Here a few words of catchup from Harkster.com and The Morning Hark

… FI - After a long time on the sidelines yields spiked higher across the board with Bunds leading the way post German inflation data and ECB’s Lane claiming that rates would leave negative territory by q3. US yields also spiked higher with the 10y rallying to 2.84 fuelled further by Fed’s Waller comments and the scheduling of a meeting between Biden and Powell for later today.

… here is a snapshot OF USTs as of 715a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower with the belly of the curve underperforming after European inflation readings surprised upwards and China's PMI data showed their slowdown decelerating. Fed Governor Waller's comments yesterday (see top link) perhaps adding pressure to bond prices too. DXY is little changed while front WTI futures are higher (+3.1%) after EU leaders committed to an embargo on most Russian oil. Asian stocks were mixed (China shares higher on stimulus hopes), EU and UK share markets are mostly lower while ES futures are showing -0.45% here at 7am. Our overnight US rates flows saw Asian real$ selling after 10's opened +6bp on a catch-up move to EGB's yesterday. Some block steepeners (FV/US and TY/US) were reported. In London's morning some Asian real$ dip buying was seen ~ the 20y point. Overnight Treasury volume was ~140% of average all across the curve

… Treasury 10yrs, daily: I picked on 10's to illustrate the idea above that rates are now 'overbought' and threatening new bear legs. In this picture you can see how 10's respected horizontal resistance (~2.71%) late last week amid increasingly 'overbought' (see daily momentum, lower panel) conditions. The bull trend off the early May move high in 10yr rates appears to be giving way. Not shown is the daily chart of the 5y5y swap rate (Libor) which is also attempting a bearish Key Reversal today: new move low in rates earlier but threatening to close above the high intraday prints from Thurs/Fri last week- with daily momentum rolling bearishly now too...

UST 5yrs, monthly: Here we zoom out for a big picture look at Tsy 5's and how they're so far respecting support (drawn in) near 3.00%. Long-term momentum into 'oversold' readings now but very similar readings were evident in early 2018 too. NOTHING bullish yet.

… and for some MORE of the news you can use » IGMs Press Picks for today (31 May) to help weed thru the noise (some of which can be found over here at Finviz).

From the inbox SINCE the weekend (and a few observations from the sellside HERE),

Is There a Bull Case? PMIs and Earnings Revisions Remain Our Focus With consensus now more in line with our bearish outlook, what's the bull case? Outside of a peace agreement in Ukraine, it's difficult to construct a case for more than a bear market rally, which could carry another 5%, in our view. Consumer remains focal point for whether recession is coming.

It will be difficult to reverse the Fire and Ice… Higher inflation and slower growth are now the consensus view but that doesn't mean it's fully discounted. The more equity prices rise, the more hawkish the Fed will be. Meanwhile, falling PMIs suggest at least 10 percent downside while a recession would mean even greater risk. Sustainable rallies will require growth rates to bottom, something we don't foresee until later this year.

Earnings revisions breadth on verge of going negative... Going into 1Q earnings season, we made the call that disappointing reports and newsflow from corporates would take earnings revisions breadth negative over the coming months (Weekly Warm-up: Earnings Season Brings Risks). We are making progress on that trend as earnings revisions breadth for the overall market dipped into negative territory last week—meaning that there are more downward than upward revisions for the overall market, a dynamic that often precedes a consolidation in forward EPS.

What to expect in terms of a forward EPS consolidation... Declines in forward EPS amid growth scares but in the absence of recessions (our base case view for earnings over the next several months) average 3% and span an average of 3 months. Applying that historical precedent to the current backdrop implies that forward EPS would drop to $231 from $238. To triangulate that approach, we calendarize our 2022 and 2023 top down base case EPS estimates into a forward 12-month number, arriving at $230. So two different approaches yield a very similar result in terms of potential downside in forward EPS from current levels.

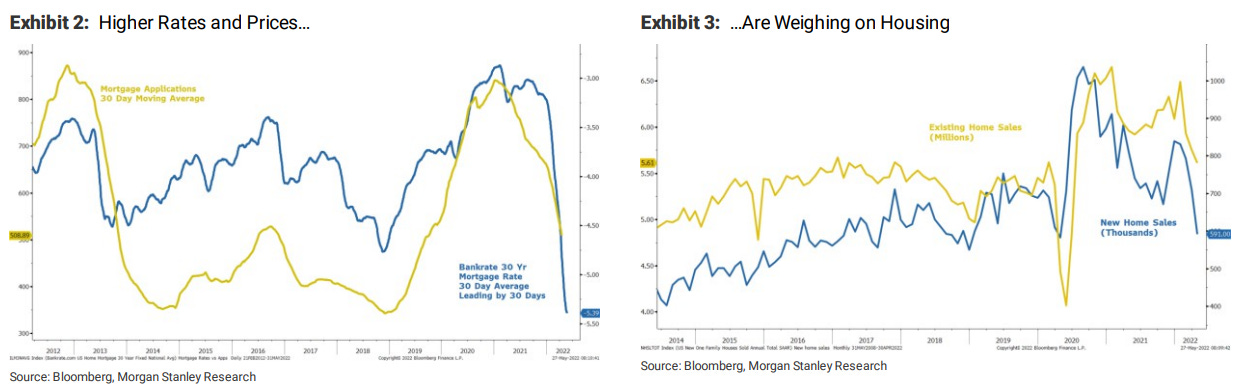

… we have been in the camp that the bond market may have overpriced how much hiking the Fed will need to do to get inflation back to a more reasonable level and/or to avoid a meaningful slowdown/recession in the overall economy. Perhaps the best argument in this regard is the decline already registered in financial markets and the dramatic slowdown in housing activity (Exhibit 2and Exhibit 3).

As we have been suggesting since late March, the bond market has already done a lot of the Fed's job even before the Fed actually makes more progress on its rate hike path and shrinks the balance sheet … The bottom line is that inflation remains too high for the Fed's liking and so whatever pivot investors might be hoping for will be too immaterial to change the downtrend in equity prices, in our view. However, that's not to say it can't get animal spirits moving higher in the short term…

Summary The U.S. national debt has increased substantially since the COVID-19 pandemic began a little over two years ago. Despite the increase in debt, interest rates generally have been very low for the past two years, and as a result net interest spending by the federal government also has remained low as a share of GDP. However, over the past several months the economic and interest rate environment has shifted dramatically. With interest rates on the rise, should we be worried about rising rates and the national debt?

No time to dissect if it is time to worry, just yet. Biden/JPOW and the Hobbit meeting as month-end indices and positions are adjusted…have a great start to your day as you plan your trades and trade your plans!