weekly observations (01.21.25): O/N news? "... peak in “anything but bonds” trade of 2020s..." (and oh, same firm jacks UP yld f'casts...); 10yy from 1870-

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

I interrupt this irregularly scheduled programming to bring you some news overnight. NO, not that of any sorta official meme coin (HERE) but that other press release o/n … THIS press releasefrom the FDIC …

Millennium Bank, Des Plaines, Ill. Assumes All Deposits of Pulaski Savings Bank, Chicago, Ill.

January 17, 2025 WASHINGTON — Pulaski Savings Bank of Chicago, Ill. was closed today by the Illinois Department of Financial and Professional Regulation, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. To protect depositors, the FDIC entered into a purchase and assumption agreement with Millennium Bank of Des Plaines, Ill., to assume all deposits of Pulaski Savings Bank.

QUESTION … might we be back to discussing ‘good’ as ‘bad’ and have rates hit a level that matter (think SVB)?

Team RateCUT and buyers of 5s, for example (see HERE), may have gotten another shot in the arm after this past weeks CPI and ensuing WallEE speak (also see HERE).

… Wednesday, in particular, saw the three major averages post their best intraday advance since November 6, 2024, while the bond market also saw some much-needed relief. The primary driver of the moves was the core consumer price index (CPI) reading for December 2024, which surprised to the downside. The favorable inflation data reignited bets that the Federal Reserve will continue to ease monetary policy…

Now back to this irregularly scheduled programming …

First UP, still waiting for Lacy Hunt / HIMCO Q4 note / thoughts and so I hope what follows will continue to provide some modest funTERtainment until further insights drop.

Alrighty, then. Lets jump in and have a quick look at 5yr yields on a WEEKLY basis on heels of pas couple / few days of a material BID (thanks, Wall-E, for adding some fuel to that fire) on heels of semi-cooperative data in the week just passed …

5yy WEEKLY: IF we look at the range as 4.65 - 3.40 THEN middle would be just north of 4.00 …

… AND then note weekly momentum overSOLD, crossing bullishly, might actually help explain exuberance in / around the spot on the curve especially for those celebrating CPI and WallEEEE in the week just past …

More below from those far better equipped to review and comment … moving right along TO some of the data inputs helping to create price action …

ZH: 'Renter Nation' Returns: Trump Victory Sparks Massive Surge In Multi-Family Unit Starts In December

… and this along with some other (housing) data added up by days end to this …

ZH: Trump Trade' Reignites, 'Dovish' Data Drives Everything Higher Ahead Of Inauguration

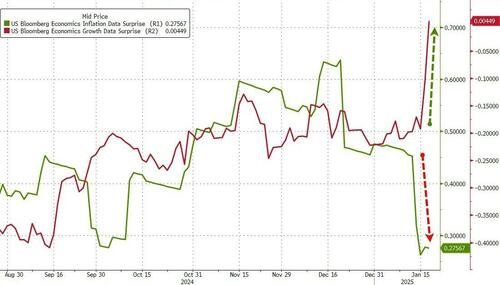

It was quite a week on the data side - with 'inflation' surprising bigly to the downside and 'growth' surprising to the upside...

… Add to that dovish comments from Fed Governors Waller and Goolsbee and we saw rate-cut hopes surge this week (erasing the post-payrolls hawkish shift)...

… AND I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox …

The British are coming … with a couple economic notes on surprising data and on Monday …

BARCAP: December IP and housing starts surprise to the upside

Industrial production increased 0.9% m/m in December, reflecting an increase in aircraft and parts output related to the end of the Boeing strike, as well as a rise in mining and utilities. Meanwhile, housing starts rose 15.8% m/m, benefiting from drier weather.

A burst of policy announcements on Trump's Day One should give better direction but is unlikely to provide markets with full clarity. This could create volatility, but for now US inflation and retail sales paint a benign macro picture. After shifts in rhetoric, the BoJ is ready to hike next week.

…US Outlook Caution: New traffic pattern ahead Next week will likely bring a flurry of post-inauguration policy announcements that should help illuminate the policy picture. For now, the macro picture looks favorable, with this week's December estimates pointing to relatively quiescent inflation and sustained resilience of consumer spending

Financial markets are likely to be volatile in the coming weeks as they absorb the details of the incoming administration’s policies. We discuss what investors should pay most attention to as the new administration takes office.

Different BRIT here … (Ryding)

Brean Economics Weekly: Discouraging December CPI, Economy Ended 2024 Strong, Debt Ceiling and Funding Markets

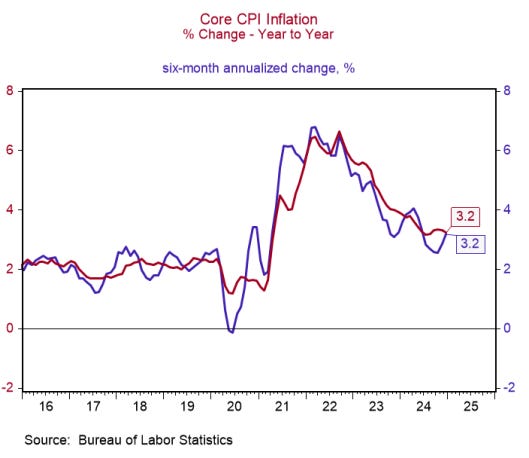

Another Poor Inflation Reading on December CPI The December CPI report was better than expected, with core CPI prices rising 0.2% in the month (slightly lower than the median consensus forecast of a 0.3% gain) and 3.2% year-over-year versus 3.3% on this basis in November. However, “better than expected” and “better” are not the same thing, and the December CPI report provide no support to the view, voiced by a number of officials this week, that there has been further progress toward the Fed’s inflation objective in recent months. Core CPI inflation on a year-over-year basis was either 3.2% or 3.3% in every month between June and December 2024. While inflation has moderated significantly since 2022, the lack of disinflation in the second half of 2024 is obvious in the chart below…

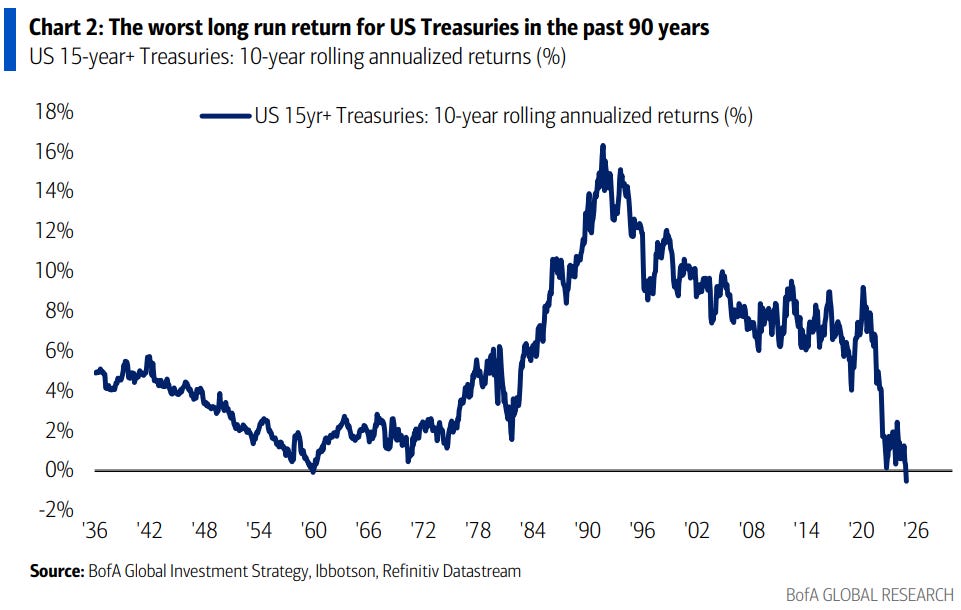

Bank of the land with a note showing UST returns as I’m always and forever a visual learner … I’ve also got note from same shop with NEW YLD F’CASTS … you know, new administration, new f’casts (? … everyone else get this memo too ?) …

… The Biggest Picture: at no time in the past 90 years has 10-year rolling return from US Treasuries been negative. It is now (-0.5% – Chart 2) – this is peak in “anything but bonds” trade of 2020s; by comparison, long-run returns for US stocks 13.1%, commodities 4.5%, IG bonds 2.4%, T-bills 1.8% (Charts 4-5).

…Rates: US rates without Fed cuts US: US rate forecasts revised higher after shift to no Fed cuts; 10y f’cast at 4.75%.

… We now revise our rate forecasts higher after the Fed call change. We revise our forecasts higher by 50bps across our forecast horizon, consistent with the shift in Fed cutting trough (Exhibit 4). Our 10y projections are stable at 4.75% across the forecast horizon in-line with our US economist expectations for robust growth (2-2.6% y/y), sticky core PCE (2.1-2.6%, y/y), & strong labor market (U3 4.2-4.5%) thru end ‘26 …

Best in biz still open to buying (front end)dip (in FFF6) …

… For the time being, the Treasury market remains decidedly in consolidation mode, and we struggle to envision a breakout in either direction. Moreover, with 10-year yields now 20 bp below the recent peaks, US rates are in a good position to respond to the Trump headlines without doing any technical damage. Said differently, with rates and the shape of the curve taking back some of the recent price action, even a kneejerk bear steepening won’t trigger a technical breakout. We’re reluctant to skew the risks in favor of lower outright yields at the moment, despite our medium-term constructive outlook on Treasuries. Trump has an incentive to make a dramatic policy entrance next week; a backdrop that reinforces the prudence of a more cautious approach to duration until the initial trade war salvos have been exchanged …

Moving on a bit and thinking about RISKS specifically those associated with L/T ‘flation expectations … and continuing to think rates on HOLD (or they go UP) …

BNP: US: Assessing risks to long-term inflation expectations

KEY MESSAGES

The significant rise of inflation expectations in the 10 January University of Michigan survey raises the question of whether elevated inflation has become embedded in expectations, and whether expectations might rise further if we see another period of above-target inflation in the coming years.

We think current inflation expectations are consistent with the FOMC’s 2% target, but we also think they are unstable and vulnerable to further upward shocks. This is a key difference between current economic dynamics and those from just before the pandemic.

We think keeping policy on hold through 2025 will help underpin stability in long-term inflation expectations.

The largest German bank in the land offering a note on investor positioning, flows and the like …

DB: Investor Positioning and Flows - Halfway Down To Neutral

Our measure of aggregate equity positioning fell from its mid-November highs near the top of the long-run historical band (z score 0.9, 96th percentile) to a 2-month low this week, about halfway down to neutral (z score 0.47, 71st percentile). The decline has been led by discretionary investor positioning (z score 0.47, 74th percentile) but that for systematic strategies (z score 0.66, 78th percentile) also slid lower this week. Survey measures of sentiment in particular fell to near the bottom of their historical bands earlier this week.

JPM asking same question as you and I …

JPM: Why have 10-year U.S. Treasury yields increased since the Fed started cutting rates?

We break down what’s causing the atypical move in 10-year yields and what to do about it.

The bond market has presented intriguing questions over the last few months:

Unusual yield movements: Why are 10-year U.S. Treasury yields rising over 100 basis points despite Federal Reserve rate cuts?

Growth and uncertainty: How are stronger growth expectations and macroeconomic uncertainty driving these changes?

Portfolio implications: What do these trends mean for your investment strategy?

…Change in 10-year yield post first Fed cut

Source: Bloomberg Finance L.P. Data as of January 15, 2024.

From the shop which bot 5s Friday (see HERE) … a note on stratEgery and on economics …

In its current form, the "Global Macro Strategist" first published in January 2020. The past five years saw change in macro economies and markets that investors came to believe in. Now the time has come to change the nature of this publication. Our global macro strategy effort continues. Stay tuned.

Global Macro Strategy We discuss our view to position for a March rate cut and go long US Treasury duration in the intermediate sector of the curve. We also discuss our view to turn bearish on the DXY and suggest selling the USD versus EUR, GBP, and JPY.

…As suggested last week, strategists will continue to publish weekly notes, individually, on all markets previously covered in this publication. In addition, we plan to change the format of Global Macro Strategist in the coming weeks to one that communicates our insights concisely and effectively. We will take care to not clutter your email inbox…

… The Time Has Come. Buy Bonds... As noted yesterday, we suggest investors go long duration in the US Treasury market by buying 5-year notes. The technical picture supports the position, in our view, with a major divergence between yield (having made a local high last week) and the moving average convergence/divergence (MACD) indicator (not having made a new high – see Exhibit 1)Exhibit 1.

Exhibit 1: US Treasury 5-year note yield candlestick chart

Source: Morgan Stanley Research, Bloomberg

Up until this point, the heightened risk of post-election better-than-expected economic data suggested a cautious, neutral stance toward government bond market duration. Strong performance of the macro hedge fund community suggested they would likely remain positioned for a continuation of the prevailing post-election trends: higher yields and steeper curves.

Thus, we advocated investors adopt a defensive, neutral stance on duration after the US election but advised them to prepare to buy a dip at some point. We think several reasons make now the opportune time for investors to turn long duration and buy 5-year notes.

Why now?

A fair amount of term premium already exists

Recent inflation data have provided more evidence of disinflation

Market pricing does not reflect the totality of fiscal policies

Carry and rolldown profile has improved…

Interest Rate Strategy In the US, we maintain receive fixed March FOMC OIS rate, long UST 5y, and M5/Z6 SOFR futures curve flatteners. In the euro area, we enter long RXH5 133.5/134.5/135.5 call ladders, maintain long 5y5y real yield, and 2s10s BTPs steepeners versus Bunds. In the UK, we enter 1Y1Y/2Y1Y SONIA steepener and maintain long 30Y ASW. In Japan, we maintain long 20y JGB versus pay 5y OIS, JGB 5s10s ASW box flattener, and pay 10y on 2s10s20s fly…

…United States | Buy UST ahead of the expected March cut

As expected, inflation decelerated in December, keeping the door open for a cut in March. FOMC members welcomed the softer print, but the next inflation readings and policy announcements are central. Sooner and higher-than-expected tariffs can take March off of the table.

Key takeaways

Inflation came in below expectations, we are now tracking 0.17% m/m core PCE for December.

Retail sales were strong, consistent with the current momentum and last week's employment report.

Our base case: A 25 bp cut in March as disinflation continues and policy announcements are broadly aligned with our expectations for gradual tariffs.

Another economic week ahead offered by the Swiss …

…Economic Comment: no January cut but more to come The "no cut" narrative's momentum, fueled by last week's employment report, seems unstoppable, even in light of this week's CPI. The chances of slowing that freight train between now and the March FOMC seems fleeting. Looking ahead to the January FOMC meeting, we doubt Chair Powell rules out a March cut, but he and the FOMC's already heightened inflation concerns likely remain. In our view, the December employment gain was helped by residual seasonality and other payback, and January may see similar support too. To us, that does little to alter the trend. However, absent revision, the December gain will simply be in the three-month moving average for, yes, three months, an argument in favor of a prolonged pause. In four weeks, we expect nonfarm payroll employment to revise down by ~700,000 jobs, reflecting the employment report's substantial overstatement of actual labor market strength. The imputations will be updated too, and the sample refreshed. The FOMC could be handed a new contour of employment in a few weeks, and the forward implications of the CPI for PCE prices look favorable. It's a close call, but maybe the March cut odds are not as low as one might think…

United States: Riding the Wave The Consumer Price Index ended the year at 2.9% year-over-year, which is a minor improvement from its 3.1% rate in January 2024 and points to stalled progress on the road back to the Federal Reserve's 2% inflation target. We now look for only two 25 bps rate cuts in the second half of 2025 and expect the FOMC to hold at a target range of 3.75%-4.00% through 2026…

…Interest Rate Watch: FOMC Likely to Enter an Extended Pause in Its Recent Easing Cycle We share the widely-held expectation that the FOMC will maintain its current target range of 4.25%-4.50% for the federal funds rate at its upcoming meeting on January 29. We also think the FOMC will keep rates on hold until the second half of the year before easing again…

Finally, from Dr. Bond Vigilante, with a long-term look at 2s, 10s and in Fed context …

… Our view has rapidly become the consensus view in recent weeks, especially after Friday’s strong employment report. That view can be described as a “higher-for-longer” interest-rate outlook, but “normal-for-longer” is the way we prefer to look at it. One of the reasons that we dissented over the past three years from the consensus forecast that a recession was coming is that we believed that the Fed’s monetary tightening simply brought interest rates back up to their normal levels in the years prior to the Great Financial Crisis and wouldn’t unduly stress the financial system, culminating in a recession (Fig. 1 below).

In his September 18, 2024 press conference, Fed Chair Jerome Powell said that the 50bps cut in the FFR announced that day by the Federal Open Market Committee (FOMC) was simply a recalibration of monetary policy: “So we know that it is time to recalibrate our policy to something that is more appropriate given the progress on inflation and on employment moving to a more sustainable level. So the balance of risks are now even. And this is the beginning of that process I mentioned, the direction of which is toward a sense of neutral, and we’ll move as fast or as slow as we think is appropriate in real time.” …

… Moving along TO a few other curated links which maybe useful …

First up ahead of Monday, an angle of tariffs impact on the Fed …

The Tax Foundation estimates that if 60% tariffs are imposed on China and 20% on everyone else, the average tariff rate will increase to 17.7%, see chart below.

With imports making up 14% of GDP, the impact will be a jump in inflation, potentially as high as 0.5 percentage points.

With core PCE inflation already too high at 2.8%, significantly above the Fed’s 2% inflation target, this could force the Fed to raise interest rates again.

Note: The 17.7% figure represents a weighted average of the proposed tariffs, a universal 20% tariff on all imports and an additional 60% tariff on Chinese goods. These tariffs are applied to the current import values, and considering the share of imports from China, the average rate for 2025 has been estimated. Source: Tax Foundation, Apollo Chief Economist

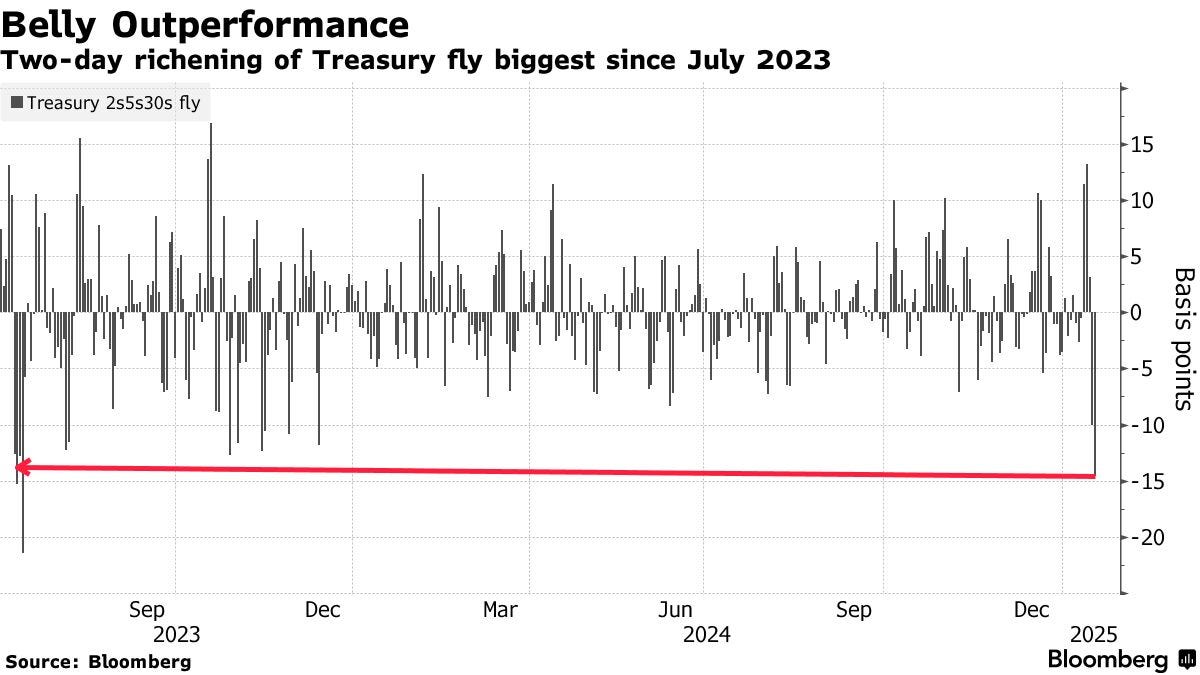

Next up a couple of very best from BBG — EBB on positions and Cam Crise …

Bloomberg: Treasury Futures Traders Shake Up Positioning on Fed Cut Bets

Open-interest changes point to short-covering and new longs

Five-year sector’s outperformance is strongest in a year

… Changes over the past two days in open interest — the number of contracts in which futures traders have positions — are consistent with exits from short positions in two-year notes and new longs further out — particularly in five-year Treasuries.

The shift comes after a one-two punch of consumer price inflation data released Wednesday that showed core prices rose in December less than economists estimated, and Federal Reserve Governor Christopher Waller’s remarks the next day that officials could cut rates again by mid-year if the trend continues.

Bond investors at Franklin Templeton “still think a few Fed rate cuts are left” and have extended their rate exposure to around five years, chief investment officer Ed Perks said. Yields “are near the upper band of where they likely trade,” he said.

The recent changes in open interest, as tracked in CME Group Inc. data, show a steep drop in two-year note and increases in the five- and 10-year note contracts. For the two-year, the drop was worth about $3.6 million per basis point in risk, equal to around $20 billion of underlying securities. The increase in the five year was the biggest for the March contract since it acquired front-month status in November.

Interest-rate strategists at Morgan Stanley late Thursday recommended setting long positions in the tenor in anticipation of a Fed rate cut in March, which remains a minority view. The swaps market prices in just six basis points of easing for March, or about 25% odds of a quarter-point move…

Bloomberg: Waller's Dovishness Is Built On Shaky Ground

… Arthur Burns, the bank’s Chair in the 1970s, invented core inflation, first taking energy and food prices out of the headline measure. He went further, eventually stripping out almost two-thirds of the basket.

When he left, inflation was near 7% and soon rose to almost 15%…

While Scotty no-neck Minerd is missed, the shop he created hard at work …

Our 10 Macro Themes for 2025 tell the story of a global economy poised for geopolitical realignment, bringing the promise of heightened volatility as well as conditions that we believe will drive compelling, long-term risk-adjusted returns for active fixed-income investors.

Popular Discontent Will Disrupt Global Policy, Elevate Volatility

A Shifting Geopolitical Landscape Will Realign the Global Economy

U.S. Economy Will Outperform, as Other Economies Face Headwinds

Reshoring, AI, and Power Needs Will Fuel Strong U.S. Investment

Global Disinflation Will Allow Central Banks to Ease Further

Runup in Equities Will Show Signs of Fatigue

U.S. Yields Will Remain in a Higher, More Normal Range

Investor Demand and Strong Fundamentals to Contain Spread Widening

Fiscal Consolidation Will Take on New Urgency

Attractive Opportunities for Active Fixed-Income Management

More on POSITIONS …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

So let me get this straight, if labor market tight thats good for wage growth and so, rate cuts or hikes? I forget …

NORDEA:Macro & Markets: Signs of a tighter US labour market ahead

In our view, there is a clear risk that the US labour market will become even tighter during 2025. This could limit further decline in wage growth and therefore the progress on inflation.

Are you curious what bonds did on tariff announcement days?

They went up, mostly. People try to argue that tariffs are inflationary but they are not. Inflation is a persistent rise in prices. Tariffs are a one off shock like a sales tax. They create a step change higher in the price level, but no inflation. Bonds look at the future path of growth and inflation and tariffs don’t really affect that very much.

In fact, tariffs have a negative economic impact as trading partners retaliate and they are bad for risky assets, so the announcements create a flight to safety (buy bonds) trade.

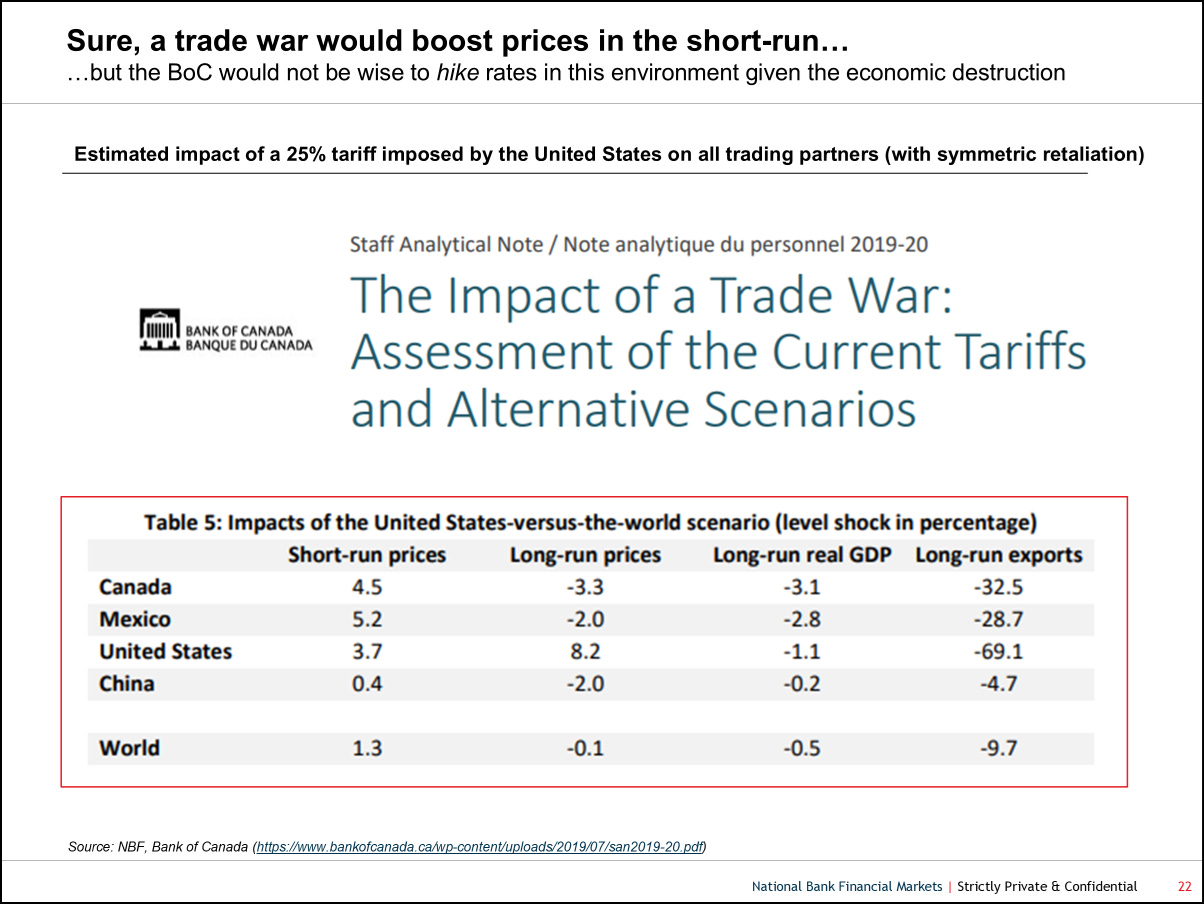

Here’s a worksheet from the Bank of Canada.

Don’t sell bonds on tariffs!

The madness of King Waller and the weaker-than-expected PPI and CPI figures triggered a zippy rally in bonds this week as we once again hit the wall on Fed expectations just as people start talking about a resumption of rate hikes. The bar for the Fed to hike rates is incredibly high and the bar for them to cut rates is like:

So every time we get to a point where someone calls “rate hikes!!”, yields do the Fosbury Flop.

Here’s the highlight reel for 10s this week.

The Bank of England also came in super dovish this week, arguing that sky-high gilt yields are a reason to frontload rate cuts. This might be true in the UK, but the irony is that if the Fed cuts to try to tame the long end, the long end will sell off more as the Fed’s inflation fighting credibility will further erode. To tame the long end, you often need to hike rates, not cut them. That is especially true in emerging bond markets such as Mexico, Brazil, and Great Britain. Hard to say if BoE cuts will help the gilt situation, but they should definitely hurt GBP.

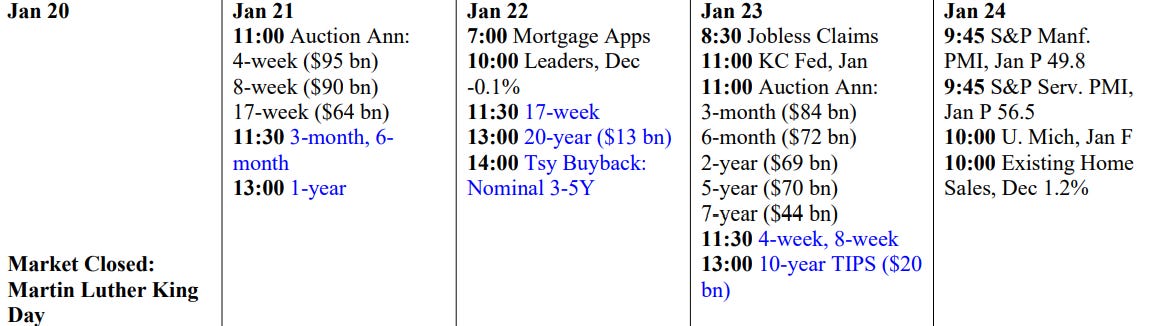

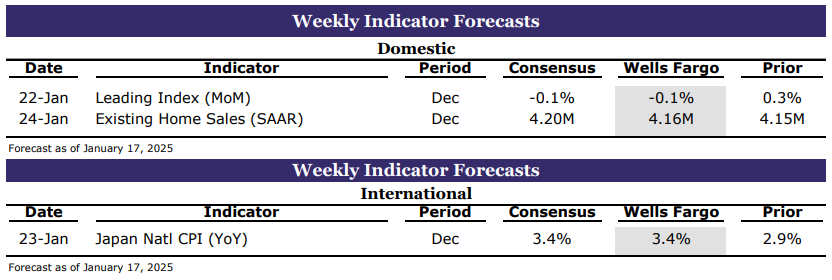

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Ahead of whatever snowfall is to come this way, am thankful to report I’ll be INSIDE watching football today / tomorrow, for the most part, and do NOT relate any longer to this fella …

… been there, done that and NOW these fellas are pulling ME and helpin’ shovel. To any / all those out there, well, enjoy the ride (or giving THEM that ride) as time certainly does fly by ….

THAT is all for now. Enjoy whatever is left of YOUR weekend …

{kind=link}

{kind=link}

Fosbury won the Gold Melal, in Mexico.

Summer Olympics 1968.

First Olympics I ever saw...

Kip Keno from Kenya, won the Mile.

Jim Ryan, from the US, fell down.

And the Black men quenched their fists on the metal stand, which I didn't understand what that meant,at age 9.

The Fosbury Flop, I remember. He went over on his back..I think he got a Metal in those Olympic games..

Waller is either very smart or very dumb. I thought I liked him, maybe as

the next Chairman, but he did surprise me with his willingness "to cut" in the face of stubborn inflation.

2025 will be Fascinating....