weekly observations (01.13.25): "...We raise our interest rate forecast on the back of our revised Fed call..." -everyone (incl JPM); "6th year of 3rd Great Bond Bear Market of past 240 years" -BAML

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Meet the new year, same as the old year. The more things change the more they stay the same.

I offer to you the following note as time / space filler as I continue to wait for latest year-ending quarterly note from Dr. Lacy Hunt.

First UP, a visual of yields which resonates with ME … 2yr yields WEEKLY with some context that 2s are an effective market pricing mechanism of FedFund expectations …

… what’s that saying, pricing leads narrative creations, or something something like that?

What follows below are more than one ‘updated call’ and this, not too long after Global Wall performed that #2025 dart throwing exercise … more on that in a moment.

For NOW, though, I see 2s nearly in middle of their larger range (5.10 - 3.50) and at the same time, I’m seeing WEEKLY momentum at what appears to be an overSOLD extreme. Not YET any signal buying should be done and I’d say Team RateCUT will likely wait until they see the whites of bearish extremes eyes before covering and getting long …

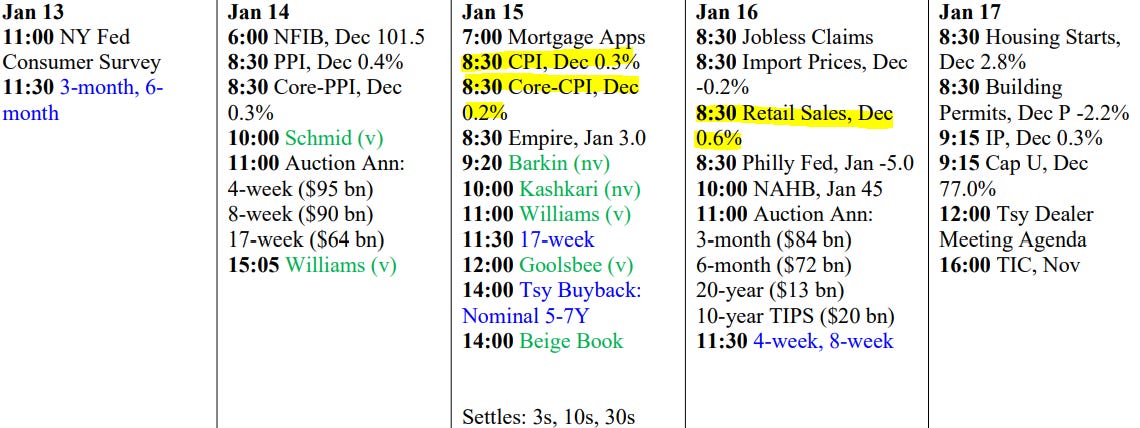

Clearly Team RateCUT took a hit yesterday and we all look ahead TO the coming weeks CPI.

Data, though, doesn’t seem to be cooperating and markets recognizing this. Guessing, then, narratives (below) will being reflecting this as it becomes more acceptable to say these quiet things out loud…

And with that — price action — in mind, coming on heels of Friday’s NFP data, a couple / few reCAPa-thon links for reference and review as the data once again BEAT in a positive way … so an UPSIDE SURPRISE … and so, the kneejerk HIGHER (above) …

ZH: Scorching Hot December Jobs: US Unexpectedly Adds Massive 256K Jobs In December, Smashing Estimates, As Unemployment Drops

… in addition TO NFP there was also some confidence measures …

ZH: UMich Inflation Expectations Soar To Highest Since 2008 As Democrats Confidence Slumps

… Alrighty, then.

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox … I’m going to try and shorten this ‘weeklies’ recap / excerptation excecise a bit in an effort to save time but still highlight a thought / a visual and some more important sellside recon (and narratives) which you can then dazzle your friends ‘round the water cooler in the days ahead.

…Rates: Hawkish Fed = higher rates US: Large US rate sell off & steepening due to eco surprises & hawkish Fed. We favor soft belly longs. Back end spread widening post Barr is fade b/c high “bar” to richen USTs.

…The Biggest Picture: Treasuries entering 6th year of 3rd Great Bond Bear Market of past 240 years (Chart 2); global shift to populism, rising US government debt (set to hit $40tn on 6th Feb'26, exactly 400 days into Trump 2.0), inflationary central banks; recession and/or default needed to reverse secular bond bear of 2020s….

NEXT a couple / FEW global ECONOMIC notes from the UK including a change in a call …

BARCAP December jobs report: Strong across the stack

The December payroll employment showed a strong gain of 256k, bringing the 3mma increase to 170k, and the unemployment rate declined to 4.1%, indicating a tighter labor market. With the report signaling more momentum in jobs and income into 2025, we expect the FOMC to cut rates only once this year.

Given the strong December employment report and the increase in household inflation expectations, we now expect the FOMC to cut rates only once this year, by 25bp in June. We then expect it to resume cuts in 2026, with a 25bp cut in June, September and December.

While Trump's ongoing MAGA rhetoric boosts uncertainty about domestic and foreign policies, the US macro reality is one of rising Treasury yields, a strengthening dollar and a labour market too hot to allow for any Fed cuts soon. All this contrasts with softer fundamentals in Europe and China.

…US Outlook When tempest tossed, embrace chaos Winds are blowing, literately and figuratively, intensifying uncertainty about what the flood of upcoming policy announcements on January 20 will mean for activity and rates. With activity resilient and disinflationary confidence intact, the FOMC seems content to downplay rate hikes.

… Market participants are beginning to revise Fed calls for 2025 – scaling back rate cut estimates. To be fair, the labor market has proven to be even more resilient than many, ourselves included, thought during Q4. As a result, the FOMC has more flexibility in pushing back further normalization until later in 2025, perhaps even into the second half. However, our base case remains that the Fed will eventually resume the path back toward neutral once the initial round of uncertainty surrounding Trump’s return to office is resolved. By the second half of the year, the Fed will have much better context for the changes coming from the White House, and if the data continues to come in as strong as the December employment report, monetary policymakers will be afforded even more time to make sure price stability has been reestablished.

The bearish tone in the Treasury market is difficult to fade at the moment, and so we won’t attempt to fight the move …

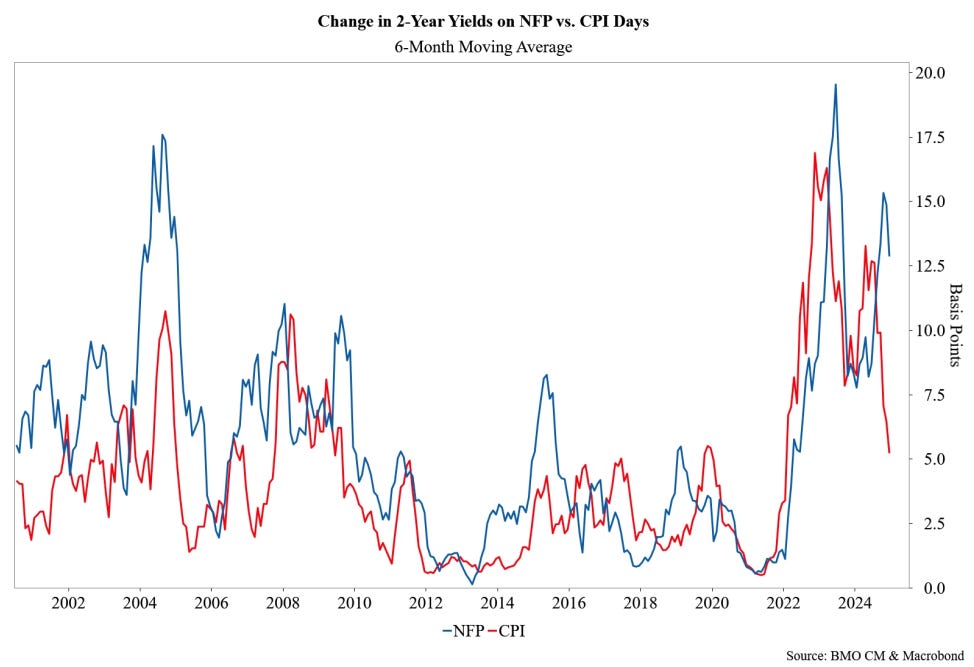

… Heading into this week's inflation data, we're reminded that CPI-day volatility in the front-end has decreased substantially in recent quarters. For context, 2-year yields moved just one basis point on the day of the November CPI release, dropping the 6-month moving average to 5 bp, a three-year low. The 6-month average CPI-day move in 2-year yields has trended downwards since last spring with the bulk of the decrease in volatility occurring in 4Q24. While CPI releases have seen increasingly muted market responses, NFP trading sessions have seen the opposite trend. Historically, the 6-month average change in 2s on the release days of these two measures tended to be closely aligned, however, there's been a meaningful divergence between the indices since the middle of 2024. Specifically, the average change in 2-year yields on NFP-day topped 15 bp in October and remains above 12 bp, while the same measure for CPI-days has fallen to 5 bp. The 7 bp spread between the two indexes is nearly the widest it's been over the last two decades …

… This week, we'll look to buy a dip in October Fed Funds Futures (FFV5) in the event that modestly stronger inflation/ spending data drives the futures market to price in less than 20 bp of rate cuts by the September FOMC meeting …

Resilience in the December jobs report reinforces our existing call for no Fed rate cuts in 2025. The risks to this view are now two-sided, with hikes possible if a soft landing for the US economy moves out of reach.

Job gains were broad across industries, particularly in cyclically sensitive ones, and the jobless rate fell to 4.1%.

Our base case is the US economy and job growth slow on average in 2025. However, more jobs reports like this one would boost the chance that the Fed hikes rates in 2025, as upside risks to inflation would combine with signs of a no-landing economy.

We expect core CPI to rise 0.25% m/m in December, which would make for its fifth straight rounded 0.3% print.

We look for a pop in rent inflation after a particularly soft November reading, with used vehicles driving a softer core goods print and non-shelter services staying resilient.

Stronger seasonally-adjusted gasoline prices and sturdy food inflation should push headline CPI to 0.4% m/m, which would be its highest monthly print since March 2024.

While our forecast translates to a relatively more benign PCE inflation estimate, we think Fed officials will remain wary about the inflation outlook, particularly on the heels of a strong December employment report and jump in inflation expectations to start the year.

… Germany recapping NFP (think Fed on sabbatical) and DB remaining BEARISH duration …

DB US Economic Chartbook - December Jobs: Signs of stability support Fed sabbatical

Another strong payrolls print in December (256k) has helped to stabilize the employment trend

Bond Market Strategy Trade update: Bearish US duration We briefly reassess our key macro trades for the new year, starting with our bearish US duration view. We maintain our short 10Y SOFR for now but remain open to changing our view if there is any evidence that the more normative policy outcome discussed in our 2025 outlook becomes more likely. Given the recent repricing, we have moved our indicative stop higher to 4.00% and, more modestly, our indicative target up to 4.30%.

The Fed’s reaction function should remain asymmetrically dovish, with hikes likely off the table until we see a continued descent in the u-rate. With 2s in the middle of the Fed funds target range, money markets not pricing in a full cut until 4Q25, we hold longs in 2-year Treasuries, but we recognize more limited upside given our revised Fed call

Further out the curve, the 100bp+ selloff since prior to the September FOMC meeting is partially explained by a more proactive Fed stance, which supported higher growth expectations...

...However, yields have risen in excess of their fundamental drivers, with fiscal expectations and rising term premium explaining this divergence. Valuations are cheap and the magnitude of the sell off is in line with other major moves over the last decade, but we expected more limited mean reversion and have duration exposure via our front-end long

We recommend adding 5s/10s flatteners to fade some of the recent steepening, but also as a hedge to our long at the front end

We raise our interest rate forecast on the back of our revised Fed call and higher term premium. We see 10-year yields at 4.55% at YE, from 4.25% previously. We expect 2-year yields to trough at 3.85%, on top of the Fed funds rate around the time of the last cut in September, before rising back to 3.95% at YE25

… and from another shop, ‘must see TV’ if you will (and IMHO) …

2025 starts with a bang: another run at 5% 10-year US Treasury yields and equally concerning moves in the UK gilt market place the focus squarely on fiscal credibility. Will central bankers decide the economic outlook demands tighter financial conditions, or will they push back? Stay neutral for now.

…Interest Rate Strategy United States We stay patient and neutral on duration. The upside surprise on nonfarm payrolls prompts us to no longer suggest playing for a rate cut at the January FOMC meeting or to suggest receiving the 7y point on the 3s7s30s SOFR swap fly with PCA risk weights.

…Defense wins championships, but don't forget you still have to score…

…A note on our bullish bond market year-ahead outlook Our description of the government bond market outlook for 2025 advocated for a bullish stance for the year as a whole. We did not suggest the exact timing of when investors should wade into long duration positions because we use our weekly publications for delivering that type of advice. We always separate the views captured in our mid-ahead and year-ahead outlooks from those delivered in our weekly or ad hoc updates.

If the December CPI report shows inflation consistent with or lower than our economist's forecast (core CPI at 0.26% M/M), then we would be inclined to play for a rate cut at the March FOMC meeting. We look to evaluate that risk vs. reward in the coming week after PPI and CPI reports.

We also discuss recent developments related to bank regulation and subsequent movements in Treasury swap spreads. Looking forward, we see three areas that could meaningfully impact spreads over the next few months: (1) Further bank regulatory developments, (2) a pause in QT, and (3) a continuation of near-term trends.

Finally, we analyze Treasury International Capital (TIC) System data on Cross-Border Portfolio Financial Flows to determine if there is evidence of foreign investors engaging in “buyers strikes” during specific time periods. Findings show that foreign investors exhibit “buyers strike” tendencies ahead of US presidential elections, while there is less evidence than expected of these tendencies during summer months.

MS US Economics: December employment: So much for downside risk

The report should reduce concerns about a weaker labor market: payrolls +256k, UE rate -0.15pp to 4.1%. Services drove the acceleration: upswings in holiday-related retail & transport, and also in business services. Payroll earnings rose 5.9% saar pace in 4Q. Fed cuts are about inflation now.

The economy has momentum; we are tracking growth of 2.5% q/q saar in Q4. While most FOMC members continue to guide markets to additional policy rate cuts, restrictive trade and immigration policies keep uncertainty about the outlook high. We think December CPI will keep a March cut in play.

Key takeaways

Employment surged in December and our tracking estimate for personal consumption rose to 3.0% q/q saar in Q4.

The Fed is signaling that it foresees further rate reductions ahead, but providing clarity is difficult when tariffs may be coming.

We expect core CPI inflation to slow to 0.26% m/m in December, as recent auto-related strength in goods prices begins to abate.

… United States Let the games begin It’s been an eventful start to the year as investors digest a bevy of political headlines ahead of the presidential inauguration on 20 January. The minutes of the December FOMC meeting confirmed a cautious Fed and a hawkish shift on concerns over inflation. The market is now pricing in an extended pause with the next 25bp cut mid-year, sustaining a further sell-off in Treasuries led by the long end. The 10yT yield is gradually approaching the 5% threshold, with the bulk of the recent increase led by a rise in term premia and expectations of a higher terminal fed funds rate. Will the sell-off continue? A momentum led sell-off in the 10yT toward 5% is a buying opportunity, in our view. A decline in equity risk premia and a tightening of financial conditions are likely catalysts for a reversal. After the job report, we look to CPI next week. Following four consecutive months of 0.3% mom increases in core CPI, any upside could prompt the sell-off to resume.

Initiate 2s10s flatteners and belly long in 2s5s10s or 5s10s30s if 10yT approaches 4.75%.

While we are neutral on duration, we prefer offsetting short 10yT positions by going long 10y Bunds…

… Swiss NFP recap (and got long last year and sticking with it) …

…The Week Ahead: Waiting for Wednesday Rising concern among FOMC members visible in the minutes released this week adds emphasis to the December CPI data released Wednesday. Next week will be our last chance to hear from FOMC speakers, with a number speaking after the release of the CPI. We expect the report to come in a little hotter than consensus expects, with core CPI expected to rise 0.29%, leaving the 12-month change at 3.3% for the fourth consecutive month. Alan's full preview outlines all the moving parts, but we currently expect core PCE remains a little softer than the core CPI at 0.23% in December. The run of inflation data, including producer and import prices, as well as the CPI, will inform this tracking, though. We expect a healthy holiday spending season with December retail sales to rise 0.6% and control group sales up 0.4% over the month. Industrial production likely improved 0.3% in December and housing starts are expected to have risen too, up 41K to 1330K. The Week Ahead begins on page 19…

• Long-end rates have moved higher due to a repricing of the expected end point of the Fed's ratecutting cycle, higher term premium given fiscal policy uncertainty, international developments, and the seasonal January supply effects.

We moved tactically long duration late last year by taking exposure to the 5-year part of the US curve and maintain our Attractive asset class recommendations on high grade and investment grade bonds. We forecast lower rates from here over the course of the year and given recent curve steepening, yield pick up is now available by switching out of cash.

Our rationale is based on our view that the Fed will cut rates more than the market currently expects. Interest rates remain in restrictive territory. There continues to be cyclical weakness in the interest-ratesensitive parts of economies such as housing. Marketbased inflation expectations remain stable. And the growth-unfriendly, rather than friendly, policy items appear to be first on the agenda from the new US administration.

… AND a couple notes to consider — one on PERCEPTION OF PRICES and another on on cutting rates but / and higher yields … wait, what?

WELLS FARGO: "Buy It Before Prices Go Up" Mindset Stokes Inflation Expectations

Summary Consumer sentiment slipped slightly to 73.2 in January from 74.0 in December, but the real story in today's report is that inflation expectations jumped sharply higher. The 3.3% expected rate of inflation over the 5-10 year time horizon rose to the highest since 2008.

… Inflationary expectations tend to beget actual rises in prices, a fact that is often stressed by Fed policymakers. The thought here is that buying-in-advance to avoid future price increases actually creates more demand which in turn stokes the fire of inflation. That's why it may be concerning that consumer long-term inflation expectations (5-10 years ahead) broke out of its narrow range rising to the highest level since 2008 in early January (chart).

This “buy it before the price goes up” mindset is detrimental to the gradual progress that has been achieved in bringing prices down, an improvement that is also evident to today's report. Take, for example, the 4% increase in Current Conditions which was “largely supported by softening worries over current prices”. The report noted that about a third of consumers spontaneously cited high prices as weighing down their personal finances, down from 47% in August 2024 and the lowest seen since February 2022.

…Interest Rate Watch: Cutting Rates, but Higher Yields When U.S. markets closed on Sept. 17, the 10-year Treasury yield was 3.65%. The next day, the FOMC announced that it was reducing the federal funds rate by 50 bps, the first rate cut by the central bank since 2020. Since then, the FOMC has cut the fed funds rate by an additional 50 bps, but the 10-year Treasury yield is roughly 100 bps higher at 4.72%. What happened?

One answer can be found in how markets have come to see the path of policy for 2025. Back in September, fed funds futures pricing implied a federal funds rate below 3% at year-end 2025. Today, markets expect the policy rate to be closer to 4% at year-end. Stronger economic data likely played a role in changing those expectations. A run of weaker-than-expected economic data over the summer that included a concerning rise in the unemployment rate was followed by better-than-expected employment reports and a string of warm inflation readings. The Bloomberg Economic Surprise Index was near the lows of the year in late August but subsequently climbed back to the annual highs by November.

The Fed's willingness to be proactive in the face of deteriorating labor market data also probably played a role in higher long-term interest rates. When the FOMC cut rates by 50 bps, the committee sent a strong signal that it would act to combat a softening labor market even with inflation still a bit above the central bank's target. This in turn may have reassured investors that, with a supportive central bank, the probability of a "hard landing" had been reduced, and rate cuts today would help reduce the risk of even bigger rate cuts down the road.

Finally, the move in the 10-year Treasury yield probably has not been solely a function of the expected path of the federal funds rate. Longer-term interest rates are a function of expectations for short-term rates over time as well as the premium associated with the uncertainty that comes with locking up money for an extended period of time. Most estimates of the term premium have risen in recent months. Given the significant uncertainty about the economic policy outlook over the next few years as the new Congress and administration take office, it makes sense that investors are demanding a bit more yield to be compensated for the murky outlook that is on the horizon.

… Moving along TO a few other curated links from the WWW which maybe useful …

This first one comes from one who’s clearly NOT on Team RateCUT

This week, the employment report came in stronger than expected, weekly same-store retail sales were better than expected, and Prices Paid for ISM Services came in higher than expected.

The bottom line is that momentum in the economy is strong, and the narrative that monetary policy is restrictive is wrong.

Combined with higher animal spirits and the latest Atlanta Fed GDP estimate at 2.7%, we see a 40% probability that the Fed will hike rates in 2025.

Our latest chart book with daily and weekly indicators for the US economy is available here.

Oil prices are surging, with gold, silver, copper, platinum, palladium, and other metals also climbing. Natural gas has reached a two-year high, and agricultural commodities are steadily gaining ground. Breakeven rates continue to rise as well.

It’s clear that inflation is picking up speed, even as the Fed searches for reasons to proceed with further rate cuts.

The combination of rising consumer prices and a financially repressed environment creates an ideal scenario for hard assets to thrive in my view.

…4. Normal no Longer? Policy rates have peaked as central banks pivoted to rate cuts. Bond yields also peaked —initially; but that’s changing. Both lines in this chart are going to be at the mercy of the macro-risk-sandwich (a binary prospect: recession = down, reacceleration + inflation resurgence = up).

For a market hooked on rate cuts, 2025 could present a wake-up call; we may need to be prepared for pauses and “unpivots” instead of just consensus cuts.

AND then there’s WOLFY…

WolfST: Treasury Yield Curve Steepens, as Long-Term Yields Coddle Up to 5% while Short-Term Yields Stay Put, Not Seeing Any Rate Cuts. Mortgage Rates Rise to 7.24%

30-year Treasury bonds sold at auction on Friday at highest yield in at least 16 years despite Fed's 100 basis points in rate cuts.

… The 30-year bonds are normally sold with a substantial term premium, as investors demand to be compensated for taking the risks that inflation and interest rates might rise over the 30-year period. Before the rate hikes started in March 2022, the 30-year yield was about 200 basis points above short-term yields. That’s the term premium. Currently, the term premium is about 60 basis points. So there is still a long ways to go.

…Over the long term, the average 30-year fixed mortgage rate didn’t drop below 5% until the Fed started buying MBS in early 2009. Trillions of dollars of QE and near-0% policy rates eventually pushed mortgage rates below 3% during the pandemic. Those mortgage rates were quirks of history and are unlikely to come back. So maybe it’s time to get re-used to these mortgage rates that were normal before 2008.

… more on NFP

YAHOO: The labor market’s upside surprise: Chart of the Week

finally, on EARL

ZH: Oil Surges To 3-Month-Highs As US Escalates Anti-Russia Sanctions

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Thoughts on the fires? I think this is pretty likely going to start a recession in the US. It’s an absolute disaster for the 5th largest economy in the world. The government has been shown to be incompetent. It’s inflationary, hurts supply chains, and contributes to the housing shortage. It might take a few weeks to realize the scope of the damage, but I think it’s absolutely devastating.

Thoughts on the fires? I think this is pretty likely going to start a recession in the US. It’s an absolute disaster for the 5th largest economy in the world. The government has been shown to be incompetent. It’s inflationary, hurts supply chains, and contributes to the housing shortage. It might take a few weeks to realize the scope of the damage, but I think it’s absolutely devastating.