while WE slept: "Bonds trade rangebound as participants await further tariff updates..."; that in mind, Bloomberg.com, "Bloomberg: China May Exempt Some US Goods From Tariffs as Costs Rise" ...

Good morning … what did I miss? Answer: not much — more of the same? A quick look at 30yy — the most volatile of securities (most of the time) would suggest bullish lean in place, remains so …

… momentum (stochastics, bottom) continue to put ‘PAID’ to the current bid and not sure I missed something which would suggest this is aggressively incorrect … not a bad way to roll into the weekend…

Now, in as far as what I actually missed, well … First answer(s) a couple things I was reading last night to get caught up … from Wednesday …

ZH: Solid 5Y Auction Stops Through Despite Another Sharp Drop In Foreign Demand

CalculatedRISK: Fed's Beige Book: "Economic outlook worsened considerably"

ZH: Beige Book Finds Inflation Mentions Tumble To 3 Year Low, Biggest "Headcount Reductions Are In Government Roles"

ZH: Headline Roulette Returns To Wreak Havoc Across Markets

… One veteran trader offered this admittedly tongue-in-cheek recap of the chaos that started the day...

Trump says something, stocks spike;

WSJ repeats what Trump said, stocks spike more;

Reuters waters-down what WSJ reported, stocks drop but then rebound;

Finally, Trump reverts back to square one, market no longer cares.

In today's case, it was a combination of Bessent and Trump comments that prompted a spike after the close last night (Trump - I was never gonna fire Powell, and China tariffs won't stay at 145%;, prompted another spike this morning (WSJ -White House considering cutting tariffs to China and Why Trump decided not to fire Trump - ring a bell).

Then Scott Bessent refuted by confirming that there has been no unilateral offer from Trump to reduce tariffs on China and also that full China trade deal may take 2-3 years (both headlines hit last night as the TsySec released his prepared remarks).

Amid all that, stocks soared over 4% before fading back - AND NONE OF IT WAS NEW NEWS!!!

… AND from yesterday …

ZH: Ugly, Tailing 7Y Auction Sees Lowest Foreign Demand In Over 3 Years

… I’ll leave it be and hope to continue getting caught up and produce something more funTERtaining over the weekend … here is a snapshot OF USTs as of 658a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: Positive China trade reports boost sentiment, GOOGL +5% post-earnings … Bonds trade rangebound as participants await further tariff updates … USTs are flat in what has been a rangebound morning thus far as traders digest the latest Bloomberg reports on China, which suggest China is said to consider exempting some US goods from tariffs as costs increase. UST futures rate in a narrow 111.02+ to 111.09 range at the time of writing; docket ahead is thin.

Yield Hunting Daily Note | April 23, 2025 | DMB Boost, PTY, PCN, PHK, DLY Best Ideas, SWZ Next Moves?

Yield Hunting: First Trust HY Opps 2027 (FTHY): A Better Way To Play High Yield

Yield Hunting: Guest Post: Total Return Securities Fund (SWZ) Quick Update

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

I’ll begin with a review … of the equity market…

25 April 2025 Barclays: Equity Market Review Damage control

Team Trump move to damage control keeps tactical pain trade to the upside post sharp HF/systematic de-grossing. Equities are still trading within our target range, though, as worst case scenario avoided but no major breakthrough yet. 'Sell America' subdued so far, watch hard data & BigTech earnings.

… same shop with a NFP precap …

24 April 2025 Barclays: US Economics: April employment preview: No tariff-related weakness yet

We expect the April employment report to show a 125k job gain, slowing from 228k in March. We forecast a steady unemployment rate of 4.2% and see hourly earnings growing 0.3% m/m (3.9% y/y). Two-sided risks have emerged, with claims data and trade policy uncertainty at odds.

So, I didn’t miss much, according to this next one, from best in biz … ?

Treasuries rallied on Thursday in a move that is consistent with an in-range consolidation far more than it was a new trend. While we’re medium-term constructive on Treasuries as an asset-class and are looking for yields to be lower by year-end, this doesn’t necessitate a straight-shot to 3.50% 10-year yields or beyond. In fact, our highest conviction call is that the longer-end of the curve (10s and 30s) will trade in a range and the market is currently in the process of defining both the extremes and center point of the range. With 10s currently above 4.25%, we maintain that yields are decidedly in the upper half (if not quarter) of the range that will define the balance of the year. Rates in the frontend of the market are well-anchored at the moment, however, at some point in the not-too-distant future, we’re anticipating a Fed pivot that will bring forward investors’ expectations for the timing of rate cuts. But before the inevitable shift in Fed messaging, we anticipate that the wait-and-see mantra will push cut expectations further into the summer months.

We’re cognizant that the market is pricing in better-than-even odds of a June cut at the moment and fully priced for a cut by July. That being said, the market has a long history of simply rolling forward the ‘on-hold’ pricing with the passage of time and consistency of Fed messaging. Said differently, in the absence of more concrete rate cut timing from Fed speakers, we expect the probability of cuts reflected in June and July will drift lower as the meetings approach. Even with this backdrop, it’s safe to assume that the Fed will remain in data-dependent mode with an eye on the evolution of the labor market in particular. Today’s jobless claims increased, but came precisely in-line with expectations and as such, were a nonevent – remaining low in absolute terms as well. Said differently, the Fed has plenty of flexibility to delay the resumption of normalization until the Committee is convinced by the realized data.

Data dependence is by no means a new policy mantra; in fact, it is arguably the Fed’s preferred stance. We’ll suggest that in light of the dizzying array of changes from the White House, Powell’s willingness to wait for the new trade policies to hit the real data carries with it the risk of a policy error in the form of responding (presumably with rate cuts) after the damage has already begun. The FOMC is surely cognizant of this potential outcome, which leaves us with the impression that the Fed’s view is that the ultimate impact of the trade war is so unknown (and unknowable at this stage) that the only prudent approach is to seek confirmation in the hard data. On the margin, this raises the risk that when the Fed cuts, the moves might be larger than the FOMC’s typical quarter-point cuts.

… and as far as aDURable goods data … well, fuhgettaboutit…

24 April 2025 Barclays: Durable goods orders: Ignore the headline

New durable goods orders jumped 9.2% m/m, reflecting a surge in the volatile nondefense aircraft component. Otherwise, orders looked soft in the leadup to Liberation Day, especially for core capital goods, hinting that frontrunning effects may be giving way to tariff-related weakness.

Spread compression OVER … putting some hay in the barn …

We recommend closing our Buy $25mn HYG (rates-hedged with $16mn CT5) / Sell $27.75mn LQD (rates-hedged with $28.75mn CT10) initiated in last Wednesday’s Eyes on iTraxx and CDX indices.

The rationale for closing the trade is essentially the performance of the trade, see Chart 1.

Net P&L: $266k (equivalent to 32bp outperformance of HYG).

…USD rates: Fed uncomfortable as range of risks widens The distribution of risks has widened, with risks largely balanced for rates: The FOMC is in a very uncomfortable position, where a broad policymaker consensus has emerged for soft growth and high inflation. Tail risks of a recession and of runaway inflation are metastasizing. This is in line with our view that the range of potential evolutions for US rates has widened materially, as SOFR option contracts imply more open-ended outcomes. We assign a 25% probability to a significant recession where the FOMC responds with rate cuts. We also assign a 15% probability to a stagflationary environment with unanchored inflation expectations, resulting in at least 100bp of rate hikes – a risk we think is currently underappreciated.

Overall, our baseline is for tariffs to settle in far above pre-inauguration levels but well below current levels (about 16%). In this scenario, we see growth clocking in at just 0.5% y/y in 2025, the unemployment rate rising to 4.6% and inflation accelerating through 4% y/y. This means heightened tension between inflation and employment mandates for the Fed, resulting in an on-hold stance through 2025, mirroring comments from FRBNY President John Williams that there is no need to change policy any time soon. 10y yields have already retraced some of the post-’Liberation Day’ sell-off and sit well within near-term historical ranges.

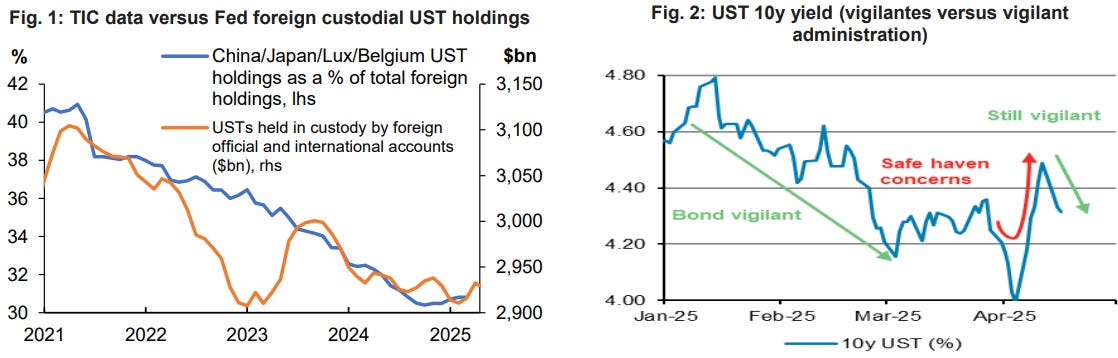

Bond vigilantes emerged, but Treasury looks keen to stabilize term premia: Foreign retaliatory UST selling does not look to be the primary catalyst for the post-’Liberation Day’ sell-off. First, foreign UST holdings are concentrated in the front end and belly of the curve, yet the sell-off was focused at the long end. Second, in the week ended 9 April, USTs held in custody by foreign official and international accounts actually increased marginally. Finally, foreign entities or international monetary authorities are typically grouped as indirect bidders at UST auctions, yet indirect bidding demand was robust across all auctions (particularly 3y and 10y). Instead, we believe the sell-off was induced by an unwind of long swap spread and invoice spread trades. That would explain the temporary pop in repo rates and continued levered fund selling in futures (and cash) which saw a tandem decline in both cash and futures prices relative to swaps.

Although bond vigilantes scored a win last week, the bond-vigilant administration plans to win the long game, showing no signs of backing down. The Fed and Treasury are both aligned with moving quickly on bank deregulation, particularly through SLR relief near term. Treasury also emphasized having a "big toolkit" to defend against bond vigilantes. Secretary Bessent downplayed the recent sell-off in long-end rates and said Treasury can boost buyback sizes to improve UST market liquidity. In March, we concluded that Treasury has the option of pushing out guidance for coupon increases on a rolling basis and delaying the increases through 2027. If Treasury can maintain the optionality to boost liquidity buybacks amid the current deficit path, then they surely can retain optionality for pushing out coupon auction size increases and relying on T-bills in the medium term.

AND … a lowered target made rounds by now and in the case was missed …

23 April 2025 DB: Tariffs And Equities: Lowering Estimates And Target

With the potential impact of the announced tariffs large and likely to fall disproportionately on US companies, we lower our S&P 500 EPS estimate for 2025 from $282 to $240, implying a decline of -5% from last year. We quantify the impacts of various channels: foreign supplier ability to absorb tariffs; the importance of intra-company imports; price increases traded off against volume declines; lost earnings from China imports and exports; slower foreign growth; potential backlash on US sales abroad; and persistent uncertainty.

Looking for a wide range in equities near term (S&P 500 4600-5600). With equity positioning at the bottom of its historical range, the market is vulnerable to squeezes. While there have been several attempts at de-escalation there has not been a credible relent on trade policy, while macro concerns have been mounting. The bottom of the range corresponds to the pricing in of a typical recession decline (-25%), while the upper end is in line with positioning returning close to neutral. We see successful passage of the fiscal package as potentially prompting a rally, but with any direct benefits for corporates dwarfed by the hit from tariffs, we see the rally as short lived.

Further out, our base case remains for a significant rally on a credible relent on trade policies, with a target of 6150 by year end. A credible relent likely needs a significant decline in approval ratings. After the initial honeymoon period, approval ratings tend to align with what is happening in the economy and particularly with consumer confidence. Approval ratings have been falling but very slowly as growth has remained solid and inflation has not picked up yet. A move to the low 40s is likely necessary, while a full catch down would see them down to the mid-30s. The risk to our view is we don’t get a relent before the nonlinearities of recession kick in.

… As trade and geopolitics are reshaping, for now investors are becoming more relaxed about the near-term outlook with few signs of deteriorating data as yet and some dovish comments from Fed officials yesterday, which reassured investors that the Fed would still cut rates if the labour market deteriorated. So collectively, that helped the S&P 500 (+2.03%) to post a third consecutive gain for the first time since Liberation Day. And in another sign that market stress was easing, the VIX index (-1.98pts) fell to its lowest since the April 2 tariff announcements, closing at 26.47pts.

Those comments from Fed officials really helped to support the market yesterday, as they were notably more dovish than Chair Powell, who’d sounded a lot more concerned about inflation. For instance, Fed Governor Waller repeated his previous view that tariffs just represented a one-time price effect, and said that if he saw “a significant drop in the labor market, then the employment side of the mandate, I think, is important that we step in.” Earlier, we also heard from Cleveland Fed President Hammack, who said that if they had “clear and convincing data by June, then I think you’ll see the committee move if we know which way is the right way to move at that point in time”. So that was seen as opening the possibility of a rate cut sooner than expected, and futures moved to price in 85bps of cuts by the December meeting, up +6.0bps on the day. And in turn, Treasuries saw a strong rally, with the 10yr yield (-6.7bps) falling back to 4.32%, marking its third consecutive decline.

Aside from those remarks, the other good news yesterday was that the labour market appeared to remain in decent shape for the time being. For instance, the weekly initial jobless claims were at 222k over the week ending April 19, in line with expectations. Moreover, that was completely in line with where they’ve been over recent weeks, having oscillated between 216k-225k for the last 8 consecutive weeks now. So yet again, there was no obvious sign that layoffs were increasing, and we even saw continuing claims (for the week ending April 12) fall back to 1.841m (vs. 1.869m expected), which was their lowest since late-January.

All that helped to spur a strong market rally, with most US assets continuing to unwind their post-Liberation Day moves. For instance, the S&P 500 (+2.03%) posted a third consecutive gain, and it was actually the first time since February 2023 that the index has managed three consecutive gains of more than +1% a day. Tech stocks led the advance, with the Magnificent 7 (+2.94%) now up by +9.67% over the last three sessions…

… AND a reFUNding preview …

24 April 2025 DB: Refunding preview: No rush to term out

We now expect Treasury to begin increasing coupon issuance sizes in Q1 2026, one quarter later than previously anticipated. Next week, we see roughly even odds of Treasury either maintaining its existing guidance or softening it to allow for greater flexibility.

For the May-July quarter, nominal and FRN issuance sizes will remain unchanged. We expect another $1bn increase to the new 10-year TIPS in July, with the new auction size at $21bn.

For Monday’s borrowing estimate, we are expecting $507bn in Q2 and $480bn in Q3. The new Q2 figure will appear much higher than February’s estimate of $123bn, although actual issuance during this quarter will likely be closer to the original estimate under ongoing debt ceiling constraints.

We move our X-date estimate to mid-August supported by above-expectation fiscal flows. Our base case is for a debt ceiling resolution attached to the budget deal in July, although a pessimistic outcome would entail this being delayed into late summer or possibly September.

Despite Secretary Bessent's recent comments about buybacks as a tool to address liquidity issues, we believe Treasury's desire to avoid being seen as actively intervening, along with improved market conditions, suggests it's unlikely that Treasury will expand buybacks above the ongoing $30bn size for next quarter.

We continue to expect QT to conclude around Q1 2026, at which point the Fed will restart secondary-market Treasury purchases using MBS proceeds at approximately $15bn per month, with purchases possibly skewed toward the front end of the curve.

Goldilocks to all us muppets …

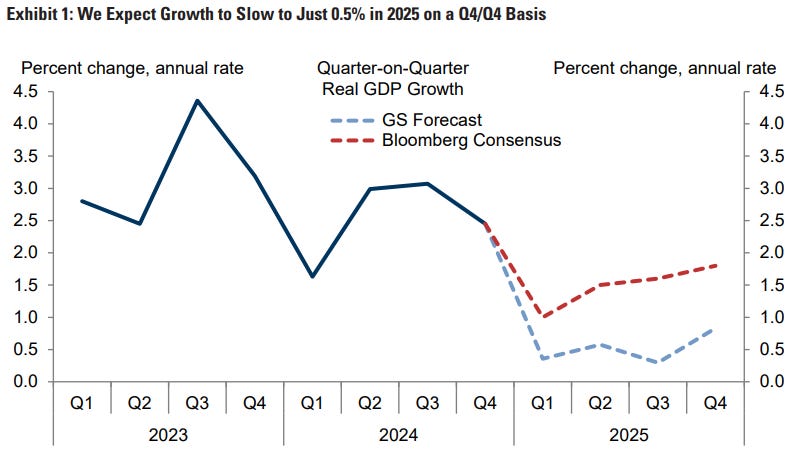

22 April 2025 | 11:20AM EDT GS: US Economics Analyst When Will Growth Slow, and When Will We Know?

We expect US GDP growth to slow from 2½% last year to just 0.5% this year on a Q4/Q4 basis, largely reflecting higher tariffs, tighter financial conditions, and higher policy uncertainty. In this week’s Analyst, we explore how quickly different economic indicators identified past growth slowdowns, how we are monitoring growth in the current environment, and what we can expect to see in the data over the next few months.

Using a daily dataset with the latest readings of 45 economic indicators in real time, we find that initial jobless claims, the Philly Fed manufacturing and ISM services indices, and (perhaps surprisingly) the unemployment rate were the timeliest indicators of slower growth. In prior recessions for which we could identify a key precipitating catalyst—such as the 1970s oil shocks—it took about four months for the hard data to weaken in real time. The expectations components of business surveys weakened much sooner, about a month after the shock.

In the current environment, we expect consumer spending to slow alongside disposable income as tariffs boost consumer prices. Most of the sequential inflation increases in the last trade war took place within 2-3 months of the tariffs’ implementation, and we expect spending growth to slow shortly after prices start rising. Historically, core retail sales has been the best hard indicator of consumer spending around growth slowdowns, providing a better signal in real time than the personal income and spending releases. We expect spending on imports to fall particularly sharply, although so far our high-frequency proxies of imports from China have slowed only modestly.

We expect tighter financial conditions and elevated uncertainty to start depressing capex growth this quarter, with a peak drag in the second half of this year. In previous capex-led growth slowdowns, the hard data available in real time (such as capital goods orders) took about five months to weaken and were much noisier than the soft data, which deteriorated about one month into the slowdown. Broader indicators like manufacturing production generally provided a better real-time signal than narrower measures of capex.

In the labor market, initial jobless claims tend to be the timeliest hard indicator around growth slowdowns. The unemployment rate and job-finding probability weaken noticeably about two to three months into a growth slowdown, but when they do they provide a more reliable signal than claims. In addition to the official statistics, we can also monitor WARN layoff notices and alternative measures of job openings on a daily basis. So far, both indicators remain at healthy levels.

Taken together, we expect to see continued softness in the survey data before the hard data start to weaken around mid-to-late summer. Our analysis cautions against dismissing the current deterioration in the survey data despite their recent record, and the evolution of the data in recent weeks is consistent with previous “event-driven” growth slowdowns. Still, it is too early to draw strong conclusions from the limited data we have so far, and we will continue to watch for indications of slower growth in the coming months.

A(nother) quick recap of what I missed …

April 24, 2025 MS: Global Macro Commentary: April 24

Heightened Fed easing expectations after fedspeak; belly led UST rally; Bunds bull-steepen as market implied probability of a June ECB cut rises; broad-based USD weakness; SOFR swap spreads widen; CE3 currencies outperform; DXY at 99.29 (-0.6%); US 10y at 4.315% (-6.6bp)

Resurgence in Fed easing expectations after Cleveland Fed President Hammack says the Fed is not afraid to move quickly and could move as early as June if there are “clear and convincing data,” while Fed Governor Waller sees "more rate cuts, and sooner" should the labor market deteriorate.

Belly-led rally in USTs (5y: -9bp) as Fed rate cut expectations rise; USTs continue to richen even after a slightly weak 7y auction with a 0.2bp tail…

Here a UK shop talking about our CB inflation mandate …

23 Apr 2025 NatWEST: Inflation mandate as policy keystone

In debt markets credibility is ultimately about willingness and ability to make full and timely payment of contractual obligations. Credibility with respect to nominal obligations is what is conventionally referred to as “credit”. Credibility with respect to real obligations is a function of the market’s subjective estimate of the probability of being repaid in real terms. Real credibility is unique to the sovereign sector in that the sovereign can influence inflation through fiscal policy, regulatory policy, and selection of key actors in monetary policy formation.

Dollar assets generally - and the Treasury market in particular - are currently afflicted with challenges in both nominal and real dimensions. We argue that real and nominal credibility are two sides of the same coin; that is, rising inflation is a result of a spending trajectory that is bumping up against the Treasury’s intertemporal budget constraint.

Fundamentally, the US and other industrialized economies are confronting structurally declining potential growth. This is at its heart a demographic issue – industrialized economies face declining birth rates and aging labour forces, presenting the problem of too few workers paying into the system to support too many in age cohorts that are net receivers of benefits.

The Treasury’s spending trajectory is not sustainable in the long run. In fact, the CBO’s recent long term budget update has debt growth overtaking GDP growth in 2044.

The sunset of TCJA tax cuts creates a fiscal mini-cliff. The current budget process has two-sided risks: unintentional fiscal tightening on the one side, and potentially explosive debt dynamics somewhat on the other.

We argue that the inflation mandate is the keystone in the current policy architecture; that is, Fed defense of the inflation target will increase the Treasury’s credibility in satisfying real obligations via future surpluses rather than allowing inflation to erode nominal debt. This credibility will reduce borrowing costs, improve market perceptions of debt sustainability, and aid in stabilizing short term demand on the margin.

China said it was not negotiating with the US over trade. US President Trump avowed that the US was talking with someone (who they are talking to is a secret, apparently). Things like this might possibly be contributing to the economically damaging levels of uncertainty. The US and South Korea have agreed a framework for trade talks (North Korea escaped US tariffs). South Korea and the US had a free trade deal with no tariffs at all until a few weeks ago.

Final US April Michigan consumer sentiment is due. The main value of this is assessing the extent to which partisan media bubbles are being burst by economic reality. Republican sentiment did dip slightly in the early April data—it will interesting to see whether that sentiment weakened further in the latter part of the month. Democrat sentiment is likely to be remain mired in extreme pessimism…

Once again, ‘sides air, not much good ‘bout aDURables …

April 24, 2025 Wells Fargo: Little Sign of Strength in March Durables Outside Aircraft-Related Lift

Summary The 9.2% gain in March durable goods orders was due almost entirely to a pop in orders for nondefense aircraft. The underlying trend in orders remains weak as businesses await clarity on tariff policy. Durable shipments pulled back, but equipment spending was still strong in Q1.

On Sunday (April 20), we observed that The Economist had just featured three consecutive very bearish cover stories suggesting that the dollar might be on the verge of collapse and that so might the US stock and bond markets along with the US economy. Make that four consecutive bearish cover stories, with this week's magazine showing an eagle battered by Trump's first 100 days (image). We repeat our conclusion from a week ago: Contrarians of the world, unite! Now, we would add that our Roaring 2020s scenario might be back on track soon.

The S&P 500 is up more than 7% from its Monday lows, the VIX is back below 28, and the high-yield corporate bond spread is down from 461bps a few weeks ago to 348bps (chart). The 10-year Treasury yield also fell 7bps today after Cleveland Fed President Beth Hammack told CNBC that the Fed could cut interest rates if the data deteriorated by the FOMC's June meeting. We still doubt that will happen.

Meanwhile, Treasury Secretary Scott Bessent is increasingly taking on more economic and trade responsibilities. Investors believe he is more like one of us given his hedge fund career. We think trade deals will need to be inked soon for the stock market to sustain its current bounce. We still believe that the latest correction in the S&P 500 bottomed on April 8, a day before Trump basically postponed "Liberation Day."…

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Just a couple today as I’m still sifting through yesterday’s rubble …

April 25, 2025 Bloomberg: China May Exempt Some US Goods From Tariffs as Costs Rise

…China’s government is considering suspending its 125% tariff on some US imports, people familiar with the matter said, as the economic costs of the tit-for-tat trade war weigh heavily on certain industries…

April 25, 2025 at 5:01 AM UTC Bloomberg: Where's Mike Tyson with advice when you need him? The ‘User’s Guide’ plan from White House chief economist Stephen Miran has taken some big hits.

… There’s a Risk That Long Yields Could Rise

If an expected change in currency values leads to large-scale outflows from the Treasury market, at a time of growing fiscal deficits and still-present inflation risk, it could cause long yields to rise. This risk will be somewhat compounded if inflation remains elevated.

Miran expected the currency to rise to offset the imposition of tariffs — which he argued would have the effect of putting the burden on to the tariffed country. But he acknowledged that it might not, and that if the dollar were to weaken, then continuing inflation worries and the high budget deficit would put pressure on Treasuries. That has happened so far. The good news is that inflation numbers have improved in the last few months, but they don’t yet take account of tariffs…

… Demand for Treasuries Is Eternal

Much (but not all) of the reserve demand for [dollars and Treasuries] is inelastic with respect to economic or investment fundamentals. Treasurys bought to collateralize trade between Micronesia and Polynesia are bought irrespective of the US trade balance with either, the latest jobs report, or the relative return of Treasurys vs. German Bunds.

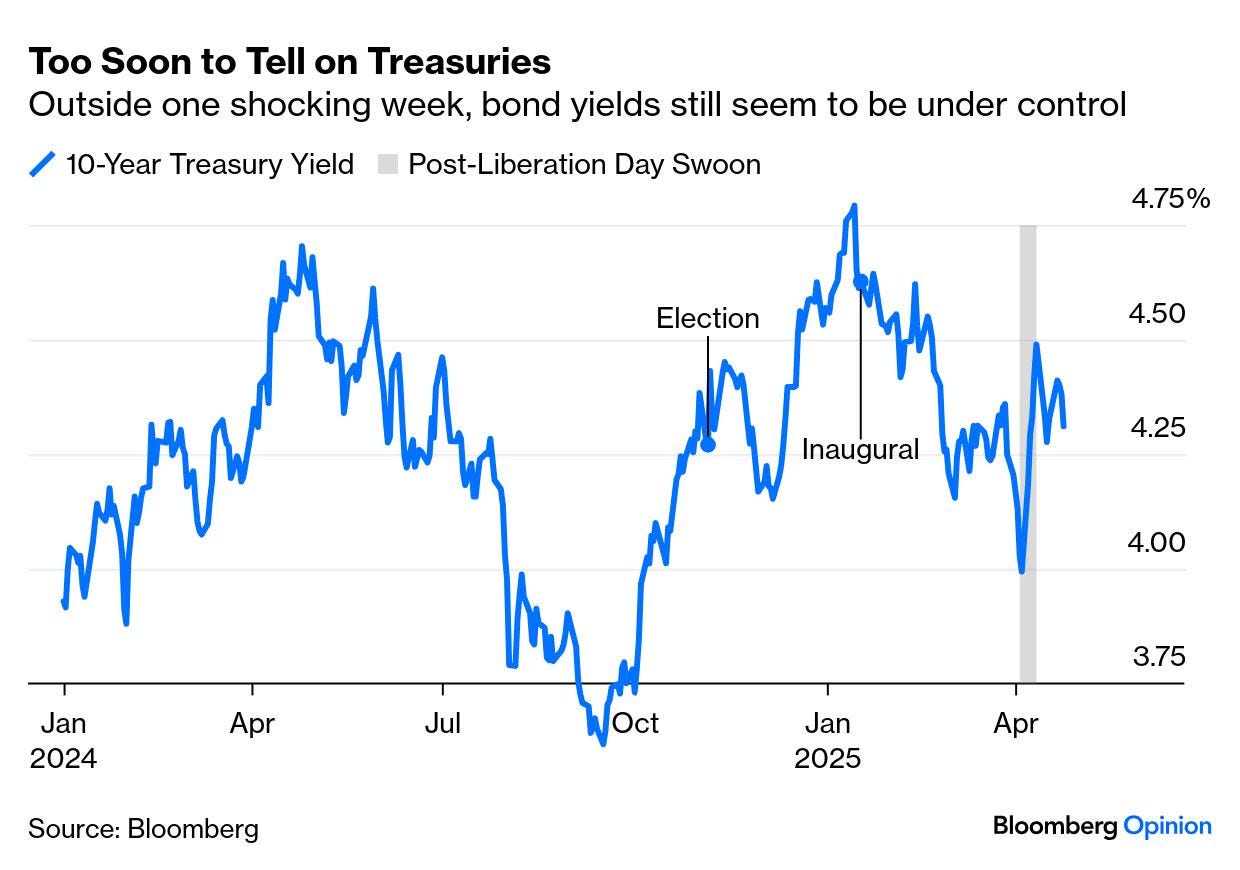

Demand may not be as inelastic as all that. The week after Liberation Day saw a combined run on both the dollar and Treasuries, which drove the 10-year yield up by the most in a week in more than 20 years. It’s a sign that foreigners have suddenly become much more discerning in their demand for US debt. That said, apart from one shocking week, the Treasury trend is still unclear:

Foreigners Will Pay for the Privilege of Lending to the US

Treasury can use the International Emergency Economic Powers Act to make reserve accumulation less attractive. One way of doing this is to impose a user fee on foreign official holders of Treasury securities, for instance withholding a portion of interest payments on those holdings.

This assertion is beginning to look very questionable. Effectively, the suggestion is that the US should charge foreigners a fee for the privilege of lending to Uncle Sam. Just this month has seen sharply increased interest in alternatives, such as German bunds, Swiss francs, gold, and even Bitcoin. If the US tries to charge a fee like this, the likelihood is that it will just stop the flow of funds into the US — and make it that much harder to fund the deficit.

… THAT is all for now. Off to the day job and hope to be back to ‘regular’ for while …