Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Joint Statement by the Department of the Treasury, Federal Reserve, FDIC and OCC … Today, 11 banks announced $30 billion in deposits into First Republic Bank. This show of support by a group of large banks is most welcome, and demonstrates the resilience of the banking system.

… Bear Stearns seemed to be riding high with a stock market capitalization of $20 billion in early 2007. But its increasing involvement in the hedge-fund business, particularly with risky mortgage-backed securities, paved the way for it to become one of the earliest casualties of the subprime mortgage crisis that led to the Great Recession.

AND … then there’s THISjust in (yest afternoon, and talked about all week long — something to look forward to in the week just ahead) …

TOKYO -- The Bank of Japan is expected to end its negative interest rates when its policy board meets on Monday and Tuesday, Nikkei has learned, marking the first rate hike since February 2007 in a turning point for the BOJ's long-running monetary easing policy…

… LINK for more but thinking we all knew this was coming, some day …

ZH: BoJ Mouthpiece Confirms Historic End Of Negative Rates Next Week, 1st Hike In 17 Years

… anyone else wondering what next? I guess why we’re all on alert for the Ides of March?

Moving right along and to a look at long bonds and 20s ahead of their auction in the week just ahead …

30yy WEEKLY: 4.335% bares watching IMO

20yy WEEKLY: watching 4.66%

… Ok I’ll move on AND right TO the reason many / most are here …some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

THIS WEEKEND, just a few things stood out to ME …

BMOrates weekly, “Wait and FOMC” (catchy BUT … even the best in biz gets stopped out once and while...)

… We were stopped out of our long 10s position we entered at Tuesday’s auction clearing level of 4.166% as Thursday’s selloff brough the benchmark rate definitively through the 100-day moving average of 4.244%

…Primary dealer positions in Treasuries have surged recently

SocGEN FI Weekly, “Time to party” (again, catchy title and a reminder they are still ready / willing / able to buy dips … or at least suggesting you do…buy 2s, 10s and maintain call for 2yr fwd 2s5s and 2s10s steepeners)

… Buy the dip. The 2yT yield is fully pricing in the Fed’s median dot, which shows three 25bp cuts this year. The 2yT and 10yT yields are near the high end of the range, which presents opportunities to leg into longs.

The buyer base for US Treasuries has shifted from yield-insensitive buyers (sovereign wealth funds and central banks, including the Fed) to yield-sensitive buyers (US households, US pensions, US insurance), see chart below.

This may become a problem once the Fed begins to cut rates because that could mean less demand from the yield-sensitive buyers, ultimately resulting in a steeper yield curve.

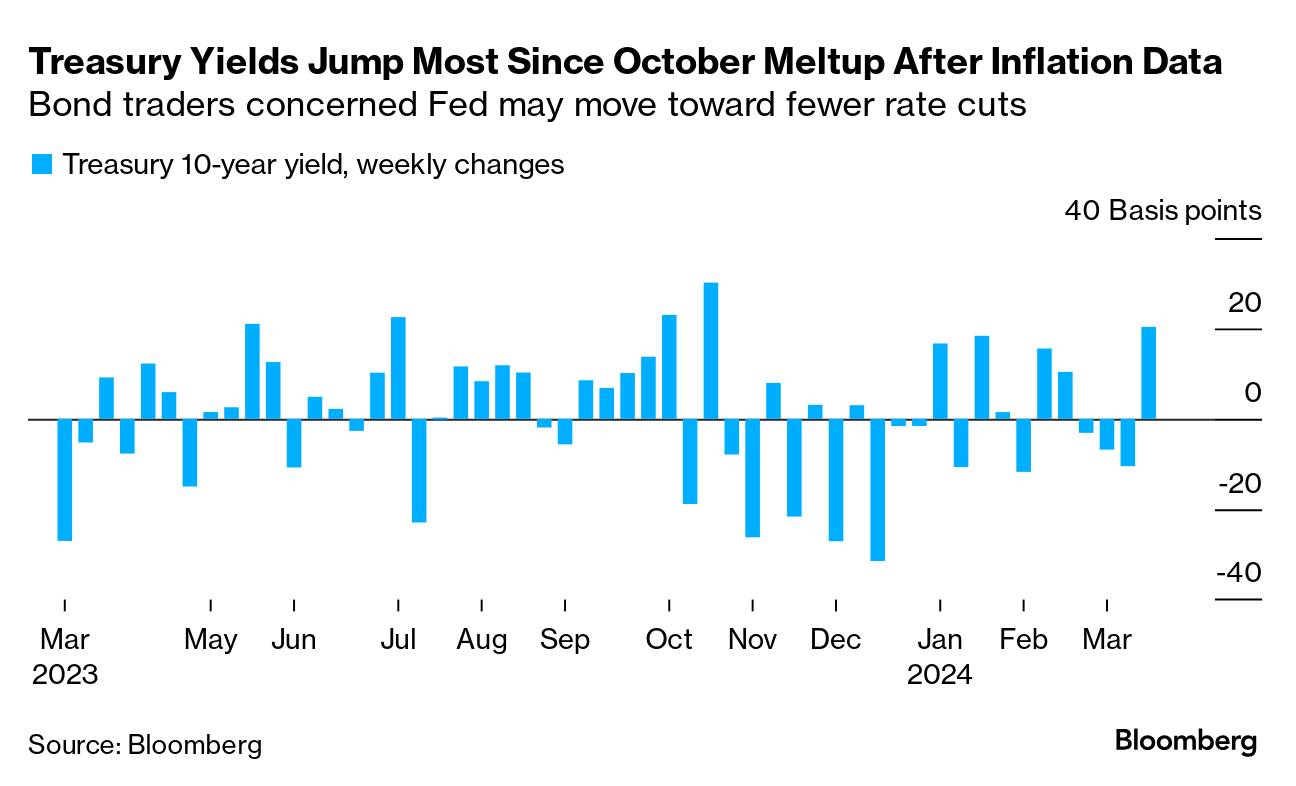

Bloomberg - The Weekly Fix: Bonds drop as hawks hover over Fed, BOJ choices (good weekly review and 10yy weekly change graphic speaks volumes…)

Oops, They Did It Again? How many times can rates traders get forced out of bets on a lower US cash rate? The answer seems to be well nigh infinite in the current Federal Reserve policy cycle. Robust readings on consumer and producer price inflation this week sent bonds crashing. Benchmark 10-year yields climbed more than 20 basis points — heading for the biggest one-week jump since October’s meltup.

Swaps traders entered the year betting the Fed would start cutting rates in March and deliver six reductions by year end, despite the central bank’s “dot plot” calling for only three moves to lower borrowing costs. Now, markets see June or July as the most likely first move, in accord with policymakers’ projections. This week’s selloff gathered momentum as the strong US data prompted speculation the Fed will shift its projections to signal only two cuts in 2024 rather than three.

That also sent money-market fund assets to a fresh record of $6.11 trillion as investors expect short-term rates to remain elevated for longer.

The move in the potential policy outlook came as US Treasury Secretary Janet Yellen flagged that rates are unlikely to revert to the pre-Covid mean. Part of the reason for that is the likelihood that government spending will keep on growing rapidly whoever wins this year’s election, according to Harvard University economics professor Kenneth Rogoff.

WolfST: Short-Term Treasury Market Walks Away from Rate-Cut Mania, Inflation Has Upper Hand

ZH: Despite All The 'Benefits Of Illegal Immigrants' NY Manufacturing Sector Is A Stagflationary Shitshow (sorry. not sorry. Mom used to say, be careful what you wish for cuz you might just get it … )

ZH: US Industrial Production Sees More Downward Revisions (You Can't Make This Up) (nuthin’ to see here folks, move along, back to your cars … Team CUTS winning the end of the week?)

… In today's episode of 'shit you believed in the past is not real at all', US Industrial Production in January was revised from a 0.1% decline to 0.5% decline. That is the 10th monthly revision lower in the last 11 months (and 14th of the last 17)...

ZH: Disappointed 'Independents' Drag Down Consumer Sentiment In March

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Um … does this all but insure not only NOT a soft landing (or a NO landing as one might infer) but rather a mother of all HARD LANDINGS on the way?? We’re all doomed … that from Economist is simply funny enough and so THAT is all for now.

Stay SAFE. Happy St Patty’s Day and … Enjoy whatever is left of YOUR weekend …

Excellent work....

Thank you for the Reality Check......