… and for some MORE of the news you can use » IGMs Press Picks for today (10 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

Given holiday conditions in the bond market (closed) and that I inadvertently passed along the wrong link initially yesterday, HERE are just a few observations from Global Wall Street’s inbox … In addition TO them, a few other items to help those still blessed to be in the FI markets, make it through the day watching only stocks and futures trade,

… Concluding back home, for the US midterm elections, polls have been shifting but most point to at least one house of the Congress changing hands and thus a split government. Our base case from my colleague Mike Zezas is gridlock. But divided governments do not always lead to benign outcomes. I was a Treasury official during a government shutdown; it was not fun. Indeed, following the 2010 midterms, divided government led to debt ceiling standoffs, a government shutdown, and ultimately the Budget Control Act. We will see if anything similar happens; high inflation should lower resistance to contractionary policy, but with our US team's base case of only 0.5% growth next year, such a shock would clearly risk recession. Policy always matters.

US after 2010 midterms: fiscal contraction amid high U3 rates

… The Fed’s FRBUS model estimates a 0.7% GDP hit for each 10% increase in the value of the dollar and a 0.3% hit for each 1% decline in foreign GDP. Our bottom-up trade model also implies a sizeable drag on GDP growth of 0.6pp in 2022 and 0.5pp in 2023 from the recent dollar appreciation and slowdown in global growth. The effect of dollar appreciation is fully captured by our usual financial conditions index (FCI) growth impulse, but the slowdown in global growth is only partially captured and will likely incrementally slow US GDP growth by about ¼pp.

Slower global growth and a stronger dollar will also put downward pressure on inflation. Imports account for about 25% of core goods and 10% of total core consumer spending, and we estimate that the recent dollar appreciation will lower core goods inflation by about 0.5pp and core PCE inflation by about 0.3pp, mostly due to lower import prices. Combined with a smaller inflation drag from slower global growth, we anticipate that foreign spillovers will lower core PCE inflation by about ½pp through end-2023…

… We continue to expect that the Fed will hike by 75bp in November, 50bp in December, and 25bp in February to reach a terminal forecast of 4.5-4.75%. Drags on growth and inflation from a stronger dollar and slower global growth should help to keep the economy on a below-potential growth path and make a noticeable if partial contribution to lowering inflation.

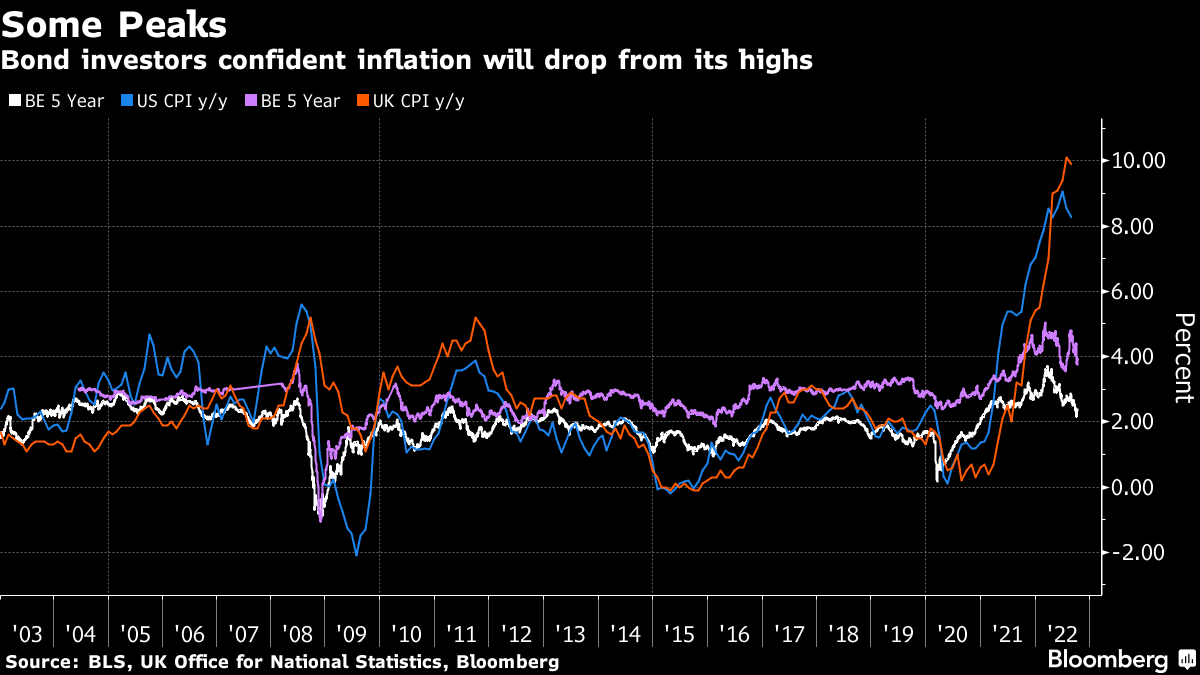

Dip buyers remain persistent across asset classes. Seemingly every robust data point and hawkish central bank decision or burst of rhetoric encounters fresh waves of investors willing to bet that inflation has peaked and so interest-rate hikes will soon slow and then give way to cuts. There are many dangers in such assumptions.

Looking just at the US and UK, five-year breakevens show inflation over the coming five years is expected to average about 6 percentage points less than the current generational highs for annual CPI readings. The threat here is double edged. There has to be plenty of skepticism that such a rapid tumble is achievable — especially considering that, in the US at least, you would need a significant period of sub 2% inflation to achieve what’s priced in. More worryingly, that sort of a slowdown would likely require a lot more central bank tightening and severe economic slowdowns.

And … moving on … some fedspeak just ahead (data calendar and amended sellside observations link HERE) but … THAT is all for now. Off to the (equity centric) day job as I continue to wait for the latest from HIMCO.