… Welcome one and all to QT day! The day the Fed starts its quantitative tightening program with an eye watering $30bn of treasuries and $17.5bn of MBS being withdrawn from the market monthly. It will be interesting to see how the market responds to this over time but it does feel like it has not been front and centre of the market’s attention of late. All eyes today on the manufacturing PMIs across the major financial centres with some central bank speakers thrown in for some fun …

Wondering if THIS is how The Hobbit planned to celebrate,

Look, I can relate as a former card carrying Transitorian … oh well. Moving on,

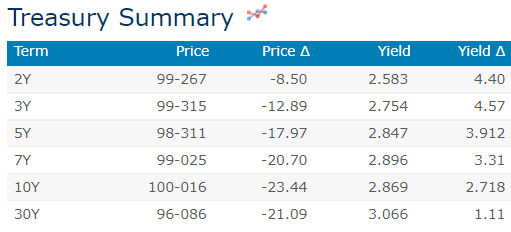

… here is a snapshot OF USTs as of 706a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are modestly lower with the belly slightly underperforming (Aussie 10's a mild drag at +6.8bp) ahead of today's data, Fed speeches (Williams, Bullard) and the start of QT. DXY is higher (+0.2%) while front WTI futures are too (+1.25%). Asian stocks were mixed, EU and UK share markets are little changed while ES futures are showing about UNCHD here at 6:55am. Our overnight US rates flows saw quieter Asian activity with modest real$ 2-way flow in intermediates a theme (sellers earlier, buyers later). Two block buys(?) in TY's of 320k each punctuated an otherwise quiet session. Overnight Treasury volume was right on top of averages across the board (save for 20yrs at 33% of average off a typically low base).

… 10s20s30s Tsy 'fly, weekly: A lesson in pricing convexity this one is. Not even larger cutbacks in 20's versus their benchmark peers can seem to offset the impact of convexity pricing and other demand-related factors for the hapless 20yr. We'd guess that, as years before, 20's might be the first on the chopping block if Treasury finds itself overfunded in the future-- being the most costly funding source curve-wise...

OR perhaps you remember it THIS WAY

… and for some MORE of the news you can use » IGMs Press Picks for today (1 June) to help weed thru the noise (some of which can be found over here at Finviz).

Along with being QT day! it is also Beige Book day and with that in mind, a few things I’m going to read / think about as I form my ideas of what next and how rates will react.

… What is the outlook for rates? In USTs, significant shorts have been cut with risks for a further short squeeze significantly reduced recently (and fast 1mth set now long). Can yields be squeezed lower technically? Lighter positioning in USTs have reduced the risks of an aggressive short squeeze and momentum accounts still required larger moves lower in yields before positions start switching long (by around 20bps). In contrast, EOM flows are supportive for outflows from USTs, but recent richening in equities has reduced the impact of this dynamics. This leaves USTs outlook more balanced with the biased to more cheapening with the focus on levels where recent longs move offside while in Europe focus squarely on the shorts side and levels where short profits get squeezed…

… De-leverage (oi) now close to 2019 levels in UST which has occurred an environment on rising volatility and illiquidity… (a combination of profit taking and rolling VaR shock?). However in Europe the impact has been smaller with rising leverage into cheapening.

ABNAmro reminds us that nothing happens without consequence,

Continued US consumer splurge risks bigger interest rate rises US consumption growth was unexpectedly strong in March and April, with goods consumption still well above the pre-pandemic normal. Consumers are so far accommodating the hit to their incomes from inflation by using savings from the pandemic, but they are also increasingly taking on more debt. This raises the risk that the Fed has to implement bigger rises in interest rates to bring consumption demand back into balance with supply. Such a move would mean a bigger chance of recession further down the line.

… The US Federal Reserve releases its Beige Book of economic anecdote—the economist’s version of "Hello" magazine. The evidence is hearsay, and some of the responses may be carefully stage managed to present a certain image (especially in politically polarized times). Labor market tightness will be of interest (with reports of some companies overhiring), as will the normalization of consumer demand…

SocGENs Kit Juckes reminisces,

Higher yields, stronger dollar – just like the old days … If another leg higher in US Treasury yields is the main risk to markets in the coming days, then I’m not sure there’s much of an alternative to the US dollar as long against GBP (say) in the short run. But the oil price, today’s Q1 GDP data and tomorrow’s Bank of Canada meeting do make my eyes wander in the Loonie’s direction. As that pair breaks 1.60, a move through 1.58 really would look ugly on the charts.

John Authers latest for any / all bond dip buyin freaks out there,

sFrom TINA to TARA There’s a difference between strategy and tactics. It’s as well not to get them mixed up. This applies to central bankers, stock and bond investors, politicians, and military leaders. The distinction is important to keep in mind at a time like this.

The last week or so has seen a switch to a “risk-on" narrative, as investors bet that central banks won’t have to raise interest rates so much after all. If that’s right, then of course you should buy bonds. That pushed down their yield — which justifies paying a higher price for stocks. This signals the demise of TINA, or There Is No Alternative (to stocks), and her replacement by TARA: There Are Reasonable Alternatives (to stocks).

Bonds To see how enthusiastically investors are now trying to buy the dip in bonds, rather than stocks, look at exchange-traded funds. In the last few months, shares outstanding in the iShares 20+ Year Treasury Bond exchange-traded fund (generally known by its ticker symbol of TLT), have surged, even as the share count in rival stock market tracking ETFs has dropped a little. This means that there is pressure from new buyers, which requires the creation of new shares:

Obviously the dip-buyers are taking the chance to invest at a relatively generous yield. For institutional managers trying to guarantee liabilities for pension funds or insurers, this is a matter of strategy, rather than tactics — if you can buy at a yield that eliminates your risk, you do it, even if there is a chance you could have made more money by waiting. But the weight of money from retail investors playing with ETFs suggests that they also see this as a good strategic call, rather than a tactical ploy when a market is temporarily oversold.

Jean Ergas, chief economist at Tigress Financial Partners in New York, suggests this is a classic confusion of strategy and tactics. The current risk-on rally gained force last week when the minutes from the Federal Open Market Committee’s May meeting failed to provide any fresh hawkish surprise, and then Raphael Bostic, head of the Atlanta Fed, commented that the central bank might want to “pause” its campaign of hikes in September.

This was the most dovish utterance by a leading figure at the Fed in a while, but Ergas suggests that Bostic was talking tactically, not strategically. He was suggesting it might be an idea for policy makers to give themselves more flexibility with a pause later in the year, not that the Fed might already be finished with its tightening campaign by the end of the summer. The market took it as a strategic announcement. Treasury yields rose sharply Tuesday (although they’re still well below their highs from a month ago) after Fed Governor Christopher Waller said that he thought 50 basis point hikes might be necessary at “several” meetings. That presumably means three or more. He was talking strategically …

Last week saw a strong recovery in risk assets after equity markets stabilised above a series of key support levels and our prior target levels. We believe that this is a corrective recovery in equity markets, which can extend further in the short-term, particularly in the US. However, the broader trend picture remains concerning and therefore our base case is that this corrective recovery will eventually peter out …

… Similarly, Global Bond Yields stay trapped in sideways consolidation phases, which we still expect to continue over the next few weeks. However, the 10yr US Bond Yield is expected to break above its 2018 high at 3.26% later on in the year.

Barclays: Beware of the 'Reasonable' Valuations Trap Although P/E multiples have fallen below pre-pandemic levels, we do not think they are "fair" given the vastly different macro environment. Inflation has been the primary driver for valuations and its persistence is a downside risk. We caution that the commonly believed dependence on real yields is very weak historically …

… The strongest driver for the P/E multiple is the level of inflation (Figure 4). The negative correlation between inflation and valuations is apparent from the decline in inflation since the 70s/80s coinciding with a rise in valuations, with a much tighter relationship than valuations and long-term rates. Most notably both inflation and earnings yield bottomed in the early 00s, while long-term yields continued to decline.

… Current valuations have ~10% potential contraction give the macro environment, but the risks are to the downside … However, if inflation and inflation volatility increase, or simply remain elevated, it will put further pressure on our PE model projections. While stronger inflation reduces our fair Value PE, persistently high inflation allows more time for current valuations to revert lower. As we believe that the risks are skewed to higher inflation, there is further downside risk to SPX valuations beyond the additional ~10% contraction implied by our FY22/nTM model projections.