weekly observations (04.28.25): NFP, reFUNDING precaps, some stopped OUT of flatteners, stayin' (long belly), others staying IN steepeners; foreigners still buy

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

DEESCALATION (JPOW, China) has helped rates stabilize and 10s found themselves back in to the middle of the range and the curve remains a directional trade …

As Trump’s 90-day pause on many tariffs continues and the trade war rhetoric persists, investors are surely not the only ones counting the days. Jay Powell’s countdown clock says 385 days left until his Liberation Day! Get it?

Episode 321: "Countdown is on!" is now available. This week, the team discusses Trump's recent efforts to de-escalate the trade war and walk back speculation that he'd attempt to fire Powell. We also contemplate this week's payrolls report, and of course, the ongoing specter of a foreign buyers' strike as the Refunding auctions quickly approach…

… OR see below for some thoughts / excerpts from BMOs weekly. Now, jumping into a couple / few thoughts of my very own …

First UP, 30yr yields DAILY continued to lean bullishly (and once and awhile a post ages well) and while one day in a row does NOT a pattern make, lets have a look at the WEEKLY as we prepare to have Bessent put the FUN back in reFUNDING middle of the week which will ALSO have month end (MS has some thoughts below on below avg extension) and by weeks end we’ll all be ready to review payroll …

Bonds. LONG bonds with (red)resistance TLINE redrawn just a touch …

30yy WEEKLY: 5.00% does appear to show up quite a bit and act as SUPPORT …

… and as far as resistance goes, well, somewhere down ‘round 4.50% would seem to be worth watching … and as we wait / watch, i’ll note medium term (weekly) momentum does NOT appear to offer as much of a signal as yesterday’s DAILY charts did / do …

… In as far as a couple / few other things ‘in the price’ …

ZH: Brainwashed Democrats Continue To See Imminent Inflation-pocalypse; But UMich Sentiment Improved Intra-Month

… still thinking by weeks end there was further reduction in tensions and obvious question comes to mind — is DJT tellin’ the truth about talks or not …

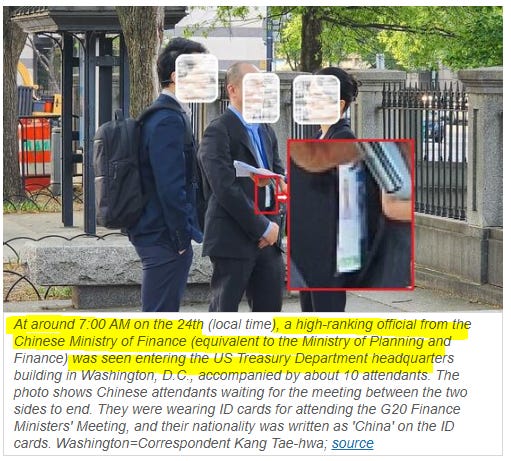

ZH: Chinese Delegation Spotted Entering Treasury Department, Demands Photos Be Deleted: Report

… However, in its overnight report, JoongAng Ilbo confirmed that at around 7 am ET on the 24th, a high-ranking official from the Chinese Ministry of Finance entered the Treasury building located right next to the White House in Washington D.C. accompanied by about 10 attendants.

…As for why China has been extremely secretive about the process, the source told the South Korean outlet that “since this tariff war is unfolding as a battle of pride with the leaders of both countries directly appearing, it may not be easy to create some kind of ‘win-win structure." He added that "the fact that China visited the U.S. Treasury Department in person could be an extremely sensitive issue for China."

Remarkably, Trump may have been telling the truth... again.

… Right about everything, then? Hard to dismiss but moving on TO … weeks end …

ZH: 'Deal, Or No Deal' - Big Week For Stocks, Bonds, & Bitcoin Despite World Questioning Trade-Talks

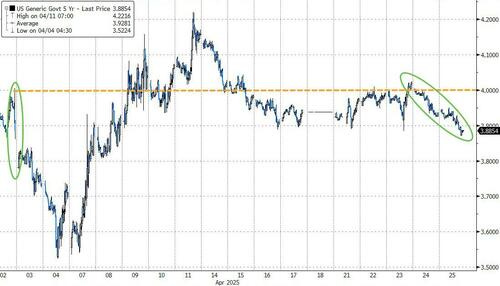

…Treasury yields were all lower this week (from Thursday's close) with the long-end outperforming...

With the 5Y yield back below 4.00% (which coincided with Liberation Day levels)...

… Alrighty, then. 5s back BELOW 4%, 10s finding middle of their range and long bonds, well, taking a step back from the edge of the cliff…

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox …

Best in show — trading UPDATE — stopped OUT for loss on 2s10s flattener and bot dip in 5s, long vs 4.02 (4.17 stop, 3.71 tgt) … read all ‘bout it and much more (like the part about how foreigners ARE NOT SELLING USTs…)

In the week ahead, the US rates market will have the benefit of a set of inputs that have historically held the potential to trigger significant price action. First and foremost, it is nonfarm payrolls week and investors will get an update on the state of the labor market on Friday morning. Expectations are for an uninspired increase of +130k in headline NFP with an unchanged UNR at 4.2%. It’s April data, and while there was a lot of White House drama during the month, we maintain that it is still too soon for the uncertainty inspired by Trump’s trade war to impact the realized employment figures. The soft, survey-based measures of confidence and sentiment have already dimmed in response to the escalation of tensions between the US and, frankly, most other nations with an emphasis on China. The missing component is flow-through to the hard data. Unless and until evidence of slowing growth becomes evident in the marquee data, both investors and the FOMC will retain a wait-and-see posture as it pertains to the ultimate fallout from the trade war.

The market will also see the May Refunding Announcement. Recall that Bessent had only been in his new role as Treasury Secretary for a few days when February's refunding was announced – and it retained the ‘several quarters’ language…

…Perhaps the most politically-relevant release comes in the form of Wednesday’s release of Q1 real GDP…

…Our first chart offers a comparison between the year-to-date performances of US Treasuries and that of government bonds for the rest of the G7 (Canada, France, Germany, Italy, Japan, and the United Kingdom). Up until President Trump's 'reciprocal' tariffs announcements on April 2nd, Treasuries and the 'G6' (G7 ex-US) had performed largely in unison with both the Bloomberg US Treasury Index and the Bloomberg Global G7 ex-US Index up +3.2% YTD as of April 1st. Trump's tariff announcements triggered a selloff in Treasuries that severed their former correlation with government bonds in the rest of the G7, as the 'G6' rallied sharply. For context, as of April 24th, Treasuries were up +2.7% YTD whereas G7 Bonds ex-US were +9.1% YTD.

The underperformance of Treasuries versus their global peers can be attributed to a handful of factors, one being that we've seen a pandemic-style dash-for-cash that triggered further position unwinds at a moment in which uncertainty was peaking. There's also been fears of a foreign buyers' strike, although there's an argument to be made that selling was primarily by domestic investors who feared selling overseas. Let us not forget the surge in term premium, as investors have demanded excess compensation for bearing the risks associated with President Trump's erratic behavior at a moment of historically-unprecedented levels of trade policy uncertainty. After all, this chart illustrates one of the biggest macro questions of the moment: will the decoupling between US Treasuries and the rest of G7 government bonds persist or reverse?

Ahead of this weeks NFP data, here’s another precap …

We expect April employment and Q1 GDP data will bear the imprint of the US administration’s economic policies but won’t be conclusive enough to move the Fed off the sidelines.

We look for a 135k gain in nonfarm payrolls and a steady jobless rate at 4.2%, alongside an import-driven stall in GDP growth.

While anecdotes point to a softening job market, an unexpectedly resilient report coupled with rising inflation risks would align with our view that the risks are not wholly one-sided in terms of the direction of Fed policy this year.

A large German operation with a couple updates … one on their BUND yield f’cast and another on (equity)positioning …

In the aftermath of the German fiscal regime change in early March, we revised our year-end 10yr Bund forecast to 3%. This was predicated on a set of assumptions around the: i) ECB policy rate path, ii) term premia and iii) ASW spreads. At that point, one month prior to 2nd April, we didn't expect the US administration to announce the magnitude of tariffs that was delivered, neither the risk-off sentiment that followed as a result of these announcements. We commented on that in our recent piece Four rights, one wrong and four mispricings…

… Summing up all the above, the lower 2025 terminal rate and richer Bund ASW lead to a small 15bp downward revision to our Bund forecast, I.e. ending up with 2.85%. Maintaining a medium-term neutral rate of 2.25% and unchanged term premia assumptions keep the Bund yield forecast above current levels and forwards. Moreover, on both these two fronts, we see upside risks. Uncertainty around the final level of tariffs remains, while potential reallocation flows out of USTs into EGBs pose downside risks to our forecast.

25 April 2025 DB: Investor Positioning and Flows - Discretionary Investors Back Near Neutral

Equity positioning has risen over the last two weeks and is back within its typical range but still near the bottom of it (z score -0.95, 11th percentile). There is a wide divergence between the positioning of discretionary investors (z score -0.16, 35th percentile) which has risen very close to neutral and that of systematic strategies (z score -1.6, 6th percentile) which is still very low.

Discretionary investors have moved their positioning dial towards expectations of a policy relent rather than rising macro concerns, especially as hard data continues to hold firm so far (Caught Between Macro Concerns And Policy Relents, Apr 11 2025). Following the 90 days pause announced 2 weeks ago, this week saw several additional attempts at de-escalation by the administration. This has seen discretionary investors move from being significantly underweight to now nearly back to neutral. A move further up to overweight is unlikely in our view absent more concrete signs of a trade policy relent. The S&P 500 is now close to the upper end of the wide range of 4600 to 5600 that we see till we get a relent (Tariffs And Equities: Lowering Estimates And Target, Apr 23 2025).

For systematic strategies, the key driver of low positioning is very elevated vol. Vol is in line with daily moves well above 1%, and so far, the market has been obliging. However, if volatility and daily ranges subside, systematic strategies will begin to raise positioning. Vol Control funds, for example, in our reading will buy equities even with market selloffs of -3%, as they are not enough to justify vol exposure at the current low levels .

Inflows into equity funds have continued to be strong but gravitating away from the US and into the rest of the world. Equity funds ($9.2bn) saw their 4th straight week of inflows. However, US equity funds (-$0.8bn) saw modest outflows again (-$5.7bn last week), following huge inflows ($33bn) in the week immediately after the Apr 2nd announcement. Europe funds ($3.4bn) meanwhile continue to see large steady inflows as do Japan ($1bn), EM ($1bn) and broad-based global funds ($5bn).

Buyback announcements in the Q1 earnings season so far have remained very strong totaling $150bn over the last month. While the aggregate is dominated by a few large high-profile companies, it is notable that on average the announcements amount to over 8% of company market cap.

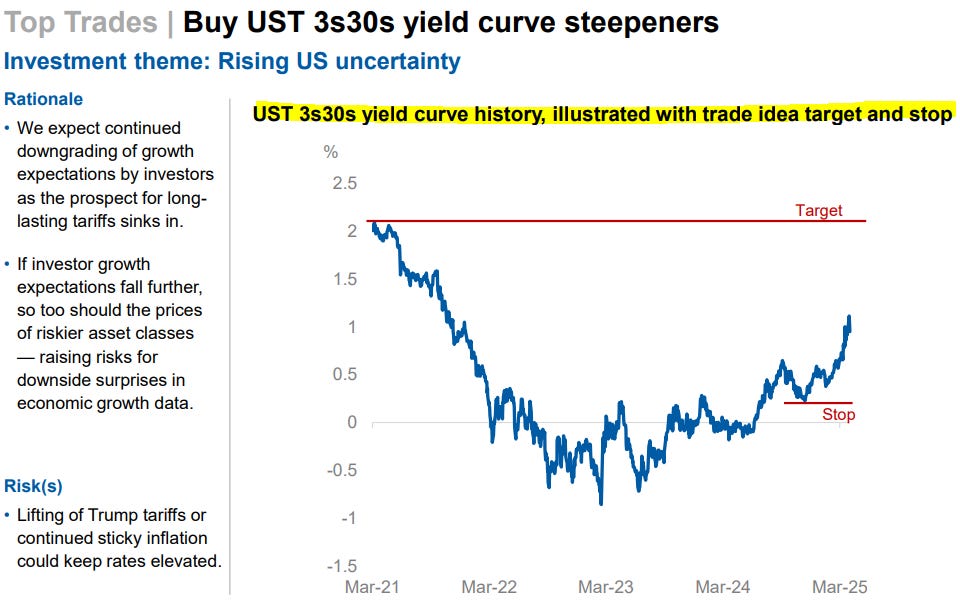

AND … another most excellent weekly where this shop stays in 3s30s steepeners (and more) …

April 25, 2025 MS: Throwing Nasty Curve Balls | US Rates Strategy

Not even Cy Young could throw a curve ball that twisted as much as the Treasury curve since April 2. The yield curve rarely twists to this extreme. We don't think the twists continue, but we think the yield curve continues to trend steeper. Use bouts of flattening to add to or enter steepeners.

Key takeaways

Since April 2, the Treasury yield curve twisted noticeably on 17% of the subsequent trading days. Since 1980, it only twists on 1% of trading days.

The subjective probability-weighted average of four policy paths laid out by our economists suggests policy rates could fall below 2.25-2.50%.

We decompose yield curves into rate expectation curves and term premiums curves to inform our lofty targets on yield curve steepeners.

The 2s10s Treasury curve could steepen another ~100bp, with rate expectations contributing 70bp and term premiums contributing 30bp.

We continue to suggest 3s30s Treasury curve steepeners and 1y1y vs. 5y5y term SOFR steepeners. March JOLTS and April nonfarm payrolls on tap.

…Exhibit 2: Percentage of daily UST 2s30s yield curve changes over previous 6 months that twist*

Source: Morgan Stanley Research, Federal Reserve, Bloomberg * We define a “twist” as a move where the 2y yield falls (rises) and the 30y yield rises (falls) on a day where both yields need to move by at least 4 basis points in order to reduce noise from affecting the twist count…

…Over the past year - until April 2 - longer-dated Treasury yields moved in sympathy with how the market priced the trough policy rate (see Exhibit 8). But since April 2, the relationship broke.

Exhibit 9 shows a regression between the market-implied trough policy rate and the 10y Treasury yield.

Exhibit 10 shows the residual of the regression. At point point, 10y Treasury yields traded nearly 50bp higher than what the previous relationship with market-implied trough rate suggested.

We interpret the residual from that historical relationship as a risk premium that investors demanded, given uncertainty over trade policies between the US and its trading partners. Since the US administration announced the 90-day pause on April 9, the risk premium subsided - though not entirely.

…Exhibit 10: Market-implied trough fed funds rate vs. 10y US Treasury yield regression residual

Here’s a(nother) note from same shop … a reFUNding preview …

April 26, 2025 MS: May US Treasury Refunding Preview | US Rates Strategy

May refunding comes at a pivot point on the direction of travel for yields. We expect no changes to coupons, with risks skewing smaller, not larger, while discussions on the buyback program are likely. Auction data do not corroborate "protest sale" narratives. Odds of late 3Q x-date rise.

Key takeaways

We do not expect Treasury to change current coupon auction sizes over the May refunding quarter, but risks skew toward smaller, not larger, auction sizes.

Growth in stablecoins represents an unconventional source of structural demand for T-bills and is another reason that supports more, not less, bill issuance.

We think constraints on Treasury buybacks limit their immediate positive impacts on market liquidity, but see discussion on a buyback program revamp as likely.

Robust tax receipts increase conviction in a late August – early September x-date, but tariff revenue and restart of student loan repayments skew risks later.

Granular Treasury investor auction allotment data do not support popular notions of foreign investor “protest sales” of Treasuries in response to tariffs.

AND this firms cross-asset views always funTERtaining …

April 25, 2025 MS: Cross-Asset Playbook: Knockin’ On (Safe) Haven’s Door

Macro – Tariff Shock and Awe Tariff policies leave US at the edge of a recession, but reacceleration in prices means the Fed remains on hold this year. Europe faces a hit to growth from weaker global demand and subdued investor sentiment. China stimulus can only partially offset tariff impact on growth.

Markets – Nowhere to Hide...? Uncertain macro means risk assets should be cheaper. But the recent sell-off has been so severe and sentiment turned so bearish that we expect some relief over the short term. That said, shifting patterns in fund flows and correlation show markets are grappling with what “quality” in “flight-to-quality” mean. The debate around USD assets’ safe-haven status, who holds USD assets, and how that may impact outflows will likely remain, as will recession concerns.

Strategy – Stay Nimble, Look for Dislocations OW fixed income but pare back exposure in loans while adding to EUR fixed income. We maintain EW global equities, but trim allocation to Japan and continue to have a slight preference for the US as we see the region tactically outperforming. We continue to build cash for opportunities created by market dislocation

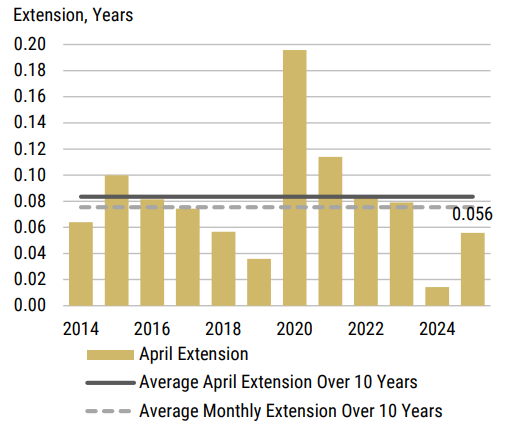

With 3s30s in mind a look ahead to index EXTENSIONS in week just ahead …

April 23, 2025 MS Global Rates Strategy: April Index Extensions

Eurogovies extend by 0.106y, in line with April avg, higher than monthly avg; USTs 0.056y, lower than the historical avg in April; UKTs to extend by -0.019y, lower than monthly avg; Eurolinkers extend by 0.359y, higher than average; TIPS to extend by 0.090y relative to April avg of 0.023y.

…We expect the 1y+ UST index to extend by 0.056y, compared to an average April (0.083y) and an average month (0.075y) – Exhibit 8 . A total of US$315 billion of supply (offered amount) will affect the extension, and US$216.9 billion market value of bonds will fall out of the index. The monthly issuance of 2y, 3y, 5y, 7y, 10y, 20y, and 30y will affect the respective maturity-wise indices.

Exhibit 8: 1y+ US index extension: Lower than monthly average

Finally, an economic week ahead to browse ahead of NFP (and much more) …

April 25, 2025 MS: US Economics Weekly: A race against time?

The US economy may be in a race against time: will trade tensions dissipate quickly enough to prevent economic damage from a sharp reduction in trade between the US and China? We think they can, but we don't think that conclusion is obvious.

Key takeaways

Increased blank sailings suggest tariffs are already reducing trade volumes between the US and China.

We present our estimates of the direct and indirect effects of tariffs on various CPI subcomponents.

We think the advanced estimate of Q1 US GDP growth will show a stall, with the drag from net trade offsetting strong domestic demand growth.

We expect payrolls rose 160k in April and the unemployment rate was unchanged: no sign of a sudden slowdown.

Here’s another weekly I read and don’t always pass along … From across the pond, this British shop talking about Fed and our dual mandate …

25 Apr 2025 NatWEST: US Weekly Economic and Strategy Brief

…Inflation Mandate as Policy Keystone: In debt markets credibility is ultimately about willingness and ability to make full and timely payment of contractual obligations. Credibility with respect to nominal obligations is what is conventionally referred to as “credit”. Credibility with respect to real obligations is a function of the market’s subjective estimate of the probability of being repaid in real terms. Real credibility is unique to the sovereign sector in that the sovereign can influence inflation through fiscal policy, regulatory policy, and selection of key actors in monetary policy formation.

… Dollar assets generally - and the Treasury market in particular - are currently afflicted with challenges in both nominal and real dimensions. We argue that real and nominal credibility are two sides of the same coin; that is, rising inflation is a result of a spending trajectory that is bumping up against the Treasury’s intertemporal budget constraint…

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

A question all are asking and an answer from one of the sharper tools in the shed …

April 26, 2025 Apollo: How Are US Consumers and Firms Responding to Tariffs?

The chart book available here looks at how US consumers and firms are responding to tariffs.

For companies, new orders are falling, capex plans are declining, inventories were rising before tariffs took effect, and firms are revising down earnings expectations.

For households, consumer confidence is at record-low levels, consumers were front-loading purchases before tariffs began, and tourism is slowing, in particular international travel.

…The share of credit card accounts only making the minimum payment is rising

Not many better than Brent Donnelly and team at Spectra … Friday speedrun’s best, delivering a message, funny, to the point AND visuals …

Rollah Coastah NASDAQ sharply unchanged in quiet trading this month.

A macro trader and an economist brace for volatility

…Global Macro Holy crap. What a month. Some measure of calm has been restored to markets this week as the market digests the new American policy and the economic tsunami that may or might not be on the horizon (depending on who you ask) has yet to appear. The next 3 months will deliver critical information as to whether or not the United States economy can survive a trade embargo with China and whether or not the global economy can muddle through.

The soft (sentiment) data is uniformly morose as investors, consumers, and businesses are frozen by policy uncertainty. The 90-day tariff pause put a bottom under stocks and now we await the July 8 pause expiry and the influx of hard (real) economic data. There is a major issue in determining what the heck is actually going on in the economy now because while hiring and investment freezes will lead to some contraction in economic growth, the first impact will be a rush to buy goods before the tariffs hit. Therefore, you could actually see a string of strong economic data points that show a mini-boom in consumption.

Therefore, economic data releases like Retail Sales and Personal Consumption are effectively meaningless and could be subject to the Roller Coaster Effect, a term I just made up right now while typing this. The Roller Coaster Effect stipulates that when faced with known and imminent price increases, consumers will buy whatever they can and businesses will build inventories as much as they can reasonably afford to do so. Once ships arrive with tariffed goods, nobody will want those goods because a) they already bought what they needed and b) those goods are now more expensive than they used to be. Elasticity and substitution effects will dampen price rises but will not fully absorb them.

The Roller Coaster Effect

How do you trade or invest in the meantime? Do you position for a recession now? Do you wait for better levels because 401k money might keep flowing in and might push stocks higher now that the macro community is aggressively short? Do you just wait and see?

It’s tempting to front run the recession, but even if there is a recession, keep in mind that even when things were quite clearly not looking so good in 2007 and in February 2020, the stock market subsequently posted a new all-time high just to inflict maximum pain on both bulls and bears. In 2007, it was EXTREMELY clear that the financial system was wobbling and yet stocks remained resilient.

And in 2020 the buildup was much shorter, but there were equal levels of disbelief as the economic tsunami was roaring across the world and stocks were making new all-time highs…

…Interest Rates The bond vigilantes got tired and took their ball and went home for a bit. They could be lurking like Slim Shady but they aren’t selling. Bonds are up this week and US yields are getting close to the bottom of the recent range again. The next chart shows US 10-year yields and you can see that there was a messy 4.10%/4.40% range for weeks before Liberation Day. Then, yields tanked because everyone thought tariffs are bad for growth. Then, yields ripped because everyone thought tariffs are bad for growth and good for inflation and will lead to a worsening of the US fiscal position. The flight from the US was exacerbated by the long list of countries and investors frightened by the huge tariffs.

Then, in reaction to 10-year yields getting the yips, Trump announced another policy U-turn and the market went right back to where it was before. I think the 4.10% / 4.40% equilibrium zone should hold until we get some clarity on the economy. That could be a while.

There is no end in sight to massive US deficits as DOGE has failed to make a dent in spending, entitlements are off the table, and defense spending is about to increase substantially. As such, the bond vigilantes will remain on guard and if they need to, they will force another US government policy change…

… Check out the site, sign up for your very own subscription OR never fear, I’ll monitor and pass along the rates-relevant tidbits !!

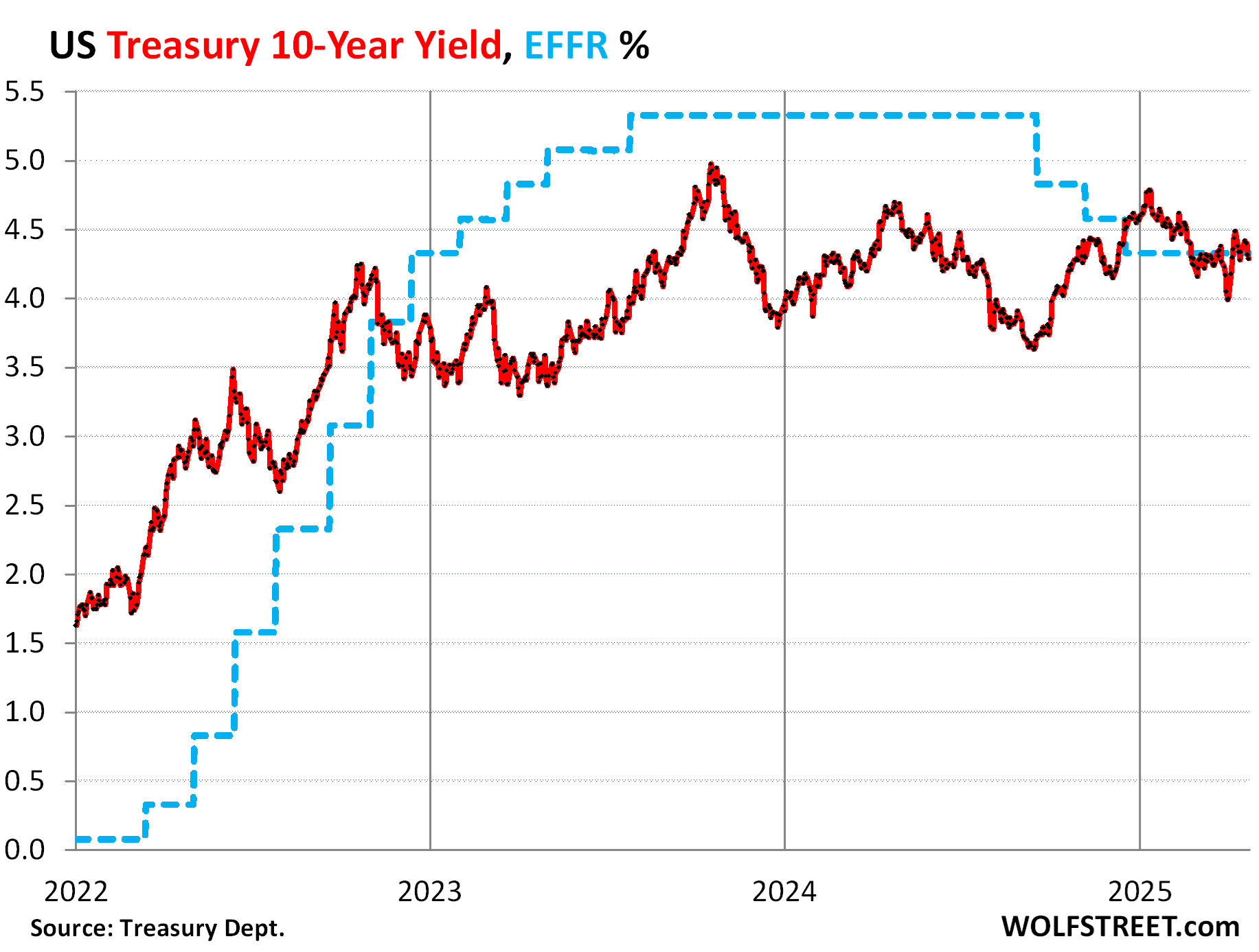

Finally, 10s (back)below FF …

Apr 26, 2025 WolfST: 10-Year Treasury Yield Re-Dips Below EFFR, Yield Curve Sags Deeply in the Middle, Dollar Bounces Back into 3-Year Range

Turns out, demand from foreigners for Treasury securities at the auctions was just fine.

The 10-year Treasury yield dipped to 4.29% on Friday, where it had been in mid-March, despite the gyrations in between, and ended up below the Effective Federal Funds Rate (EFFR), currently at 4.33%, which the Fed targets with its policy rates (blue). Spikes followed by plunges, and vice versa, in an always edgy bond market, are part of the deal with the 10-year yield…

…Foreigners kept buying Treasuries just fine.

When the 10-year Treasury yield snapped back 50 basis points in early April – after having plunged by 80 basis points from January through April 3 – rumors started flying that foreigners weren’t buying Treasury securities at the auctions anymore to punish the US for the imposition of tariffs, or whatever.

Those were fake rumors, as we now know from the Auction Allotment Report released by the Treasury Department this week. Foreigners kept buying the US debt just fine.

Foreigners bought 18.4% of the 10-year Treasury notes issued at the auction on April 9, following Liberation Day. That was a much larger portion than they’d bought in March (11.9%), a smaller portion than in February (20.6%), and a much larger portion than in January (10.5%), December (10.4%), and November (13.2%).

The portion of the 30-year Treasury bonds that foreigners bought at the auction on April 10, at 10.6%, was roughly similar to the portions in the prior five months – a little larger than in three, a little smaller than in two.

Zooming out, these gyrations barely register. In the grander scheme, the 10-year Treasury yield has been trading fairly closely to either side of the EFFR since late February, and has been in the same range for the past two years.

Given the current rates of inflation, and where they threaten to go, and given the risks with 10-year duration, the 10-year Treasury yield remains relatively low and presumably unattractive – and yet investors, including foreign investors, kept buying them, and this massive demand is why the 10-year yield is so low (and prices so high):

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,