while WE slept: 10yy above 4% (highest since 8/8th); 'bond traders buckle up for 'no landing''; surprise; (and a h/t to reader for pointing out mislabeled visual)

First up, i’ve corrected / updated visuals posted over weekend — intent was to search for answers in the charts, talked of 2s and showed 10s (i’ve still got monthly of 10s).

My apologies for any of MY confusions and my gratitude to the reader for pointing out to me …

NOW lacking any further insight (not saying this past weekends note offered anything of consequence, other than a couple visuals which needed correction and have now been updated), i’ll begin the day and week with a couple links …

The stronger jobs data has redefined the US rates market yet again and uncertainty has become the new norm. We do take solace in the knowledge that the one thing we can always count on from the BLS is that the numbers will be revised. "Revisions make decisions." - No One Ever. And as we scroll through the recent round of headlines regarding claims to have finally located the Loch Ness Monster as well as Bigfoot (in separate discoveries), it strikes us that perhaps Powell's soft landing isn't that crazy after all. We wonder what the unemployment rate is at Area 51... it's probably out of this world…

… AND from a head of rates via LinkedIN, something which I read and strikes me as common sense …

Good Sunday morning. The pandemic view on UST 10-year below. We get lots of questions from clients on rates further out the curve. If we called a broader range of 3-5% in this brave new world, we sit in the middle. Inflation running 2-3%, growth 1.5-2%. It doesn't appear all that mispriced. We caught the Q1, higher inflation reading down. But there was no interest to chase yields lower. Friday's number is just that. A number. Subject to revisions? We know the answer but it was enough to balance out thoughts around yield levels. And there is plenty ahead. As I said to a friend last night; Feels like 2024 is just beginning. We could care less about this week's inflation readings. Keep an eye on oil moving forward as central banks around the world ease policy.

This week: FOMC Minutes, CPI, PPI, 10/30s UST, plethora of Fed speak. Have a great Sunday. The weather in NY is perfect!

… AND here is a snapshot OF USTs as of 648a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Equities modestly lower, US 10-year yield climbs to highest since August 8th … Bonds continue to extend on the post-NFP losses with the US 10yr yield now incrementally above 4%; highest since Aug 8 … USTs are extending the downside seen in the wake of last week's unambiguously hot NFP print which saw the odds of a 25bps rate cut rise from around 65% to current levels of 93%. US data docket today is light, so focus will be on US CPI/PPI later in the week. The US 10yr yield has climbed above 4% for the first time since Aug 8.

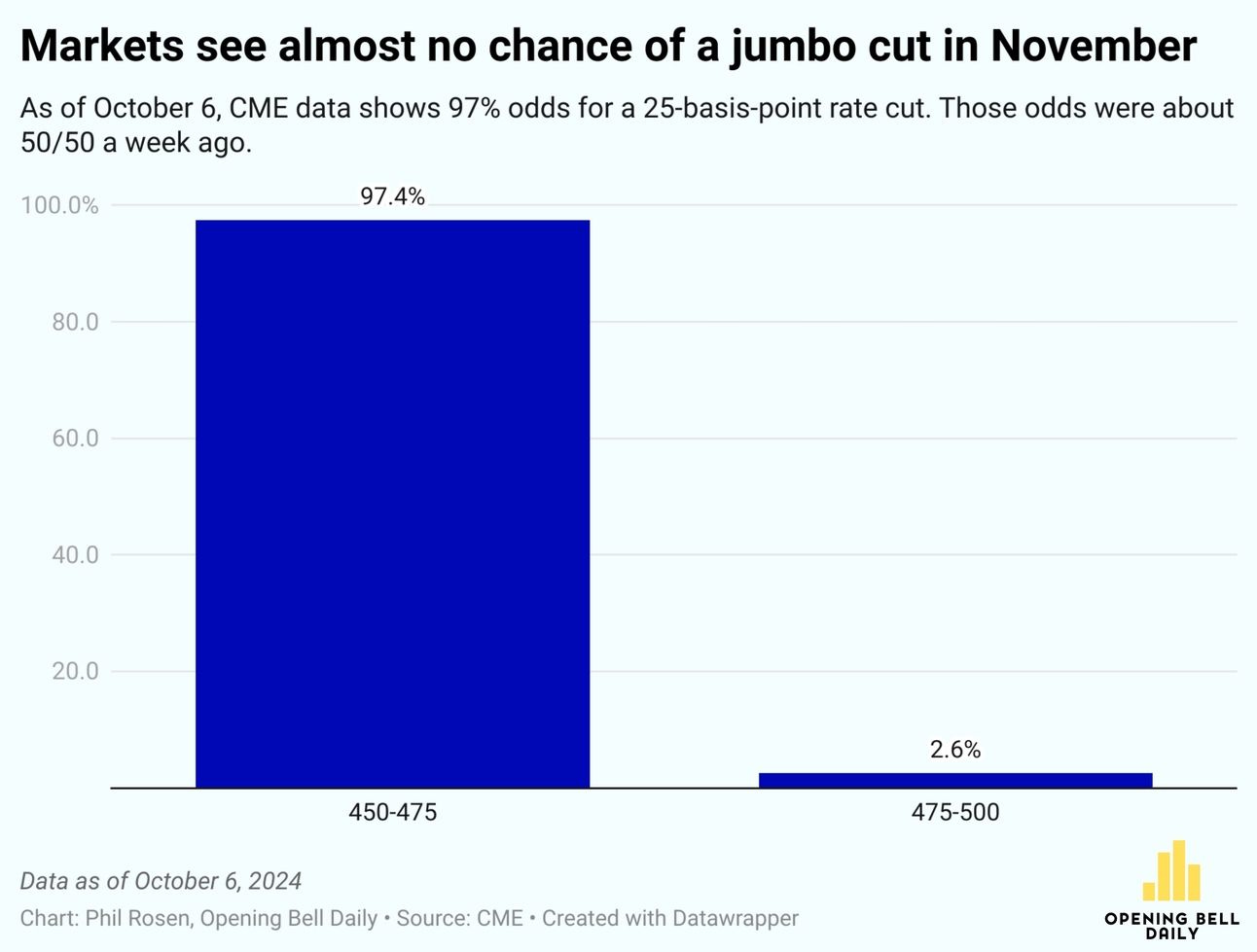

Opening Bell Daily: Fed overreaction - Blowout jobs data suggests the Fed overreacted with its jumbo rate cut … Employment, economic growth and income data have all come in more robust than expected after the 50-basis-point rate cut.

… As of Sunday evening, CME data showed about 97% odds for a 25-basis-point rate cut in November.

One week prior, that stood at about 50%.

“The bottom line here is that a resilient labor market is continuing to support consumers and the Fed is cutting rates,” said JPMorgan’s Ausenbaugh.

“Historically, that has been an environment conducive to the outperformance of stocks and bonds over cash.”

Finviz (for everything else I might have overlooked …)

We estimate the recent monetary, equity market and housing policies collectively could lift GDP growth by 0.2-0.3pp, reflecting eased corporate and household debt burdens being partly offset by lower returns on savings, modest wealth effects from the equity rally, and some recovery in housing market sentiment.

…. some of the times, a headline does plenty enough to capture your attention and make you WANT to read on … here’s an example …

Geopolitical risk premium is underpriced, in our view, so we are turning tactically bullish dollars as a hedge for further escalation in geopolitics and approaching US elections. As such, we added long USDHUF and long USDTHB trades last week.

We expect 0.3% m/m rounded US core CPI inflation this week. Despite a sturdy core print, the implication for core PCE is likely to be more benign at 0.2% m/m, which would keep 3mma and 6mma saar trend indicators around 2%.

Payrolls data shows the US economy is running at a solid pace and suggests the Fed will proceed in measured steps. We see value in hedging both harder-landing and softer-landing scenarios via limited downside or low-cost structures.

…This week, we expect September’s US core CPI to print a second consecutive 0.3% m/m, driven by a pickup in used vehicle prices and a rebound in some services categories, such as medical care and lodging-away-from-home prices. Despite a sturdy September core CPI print, we think the implication for the core PCE will be more benign at 0.2% m/m, leaving the 3mma and 6mma saar trend around 2% (see US September CPI preview: A little more upside, 3 October).

… On CHINA and the policy pivot (aka PPT, sticksave) …

MS: Sunday Start | What's Next in Global Macro: Hopeful but Not Yet Confident

… and everyone’s fav economist weighing in on what sorta landing to expect post JOBS report …

The US employment report last week was wrong, because the data always is. However, the general direction of US employment signals an economy very far from “recession”. However, voters do not think about abstract concepts like GDP, have a distorted view of price levels, and believe that pay increases are due to them working harder. While the reality is people have a higher standard of living for the same amount of work, the perception is people are working harder to stand still.

US consumer credit data tend to be volatile, and the consensus is not a reliable guide to the numbers. With the rise in online retail, people are using credit cards more, but are also more likely to repay their balance each month. Delinquency rates remain relatively low, reflecting the rise in real incomes…

Finally, a couple notes from the good doctor — an economic calendar in case you missed THESE and on FF …

This week's inflation indicators should show that it continues to moderate toward the Fed's 2.0% target. Also, this week's initial unemployment claims (Thu) will be for the same week that October's payroll employment report will reflect. That should provide a sense of how Hurricane Helene (and some workers' strikes) might have impacted the next monthly jobs report. Of course, we will continue to monitor developments in the Middle East.

Here's more on what we're watching on the home front:

(1) Inflation. September's CPI (Thu) should show headline inflation falling closer to 2.0%. The Cleveland Fed’s Inflation Nowcasting model projects that the headline and core CPI rose 2.3% and 3.1% y/y (0.11% and 0.27% m/m) last month. However, core services inflation likely remained elevated above 4.0% (chart). The so-called "supercore" inflation rate remains sticky.

Services inflation is likely to become a hotter topic. If China's stimulus measures and the longshoremen's wage increase raise import prices, goods PPI (Fri) and goods CPI inflation rates may rebound after several months of deflation (chart). The escalating conflict between Iran and Israel threatens higher oil and gasoline prices as well. Rebuilding from Hurricane Helene and other extreme weather events will likely prove inflationary, too.

We've been disinflationists since mid-2022, expecting that inflation would fall to 2.0% without a recession. However, the Fed's "mission accomplished" 50bps-rate cut on September 18 may prove to be premature if services inflation remains sticky and goods inflation heats up…

Remember the "higher for longer" mantra about the outlook for the federal funds rate (FFR) during the spring? It turned into "lower and sooner" this summer in response to the economy's soft patch. After Friday's strong employment report, the consensus might pivot to "no rush to ease further" during the fall. We can't rule out "higher for longer" making a comeback this winter. We are in the none-and-done camp for the rest of this year.

In the past, once the Fed started cutting the FFR, it was followed by a quick succession of additional rate cuts (chart). So far, the difference this time is that there's no credit crisis, credit crunch, or recession. Instead, the economy continues to grow at a solid pace around 3.0% on a y/y basis. So there's no rush for the Fed to ease, especially if the economy continues performing well.

In recent weeks, everyone agreed that lower interest rates should be bullish for smaller companies with floating-rate debt. The Russell 2000, S&P 400 MidCaps, and the S&P 600 SmallCaps have been rallying this year on expectations of Fed easing (chart). So have the S&P 500 Utilities and Real Estate sectors…

… And from Global Wall Street inbox TO the WWW … did someone say BONDTRADERS …

Bloomberg: Bond Traders Buckle Up for ‘No Landing’ After Jobs Surprise October 6, 2024 at 7:00 PM UTC

Strong growth in payrolls sends Treasury yields surging

Risk is that growth, inflation keep Fed cuts in check

… Data showing the fastest job growth in six months, a surprising drop in US unemployment and higher wages sent Treasury yields surging and had investors furiously reversing course on bets for a larger-than-normal half-point interest-rate reduction as soon as next month.

It’s the latest wrenching recalibration for traders who had been setting up for slowing growth, benign inflation and aggressive rate cuts by piling into Fed rate-sensitive short-term US notes. Instead, Friday’s report revived a whole new set of worries around overheating, spoiling the rally in Treasuries that had sent two-year yields to a multiyear low.

“The pain trade was always higher-front end rates due to less rate cuts being priced in,” said George Catrambone, head of fixed income, DWS Americas. “What could happen is the Fed either delivers no more rate cuts, or actually finds itself having to raise rates again.”

Much of the recent market debate had centered on whether the economy would be able to achieve the “soft landing” of deceleration without recession, or veer into the “hard landing” of a severe downturn. The Fed itself had signaled a shift in focus toward preventing a deterioration in the job market after fighting inflation for more than two years, and its pivot to rate cuts began with a half-point bang in September…

… same shop on <economic) SURPRISES …

Bloomberg: 5 Things You Need to Know to Start Your Day: Asia

… As expected, Friday’s US session was volatile, with yields spiking across the curve. After a jobs report that surpassed all expectations, resiliency in the US labor market suggests yields can go even higher. And that won’t deter stocks from continuing to rally on the prospect of a no-landing US economy.

The September jobs report ended speculation that the Fed would cut by 50 bps in November or in the meetings ahead. Now quite suddenly, the question has become not whether the Fed is behind the curve in easing monetary policy, but instead whether it is stoking an unsustainable boom.

In retrospect, the Fed’s large cut in September may have been a policy error. The Fed could have cut a standard 25 bps in July and again last month, giving it greater optionality to hold the line as the economic data turned up decisively from July relative to expectations. Larry Summers is among prominent voices on Wall Street warning about the same.

The latest data print is bad news for Treasury investors then. The increased prospect of “no landing” has also eliminated a floor for Treasury prices predicated on Fed rate cuts designed to remove policy restrictiveness by reducing real interest rates. Instead, we can now look forward to the upcoming CPI report with fear that the last mile in the Fed’s anti-inflation journey is even more protracted than it had anticipated. Future rate pauses on poor inflation prints cannot be ruled out — putting yields beyond 4% for maturities beyond two years within reach.

But this is all rocket fuel for stocks irrespective of what Treasuries do. The risk, for a market already trading at high price-earnings multiples, is a larger and longer boom followed by a more severe bust as the economy overheats.

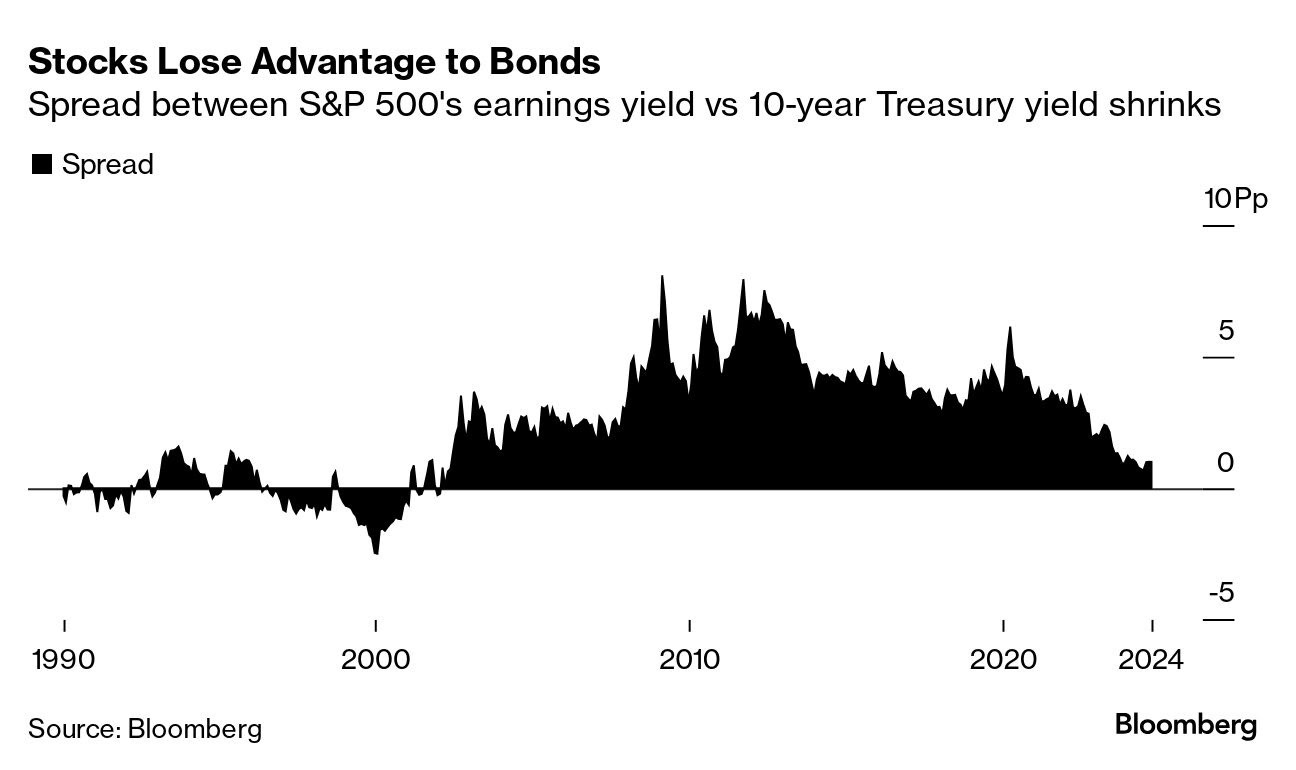

… speaking of SURPRISES, how about faces when they see / read ‘bout how, “Stocks Lose Advantage to Bonds” …

…It’s fair to assume the S&P 500 will hold onto most of its gains into year-end. Corrections are always possible, particularly with poor seasonals and election volatility coming up. But there hasn’t been a bear market without an accompanying profit or economic recession since at least 1998 — and none seems to be on the horizon now.

Bullish reasons for stocks outnumber bearish ones. Those include: ample global liquidity and Federal Reserve support; invincible consumers, and corporate earnings that are set for solid growth in 2024.

Still, I’m not turning into a raging bull. To balance out the many positives, one big negative is that stocks are expensive. At a multiple of nearly 22 times price to estimated earnings, the S&P 500 is trading at a record premium to the rest of the world — and a big one versus its own historic norms. Its earnings yield versus bonds is also unappealing.

That said, previous periods of exuberance like the dot-com era show that valuations can stretch for a long time before they start bothering investors. For now, while it’s premature to declare the all-clear on the economic front, the case for selling has greatly diminished.

… and once more on surprises of a different sort …

Bloomberg: Two Jumbo Cuts Were Too Much to Hope For

Strong jobs report puts another 50-basis-point Fed easing in November out of the picture.

… As the year has proceeded, the Fed has messaged, and the market has believed, that unemployment now matters as much as inflation to the central bank, if not more. That is now in question. The September non-farm payrolls prompted a rise of 12 basis points in the 10-year yield, its biggest since the June employment data. As the chart shows, Treasuries have lurched violently in both directions in response to new data throughout the year, with jobs now in the driver’sseat. After August’s recession scare, we’re back to worries about overheating and inflation:

There is inflation data on Thursday, which will matter as always. It’s hard to see how it can create a surprise to counteract what has just come from the payrolls. In conjunction with China’s stimulus, this economic cycle looks likely to carry on for longer. That means stocks can continue to beat bonds. As for the Fed, we can pencil in a 25-basis-point cut for next month, and concentrate on worrying about the election…

… One fascinating specific example is Walmart Inc. The biggest US brick-and-mortar retailer, and biggest private sector employer, has over the last quarter-century tended to beat the benchmark only when the overall market is selling off; indeed it was the only major company whose share price rose during the massive selloff from October 2007 to March 2009. The extent of its outperformance this year is something that typically only happens when everything else is falling apart. Confidence in Walmart looks extraordinary:

It’s also, somehow or other, outperformed Amazon.com Inc. this decade:

… I couldn’t pass up a quick look / link on 5yr BREAKS …

Inflation expectations have steadily risen since the Fed’s decision to cut interest rates. It is also fascinating that the 5-year breakeven rates have nearly perfectly bottomed out after retesting what was once a major resistance level, which we now view as historical support.

October 7, 2024 | The term “jump the shark” dates back to 1985 and the sitcom “Happy Days.” The character Fonzie jumps over a live shark while water-skiing. The idiom "jumping the shark" or "jump the shark,” according to Google AI, means “a creative work or entity has reached a point where something stops becoming more popular or starts to decrease in quality.”

… turning away from Bloomberg and for somewhat more on JOBS …

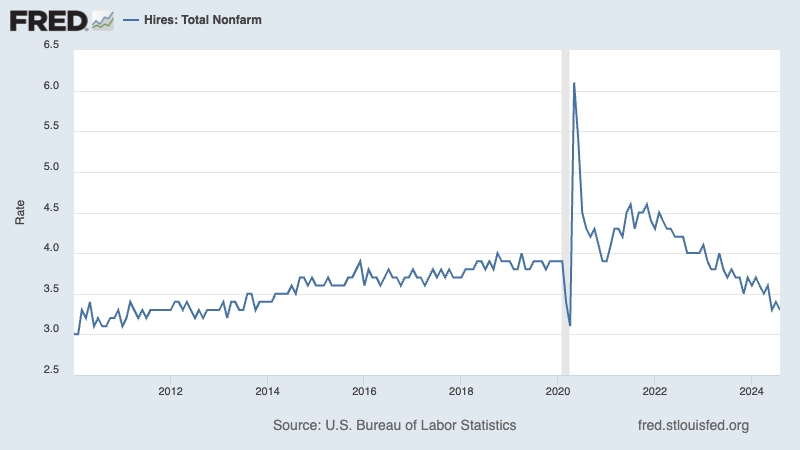

…And to be crystal clear, most metrics point to a strong economy that continues to grow at a healthy clip. In fact, the hiring rate today is higher than where it was during much of the 2009-2020 economic expansion. Our discussion today is not about sounding alarms. However, we should always be mindful of the fact that economic downturns do happen. And those downturns often come with early warning signs.

… on HOUSING …

WolfST: Mortgage Rates Explode, 2-Year & 10-Year Treasury Yields Spike, Monster Rate-Cut Hopes Doused, Inflation Fears Resurface: Yield Curve Before & After the Rate Cut

The yield curve moved further toward un-inversion, but not the way it was hoped.

… The average 30-year fixed mortgage rate exploded on Friday by 27 basis points to 6.53%, according to Mortgage News Daily. It was quite a mess (chart via Mortgage News Daily).

Mortgage rates roughly parallel the 10-year yield but at a higher level. The spread between the average 30-year mortgage rate and the 10-year yield has been around 2.5 percentage points all year, which is higher than average over the past four decades, in a range that went from near 0 percentage points to over 4 percentage points.

With the 10-year yield 3.98% on Friday, and the average 30-year fixed mortgage rate at 6.53%, the spread between the two measures was 2.55 percentage points.

The spread could remain in this wider range because the Fed no longer supports the mortgage market, as it had done during QE. As part of QT, it is letting its holdings of MBS run off at the pace of the passthrough principal payments, and it’s letting its holdings of Treasury securities run off at a pace of $25 billion a month. In September, the Fed’s total assets fell by $66 billion, to $7.05 trillion.

The Fed said it would let the MBS run entirely off its balance sheet even after QT ends, which would take years, and market participants will have to be enticed to take the Fed’s place, and this could mean that the spread will average wider than during the era of QE.

… THAT is all for now, thanks again for reading (AND reaching out to point out mislabeled visual!!) … Off to the day job …

President Trump, returns to Butler, PA..."As I was saying"

https://substack.com/app-link/post?publication_id=726749&post_id=149897886&utm_source=post-email-title&utm_campaign=email-post-title&isFreemail=true&r=1ecjk0&token=eyJ1c2VyX2lkIjo4NDU2NjAxNiwicG9zdF9pZCI6MTQ5ODk3ODg2LCJpYXQiOjE3MjgzMDM1MzQsImV4cCI6MTczMDg5NTUzNCwiaXNzIjoicHViLTcyNjc0OSIsInN1YiI6InBvc3QtcmVhY3Rpb24ifQ.qDfypu3d-QsTDdv0O0uKYBI1b2mtFmzh00MeLbZWXOk

ECONOMIC DECLINE: Recession, Money Supply Contraction, Tariffs on Consumers | Dr. Steve Hanke

https://youtu.be/po4iCyttgZg?si=-6ROwLtO11gvr_dd