ungewitter Long-term bonds have plenty of upside if June 2022 was a cyclical bottom. Big if, of course.

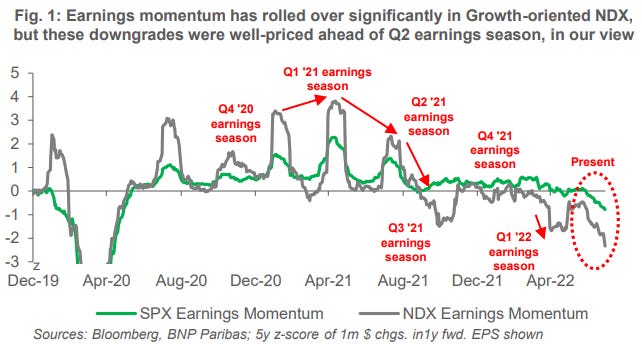

Here’s another couple charts from BNP and these are directed at your inner stock-jockey. First on EARNINGS (and kindly note the direction of travel)

And then somewhat MORE about the path of least resistance,

… Pain trade still to the upside: With the Fed laying the foundation for a more moderate approach in the back half of the year, alongside resilient earnings from Tech heavyweights, this has driven stocks higher as we had anticipated – see Selling the right tail in a new range, dated 18 July. While we previously highlighted 4150 as the top-end of the S&P 500 range, with the close above the 100d MA on Friday, positioning in equities still very defensive, and volatility having come down materially, we see scope for further upside in the near-term as market participants get crowded in. We though maintain our view of selling the right tail of the equity return distribution, thus investors may consider rolling and re-striking the call flies/ratios we previously highlighted as the market hovers just below the middle strike (4150).

And finally, a blast from the past (or at least someone I’ve not seen hitting inboxes recently) is the latest from Zoltan Pozsar of 1stBOS who reiterates what I think we can mostly all agree on. WAR = INFLATION.

Wars come in many different shapes and forms. There are hot wars, cold wars, and what Pippa Malmgren calls hot wars in cold places – cyberspace, space, and deep underwater (see here). We would also add to the list of cold places “corridors of power” in Washington, Beijing, and Moscow, where great powers are waging hot wars involving the flow of technologies, goods, and commodities – hot economic wars – which have been major contributors to inflation recently.

Inflation did not start with the hot war in Ukraine…

…but the war did fan the inflationary currents that had been under way already: understanding today’s inflation as the result of an escalating economic war and a lingering pandemic is important, for if war and zero-Covid policies stay, the view that inflation is mostly cyclical, driven by excessive stimulus, is wrong …

… Our jobs used to be simple. Central banks became the epitome of transparency, and with slight exaggeration, the only skill we needed to get by in markets was the ability to read and comprehend English: central bankers have been saying for over a decade that their aim was to fight deflation by inflating asset -prices, and all we had to do was borrow at low rates and buy assets irrespective of quality.

Now our jobs are becoming more difficult.

The policymakers to follow are no longer central bankers, but heads of state at the pinnacle of power who aren’t known for the transparency of their thinking – especially not when at war. Translating speeches from Russian and Chinese and catching high -fives as opposed to fist bumps are becoming more important than parsing subtle grammatical nuances in central bankers’ policy utterances.

Central banks’ policy objectives are changing …

… Between a deep recession and damaging the Fed’s reputation as an institution, a deep recession is the lesser of two evils. The former is public service, and the latter is public disservice. The former is a central banker’s clear conscience, and the latter is a life-long burden. Whether Jay Powell will succeed in slaying inflation is not the question; in the context of economic war, we can doubt that. Rather, the question is whether he’ll try his best to slay it. There I have no doubts.

Combine ALL the above and what do you get as we enter August thinking about back-to-school spending and how it is Summertime is simply flyin’ by,