Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Allow me to be the first to wish one and all a very happy 2% ‘flation goal-A-versary. HERE is the press release from this day — January 25 — back in 2012 …

… The inflation rate over the longer run is primarily determined by monetary policy, and hence the Committee has the ability to specify a longer-run goal for inflation. The Committee judges that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve's statutory mandate. Communicating this inflation goal clearly to the public helps keep longer-term inflation expectations firmly anchored, thereby fostering price stability and moderate long-term interest rates and enhancing the Committee's ability to promote maximum employment in the face of significant economic disturbances…

For somewhat MORE, HERE is transcript of that very day’s press conference in the case you are having any trouble sleeping at night (perhaps you can also find it on YOUTUBE?) and somewhat more …

…United States In a historic shift on 25 January 2012, U.S. Federal Reserve Chairman Ben Bernanke set a 2% target inflation rate, bringing the Fed in line with many of the world's other major central banks.[29] Until then, the Fed's policy committee, the Federal Open Market Committee (FOMC), did not have an explicit inflation target but regularly announced a desired target range for inflation (usually between 1.7% and 2%) measured by the personal consumption expenditures price index.

Prior to adoption of the target, some people argued that an inflation target would give the Fed too little flexibility to stabilise growth and/or employment in the event of an external economic shock. Another criticism was that an explicit target might turn central bankers into what Mervyn King, former Governor of the Bank of England, had in 1997 colorfully termed "inflation nutters"[30]—that is, central bankers who concentrate on the inflation target to the detriment of stable growth, employment, and/or exchange rates. King went on to help design the Bank's inflation targeting policy,[31] and asserts that the buffoonery has not actually happened, as did Chairman of the U.S. Federal Reserve Ben Bernanke, who stated in 2003 that all inflation targeting at the time was of a flexible variety, in theory and practice.[32]

Former Chairman Alan Greenspan, as well as other former FOMC members such as Alan Blinder, typically agreed with the benefits of inflation targeting, but were reluctant to accept the loss of freedom involved; Bernanke, however, was a well-known advocate.[33]

In August 2020, the FOMC released a revised Statement on Longer-Run Goals and Monetary Policy Strategy.[34] The review announced the FED would seek to achieve inflation that 'averages' 2% over time. In practice this means that following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.[35] This way, the fed hopes to better anchor longer-term inflation expectations, which they say would foster price stability and moderate long-term interest rates and enhance the Committee's ability to promote maximum employment in the face of significant economic disturbances.

First UP, a brief look back at the day that was …

ZH: US Services PMI Pukes In Preliminary January Data, Manufacturing Back In Expansion

ZH: UMich Inflation Expectations Soar As Democrats Panic

ZH: Insider-Selling Soars As S&P 500 Hits Record High; Gold & Crypto Jump As Dollar & Crude Dump

…This all after having a chance to pass along latest thoughts from none other than Dr. Lacy Hunt who, yes, is still bullish long bonds … see his note HERE …

… Inflation and Bond Yields Historically, on an annual basis, there has been a high correlation between the thirty-year Treasury bond yield and the inflation rate. That relationship did not hold in the past two years when the long bond yields rose even though the inflation rate moved downward. Despite this recent divergence, inflation and the long bond yield moved in the same direction for 71% of the years since 1954, when Treasury bond yields started trading freely. Historically, such divergences have been brief.

The previously discussed fundamental determinants of inflation indicate the prospects for slower price increases are even more significant than in any year since the late 1990s. In addition to the growing factory capacity glut and rising UR, the percent decline in modernized world dollar liquidity (WDL) reached another record low in the fourth quarter. The accelerating decline in WDL will intensify the liquidity/money squeeze domestically and globally. We estimate the trend adjusted real M2 declined further in the fourth quarter. Since the Fed's first reduction in the policy rate in September, critical consumer and small business borrowing rates have remained unchanged or increased. Such considerations argue that lower inflation will lead to a surprising drop in thirty-year Treasury bond yields in 2025.

… Alrighty, then.

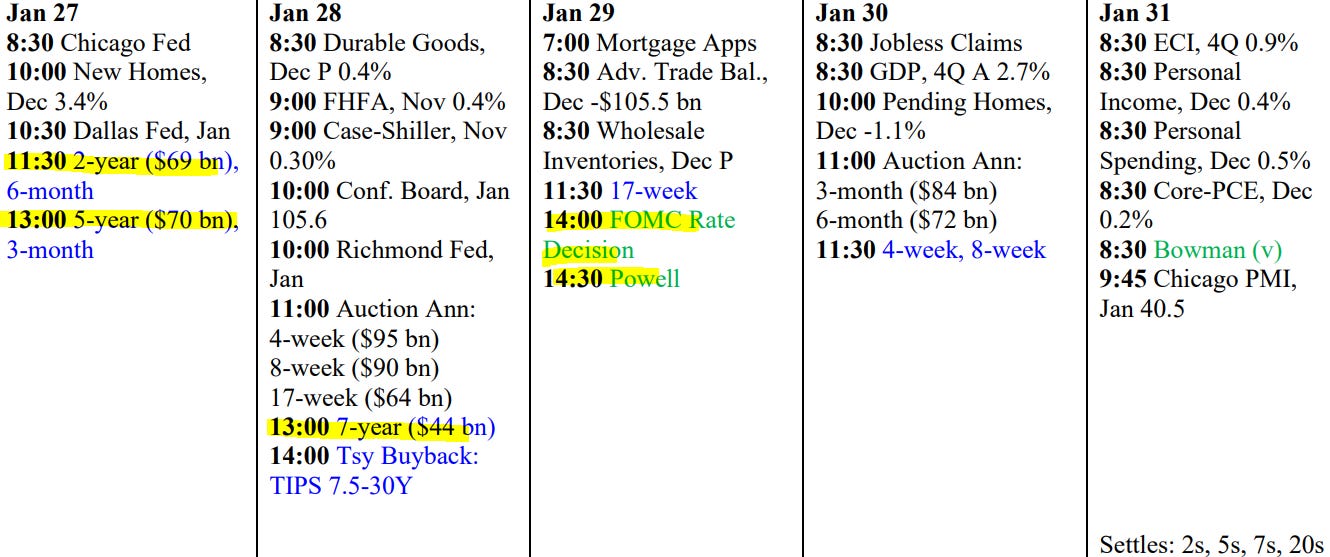

I would like to move along and take a quick and updated look at 5s ahead of Mondays upcoming UST auctions (69bb 2s and 70bb 5s) . I do so at the risk of looking like the amateur that I am on the heels of some charts from THE very best tech-A-mentalists out there (CitiFX HERE as they contrasted the … short & medium term indicators … of 2s, 5s, 10s and 30s)

5yy WEEKLY: last week 5s ended at 4.43, this week 4.42 (look kids, big Ben …) … one thing for sure, we continue to romance (green)TLINE …

… as momentum continues to look overSOLD and turning down, which would suggest the path of least resistance is (still)lower …

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

Economically speaking …

BARCAP: Global Economics Weekly: So far, so transactional

Trump's initial policy restraint and signals for 'deal-making' reduced concerns about trade disruption, softened the USD and further fueled equity euphoria. That said, the ultimate outcomes of his transactional approach remain uncertain. Next week, we expect the Fed to hold and the ECB to cut rates.

…US Outlook Appetite for disruption: Week one Inauguration week brought a flurry of executive orders that aimed to disrupt the status quo for regulation and energy. Although the president's big week grabbed headlines, little of this was surprising, and we retain our outlook as we await clarity about tariffs and fiscal policy.

AND best in biz, looking towards ‘fwd entry of a 2s10s steepener’ (35bps) …

In the week ahead, there are several potentially market-moving events that investors in the US rates market will be tracking. The most obvious is Wednesday’s FOMC decision and while no change in the policy rate is expected, Powell’s press conference will be closely followed for any initial reaction to Trump’s recent tariff announcements. On net, we’re looking for a dovish pause. The Fed will delay lowering rates in favor of buying more time to evaluate the economic implications from the ever-evolving global trade environment. While investors would like Powell to have a strong stance on the longer-term impact from what has already been announced by the White House, at the end of the day we suspect that the Chair will conclude that it is still too soon to make any definitive estimates for the impact on the US economy from Trump’s changes. It’s a fair stance given that the 25% tariffs on Mexico and Canada as well as the 10% further tariffs on China appear to be the President’s working assumptions as opposed to hard facts.

While the lack of clarity from Powell will surely lead to disappointment from investors looking for more concrete guidance, the Chair is also likely to reiterate the Fed’s intention to move further on its journey toward normalizing policy rates. The futures market is currently pricing in roughly 30 bp of cuts for 2025, a level that we read as underestimating the Fed’s commitment to bringing rates back closer to neutral in the coming quarters. We’re reminded that from the perspective of monetary policymakers, the Fed is cutting, not easing. This implies that lowering rates further requires progress toward a cooling inflation profile as opposed to a dramatic slowdown in the real economy or spike in unemployment. Setting aside the recent increase in the jobless claims figures, the labor market remains on solid footing and, as evidenced by December’s supercore CPI print, inflation has resumed its progress toward the Fed’s objective…

…Treasury investors also have early-week supply to underwrite. The timing of the FOMC and month-end, as well as the Treasury Department’s extra day to ensure against settlement issues, means that Monday will see both the 2- and 5-year auctions. Tuesday afternoon’s 7-year offering will round out January’s nominal coupon issuance; leaving the balance of the week to be driven by monetary policy, the fundamental data, and, of course, further policy announcements from the White House. The biggest issue to be resolved in the near-term is whether Trump plans to implement the 25% tariff increases on Canada and Mexico on February 1st or if the gravity of such levies warrants a fuller review and an April 1st rollout…

Treasuries/TIPS: The current setup offers an asymmetric risk/reward opportunity to own TIPS. We suggest owning 10y TIPS outright and also like long 5y breakevens.

Two contrasting dynamics have opened the opportunity: i) markets have priced higher growth and discounted tariff/inflation risks, while ii) the Fed in contrast has pre-emptively hedged the risk of high inflation. These have driven disproportionately higher real yields and subdued breakevens.

The Fed’s stance and the market’s view on inflation cannot both be true. The one that proves correct can drive a repricing to lower real yields.

We entered long 10y TIPS at 227bp. We continue to like the trade and now move the target lower to 180bp and the stop-out lower to 230bp.

Treasuries: We preview the quarterly US Treasury refunding, expecting unchanged coupon sizes and looking for guidance on future coupon raises.

Same shop lookin’ at GDP (and so, some sort of FOMC read thru) …

BNP: US Q4 2024 GDP preview: Strength to carry over into H1 2025

KEY MESSAGES

We estimate real GDP growth of 3.0% q/q saar in Q4 2024, reaffirming what was a well-above-consensus estimate when we unveiled it in early December.

We are also upgrading the H1 2025 outlook on account of tailwinds including a stronger labor-income backdrop. We still expect deceleration to a sub-2% pace in H2 as tariffs lift prices and restrain real spending.

US economic resilience reinforces our view that the Fed will approach rate cuts cautiously and ultimately leave rates on hold in 2025.

Same shop taking a look at the upcoming reFUNding …

We expect Treasury to maintain current nominal coupon and FRN auction sizes at the February refunding but look for any indications on the timing of future increases as we pencil in auction size boosts to start in August.

Treasury has invoked extraordinary measures with sharp T-bill paydowns likely to begin in late February and through the spring until Congress passes a debt ceiling resolution in late May, in our view.

Primary dealers were asked about long-run Fed balance sheet expectations after QT ends, where we expect the Fed to reinvest MBS proceeds into T-bills and begin reserve management operations in 2026 to grow its balance sheet and keep reserves at ample levels.

In the attached Weekly we discuss our early takeaways from the first few days of the second Trump Administration. We argue that a systematic approach to setting monetary policy would shield the Fed from political pressures on interest rates and show why the delivery of a new Golden Age would mean higher interest rates (i.e., higher interest rates result from the success of the Trump Administration’s policies, rather than lower rates being the source of that success). We also preview next week’s advance report on real GDP for the fourth quarter of 2024…

…Rates on Hold, No New Forecasts, How to Counter the President’s Demands …Rates and the Golden Age …If President Trump’s policies succeed, therefore, interest rates would have to be substantially higher than would otherwise be the case. If Powell simply played the role of a disciplined macroeconomist, he could lay this out without having to argue that Trump’s tariffs might be inflationary, requiring a Fed response. He could simply say that if the Fed tried to force interest rates lower, then the policy rate would be substantially below the natural rate, which would lead to inflation. An alternative way to think about this is that success in creating a Golden Age would result in significant gains in stock prices and to compete with stocks, bonds would need to pay a higher yield. A higher interest rate, therefore, would be a measure of the President’s success rather than seeing lower rates as a source of the success of Trump’s policies…

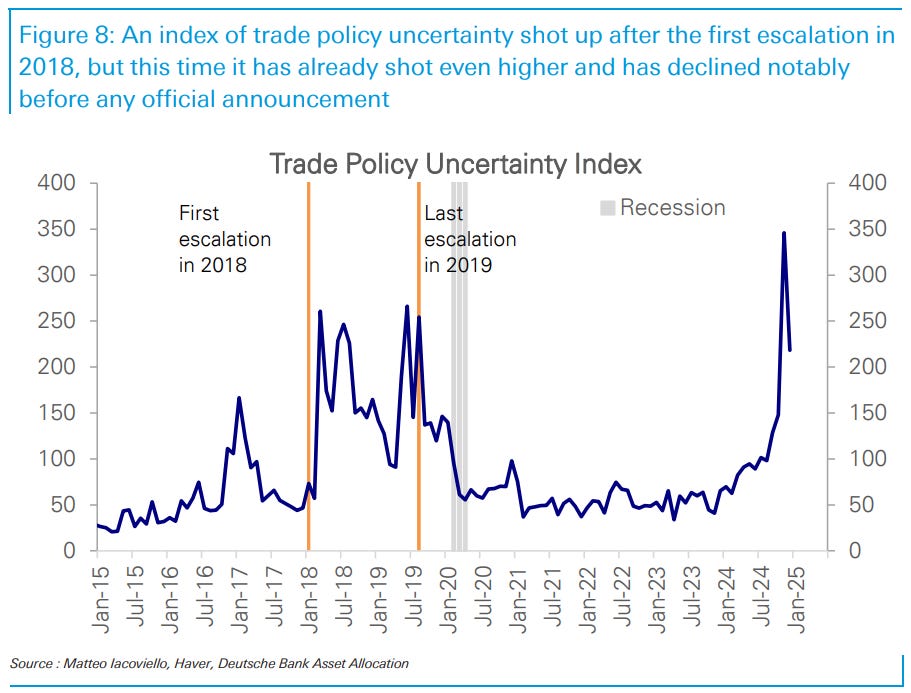

Investors position and flows based on TRADE POLICY UNCERTAINTY …

DB: Investor Positioning and Flows - Are Equities Complacent On Tariffs?

…Equities have rallied broadly to record highs with very little volatility despite a continued barrage of hawkish tariff headlines. This is in sharp contrast to the last trade war when equities saw a large selloff after the first announcement and then went sideways for 18 months accompanied by enormous volatility. Are equities being complacent this time?

We would make five points for why the equity market has not reacted more negatively so far: (i) rallies following close Presidential elections are very typical, reflecting a dissipation of event risk premium, and this one has largely been in line with past ones, with no discernible shifts in medium- or longer-run trend channels; (ii) tariff escalation is one of the most well anticipated policies this time; (iii) companies are battle ready after navigating a host of disruptions in the last few years, tariffs and otherwise; (iv) cyclical growth indicators like manufacturing PMIs have plenty of room for upside, unlike at the start of the last trade war when they were already at the peak of a cyclical boom; (v) leading with the tariff stick means growth boosting carrots can follow, i.e., the sequencing of policies led by tariffs first has been contrary to consensus expectations, but rather than being a negative, this should limit market selloffs because positive catalysts are yet to come, in contrast to the last time when they had already played out by the time the adverse tariff surprise arrived…

Same shop with an FOMC precap …

DB: January FOMC preview: All they need is just a little patience

We expect the Fed to keep rates steady at the January FOMC meeting and provide limited guidance about future policy decisions. While Chair Powell may not rule out a March cut as he did last January, the broad signals from the meeting should confirm that outcome is not likely. To this end, Powell could emphasize that the underlying strength of the economy and signs of stabilization in the labor market reinforce patience in removing further restriction.

Our baseline remains that a skip at the January meeting could turn into an extended pause this year. In our view, the nominal neutral rate is around 3.75%, and there is a need for the Committee to stay restrictive relative to that level. As such, the fed funds rate is likely to remain above 4% this year, with a base case of no additional reductions. For a full discussion of our outlook for the economy and the Fed, see our latest publication: "Trump II: Growth too fast, inflation too furious for Fed cuts".

#GotRATES … here’s some stratEgery for you … maybe NOT the best in the biz (institutional investor - wise) but a shope I’ve always found interesting who’s notes are very DEEP and the process and bench is just outstanding IMO …

MS: Buy US Treasuries Before The Buyers' Strike Ends | US Rates Strategy

The US presidential inauguration passed without the "day one" tariff increase many investors expected. The longer the administration decides on tariffs, the more comfort investors – currently on a buyers' strike – will feel about putting money to work. Buy US Treasuries before the strike ends.

Key takeaways

Investors who have been on a buyers' strike should grow more comfortable putting money to work as President Trump's second term progresses.

The inauguration ended with growth-negative immigration orders, not inflation-inducing tariffs. The longer this policy mix continues, the lower yields will go.

Lower inflation than feared, less growth than expected, and a Fed that cuts rates more than priced into markets should lead to lower US Treasury yields.

Investors should stay long US Treasury duration at the 5y key rate and stay positioned for a March FOMC rate cut. Buy the 1.375% Nov31s vs. TYH5 basis.

The January 28-29 FOMC meeting and prospects for a weaker January payroll report should catalyze the next leg lower in Treasury yields.

Same shop, thinking economically …

MS: US Economics Weekly: Day 1: Heavy emphasis on the border and trade

Restrictive trade and immigration policies featured prominently on 'Day One' of the Trump administration. Deregulation and fiscal policies drew less attention. We think markets are underestimating the effects of restrictive immigration on actual and potential growth.

Key takeaways

Review over immediate action: the administration indicated it would undertake a large-scale review of its trading partners. Tariff increases could come later.

Immediate action over review: President Trump issued a series of executive orders that are in line with our forecast for sharply reduced immigration.

Our base case is the policies that dampen growth and stiffen inflation (trade and immigration) are likely to come first. Growth-enhancing policies come later.

Rates move up. Rates move down … when they move UP (as they have recently) they RESTRICT the economy and so, undoes some of the Feds recent ‘handy work’ …

…Interest Rate Watch: 100 Basis Points Lower & 100 Basis Points Higher When the Federal Reserve concludes the two-day meeting of its Open Market Committee (FOMC) on Wednesday of next week, we expect policymakers to maintain the target range for the federal funds rate at 4.25%-4.50%.

The case for lower interest rates is less urgent today than it was in the autumn of last year when the labor market was showing signs of lost momentum and inflation was trending lower. Neither of those dynamics have done a complete about-face, but the economy enters 2025 with renewed momentum, and progress on inflation has stalled. Both of these dynamics were evident in the ISM’s survey of purchasing managers in the service sector. These businesses report that activity snapped back into action in December. Most sub-components notched gains, but, tremblingly for the FOMC, none rivaled the 6.2-point jump in the prices paid-component, which signaled the broadest increase in service sector costs since February 2023.

From that September meeting when the FOMC first lowered rates as part of a cumulative 100 bps easing, the yield on the 10-year Treasury has climbed 102 bps. The return of a positive slope to the yield curve is welcome, but a rise in longer-dated interest rates signals inflation expectations are creeping higher.

Next week brings the December reading for the Fed’s preferred inflation gauge, the core PCE deflator. By that measure, core inflation was 2.8% in November and our forecast is for that measure to stay put at 2.8% in next week’s report for December. That report drops after the FOMC meeting, so the FOMC will be forecasting as well, but it is clear that inflation is still above the 2.0% target. Take that alongside the renewed labor market momentum evident in the more than a quarter million jobs added in December and there is no rush at all to lower rates now.

We suspect that the ascent in the 10-year Treasury yield could restrict activity, and a question for next week’s Fed meeting is: Do Powell and other members of the FOMC see higher longer-dated rates as being restrictive as well? If so, the upshot would be dovish to the outlook for fed funds because whether policymakers view higher long-term rates as helpful in bringing inflation down or disruptive in restoring momentum to the labor market, it argues for lower short-term rates.

Financial markets are trying to gauge the degree to which Trump policy proposals—tariffs in particular—could affect the outlook for inflation and Fed policy. We do not look for much explicit guidance in this regard in the official statement, but it will no doubt be a topic that comes up in the press conference.

… Moving along TO a few other curated links from the WWW which maybe useful …

This first note is NOT, repeat NOT, gonna be something which ‘47 gonna wanna see … and is more a weekly recap of things rather than breaking any new ground BUT the point is one which runs counter TO HIMCO (noted HERE …)

Apollo: Interest Rates Higher for Longer Continues

The incoming data shows that weekly same-store retail sales are strong, daily debit card spending data is strong, daily TSA air travel data is strong, the JOLTS layoff rate is very low, WARN notices are low, jobless claims are low, and announced job cuts are very low.

Combined with the latest Atlanta Fed GDP estimate at 3.0% and a boost coming to growth and inflation because of the Fed cutting interest rates since September and higher animal spirits since the election, the bottom line is that the US economy is entering 2025 with some really strong tailwinds, and the market is underestimating the risk that the Fed will have to hike interest rates later this year.

Our chart book with daily and weekly indicators for the US economy is available here…

Note: Consists largely of debit card transactions. Source: Bloomberg, Apollo Chief Economist..

That said, and with Lacy Hunt / HIMCO latest in mind (noted HERE …), a fella who’s remarkably similar to Lacy — process and knowledge-wise …

EPB RESEARCH: The Sequence of the Business Cycle: Overview An in-depth overview of the Business Cycle Sequence and the EPB Four Economy Framework.

Making sense of the economy requires more than just tracking the latest data—it demands a framework for connecting the dots. The good news is that the economy doesn’t move in random spurts—it follows a predictable sequence.

This sequence has remained the same in every Business Cycle, from the inflationary 1970s to the more modern 21st-century recessions. Recognizing that sequence and following its predictable rhythm is critical for understanding where we are today and where the economy may be headed tomorrow…

…By synthesizing these sequential trends, the framework provides a repeatable, consistent, and structured way to approach the economic environment and resulting investment decisions.

While no single indicator tells the full story, creating buckets of indicators that all move at the same time in the overall sequence creates a more robust way to analyze the economy…

…Summary President Trump’s pro-growth agenda, a reprieve from rising rates, and solid earnings thus far have recently renewed investor optimism. Momentum has turned bullish as the broader market approaches record-high territory. However, market breadth measures have not kept up with the recent rebound in stocks, implying the latest advance has been relatively narrow. While deviations between price and market breadth can persist for extended periods, they can often foreshadow building vulnerabilities of a rally susceptible to stalling. While we are not making a call for an imminent correction, investors should not be surprised if one develops this year as history shows they occur at least once per year.

LPL Research expects stocks to move modestly higher in 2025, while acknowledging reasonable upside and downside scenarios. Upside support could come from economic growth, a supportive Fed, strong corporate profits, and business-friendly policies from the Trump administration. The most likely downside scenarios involve re-accelerating inflation, higher interest rates, and geopolitical threats that do economic harm.

… finally, something that impacts us all every. single. morning …

ZH: "Nervousness" Ripples Across Coffee Market As Prices Hit Fresh Record Highs

Arabica coffee futures surged to record highs on Friday, fueled by the ongoing global supply crunch. The most-active contract climbed nearly 2% in late morning trading, reaching the highest price levels on record dating back to 1972. The multi-year parabolic move in coffee prices only suggests higher Starbucks and/or supermarket market prices in the months ahead if hedges fail to offset bean inflation.

The big price jump has traders reducing their exposure to the futures market due to elevated costs, making the market more prone to volatility.

Bloomberg data shows aggregate open interest — or the number of outstanding contracts — has declined in the past five years while prices moved higher…

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Top 3 Substacks ever!