… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are sharply lower and the curve flatter after a regional bank bought large chunks of a recently failed banks' business and also after Friday's US rates price action traced out clear bull trend exhaustion signals (see below). DXY is UNCHD while front WTI futures are higher (+1.1%). Asian stocks were mixed, EU and UK share markets are all higher (SX5E +1.1%, SX7E +1.9%) and ES futures are showing +0.55% here at 6:55am. Our overnight US rates flows were unobtainable this morning while overnight Treasury volume was ~65% of average overall- except in the 30yr (209%)...

… and for some MORE of the news you can use » IGMs Press Picks for today (27 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Here are a couple / few things from Global Wall St as well as the intertubes (all in addition TO what was noted HERE Saturday morning),

What’s unclear for us is how much of these banking stresses are leading to a widespread credit crunch. And then that credit crunch… would then slow down the economy

And before Ka$hkari comments, shortly AFTER hitting send HERE Saturday morning, another BBG ‘scoop’ made it’s way ‘round the intertubes — ZH,

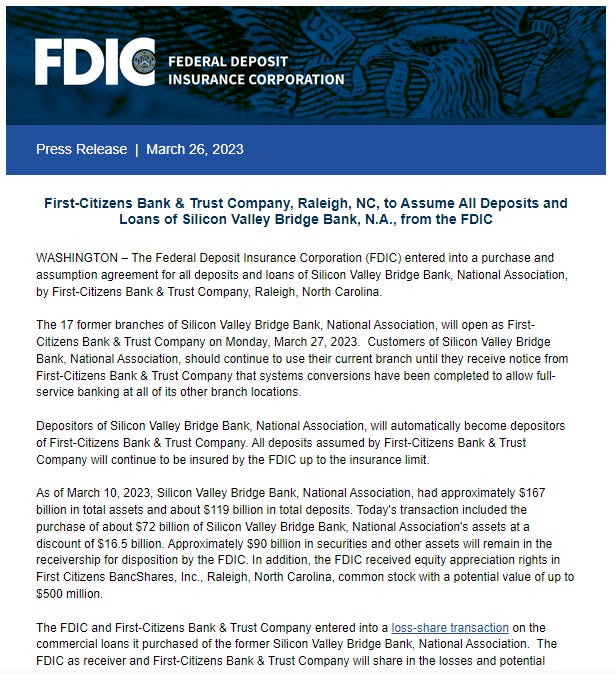

One day after a lengthy meeting on the growing bank crisis by the Financial Stability Oversight Council (chaired by Janet Yellen who five years ago vowed there would be "no financial crises in her lifetime") on the last day of a week which started with the collapse of Credit Suisse and culminated with US regional banks nursing historic losses amid speculation that First Republic Bank could keel over any moment and drag down countless other names with it, even though the FSOC assured Americans that "while some institutions have come under stress, the U.S. banking system remains sound and resilient", Bloomberg reports that in their attempt to rescue the most trouble of regionals, authorities are considering expanding the recently introduced emergency lending facility for banks - the BTFP - in order to give First Republic Bank more time to shore up its balance sheet.

Or they may not: after all this has been a crisis has been marked by at times puzzling second-guessing, miscommunication and lack of conviction on the part of regulators, whose actions not only precipitated the contagion from the collapse of Silicon Valley Bank when they blocked potential buyers from acquiring the bank and avoiding a complete wipeout of shareholders, but where Janet Yellen has actively sought to destabilize the regional banks by explicitly refuting what Fed chair Powell was stating, the most vivid example being last Wednesday's market crunch when stocks stabilized after the dovish FOMC only to puke after Yellen inexplicably said that US regulators were not even contemplating uniform deposit insurance.

And sure enough, the BBG report adds that "officials have yet to decide on what support they could provide First Republic, if any, and an expansion of the Federal Reserve’s offering is one of several options being weighed at this early stage." Meanwhile, regulators continue to grapple with two other failed lenders — Silicon Valley Bank and Signature Bank — that require more immediate attention... attention they wouldn't need if regulators had intervened more competently in the beginning and not waited until almost a trillion in deposits had been pulled from small banks as confidence cratered…

Look kids …

The good news IS … we’ve apparently moved on it’s becoming more like the boy who cried wolf and so …

We’ll begin with chief econ and head of the ivory tower and a guy thought of in running for a role at the Fed, Seth Carpenter,

Major central banks have hiked rates despite volatility in markets. They collectively said that inflation clearly means it is too soon to conclude that the hiking cycle is over. The banking sector developments haven't stopped the hiking, and indeed, I have noted that the idea of focusing on financial stability at the expense of inflation is a false dichotomy. Central banks are deliberately tightening financial conditions in order to slow their respective economies and thereby bring inflation down…while hopefully avoiding an unnecessarily painful recession. What the banks disruption does, however, is make it harder to calibrate the correct degree of tightening…

… So how does it end? If disruption in the banking sector delays an extension of policy tightening, then a soft landing is still possible. Our banking analysts see higher funding costs and rising deposit betas combined with tighter lending standards restricting loan growth. This view is consonant with Powell’s. But the downside risks have gotten bigger. A broader, more persistent contraction in credit would cause a recession given that growth will be near zero in the best version of the world. And central banks will be ruling out the upper tail of possible outcomes. The ECB is clearly focused on inflation, so growth can be sacrificed, and upside surprises like last week’s PMIs will add to its resolve. January’s strong data in the US initially led Powell to re-open the door to 50bp rate hikes. The other lesson from the past two weeks is that the “no landing” notion never made any sense. Central banks were always going to force a landing, one way or another; the banking sector may hold the key to which kind.

Ok then … as it ain’t over til it’s over, another shop (Goldilocks) leaning on the concept of a WORK IN PROGRESS,

… We continue to think that the Treasury has the capacity to provide a backstop for uninsured deposits if it becomes necessary. However, the last week demonstrated that the political hurdle to doing so is high. Sec. Yellen’s position on unilateral Treasury action was unambiguous. While we would not entirely rule out Treasury action if acute banking stress returns, the odds of a unilateral move from the Treasury appear very low.

This leaves Congress as the only plausible source of a broad explicit guarantee on uninsured deposits. However, the odds of congressional action on deposit insurance have risen slightly but remain fairly low. While a number of Democratic lawmakers have expressed support for increasing the limit on deposit insurance, many Republican lawmakers have expressed skepticism, and some are clearly opposed.

Incremental reforms to deposit insurance over the medium term—the next few months, not the next few weeks—are somewhat more likely but also face hurdles. Raising the deposit insurance limit for noninterest-bearing transaction accounts is the most likely to win bipartisan support, though unlimited deposit insurance even for this subset of accounts looks difficult, as there is likely to be disagreement over regulatory changes that would likely accompany any deposit insurance changes.

(Bloomberg) -- Bond investors are piling into wagers that a US recession is around the corner amid a growing dissonance between how markets and the Federal Reserve see the outlook for the economy.

And whether or not you like / agree with it, Murphy the chart guy says,

… The 10-year US Treasury Yield remains in an uptrend, but is trading a hair beneath the 50-week moving average. Momentum as measured by the relative strength index or the price momentum oscillator, remains in a bullish regime. Price is yet to confirm a true breakdown in benchmark yields. However, market rate expectations have changed drastically this month.

Finally, for our inner stock jockey, MSs Mike Wilson helping get the week started,

When Markets Question the "Higher Powers," They Can Re-price Quickly With bond markets questioning the Fed's dot plot, bond volatility has increased markedly. We think stocks are next as investors realize earnings guidance looks unrealistic. This is when the ERP typically reprices, and stocks may finally get ahead of the downside we see in earnings estimates.

Bond markets no longer appear to believe the Fed's guidance… over the past month, bond markets have aggressively strayed from the Fed's dot plot "guidance" regarding likely policy decisions. More specifically, while Fed Chair Powell was quite explicit the Fed is unlikely to cut rates this year, the bond market has priced in 100bps of cuts starting in June. In short, the bond market seems to be saying the US economy will fall into recession or the banking stresses are far from resolved and will require more explicit Fed action to deal with them. This divergence led to offsides positioning for many bond participants expecting more hikes just 30 days ago. To be clear, our economists still expect to avert a recession.

We think stocks are next… just as bond markets have become dependent on Fed guidance over the past decade, the equity markets have become dependent on company earnings guidance. Given the events of the past few weeks, we think guidance is looking more and more unrealistic, and equity markets are at greater risk of pricing in much lower estimates ahead of any hard data changes. This is typically how bear markets end—i.e., P/E multiples fall precipitously and unexpectedly, catching many investors off guard. The recent underperformance of small caps and low quality stocks suggests it could be imminent.

And from across the pond, another equity related kick in the pants to help get us outta the Monday morning starting blocks,

Flight to (Selective) Quality Flight to safety has benefited Tech thanks to lower yields and the sector's quality bias. We caution against chasing this trade however, considering elevated valuations and exigent inflation/rate risks. Quality exposure remains prudent and we highlight a basket of quality stocks at less demanding multiples.

… The speed and size of SIVB's collapse has raised concerns about deposit flight spreading to other regional banks. Judging from recent share price action, markets remain very nervous about regional bank business models, and while newly announced federal backstops should help to stem major bank runs, lending standards are likely to continue tightening across the banking industry nonetheless. To be clear, we do not envision this crisis of confidence to transform into one of solvency. The banking industry is far better capitalized than it was in 2008, with high asset quality and strong regulatory capital. However, credit availability was already suffering the effects of the Fed tightening cycle - one of the fastest on record - even prior to the recent turmoil, with banks tightening their lending standards sharply over the past 3 quarters (Figure 5).

Click HEREfor somewhat MORE of the global wall st NARRATIVE … THAT is all for now. Off to the day job…

If you look closely in the background there is a line of small local banks being lined up for consolidation, or, is it a line of foreign banks with branches in the US lining up at a deposit window? IDK, but, when betting on the winner(s) in a snake pit it makes sense to bet on the largest (harder to swallow) reptiles. As there are still ~4000 mostly small locals left in the US it should be quite the reptilian smorgasbord. What I wish I knew was how the pit-masters are going to tilt the odds. Towards the larger regionals with enough tidbits to placate the systemics? KBWB dip seems to be within range of a reasonable risk for 3 to 5 year timeframe assuming only total return.

'I love the smell of consolidation in the morning ... someday this is going to end'

https://www.youtube.com/watch?v=vRp7tYWnJJs

If you look closely in the background there is a line of small local banks being lined up for consolidation, or, is it a line of foreign banks with branches in the US lining up at a deposit window? IDK, but, when betting on the winner(s) in a snake pit it makes sense to bet on the largest (harder to swallow) reptiles. As there are still ~4000 mostly small locals left in the US it should be quite the reptilian smorgasbord. What I wish I knew was how the pit-masters are going to tilt the odds. Towards the larger regionals with enough tidbits to placate the systemics? KBWB dip seems to be within range of a reasonable risk for 3 to 5 year timeframe assuming only total return.