weekly observations (08.12.24): downward RATES revisions, sky's NOT fallin' and finally the trade of the year(s) -- the steepener -- workin!! #GotDURATION?

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

It’s not much fun being a ‘bond guy’ as you cannot turn the switch on / off despite your surroundings and company.

Out last night ‘down the shore’ with friends having drinks listening to live music with the NYC skyline and this as the backdrop …

… company would NOT have understood or cared and thankfully did not notice me snappin’ the picture but I’m thinking this was a sign. Team Rate CUT representing 'down the shore’ and are LONG BONDS … ?

Last week we learned again how / why BONDS work (besides being able to get long a boat as a result?) as a part of a portfolio and again how / why it is the death of the 60/40 (specifically the ‘40’) has been exaggerated. Again.

We went from the week prior thinking the end is near (it isn’t, see Barclays below), stock markets in turmoil and bond yields dropping like a stone.

NOW bond yields are poppin’ as stocks erased losses with a vengeance and emergency 50bps rates cuts calls fading …

ZH: Stocks Erase 'Black Monday' Losses As Vol Tumbles; Bond Yields & Black Gold Surge

… Rate cut expectations tumbled from the initial surge on Monday with most of the swing in pricing concentrated in 2024...

Bloomberg: Investor Behind Record $2.7 Billion Bond Bet Says Recession Near

… Sure tell us all ‘bout it now that you KNOW it’s worked and you didn’t get forced to book YUUUUuuuuge losses (or run for cover with tight stops … since an insurance co behind the trade, guessing they were ‘hedged’) …

This weekend now we’re learning of Fed gov (so, a voter) Bowman …

Bloomberg: Fed’s Bowman Sees Upside Inflation Risk, Signals Caution on Cuts

Cites fiscal policy, geopolitics, pressure on housing market

Powell has put rate cut on the table for September Fed meeting

… “The progress in lowering inflation during May and June is a welcome development, but inflation is still uncomfortably above the committee’s 2% goal,” Bowman said Saturday in a speech to the Kansas Bankers Association in Colorado Springs, referring to the Fed’s rate setting panel. “I will remain cautious in my approach to considering adjustments to the current stance of policy.”

I left off looking at 20s (and so, a decent look at TLT, the 20+ yr UST etf) and I’ll jump in to look at 10s and bonds in a daily / WEEKLY context …

10yy WEEKLY … downtrend line comes in just below 4.10% — watching …

… momentum hookin’ higher SO rates confronting that ‘fork in the road’ Yogi spoke of … they are going UP OR they are going to need to spend time at a price

… hunting for some clarity and the hunt continues … Sorry. Not sorry. Perhaps if the guy with the boat has some answers…

NEXT UP … Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, here a few things which stood out to ME from the inbox … things you might ought to consider ahead of this weeks ‘most important CPI ever’ … Yield forecasts are being revised LOWER (BAML), apparently the sky NOT falling (BARCAP), lots of attention TO the TRADE OF THE YEAR (couple years runnin’) as we’re advised to STAY in steepeners (BMO, MS) and SOME are thinkin’ ‘bout BUYIN’ PPI inspired DIP (BMO) if we get one … call it a DIPportunity …

The View: When the noise settles US data the main focus after a noisy week. CPI and retail sales are unlikely to get the market to question focus on soft vs hard landing, which is likely enough to see US 10y settle into a new lower trading range.

Rates: Taylor swiftly rules US: We revise UST forecasts & 10Y trading range lower (3.5-4.25%). Nibble on duration with 10Y >4%, shift long 4.15-4.25%, stay in steepeners. Taylor rule says swift cuts.

… Our forecasts are justified by a shift in view from our US economists to earlier Fed cuts & a lower cutting trough (see: Federal Reserve watch). We incorporate downside rate risks in our forecasts given moderating US economic data & a rate market pushing for a swift cutting cycle.

We flag the following in our revisions: the changes (1) are below the forwards & BBG consensus (2) incorporate a cutting cycle trough in-line with the Fed's end '26 median of 3.1% (3) include 10s30s steepening over time to account for elevated UST supply & a likely slowdown in pension demand as funded status deteriorates (funded status worsens with lower discount rate & recent equity drop).

Technicals: Short term stretched, medium term not Short term stretched, 10y yield bounce to +/- 4.10% reasonable. Reiterate 2024 view of yields up in Q1, peak by Memorial Day, down in H2. Still buy dips / being long

… Zeitgeist: "The Bank will continue to raise the policy interest rate going forward", BoJ July 31st; "The Bank will not raise its policy rates when markets unstable”, BoJ Aug 7th; painfully (biggest FX carry-trade loss since Mar'20 - Chart 3) Wall St has now stopped BoJ hiking; Wall St's Aug/Sept goal now appears to be bossing the Fed into big rate cuts.

… The Biggest Picture: lowest interest rate small businesses can borrow at is prime, and in real terms US prime rate is 6.5%, highest this century (Chart 2);

BARCAP: Global Rates Weekly The sky is not falling

In the US, absent an acceleration in inflation, we think markets will continue to see the easing cycle as having downside asymmetry, which should limit any sell-off. In Europe, we remain bearish on the front end. In Japan, given the overall increase in interest rate volatility, we take a neutral stance on duration.

… We view the modal outlook as still of a soft landing where the labor market normalizes at full employment, inflation gradually declines towards the target and the Fed gradually lowers the policy rate. Current intermediate yields are 30-35bp below the fair levels implied by this modal scenario. However, we see the markets as continuing to put some weight (albeit less so, with the passage of time) on the tail scenario of a hard landing and aggressive cuts, at least until upcoming labor market data show stabilization. Absent an acceleration in inflation, this dynamic should keep a lid on any near term sell-off, though yields should still end up above those implied by forwards…

BMO: Bar is High for CPI (2s10s steepener maintained and lookin to buy dip 10s **IF** PPI surprises to UPSIDE)

In the week ahead, the trajectory of US yields will be contingent on the July core inflation update. As it currently stands, the consensus is for a +0.2% monthly gain in core-CPI – the average estimate is +0.19% and forecasts are in a narrow range of +0.1% to +0.2%. Said differently, the market is particularly vulnerable to an upside surprise on the inflation front following the Fed’s successful messaging of a September rate cut…

… Despite being the middle of August, we anticipate the upcoming week will be well-attended insofar as conviction, flows, and participation …

Position unwinds in equity and FX funders last week triggered high vol and reflexive markets. The speed and size of the current drawdown mark it as the fifth “highest velocity” US equity market drawdown in the last century.

Fed funds pricing implies a recessionary rate-cut cycle, but there are signs the risk asset sell-off may be overdone. We have added long USDJPY exposure to position for a short-term recovery in risk appetite.

US CPI will be the key focus this week where we expect 0.19% m/m and we think asymmetry remains in favour of lower rates in the event of a softer-than-expected print. Elsewhere we expect a dovish tone from UK data, an RBNZ rate cut, but a hawkish tone from Norges Bank given NOK weakness.

… Too far, too fast? At the same time as position unwinds last week, fed funds futures briefly discounted an inter-meeting fed funds rate cut. By the end of the week, market pricing of FOMC rate cuts for this year remains at more than 100bp (compared to 160bp at peak panic on 5 August), and is more than 200bp over the next two years.

At peak panic, the level of rate cut pricing was in line with the out-turn of rate cut cycles over the last four recessions (see Global Macro: Too far, too fast?, dated 5 August). It seems investors are downplaying GDP tracking (the latest Atlanta Fed Nowcast is at an abovetrend 2.9%), instead emphasising the Sahm rule (an indicator which the creator initially designed as a signal for the government to send out stimulus cheques) as a predictor of upcoming recessions.

Does deep rate cut pricing mean a recession is already fully priced in, though? One could argue that policy is more restrictive today than at similar periods in previous cycles and that a recession would therefore warrant a deeper magnitude of rate cuts. We would agree, but nonetheless judge that the burden of proof is on a rapid, significant deterioration in the macroeconomic data to justify the extreme levels of Fed cut pricing observed last week…

DB: Investor Positioning and Flows - Abrupt Cut To Underweight

Aggregate equity positioning plunged this week, falling from a mid-July peak at the top of the historical range (z score 1.00, 97th percentile) to below average or underweight (z score -0.26, 31st percentile). This marked one of the steepest declines in recent years, certainly the sharpest cut since the onset of the pandemic.

Both discretionary investor positioning (z score -0.15, 36th percentile) and systematic strategies positioning (z score -0.05, 38th percentile) got reset this week from elevated levels to slightly below average levels. From a fundamental perspective, aggregate equity positioning is now in line with a sharp slowing in earnings growth to the low single digits down from the 11% yoy we just got in Q2. On the systematic side, if vol remains elevated, it will pressure their positioning in equities further, though their sensitivity to market selloffs has declined.

Across sectors, positioning in MCG & Tech continued to get cut and is now in line with the deceleration in Q2 earnings growth for the group, whereas that in Utilities and Real Estate raced ahead.

Despite the market turmoil, inflows to equities continued for a 16th straight week, actually picking up from the prior week, while inflows to bond funds slowed.

MS: Risk Reversals | Global Macro Strategist (stay in 2s20s steepeners)

Better-than-expected US data saved global risk markets from a continued deleveraging.The rebound in risk sentiment reversed some of the repricing in central bank policies, yield curves, and exchange rates, but not all. We continue to advise a defensive stance and staying with UST curve steepeners.

…Interest Rate Strategy United States We discuss the continuation of the Treasury curve steepening trend. We think the 20y new issue and 30y TIPS reopening, coming just before the Jackson Hole Economic Symposium and Chair Powell's opening remarks, could help the trend continue. We continue to suggest UST 2s20s yield curve steepeners.

… We arrived at our decision to sell the 20y point on the curve, instead of 10s or 30s, given its then-recent outperformance on the 10s20s30s butterfly. As yields subsequently fell and the curve steepened, the 20y point cheapened - adding even more steepening pressure to the 2s20s curve…

Given Treasury's recent guidance that current coupon sizes would be maintained for "at least the next several quarters" and continued large deficits, we don't expect comments from former Treasury Secretary Mnuchin about the viability of the 20y bond and the upcoming election to affect its performance or the yield curve shape.

With labor market data having showed some "unexpected" weakening since the July FOMC meeting, we think investors will contemplate more dovish remarks from Fed Chair Powell than what he delivered at the July 31 press conference. This idea should keep investors discussing a 50bp rate cut on September 18.

Even if Powell downplays a 50bp rate cut at Jackson Hole, important data remain on the calendar which could change his mind. The data include the second release of 2Q24 GDP and July PCE inflation (August 29-30), JOLTS (September 4), August payrolls (September 6), August CPI (September 11), and August retail sales (September 17). We continue to suggest Sep/Nov FOMC OIS flatteners.

MS: Friday Finish – US Economics: A slowing, not a slump: what we're watching

We expect a moderate slowdown, and the Fed cutting 25bps in September. But the burden of proof is on the soft landing. Last week's data suggested a soft landing; this week's data look less sure. We list the major economic events between now and the next FOMC, with our expectations.

… We expect the trend for disinflation to continue, with core CPI at 0.19%, a modest bounceback from June’s weak print. In particular, we expect housing inflation to be around three-tenths, but that component is in the process of inflecting down. Overall, inflation data pose a two-way risk: a high reading could prompt fears of stagflation, while a low print could give more breath to the hard landing narrative. CPI Preview: The Trend Continues…

MS: Sunday Start | What's Next in Global Macro: On Tenterhooks

… In our view, at the core of the market volatility is the changing market narrative about US economic growth – though it bears noting that our economists’ view of the outlook is unchanged, as we discuss below. While there have been downside surprises in the data over the last few weeks, such as the latest ISM Manufacturing PMI, the across-the-board softness in last Friday’s US employment report was the catalyst for the latest gyrations, bringing the risks of a hard landing into focus and, by extension, the Fed’s path for monetary policy. This contrasts with the particularly rosy thesis that had been baked into market prices, where valuations were already stretched. Market pricing of the Fed's rate cuts this year has changed dramatically yet again, from under two 25bp cuts about a month ago to now over five, with an over two-thirds probability of a 50bp cut at the September meeting…

…What happens next? While risk markets have reversed some of the losses and Treasuries have given up some of the gains, we expect markets to remain on tenterhooks until data emerge that either confirm or reject the soft-landing/hard-landing scenarios for the US economy. Every incoming data point, particularly related to the labor market, will be under the microscope. We will also pay close attention to the robust functioning of the funding markets, as well as capital market access to companies for credit. Thus far, the funding markets have remained intact, and some IG bond transactions pulled from the markets earlier in the week have returned and been well received – the best day year to date for IG bond supply (US$30 billion+) was recorded this week. We will keep you abreast of developments.

Treasuries experienced a perfect storm over the past two weeks, with investors likely to remain focused on carry trade unwinds, labor market and growth data, inflation, and geopolitical risks in the weeks to come.

Markets will remain worried about the risk to a 50bp cut in September and intermeeting cuts, though the pricing for both has receded significantly from recent highs. A faster pace of Fed rate cuts also remains a worry, and we expect the Fed to cut rates by 25bp at each meeting starting in September until rates reach neutral at 3% by late-2025.

If economic growth begins to slow sharply, we see a significant risk of the market's terminal rate pricing declining sharply from 3.2% today. This would likely drive longer-dated yields lower in tandem.

While we expect 10y rates to finish 2024 at 3.4% and 2025 at 3%, yields may have moved too far too quickly. We continue to favor buying dips, but prefer to wait until more favorable levels to re-enter longs. We remain in 5s30s steepeners, and don't expect the curve to fully retrace recent steepening.

…Topic of the Week: Have Lower Bond Yields Started the Easing Process Early?

A monetary policy pivot looks to be forthcoming. A move down in long-term interest rates has raised hopes that the easing process may already be under way. Unfortunately, lower mortgage rates have yet to result in a meaningful pickup in the mortgage demand, one sector of the economy most likely to benefit from reduced rates…

… AND more. MUCH, much more…

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Bonds Rallying? Buy Real Estate (08-10-2024)

… Here is a look at those multi-year bases in bonds and real estate. Notice how they look the same:

If these resistance zones are cleared, the path of least resistance for both these asset classes shifts higher…

Jobless claims declined this week, the Atlanta Fed GDP for Q3 currently stands at 2.9%, and the Dallas Fed weekly GDP indicator is currently 2.2%.

The bottom line is that there are still no signs of a US recession, and the US economy is doing just fine with steady growth in daily and weekly data for restaurant bookings, air travel, hotel bookings, credit card data, bank lending, Broadway show attendance, box office grosses, and weekly data for bankruptcy filings trending lower, see our chart book with indicators updated as of August 10.

In short, Fed pricing is wrong, and the market is making the same mistake it made at the beginning of the year.

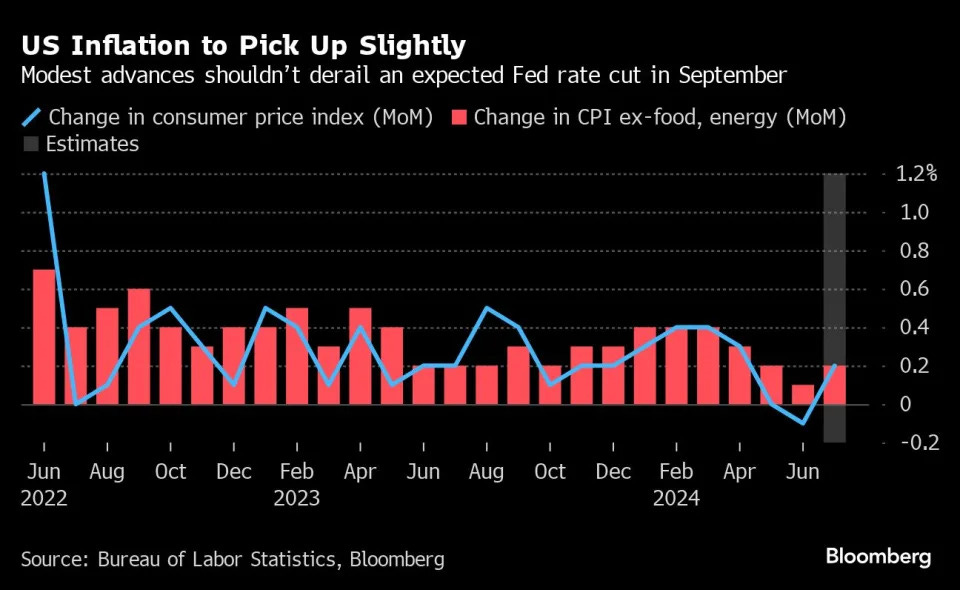

Bloomberg: Small US Inflation Pickup Won’t Derail a Fed Rate Cut in September

Easing pressures have started drumroll toward US rate cuts

UK, China data due; Norway, New Zealand may keep rates on hold

US inflation probably picked up modestly in July, but not enough to derail the Federal Reserve from a widely anticipated interest-rate cut next month.

The consumer price index on Wednesday is expected to have risen 0.2% from June for both the headline figure and the so-called core gauge that excludes food and energy. While each would be an acceleration from June, the annual metrics should continue to rise at some of the slowest paces seen since early 2021.

The recent easing of price pressures has bolstered Fed officials’ confidence that they can start to lower borrowing costs while refocusing their attention on the labor market, which is showing greater signs of slowing…

StockCharts: S&P 500 Teetering On 100-Day Moving Average Support

… Until the index breaks above the 5400 level, you can't call this week's price action a bullish rally. All the more reason to watch the price action in the S&P 500.

CHART 1. DAILY CHART OF THE S&P 500. The index ended the week closing above its 100-day moving average and its 50% Fibonacci retracement level, but it's too early to call this a bullish move.Chart source: StockCharts.com. For educational purposes…

… Inflation Data: What To Know

With rate cut expectations on the radar, you'll want to stay on top of next week's inflation data. The Federal Reserve Bank of Cleveland estimates a year-over-year percent change of 3.01% for headline CPI and 3.33% for Core CPI. If the data shows that inflation is coming down as it has been in the last few months, investors could sigh a huge relief. Conversely, if the data comes in hotter than expected, it could throw things off. But that's unlikely since a rate cut in September is very probable. That's not to say it's not possible, though.

Which direction will TLT move? If the inflation data supports a September rate cut, then TLT will move higher, possibly before the report is released.

Another note is that the CME FedWatch Tool shows the probability of a 50 basis point rate cut in September at 49.5. That's a significant drop from the end of last week, when the probability was close to 90%.

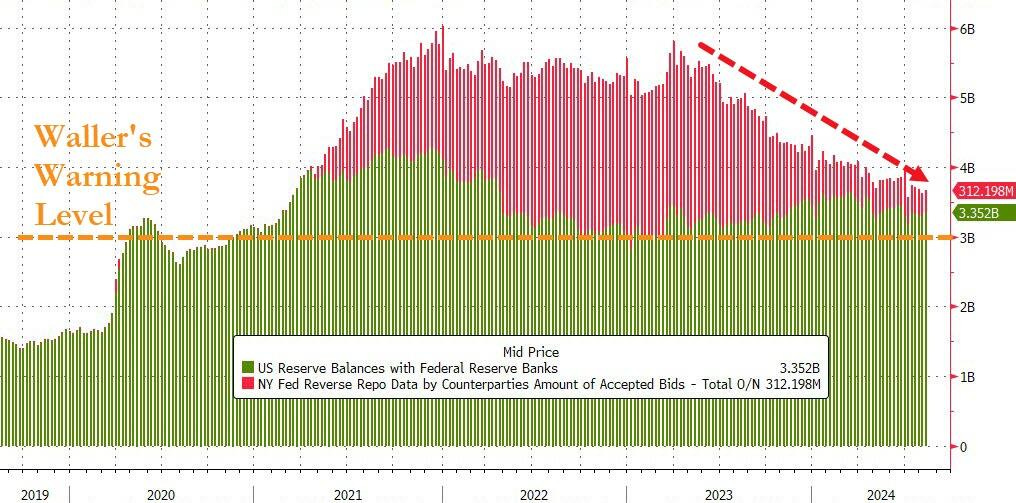

ZH: Investors Flooded Into Money-Market Funds & Bank Deposits As Markets Crashed (update TO what was noted / passed on / mentioned HERE)

Money-market fund assets rose to a fresh record ($6.19TN) as a global selloff in risk assets earlier in the week sent investors flying into cash. About $52.7BN flowed into US money-market funds in the week through Aug. 7, the largest weekly inflows since the period ended April 3 (Tax-Day prep)...

… Reserves are closing in on the $3 trillion level Federal Reserve Board member Christopher Waller has touched upon as the lowest comfortable level of reserves, i.e. the level that funding problems could manifest.

The RRP represents a sort of buffer on top of the current level of reserves, as (principally) money market funds can draw down it, adding to reserves in the process.

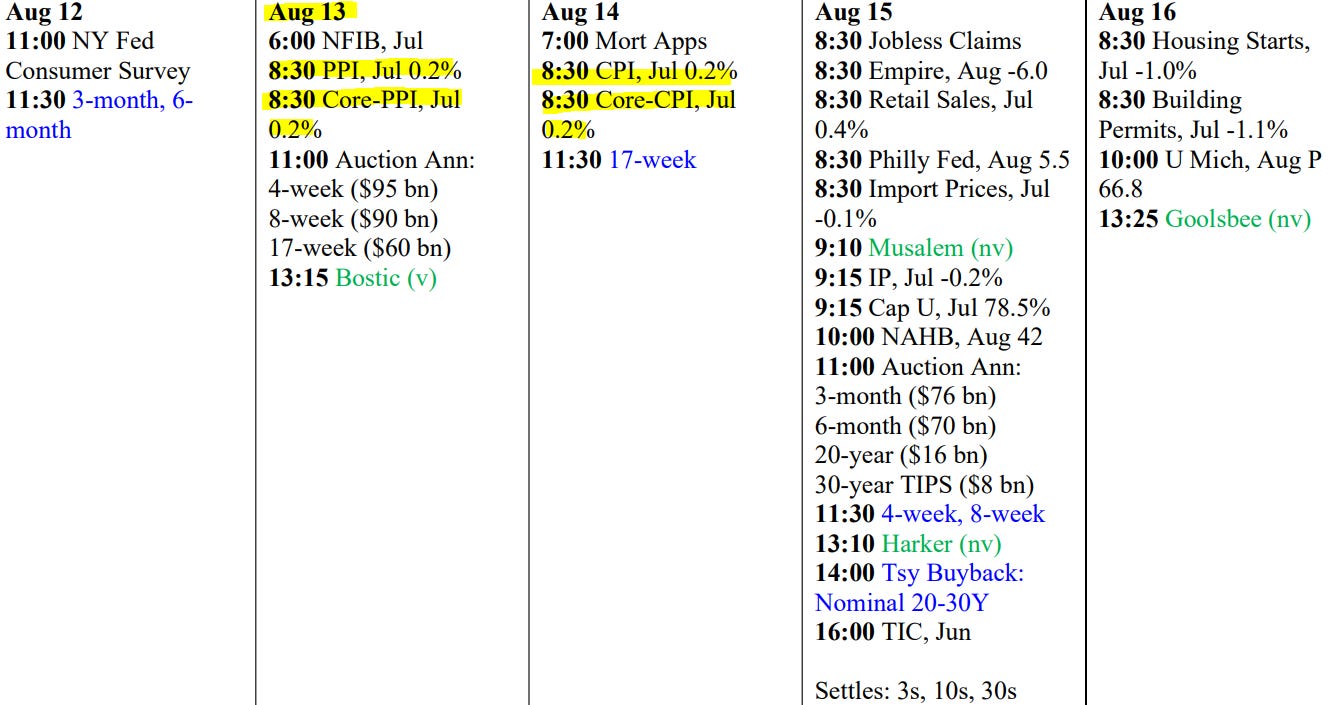

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

I'm not much for reading at the moment, but checking in. I've completed my own 20 yr There and Back Again Bilbo Baggins journey. I awake in my long neglected home after over 14 long yrs. I've Followed My Heart, and rescued my property before the pyromanic tweaks who lived here the last 4 yrs burnt it down. There's a lot of work ahead, but the rehabilitation of my property, and my heart, has begun. I'm glad you're a part of my journey Thank You.

{kind=link}

I'm not much for reading at the moment, but checking in. I've completed my own 20 yr There and Back Again Bilbo Baggins journey. I awake in my long neglected home after over 14 long yrs. I've Followed My Heart, and rescued my property before the pyromanic tweaks who lived here the last 4 yrs burnt it down. There's a lot of work ahead, but the rehabilitation of my property, and my heart, has begun. I'm glad you're a part of my journey Thank You.