Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Shorter note / view than normal this weekend, for a couple reasons.

First, family in for the holidays and I’ve already spent too much time in front of the machines and away from the weekend and family … certainly more than I should when put in to context / relationship to what I might possibly have to offer.

Second, I’ve not run through HIMCOs LATEST (noted HERE) enough and while I will admit, the more removed I have been from the front row seat IN the institutional bond market, the more optimistic (ie NOT yet card carrying member of Team Rate Cut) I have become.

Synagogue Friday night an excellent example … the handful of those portraying to be ‘in the know’ (private equity and commods guys) all ready for the proverbial FIT to hit the shan with regards to the past weeks PIVOT and then PIVOT FROM THE PIVOT AND the hotting up situation in the middle east.

Yet the surprise on their face when confronted with … math. From S&P Dow Jones …

S&P +4.15% YTD S&P +19.56% 1yr S&P +11.33% 5yr

… and so on … You get the point. Nothing YET has broken and while I’ll readily admit, last year (SVB, FRC), I thought Fed had done it. Achieved max traction and finally gotten something to break therefore flashing that much anticipated GREEN LIGHT for Team Rate CUT …

Yet, there we went from 7 rate cuts to now … what, perhaps a coin flip?

Do yourself a favor and follow a friend from my past on Twitter …

#FOMC Meme Watch Apparently it takes a Day to explain to people what Mr. Powell said?? Back to Certainty of cut by September?

… perhaps we get one? Maybe we don’t?

It is with that in mind, I defer TO HIMCOs LATEST (noted HERE) and highly recommend a point / click / and READ of his STILL BOND BULLISH view … have a look at this visual of WORLD DOLLAR LIQUIDITY — A Modernized World Dollar Liquidity (MWDL) Measure — contracting …

The Long View

The dynamics of fiscal and monetary policy are now entering a new phase. Due to the emergence of negative Net National Saving (NNS), the law of diminishing returns can no longer fully capture the harmful effect of debt on economic growth. This new analytical framework indicates that the pronounced downward trend in the growth rate of the standard of living, evident since the 1970’s, is likely to persist. A redefinition of the monetary base and world dollar liquidity (WDL) is needed to capture the pure impact of central bank actions on business conditions. These new monetary measures, which are more restrictive than the old standards, indicate that the Federal Reserve is on the path to reducing inflation to the policy objective…

… Four decades ago, Dr. Rod McKnew argued that since the dollar is the world's reserve currency, the Fed is also the world's central banker. To reflect that, he created the concept of WDL, which he defined as the MB plus marketable securities held in custody for foreign official and international accounts at the Federal Reserve. PR should replace MB in this definition. Chart 1 illustrates the outstanding track record of this MWDL, which decelerated sharply before all the recessions since 1976.

The year-over-year change in MWDL went negative in all recessions except the one in 2000-01. MWDL has dropped by a record 9% in the twelve months ending February 2024, indicating the Fed’s restraint is intensifying on global markets. For instance, real money growth is negative in the Euro Area and the United Kingdom, and Japan is experiencing the slowest growth in twelve years (Chart 2). Combined with Japan's recently adopted tighter central bank policy, the risk is that Japanese money growth could turn negative. The record contraction in MWDL will exert additional restraint on a global economy where the Euro Area, the UK, and Japan are in either technical or quasi-recessions, and China is in deflation.

… And with that in mind, I’ll have a closer look at 2s, 5s and 7s as we go along thru the week and ahead of daily liquidity events.

For now, I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

THIS WEEKEND, a couple / few things which stood out to ME this …

BARCAP Rates Weekly, “Shaken” (updated call .. here we go again?)

… We remain short 10s, as financial conditions need to be tighter and QRA is unlikely to provide supply relief…

… Forecast tweak: Consensus is too optimistic on falling 10y yields … Following the disinflation false alarm, we tweaked it lower to 4.35%, as we expected a sooner start to the easing cycle. We are now reverting to 4.6%, somewhat above what we had originally forecast

… We recommend going long the 5Y point. Logic: Fed unlikely to hike, risky asset rate sensitivity, and cleaner positioning. Risks are momentum & technicals…

… we'll look to buy 2s at the auction clearing level on Tuesday. Looking back to 2023, each time 2-year yields were approaching 5.0%, the market had been seriously considering the potential for rate hikes as the Fed was perceived to be laying the groundwork for such a move.

… New UST forecasts: With recent data, our economics team now expects rate cuts to start in July, and three cuts in 2024, followed by four in the first four meetings of 2025. With this new Fed path, we revise our UST forecasts and now expect 10-year yields to end 2024 at 4.15%, 20bp higher than our previous forecast of 3.95%. Our forecast is nearly 45bp lower than market-implied forwards. We see 2-year yields at 4.30% by the end of 2024…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW …

… The bottom line is that base effects and strong recent readings complicate the Fed’s efforts to get inflation back to its 2% inflation target. Put differently, it will require a sharp, immediate slowdown in consumer spending and capex spending for the Fed to be able to cut rates by the end of this year.

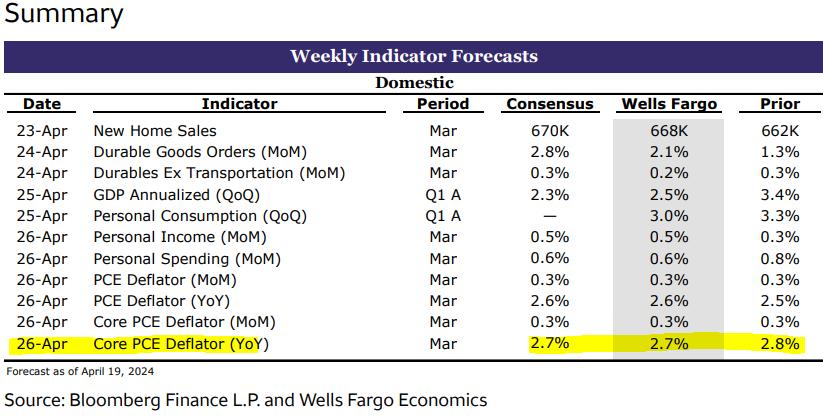

Bloomberg: Fed’s Preferred Inflation Gauge Is Set to Back Rate-Cut Patience

After CPI data rocked global markets, focus shifts to core PCE

BOJ may hint at future rate hikes; German Ifo index due

… Policymakers’ preferred inflation gauge — the personal consumption expenditures price index — probably stayed elevated in March, according to data due in the coming week.

The measure is seen accelerating slightly to 2.6% on an annual basis as energy costs rise. The core metric, which strips out energy and food, is expected to rise 0.3% from the prior month after a similar gain in February.

While the core PCE data may not be as strong as the consumer price index — which topped estimates and rattled markets earlier this month — Fed Chair Jerome Powell and other officials have signaled that it’ll take longer for them to gain the necessary confidence in a downward trajectory of inflation before cutting rates…

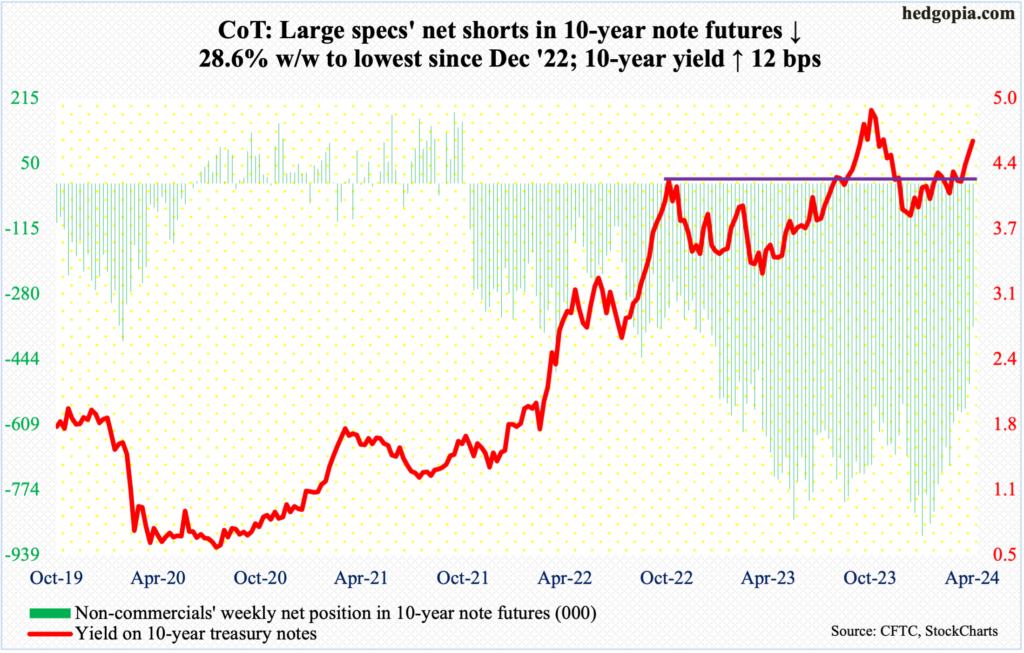

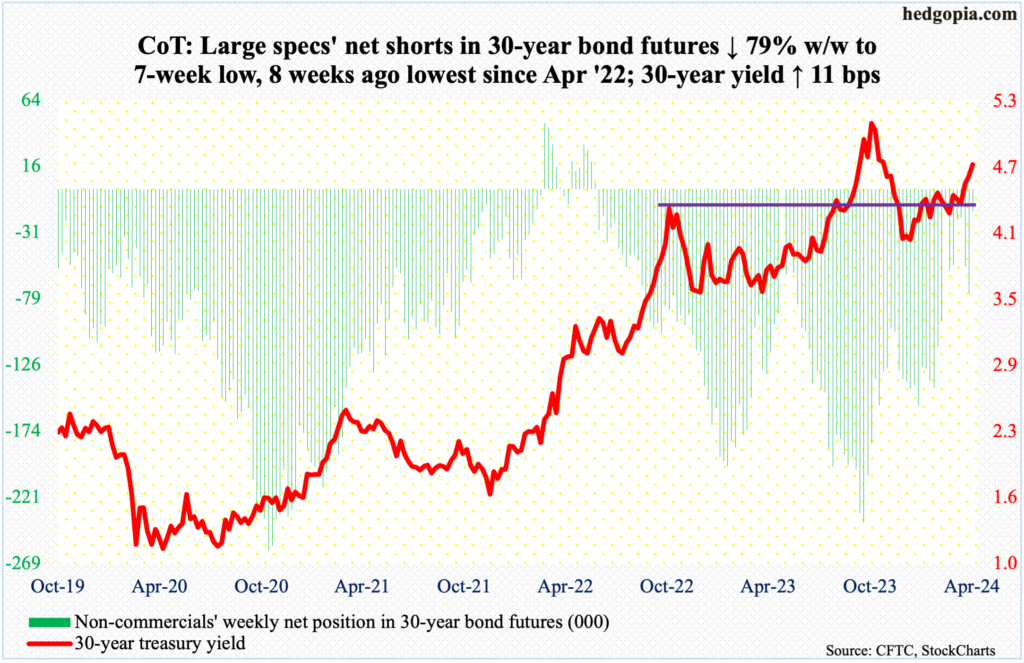

Bloomberg: The Weekly Fix: Higher for longer hits bonds as 5% back in play

📈 CHART OF THE DAY: UST 2-Yr Pressure Cooker Has Release Valve in 4.99%

We think UST 2-Yr yields are in a ‘pressure cooker’ type situation, ready to explode higher (again) with 4.99% Fib seen as the release valve. Next set of RES’s at 5.03% and 5.11%; yield support at 4.85% which is the marubozu point of the CPI-day April 10th candle; a daily close under there would temper the bullish-yield outlook; Despite the quiet(er) week, we stay bearish USTs across the curve.

Reminder that THE rising pattern in open interest (on TU) shows that market is building shorts rather than liquidating; so both trend and positioning are your friend (H/T Bbg news).

ZH: A Very Ugly Week For The Nasdaq, A Terrible Week For Semiconductors

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

{kind=link}

{kind=link}