weekly observations (10.07.24): when the facts change (JPM changes a call...); Multiple job holders hit record high; spec net SHORT 10s hit record high ...

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

I turn away from screens for a couple of days (it’s been years since I’ve not been watching some sorta screen on a NFP Friday) and I think there are now more questions than answers …

30yy DAILY: support up nearer 4.15%, month-end coming…#GotBONDS

… Gosh, whatever did I miss? Da HECK was I thinkin’?

I’ll run thru the inbox and see who’s sayin’ what and detail some of the victory laps and data recaps in a moment but I’m struck by the moves in rates (more so than the moves in stonks) …

I mean, hey … stocks are up. Jobs are being created (until next benchmark revisions) — government sector or otherwise. Gas prices are lower and so, too, is inflation … House prices are what they are. Not much use in complaining about higher interest rates there (although many still locked into jobs / locations given pandemic mortgage rates unwilling to give up).

The hope (not a strategy) is that rates will ultimately follow MARKET rates lower (only a problem on days like Friday …).

Interest rates are now being reduced and it seems to me the conversation isn’t so much as to IF they should / shouldn’t be, but the dialogue and betting markets focused on by how MUCH are rates to be CUT and how soon.

More questions than answers and I’ll begin MY journey for some answers in charts …

2yy DAILY: 4.00% psychologically important level of support … next up 4.1354%

… overSOLD momentum (stochastics, bottom panel) make ME think 2s are buyable after Friday’s rinsing …

2yy MONTHLY:

… momentum NOT looking so ‘attractive’ from a longer-term perspective …

… monthly chart above would urge CAUTION as we approach what could / should be support (4.00%) with momentum overBOUGHT and a bit of concession may very well be warranted ahead of this coming weeks supply …

… and so, with more questions than answers, what matters is whatever time frame and style YOU value and however, then, it is YOU wish to frame ‘markets’…

Rates charts in mind, a fan favorite segment of Friday’s NFP report I have always paid attention to is the number of MULTIPLE job holders … there are ways to frame this one, too, as with other points of data. One can make a compelling story / narrative and I’ll refrain from choosing sides except to simply point out as something for ones consideration …

at spomboy

In all the fixation on the quantity of jobs, the QUALITY is the issue. Jobs are of such low quality (in terms of wages) that Multiple Job Holders just notched a new record.

But wait, there’s more … see below for how some on Global Wall put in context of percentage of the employed (MS below) — FAIR.

For somewhat more context of all this, former Fed insider Danielle DiMartino Booth sheds some further light …

at DiMartinoBooth

"right now we are seeing multiple job holders at an absolute record level. The sum of continuing jobless claimants and part-time workers in the United States is also higher than it’s been, and it is also – there you go, multiple job holders…"

NOW, lets deal with a couple / few items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) … NFP

WolfST: OK, Forget it, False Alarm, Labor Market Is Fine, Bad Stuff Last Month Was Revised Away, Wages Jumped. No More Rate Cuts Needed?

Pandemic distortions and millions of migrants suddenly entering the labor market, who are hard to track, have wreaked havoc on data accuracy.

ZH: Blowout Payrolls: Sept 254K Jobs Soar Above Highest Estimate, Unemployment Rate Drops And Wages Spike

ZH: Behind Today's Stunning Jobs Report: A Record Surge In Government Workers

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, a few things which stood out to ME from the inbox … NOT all govt jobs, revisions still NEGATIVE, too soon to consider a PAUSE, a couple / few thoughts on this coming weeks CPI and an updated (changed) yield f’cast ALL worth a look …

BARCAP US Economics Research: September jobs report weakens the case for aggressive Fed cuts

Nonfarm payrolls increased by 254k alongside a drop in the unemployment rate to 4.1%. This report undermines the widely held view that labor demand is losing steam, reinforcing our call for continued resilience in activity and a high likelihood of a soft landing. We maintain our call for a 25bp Fed cut in November.

…US Outlook Seriously, no need to rush Nonfarm payroll employment roared back in September and the unemployment rate edged further downward, making another jumbo Fed cut in November seem unlikely. This was foreshadowed by more hawkish messaging from Powell earlier in the week, emphasizing that the committee is in no hurry to cut…

… Even before today's positive employment report, we had detected a shift in Fed messaging, with Powell emphasizing this week that the FOMC is in no rush to cut and leaning against the perceived sensitivity of Fed policy to the labor market. Today's data make another 50bp cut in November quite unlikely, though another 25bp is still likely in train…

We expect core CPI inflation eased 4bp, to 0.24% m/m (3.2% y/y), in September amid a moderation in core services, led by shelter. On the other hand, we expect a flat core goods CPI print amid modest inflation in used cars. We expect headline CPI increased 0.1% m/m SA (2.3% y/y) and forecast the NSA print at 314.891.

The most recent immigration data confirm a sharp decrease in humanitarian entries through 2024. The decrease can be explained mainly as a combination of President Biden's executive action on restricting immigration and fewer people arriving at the southwest border.

… Our estimates flag a sharp slowing in humanitarian immigration since December 2023. This appears to have been driven by three key factors: Biden's executive order on June 4, 2024, reduced flows of would-be immigrants arriving at the southwest border, and a suspension of the advance parole program for Cuba, Haiti, Nicaragua, and Venezuela …

… In our endeavor to be intellectually honest, it is worth briefly pondering what it would take for the Fed to pause next month. First, a prerequisite would be a comparable jobs report from the BLS for the month of October – which will be released on November 1st. This would not be sufficient in and of itself, however. Recall that the Fed is normalizing, not easing. As a result, there is no requirement for the outlook to involve a near-term recession or for the labor market to severely weaken. In fact, the only thing the Fed needs to see in order to justify a quarter point cut at its upcoming meeting is further progress on the inflation front comparable to the September core-PCE report. The Fed and the market agree that policy rates are at least 150 bp above neutral and therefore well into restrictive territory. Lowering rates by a quarter-point won’t change the Fed’s restrictive bias – aside from making it marginally less so.

To truly put a pause on the table, the Committee would need to be faced with a sharply higher core inflation profile with the September combination of core-CPI, core-PPI, Import Prices, and core-PCE. In the event of another comparably strong payrolls print and core-PCE at +0.4% (or higher) in September, it would be safe to assume that the Fed’s data-dependent policy bias would necessitate a pause. The week ahead will be very instrumental in refining expectations for core-PCE as investors will get core-CPI and core-PPI – providing a solid dataset for core-PCE forecasts. Barring unanticipated strength in US inflation, we’ll err on the side of continuing to favor a 25 bp November rate cut assumption …

BNP: US September jobs report: Strong data augurs ‘measured’ easing pace

KEY MESSAGES

The sizable acceleration in September payrolls and the lower unemployment rate, coupled with broader strength in US economic data over the last couple of weeks (including upside revisions to the national accounts), add to signs of resilience and strengthen the case for a soft landing. This should allow the Fed to continue the rate-cutting cycle at a measured pace.

Acceleration in private services payrolls – a sign of continued solid consumer demand – and the falling unemployment rate (to 4.05% unrounded), resulting from a decline in unemployment, validate the message of resilience contained in the headline numbers.

The latest data significantly reduces the risk of a hard landing and solidifies our expectation for 25bp cuts at the November and December FOMC meetings, as the Fed continues to remove policy restraint.

BNP US September CPI preview: A little more upside

KEY MESSAGES

We expect a pop in used vehicles prices and sturdiness in several services categories to drive a second straight rounded 0.3% m/m US core CPI print in September (released on 10 October).

Despite this ostensible strength, we forecast a more moderate corresponding 0.2% m/m print for core PCE inflation for the month.

While the strike by longshoremen could reintroduce upside pressure to goods inflation if it persists, recovered inventory levels should give retailers a margin of safety in the near term.

Overall, we think September inflation data should do little to challenge the Fed’s confidence that inflation is moving sustainably toward its 2% target, keeping policymakers squarely focused on risks to the employment side of the mandate.

BREAN: Economics Commentary: The September employment report was much stronger than expected

Key Takeaways: No matter how you slice and dice this report it was strong. The Fed looks somewhat foolish plunging into a recalibration of policy with a 50-basis-point cut in rates that was justified in terms of heading off potential weakness in the labor market, given that core PCE inflation has also failed to move toward its target over the last four months. The increase in employment plus the net upward revision to the prior two months put the level of payrolls in September 326,000 above the originally reported level for August. The even stronger 430,000 increase in household employment lowered the unemployment rate to an unrounded 4.051% and average hourly earnings for all private sector employees increased by 4.0% over the last year (on particularly strong gains in the last two months). The average increase in payrolls over the last three months was 186,000 per month, which is more than fast enough to push the unemployment rate lower, especially since the labor force has only grown by 67,000 persons per month on average over the last year. The ratio of job openings, which rose in August, to unemployment now stands at 1.18, the highest in three months. The labor market is not the source of inflation, monetary policy is, and there is likely to be a number of FOMC participants who were cajoled into supporting a 50-basis-point rate cut on September 18 who are now regretting that decision. The Fed is still likely to cut rates by a further 25 basis points next month, but an aggressive rate cut seems out of the question.

DB: US Economic Chartbook - Amazin’ jobs report sets up for a fall classic (25bps cut)

… In summary, while the report doesn't necessarily suggest a re-acceleration in the labor market, the September figures unwound much of the weakness in the previous two reports. The data are thus more consistent with a stable labor market picture with diminished downside risks, which argues against the Fed delivering another outsized cut in November. Given that recent weather disruptions are likely to impact some of the October economic data, the Fed is likely to put more weight on the solid September labor data heading into their November 7 FOMC meeting. In turn, we continue to expect the Committee to cut by 25bps (see "September FOMC recap: Powell delivers some good dovin'")…

…Government employment has picked back up in recent months, but remains below the robust pace of ‘23

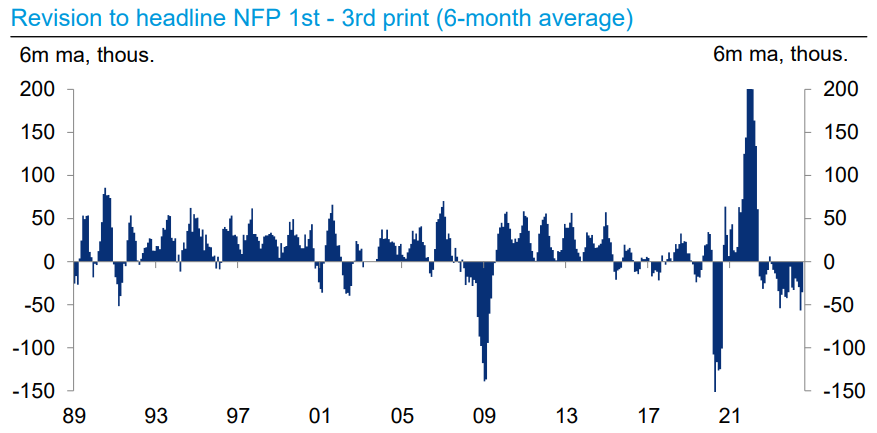

…Revisions to nonfarm payrolls still broadly negative

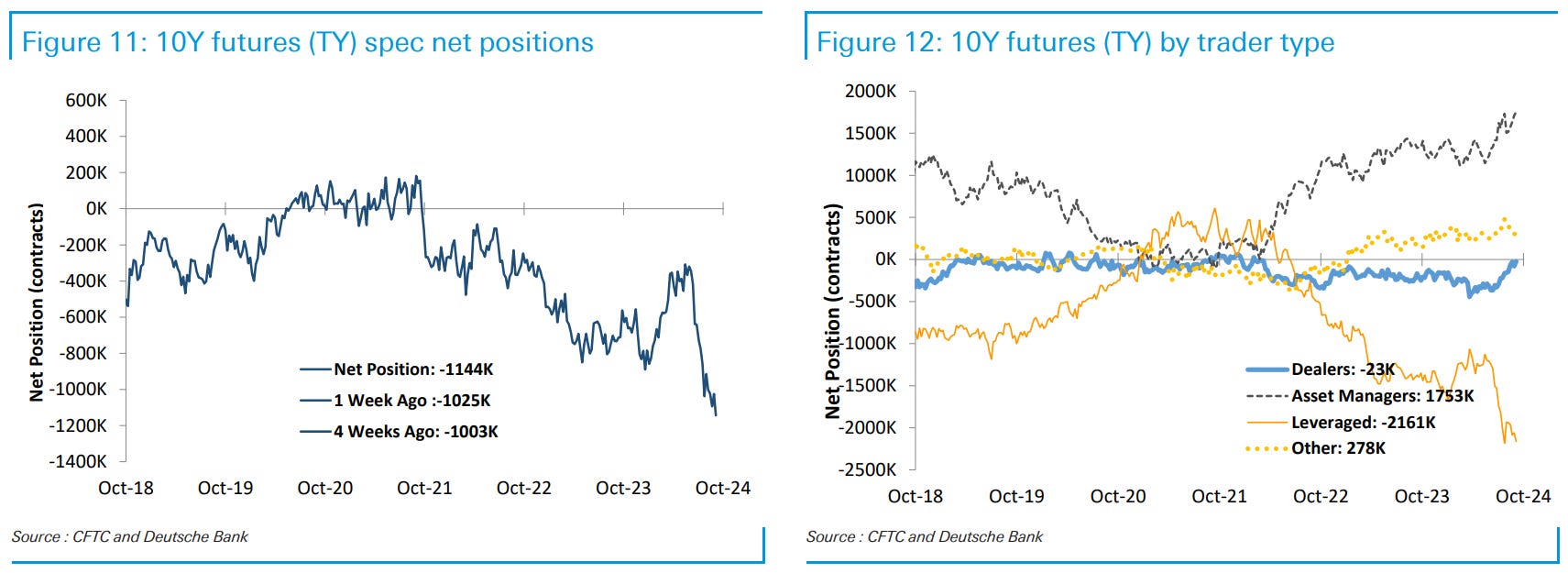

… Speculators sold 119K contracts in TY to extend their net short positions to a record high of 1,144K contracts

DB: Investor Positioning and Flows - Five Considerations For A Catalyst Rich Month

This month brings a plethora of potential catalysts with the ongoing geopolitical escalations, the Q3 earnings season, the lead up to the US elections, and see-sawing cyclical concerns with several key data releases in store. While there is potential for vol around these catalysts, we note that the demand-supply backdrop for equities remains solid.

Looking for resilient earnings growth but this earnings season is likely to elicit a muted reaction

Geopolitical escalation so far not following the historical playbook of a sharp short selloff

The election vol premium is modest so far but in line with levels at this stage in past elections and has historically risen gradually going into the event

Cyclical concerns, not rates, the key driver for equities

The demand-supply backdrop for equities remains solid

ING: Surging US jobs suggests the Fed needs to tread carefully

The US jobs report was incredibly strong on every front possible – job creation, unemployment, wages and hours worked. Nonetheless, caution lingers given the lack of corroborating data. While the inflation backdrop is allowing the Fed to start moving monetary policy back to neutral, we think it will be in 25bp incremements, not the 50bp we saw in September

We now look for a 25bp cut at the November meeting, as strong labor market data reduced the need for more aggressive Fed action...

...We raise our interest rate forecasts through year-end to reflect a slower pace of easing. We now forecast 2-year yields will drop to 3.70% at year-end (from 3.40% previously) and 10-year yields will be roughly unchanged at 3.90% (from 3.55%)

We no longer look for a near-term curve steepening, as a deeper cutting cycle appears less likely. If the tail risks around growth are falling, markets can price in a higher terminal rate, causing the curve to flatten further. Hence we unwind 3s/20s steepeners at a loss

Similarly, a bearish repricing of the terminal Fed funds rate would drag Treasury yields up as well, as long-term yields have been highly correlated with the market’s terminal expectations. However, cheap

Nonetheless, given the residual risk of further repricing of Fed expectations over the near term, we stay neutral on duration…

…In the absence of new information on weakening labor demand, we think there is a risk that markets price in a higher terminal rate over the near term, which would flatten the curve further, as the market’s medium-term Fed policy expectations remain the main driver of the slope of the yield curve. As a result, we recommend stopping out of 3s/20s steepeners at a loss (see Trade recommendations).

Data this week reinforce our view that the labor market remains strong despite slowing. The rebounds in payrolls and JOLTS should keep the Fed on pace for a 25bp cut in November.

MS: A Phoenix from the Ashes? | Global Macro Strategist

Unforeseen strength in September US nonfarm payrolls should make it more difficult for the US Treasury curve to steepen for now and makes the October payroll report less meaningful for markets. Focus turns to other central bank policies and related guidance ahead of the US election that looms large.

…Interest Rate Strategy United States The September nonfarm payroll report sent front-end yields higher and the yield curve flatter – both against our suggested positioning. The market-implied trough rate for Fed policy sits only 19bp below the median 2025 dot from the Summary of Economic Projections (SEP).

… The strength in the payroll survey may have been helped by multiple job holders, according to the household survey - which also showed impressive strength by lowering the unemployment rate to 4.1%.

The number of multiple job holders in September hit a fresh high for the month (see Exhibit 20). In addition, the percentage of people with multiple jobs hit a post-Great Financial Crisis high (see Exhibit 21).

The level on both trades reached our trailing stops, so we no longer suggest investors embrace UST 2s20s steepeners or receive the November FOMC OIS rate. Given the market prices Fed policy close to the SEP – which is consistent with our economist's view on the Fed – and the lack of major catalysts ahead of the US general election in November, we adopt a neutral stance on the US rates market.

We extend our butterfly metrics and infrastructure to 3-month SOFR futures butterflies. We craft all possible butterflies from the current outstanding contracts, up until the Jun-27 contract, resulting in 220 possible wings and body combinations. We recognize trading conventions focus on 6m or 12m "gap" butterflies, i.e., a 6m or 12m gap between each contract in the butterfly structure.

However, we wanted to maximize the flexibility of the analysis and the ability to choose more precise exposures, should investors feel the same way. With a larger sample of butterflies, more variance in the butterflies allows for more targeted trades. An investor with a bullish duration view should sell the U5/H7/M7 50:50 3-month SOFR future fly. An investor with a bearish duration view should sell the H5/Z5/M7 50:50 3-month SOFR future butterfly.

Of the conventional "gap" butterflies, most screen as not as attractive. If an investors wanted to trade a conventional gap butterfly, selling the H5/U5/H6 50:50 3-month SOFR future butterfly is comparable to the H5/Z5/M7 fly recommended above, albeit with slightly more of a negative correlation and less carry.

We expect core CPI at 0.26% in September (0.2%M cons, 3.2%Y). Our forecast implies core PCE at 0.19%M – a continuation of the overall disinflation trend. Housing inflation softens, but used cars accelerate and airfares remain positive. We see headline CPI at 0.09%M (2.3%Y, NSA Index: 314.718).

RBC: U.S. unemployment rate drops again in September

…Bottom line:

If you take September’s U.S. monthly jobs report as the best gauge of the health of the U.S. economy, the most recent report says conditions are far from crumbling, but holding onto the “American resilience” theme just fine. Taken alone, the strength of the report will take the pressure off of the Fed to reduce rates by another 50bps chunk at its November 7th meeting and ups the chances of a 25bps cut, though with still plenty of data to contend with before then.

The story isn’t completely cut and dry, however. Other U.S. jobs market data, like job openings quit rates and various surveys still suggest momentum is trending downwards and will keep the U.S. central bank focused on downside risks, happy to be surprised to the upside as opposed to the reverse.

For Canada, a more aggressive downturn in the U.S. has long been a risk for the economy that’s suffering from its own set of domestic challenges. We think today's U.S. Jobs report also take some of those worries away from the Bank of Canada as they grapple with a 25bps or 50bps cut decision on October 23rd. Although they still have plenty to contend with.

Wells Fargo: September Employment: Some Sizzle in a Cooling Trend

… Today's employment report is welcome news and suggests that the soft readings over the prior few months were not a sign of an imminent and sharp increase in unemployment. That said, one point does not make a trend, and there is still plenty of evidence to suggest that the labor market is cooling. That this cooling appears to be gradual rather than sudden reinforces our view that the FOMC will opt for a 25 bps reduction in the fed funds rate at its November 7 meeting instead of a second-straight 50 bps rate cut.

Wells Fargo: September CPI Preview: Sticky-Looking Core to Be Temporary

… Reducing core inflation remains more of a grind. We estimate the CPI excluding food and energy will post another "low" 0.3% increase (0.26% unrounded) in September, which would lead the year-over-year rate to slip back to 3.2%. Although we expect a similarlysized gain as in August, the drivers are likely to be different. Core goods prices look poised to take a temporary breather from the deflationary trend we believe is still underway, while core services inflation should moderate amid smaller gains in shelter and travel prices …

United States: Jobs Up, Rate Cut Expectations Down Nonfarm payrolls blew past expectations in September, rising 254K. Upward revisions to the prior two months' data sweetened the headline gain and bucked the trend decline in hiring, while the unemployment rate unexpectedly ticked down a tenth to 4.1%. The solid jobs report tamped down expectations for another 50 bps rate cut at the FOMC's next meeting in November

… Interest Rate Watch: The Outlook for Longer-Term Interest Rates The FOMC cut the federal funds rate by 50 bps on Sept. 18, and other short-term interest rates promptly moved lower. The Secured Overnight Financing Rate (SOFR) dropped roughly 50 bps in the aftermath of the rate cut, and yields on shorter-dated instruments such the four-week T-bill also fell materially. However, longer-term yields generally have risen modestly since the FOMC reduced the federal funds rate a couple of weeks ago. For instance, the 10-year Treasury yield has climbed from 3.65% on Sept. 17 to 3.95% today.

This move was not especially surprising in our view. We expect the FOMC to reduce the federal funds rate by an additional 175 bps over the next nine months or so, but we do not expect nearly as large of a decline in longer-term interest rates such as the 10-year Treasury yield or the 30-year fixed rate mortgage. One reason for this is that financial markets are already priced for a material amount of policy easing from the Federal Reserve. Fed funds futures imply 137 bps of rate cuts between now and the July 2025 FOMC meeting, not much different from our own forecast.

Of course, the realization that easing might still impact longterm yields, and other factors beyond just the outlook for the federal funds rate impact on long-term interest rates. The fiscal policy outlook could change on the other side of the upcoming U.S. election, or the economy could slow down more than we are currently anticipating. But in the absence of shifts like these or more Fed easing than we currently have forecast, we would expect the decline in longer-term interest rates in the coming months to be modest rather than sizable. We look for the 10-year Treasury yield to be in the mid-3s over the next few quarters, with 30-year mortgage rates 200 bps-250 bps higher than the 10-year yield. In other words, a return to the 2019 world of ~2% 10-year Treasury yields and ~4% mortgage rates is probably not in the cards anytime soon.

Yardeni: The US Economy Is Roaring! Yardeni: US Economy Passing Tests With Flying Colors Yardeni: Big Employment Increase Puts Recession Story to Bed

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

The incoming data continues to remain robust. The US economy added 254,000 jobs in September versus a consensus expectation of 150,000 jobs, the unemployment rate fell from 4.2% to 4.1%, wage growth is solid and remains sticky, job openings are going up, and the ISM services reading is also strong.

Why is the economy still strong? Because of lower sensitivity to Fed hikes for consumers and firms with locked-in low interest rates. Because of strong AI spending. Because of strong fiscal and defense spending. These tailwinds are countering the long and variable lags of monetary policy. And now the Fed is cutting rates, which is boosting growth and inflation further. Combined with very easy financial conditions, the bottom line remains that rates will stay higher for longer.

Our chart book with daily and weekly data is available here.

… In general our view; a recalibration of 100-basis points. We are 50-basis points closer following September's outcome. Markets today taking the froth off 75-basis points more for 2024 down to Powell's two doses of 25-basis points for next month and December. And for the forward curve, SOFR December 2025, we've highlighted the richness in pricing to the Fed's longer run neutral rates of 2.80-2.90%. And have backed off some 40-basis points with likely more to go.

On the Ground

The good money with appreciation in the US Treasury market was made with the backup in the first quarter of 2024. Higher inflation readings. The price action of late one of consolidation. It's healthy. Employment reports like this, coupled with some Fed "recalibration", is good for risk. But financial conditions in general have already been loose. And earnings need to show.

The Fed should be paying closer attention to balance sheet dynamics and market plumbing than being hell-bent on interest rate cuts. We have favored a slower approach from this Fed. Nonetheless, Chair Powell will continue to lower rates albeit at a slower pace. And the election outcome will matter. And we get another employment report on November 1st. So, nothing is a given at the moment.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

McClellan Financial: Deficits Are Horrible, But They Are Bullish - Chart In Focus

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Luke Gromen had a most fascinating interview on Macro Voices. He articulates a thesis that there's a tight relationship between Hedgefunds being the primary buyer of T-bills providing Gov Financing and backstopping Stonkmarket liquidity. Something like that anyways I probably need to listen again!

Luke Gromen had a most fascinating interview on Macro Voices. He articulates a thesis that there's a tight relationship between Hedgefunds being the primary buyer of T-bills providing Gov Financing and backstopping Stonkmarket liquidity. Something like that anyways I probably need to listen again!

Appreciate heads up little distracted this weekend will fix, thank u