(USTs 'modestly' higher, belly BEST on SOLID volumes)while WE slept; households BUYIN', CEOs worried, rates hitting multi year HIGHS (here, there, everywhere...)

Good morning … rates UP, stocks down. Central banks take a pass (temporary or not — to be determined). Latest was overnight where the BOJ left rates UNCH as expected. Many hoping BOE is at peak rates … what could possibly go wrong? A VISUAL

Bloomberg’s 5 things to start your day (Europe — with a VISUAL i cannot recreate without a Terminal and which details one important factor driving lots of moves these days)

…Bond yields are headed higher around the world. The Federal Reserve took a hawkish stance Wednesday. The Bank of Japan hasn’t even gotten started in tightening.

Meanwhile, the Bank of England kept rates unchanged after a run of 14 increases. Sweden and Norway hiked, so did Turkey. South Africa’s central bank held its rate steady while signaling borrowing costs are likely to stay higher for longer. The Swiss National Bank unexpectedly paused. As for the European Central Bank, officials are sending mixed messages on whether they’re done tightening.

The BOJ held policy unchanged Friday, though traders are betting on tightening next year. Ending the world’s last negative policy rate will only add to upward pressure on yields worldwide.

This year’s return on the Bloomberg Global-Aggregate Index has turned negative in August and has only worsened since then. It looks like bond investors are about to suffer a third straight year of losses thanks to central bank rate hikes, something that last happened nearly a decade ago.

Not sure it’s all that different from any graph you might stumble on up here on the WWW (such as the one of 2yy US offered yest) but I suppose the point here is that whatever happened in March and whatever is still ahead, is NOT only going to be possible here but risk / potential issues are, well, everywhere.

AND so … here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher with the belly outperforming this morning with some modest out-performance in Gilts after their Composite PMI hit a 32-month low this month. DXY is higher (+0.25%) while front WTI futures are too (+1%). Asian stocks were mixed with Chinese stocks up smartly (China Ent +2.7%, CSI 300 +1.8%), EU and Uk share markets are mixed (FTSE 100 +0.5%, SX5E -0.2%) while ES futures are showing +0.18% here at a tardy 7:20am. Our overnight US rates flows saw an Asian session our desk characterized as one with clients there 'in a daze' after yesterday's massive bear-steepening here. We saw real$ selling in 10's in the AM hours and then real$ dip buying (front-end to intermediates) into the London crossover. Our London desk saw 2-way action in their morning time. Our overnight Treasury volume sheet shows it was very solid (~195% of ave overall) this morning with 7yrs (275% of ave) seeing the highest relative average turnover this morning.

… Our second attachment shows the updated daily chart of Treasury 10yrs. Two things stand out to us: 1) the prevailing bear channel that dates back to May 4th remains intact and in the driver's seat. That said, the channel top has been, and could continue to be, a local support level and that top comes in near 4.54% right now. That's as good a next-support level in 10's as any, we believe. 2) Look at daily momentum in the lower panel where the oscillator lines have begun to converge. This convergence is the indication that flows have become more balanced here at these deeply 'oversold' levels. The medium-term, weekly chart set-up looks much the same. For the uninitiated, what the momentum oscillators hint at is precisely what economists might look for in CPI. It's like looking under the hood hood of YoY CPI and seeing that sequential inflation measures (EG: 3m annualized and 6m annualized) are converging, a hint that inflation pressures may be stabilizing.

… and for some MORE of the news you can use » The Morning Hark - 22 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Apollo- US Households Are Big Buyers of Treasuries (we got THAT going for us, which is nice …)

Since the Fed started hiking rates last year, US households have bought $1.5 trillion in Treasuries, and over the past six months, US pension and insurance have also emerged as a buyer, see chart below. Over the same period, the Fed has been doing QT and been a net seller of Treasuries. The bottom line is that US households and real money are finding current levels of US yields attractive.

Apollo- CEOs More Worried (great find as I don’t have direct access myself — never did — to the biz roundtable data)

The Business Roundtable CEO survey is designed to provide a picture of the future direction of the US economy by asking CEOs to report their company’s expectations for sales and plans for capital spending and hiring over the next six months.

Since the Fed started raising rates in March 2022, CEOs have gradually worried more and more about the economy slowing, see chart below.

This is how monetary policy works. Higher cost of capital slows down business spending. The decline in the employment sub-index to 2020 levels is particularly noteworthy.

Barclays - August existing home sales show further weakness

Existing home sales declined 0.7% m/m in August, continuing the downward trend since February's peak. Single-family sales declined while multi-family sales rose, leading to no change in the monthly supply of homes. Mortgage lock continues to be a driving factor of weakness in sales.

Barclays - Bank of England Watching: View from the mountaintop

The MPC voted 5 to 4 to hold Bank Rate at 5.25%. We expect this is the peak of the rate cycle and that Bank Rate will remain on hold until mid-2024. QT was accelerated to £100bn.

BloombergBNP - US: Student loans sending consumers to detention in Q4

KEY MESSAGES We estimate the resumption of student loan payments could contribute to an acute GDP slowdown in Q4 – potentially even stall. These repayments could take out as much as $100 billion annualized from consumers’ pockets.

The impact could also be felt indirectly through higher delinquencies on other types of debt amid surging interest rates. During the pandemic, consumers with student loans added new borrowing.

Consumer sentiment, retail sales, and broader personal spending data going into the holiday season will likely bear the brunt of lower personal income available for consumption.

… The data from the daily Treasury Statement shows student-loan repayments totaled $6.4 billion in August (or roughly $70 billion annualized) – a sevenfold increase from around $10 billion annualized earlier this year. At the current rate based on the available September data, student loan payments would total $105 billion annualized (see Figure 2). October, the month when repayments become mandatory again, will provide more comprehensive information on the total impact.

… Back then, interest paid on personal loans kept rising for a year after the Fed delivered its last hike of the cycle, persisting until the first cut in September 2007. Figure 7 shows personal interest payments (excluding mortgages) as a share of after-tax personal income versus the Fed’s policy rate.

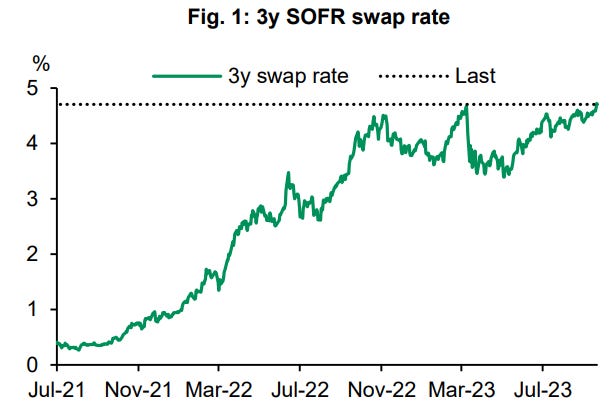

BNP - US Rates: Receive 3y swaps (seems like they WANNA get long BUT…what follows isn’t sounding like a ‘screamin buy’ at all…)

The reset in yields and the presence of identifiable catalysts support adding outright longs in US rates, in our view.

We view the tightening in financial conditions, coupled with the confluence of potential hurdles to US economic momentum into year-end, as factors that could support a rates rally.

We do not think data will support further Bank of England rate hikes, although the MPC today left the door open to them. Accordingly, we revise down our terminal rate forecast to the current Bank Rate of 5.25%.

We now expect one cut fewer in Q2 2024. We still expect Bank Rate to end 2024 at 4.00%.

That said, the BoE’s reaction function is highly variable and the UK’s data highly volatile, so we cannot rule out a further 25bp hike.

Rates: There was a small front-end reaction on the news. Looking ahead, we expect ongoing 2s10s gilt curve steepening. The pace of quantitative tightening rises to GBP100bn, broadly in line with our expectations, continuing to cheapen relevant sub-10y gilt swap spreads.

FX: The risks to the GBP continue to appear skewed to the downside, in our view, as we expect data to deteriorate, see scope for CTA position liquidation and as political risk could be increasingly priced in. We favour selling GBP on rallies, and via crosses.

S&P 500 is on track for largest weekly selloff since SVB. Techs show we are testing important support levels in S&P 500, S&P eminis and Nasdaq Composite.

Why it matters: A weekly close below, opens up another >3% move lower across the board to the 200-day MAs.

S&P 500:

Key support: 4328 - 4335 (June 26th and August 2023 low)

Opens a move towards: 4189 (200-day MA)

… Techs building blocks:

We have a 55-200 day MA set-up in play, which suggests a move towards 200-day MA

A rebound from mid August was resisted at the 76.4% retracement

A lack of key strong support levels below the August lows

Golidlocks - Philly Fed Manufacturing Index Below Expectations; Jobless Claims Fall

BOTTOM LINE: The Philadelphia Fed manufacturing index declined by more than expected. The composition was weak on net, as the new orders and shipments components declined, though the employment component edged up. Initial jobless claims fell to the lowest level since January, against consensus expectations for a slight increase.

Goldilocks - Global Markets Daily: Fed dots and front-end pricing (an important f’cast update, goal post moved from the narratives marketplace here)

The Fed, in its Summary of Economic Projections yesterday, signaled less easing in 2024, sparking a selloff in US rates led by the front-end. The changes were roughly in line with our empirical sensitivity estimates. Although investors “learn” from the Fed surprises on meeting days, there appears to be flow of information in the opposite direction as well (at a different horizon), and potentially common macroeconomic factors driving both.

Averages from the dot plot have served as an anchor for investors' modal views of front-end rates. So long as policy is viewed as restrictive, both investor expectations and market pricing are likely to remain below this modal outlook, with the latter unlikely to benefit from any significant upward repricing of front-end risk premium in the near term.

Following the meeting, our economists now expect only one 25bp cut next year (vs three previously), though levels from the dot plot and potential soft data in Q4 may keep current market pricing for about 75bp of easing in 2024 from fading materially in the near term.

BOTTOM LINE: Existing home sales declined by 0.7% to a seasonally adjusted annualized rate of 4.04 million units in the August report. The imbalance between housing supply and demand improved slightly but the median sales price nonetheless increased 1.5% month over month (sa by GS), surpassing the prior peak of May 2022. We left our Q3 GDP tracking estimate unchanged at +3.2% (qoq ar).

Goldilocks - BOJ MPM: Maintains Status Quo as Expected

… The BOJ also made no changes to its assessment of the economy and prices, which were revised upward in the previous Outlook Report. Specifically, its statement maintained the view that "Japan's economy has recovered moderately." In terms of individual items, it again stated that "consumption has increased steadily at a moderate pace," and that business fixed investment has also "increased moderately." On the inflation front, it adjusted its assessment of core CPI inflation, which has started to slow recently, to “has been at around 3 percent recently,” from “has been in the range of 3.0-3.5 percent.” Its view on inflation expectations was unchanged, as “have shown some upward movements again.” The BOJ also made no revisions to its view on risk factors, reiterating that "it is necessary to pay due attention to developments in financial and foreign exchange markets and their impact on Japan's economic activity and prices."..

Goldilocks - BoE Keeps Policy Rate Unchanged; Increases Gilt Stock Reduction Target to £100bn (yest was ALL FOMC and today … well …)

BOTTOM LINE: The MPC voted by a majority of 5-4 to keep Bank Rate unchanged at 5.25% in today's meeting, highlighting the recent loosening of the labour market and the downside surprise in services inflation yesterday. On the path ahead, the guidance was left largely unchanged, with the MPC retaining its data-dependent approach and noting that monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably over the medium term. On QT, the MPC voted in favour of increasing its gilt stock reduction target to £100bn for the upcoming 12-month period (from £80bn over the previous 12 months)

ING - US housing feels the squeeze from high mortgage rates (wait, what, actions have consequence? who’d a thunk it)

A tripling of US mortgage rates constrained both the demand and supply of housing, leaving existing home sales at post-GFC lows. Mortgage rates will rise further in the wake of the market's reaction to yesterday's Fed forecasts, further constraining activity

UBS - The art of doing nothing (wait, thats MY job)

Several central banks have been demonstrating masterful inactivity recently. The world leader at masterful inactivity is the Bank of Japan, which did nothing overnight. The Bank of England and the Swiss National Bank both left policy rates unchanged yesterday. Differences in inflation mean inactivity by the Bank of Japan continues a loose policy stance, but real borrowing costs rise with inactivity by the Bank of England and the Swiss National Bank…

… There is a rush of business sentiment polls today. These increasingly exaggerate economic realities—media sensationalism and a tendency to answer surveys with perceptions may be to blame. Worryingly, some market participants view the world as a rigid and unchanging place and do not adjust for the changing reliability of sentiment surveys when modelling markets.

Several central bank speakers make their way onto the world stage. Those central banks that have trashed forward guidance will be at a disadvantage in issuing hawkish rhetoric if data starts to move against them.

Wells Fargo - LEI: Leading to Recession or Leading Us Up the Garden Path?

The 0.4% decline in the Leading Economic Index (LEI) in August marks the 17th consecutive monthly decline. Six of the components barely budged, exerting a contribution smaller than 0.05 percentage points in either direction. A bounce in building permits was the only real positive.

The Alarm May Have Gone Off Too Early, but It's Not a False Warning…

Wells Fargo - Government Shutdown: Deadline Déjà Vu (deja vu all over again … if only Yogi were president)

Summary

Federal fiscal year (FY) 2024 begins on October 1, and as of this writing none of the 12 annual appropriation bills have been enacted into law. As a result, in the absence of Congressional action, a government shutdown will begin on October 1.

During a government shutdown, unfunded federal agencies must discontinue non-essential functions. Essential services, such as those related to public safety or national security, continue to operate.

A government shutdown only impacts the 25% or so of federal spending that is characterized as discretionary. Mandatory spending, such as outlays for Social Security, Medicare and Medicaid, is not part of the annual appropriations process and thus generally continues unabated.

Earlier this year, bipartisan majorities in Congress passed the Fiscal Responsibility Act (FRA), which suspended the debt ceiling and set "topline" spending levels for defense and nondefense discretionary spending. The FRA stipulated roughly a 3% boost to defense discretionary spending and an 8% cut to nondefense discretionary spending for FY 2024, though our sense was that the latter number would be closer to flat after accounting for a number of adjustments and side agreements.

However, some more-conservative House Republicans are unhappy that the trajectory for discretionary spending was not reduced even more. Given that the Republican majority in the House of Representatives is a razor-thin four seats, Speaker of the House Kevin McCarthy has faced pressure to reduce discretionary spending below the levels agreed to in the FRA. This hurdle, alongside several others, have led to gridlock in the budget process.

There does not appear to be enough time to complete the annual appropriations process by October 1. As a result, a continuing resolution or a shutdown are the two most likely near-term outcomes. At this point, we view the chances of a shutdown starting on October 1 as more or less a coin flip.

Past government shutdowns are instructive for assessing the potential economic impact. The direct hit to economic growth in the 2013 and 2018-2019 government shutdowns was a relatively modest few tenths of a percentage point. Growth rebounded by a similar amount once the shutdown ended. That said, not all the lost economic activity was recovered in full, and the indirect hit to the economy is more difficult to measure yet should not be ignored.

A shutdown could delay influential economic data reports published by government agencies. Following the 16-day government shutdown in 2013, the Department of Labor's monthly Employment Situation and Consumer Price Index reports, among others, were delayed by about two weeks. Collection, processing and publication delays stretched into the following month as well.

Determining the correct monetary policy setting in real-time is never easy, and it would be made all the more difficult by a lack of timely economic data. A government shutdown that leads to economic data blind-spots could raise the risk of a policy misstep by the Federal Reserve.

Wells Fargo - Existing Home Sales Slide Once More in August. Climb in Mortgage Rates Continues to Weigh on Activity and Constrain Listings (shocking as it may be, nothing — higher mortgage rates = lower affordability — happens without some sorta consequence)

Summary Worsening Affordability Fuels the Long Slide in Resales, With Little Relief on the Horizon Existing home sales inched down 0.7% in August as resales continue to be constrained by low inventory and rising borrowing costs. The 4.04 million-unit sales pace is the slowest since January and the second slowest pace since October 2010, when the housing market was recovering still in recovery from the housing market crash. August's turnout continues the long slide in existing home sales, which have fallen 17 of the past 19 months, and are now down 15.3% over the year. Elevated mortgage rates continue to be a prohibitive force and thus will weigh on demand for the foreseeable future. The outlook for a persistently high financing cost environment was affirmed by the FOMC's September meeting yesterday in which it communicated a higher for longer interest rate outlook with minimal cuts projected for 2024…

Wells Fargo - Bank of England Pauses Monetary Tightening

Summary

In what was a finely balanced decision, Bank of England (BoE) policymakers held their policy rate steady at 5.25% at today's monetary policy announcement. In a significant change, the BoE said there were mixed developments on indicators of inflation's persistence, noting slower varied signals on wage growth and slower services inflation.

We believe today's interest rate pause could also represent an interest rate peak. The BoE said it views the current level of interest rates as restrictive, and that monetary policy would need to be sufficiently restrictive for sufficiently long to return inflation towards target.

We do not anticipate an initial 25 bps rate cut until the May 2024 meeting, and see the BoE's policy rate ending next year at 3.25%. Today's decision also represents a loss of interest rate support for the pound. In that context, we view the risks as tilted towards further U.K. currency weakness through early 2024, and cannot rule out a move toward $1.2000 or below.

Yardeni - Good News Is Bad News, For Now (oh no, not this … this is what we’ve all been reduced to …?)

The Fed's hawkish pause has unsettled the bond and stock markets. During 2022 and early 2023, the widespread fear was that the Fed's tightening of monetary policy would send the economy into a recession, depressing corporate earnings and the stock market. Now the fear is that stronger-than-expected economic growth will force the Fed to maintain its restrictive stance for some time. So good news is bad news. Today's selloff in bond and stock prices was partly attributable to this morning's good news, i.e., the drop in initial unemployment claims (chart).

Yardeni - Bond Yield Climbs to 4.50% As Yield Curve Is Disinverting.

The Fed's hawkish pause, announced on Wednesday afternoon, has lifted the 10-year US Treasury yield to 4.50% this evening. We think it might consolidate here for a while consistent with our view that the yield has normalized back to where it was from 2003-2007, i.e., before the Great Financial Crisis (GFC). Back then, the 10-year TIPS yield and the expected inflation spread hovered around 2.00% and 2.50%, respectively (charts). Currently, the TIPS yield is 2.11% and the expected inflation spread is 2.38%.

The yield might rise to 5.00% if the TIPS yield climbs to 2.50%, while the inflation spread rises to 2.50%. That would also be consistent with the pre-GFC old normal. (BTW: It's interesting to observe that the expected inflation spread is very highly correlated with the price of copper, which remains under $4.00 per pound despite recent attempts by the Chinese government to stimulate growth.)

The S&P 500 is down 5.6% from its July 31 bull market peak. That's mostly because the bond yield has been climbing above 4.00% since then. The forward P/E is inversely correlated with the 10-year TIPS yield, suggesting that there is still more downside for the S&P 500 (chart)…

And from Global Wall St inbox TO a couple / few things I might have been pointing out TO my friends / clients who were all together part OF the club of Global Wall St and things which we all might very well be passin’ round

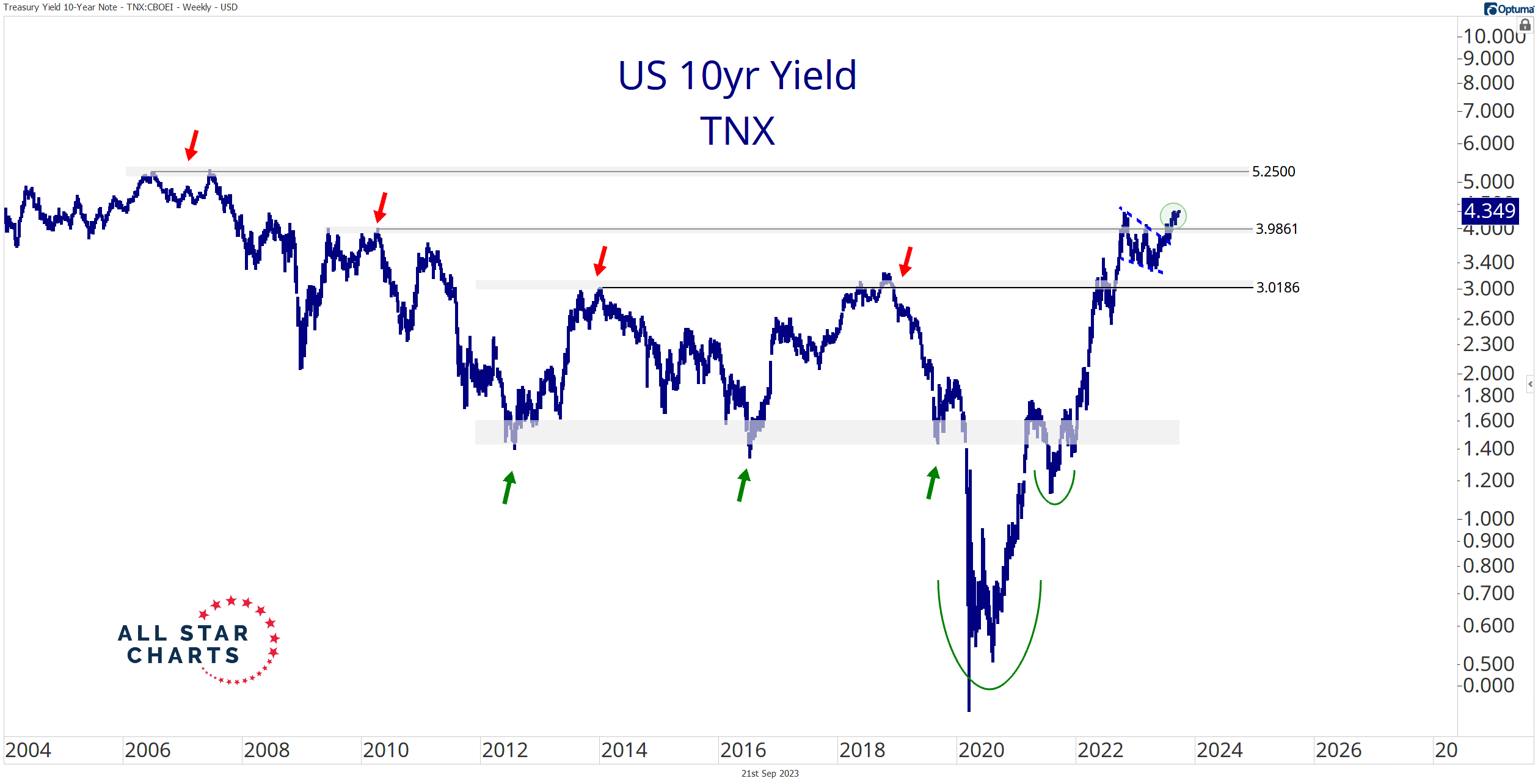

AllStarCHARTS- US Benchmark Rate Hits 16-year High (somehow I get sense this will end with reasoning to SELL bonds and buy stocks…)

Bonds across the curve are skidding to fresh contract lows as interest rates have a one-track mind…

Higher!

Check out

the US

10-year yield posting fresh sixteen-year highs:

Not to be outdone, the 2-year yield just registered its highest level in seventeen years.

Interest rates across the curve are breaking to decade-plus highs in what has become a foot race.

It’s clear that the rising rate environment remains alive and well. An inverted yield curve keeps score, reminding us that shorter-duration yields are winning.

But I honestly don’t care what area of the curve is leading.

I simply want to catch and ride trending markets rather than fight a sideways mess.

Bonds, currencies, and commodities all provide excellent trading opportunities and will continue to do so as long as rates rise. Luckily, I focus on those market areas every day.

Spencer and I will be joined by Tracy Shuchart @Chigirl, Chief Market Strategist at Hilltower Resources Advisors, on tomorrow’s episode of “What the FICC?.”Be sure to tune in as we dive into commodities and energy.

If these markets aren’t in your wheelhouse, have no fear.

There are plenty of stocks enjoying a solid bid. I hate to beat a dead horse, but energy is your best bet during a rising-rate environment. Or at least in today’s environment.

More importantly for US stock indexes, it’s not if but how the 10-year arrives at those former highs that will impact the averages most. (A slow and steady yield increase is the best scenario for the broader equity market.)

Meanwhile, avoid the mess at the index level and trade what’s trending.

That means shorting bonds and global currencies against the US dollar while buying energy…

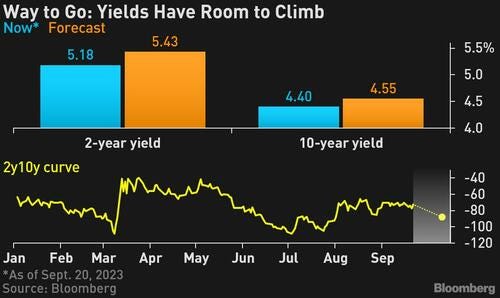

By Ven Ram, Bloomberg Markets Live reporter and cross-asset strategist

The resounding selloff in front-end Treasuries we have seen in this cycle isn’t done yet, with yields likely to reach the highest in more than two decades should the Federal Reserve follow the path of its latest dot plot.

Treasury two-year yields will reach 5.43%, a level not seen since December 2000, if the Fed were to raise rates once more in this cycle and the US labor market continues to stay resilient through the spring of 2024.

The Fed’s stance — together with rising real rates — also spells bearishness for 10-year bonds, with that yield likely to hit 4.55%. That implies a deeper curve inversion, with the differential between the two maturities set to reach -88 basis points from -75 basis points now.

The outlook marks an update to my previous view, where I had suggested the two-year yield might reach 5.22%.

The bearish revision stems from the Fed’s dot plot for September, which was pretty hawkish. The central bank — which had penciled in rate cuts of 100 basis points through 2024 when it met in June — took 50 basis points off the table, concurrent with a lower unemployment rate and faster inflation.

“Don’t fight the Fed” may be one of the oldest commandments in the financial markets, but traders have continually ignored what the central bank has been saying through much of this cycle, on conviction that a recession will force policy makers to pivot.

Almost a year ago, traders were similarly skeptical of the dot plot and reckoned that the Fed, whose benchmark rate then was 3.25%, would stop at 4.50%. And yet we are at 5.50% and counting.

Investors have been positioned for a recession since the middle of 2022 as the yield curve inverted. But so far, positioning for rate cuts has failed to pay off. As happened before the dotcom bubble and the financial crisis, the yield-curve inversion may continue for long before we actually see an economic contraction.

Meanwhile, real rates have also been surging, with the 10-year yield having shot up above 2% — a far cry from levels of zero that prevailed at the start of the pandemic. That may be due to a structural shift in the markets, and so long as that trend continues, 10-year nominal yields will stay aloft.

What could go wrong with the outlook for Treasuries? The resilience in the labor market may snap abruptly, which would cause the markets to pivot and the Fed to abandon its dot plot.

Two-year Treasuries have had an eminently forgettable 2023 so far, and indications suggest that there is no turnaround in sight

Authored by Simon White, Bloomberg macro strategist,

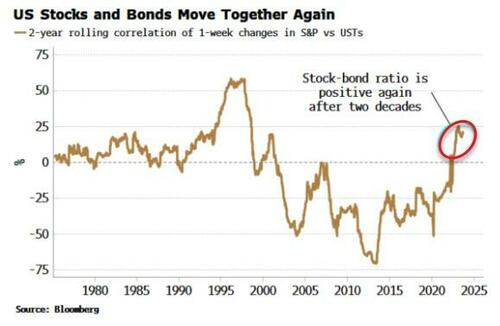

Banks are exposed to bond prices falling at an increasing rate as a rising and positive US stock-bond correlation drives a widening in the bond risk premium.

After two decades of being negative, the stock-bond correlation - one of most important relationships in finance - has turned positive again. Bond prices, under renewed pressure after the hawkish lean in Wednesday’s FOMC, are biased structurally lower as the risk premium for bonds rises, leaving leveraged and mark-to-market holders of USTs – such as banks and hedge funds – exposed to potentially significant capital losses.

Of all the cognitive biases, recency bias is one of the most pernicious and prevalent. Nowhere in markets is this more pertinent than the relationship between stocks and bonds. For most of the last century they have moved together, i.e. their correlation has been positive.

But for the past 20 years the correlation was negative. Bonds acting as a natural hedge for stocks had profound implications for investment, fueling strategies such as risk parity.

That correlation has now flipped back to positive. But recency bias means most have yet to fully digest what this means.

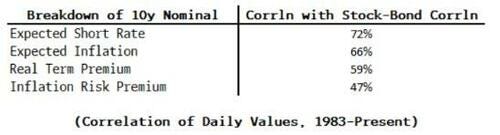

Why have stocks and bonds started to move together again? As with anything in markets that’s not doing what it used to, the culprit is inflation. To see this, we decompose nominal yields into the expected real short-term rate, the real bond risk premium (aka term premium), expected inflation and the inflation risk premium (the DKW model, explained in this Fed paper).

In simple terms, there is a positive relationship between nominal yields and the stock-bond correlation - higher yields coincide with a higher stock-bond correlation - but the decomposition tells us that all of the underlying inputs are statistically significant positive drivers of the ratio (with high t-stats and relatively high correlations).

The highest correlations come from the expected short rate and expected inflation, but as the Fed is expected to raise rates in response to higher inflation, these two are themselves positively related.

Thus the primary underlying driver of the stock-bond ratio is inflation expectations. This is what we saw in the mid 1960s to the late 1990s period of elevated inflation and a positive stock-bond correlation, i.e. inflation expectations were driving stocks and bonds together.

We are now back in that world, where rising inflation expectations are causing stocks and bonds to co-move. This has two pivotal implications:

Bonds are no longer a portfolio hedge

Bonds are not a recession hedge

When stocks have a negative correlation with bonds, they are highly sought after as not only do they make money when bonds lose money, they also smooth returns. In a recent paper by Robeco’s Roderick Molenaar et al, they show that when stocks and bonds are negatively correlated, 100% of the variance of a multi-asset portfolio comes from the equity contribution.

The risk-parity strategy of volatility-weighting portfolios of stocks and bonds has been a beneficiary of the negative stock-bond correlation.

It’s perhaps little surprise that Ray Dalio, co-CIO of Bridgewater Associates, the pioneer of risk parity, recently said he would prefer to be in cash than bonds.

Bonds’ portfolio “super power” has driven their risk premium to all-time lows in recent years. But as they lose this enviable capability, the risk premium – still negative on market-implied measures – is highly likely to keep rising, perhaps significantly so, taking bond prices much lower.

Compounding the problem is that bonds are losing their efficacy in acting as a recession hedge. In the prior low-and-stable inflation regime, the Phillips curve (if you believe in those sort of things) was linear and stable, meaning that as unemployment rose, inflation typically fell.

That becomes self-fulfilling, as when stocks fall in response to a growth shock, bonds should rise as inflation eases. Even if you’re not a fan of academic models like the Phillips curve, that’s empirically what we saw in 21st century recessions.

But once more, elevated and more volatile inflation has upended everything. Higher inflation past a certain threshold typically leads to a non-linear and unstable Phillips curve, consistent with what we are observing today. Now, inflation and unemployment are not assumed to move as inversely, or with the same regularity. A growth shock may come with rising inflation, bad for bonds as well as equities.

The expectation that higher inflation has corrupted the Phillips curve adds additional upward pressure to stock-bond’s correlation, taking it positive and ensuring bonds will not act as a recession hedge when the next downturn hits.

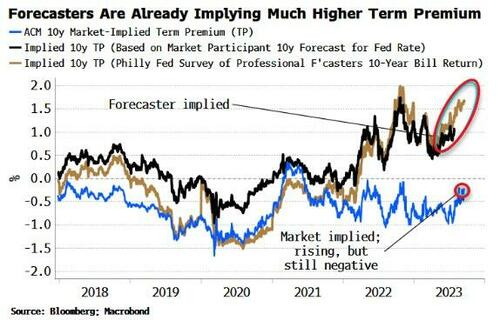

Bonds thus suffer a double whammy to their appeal and so cannot command the same yield discount. Yet even though market-implied estimates of term premium such as the ADM model have risen, they are still negative. Further, they are much lower than survey-based estimates, which are now significantly positive and began to accelerate higher in 2022.

Term premium is prone to moving much higher, and thus bond prices much lower, to fully express the risks from a positive stock-bond correlation that is perhaps already being picked up in forecasters’ surveys.

With positioning in USTs long, this poses risks to bond holders, to yields and to the wider market.

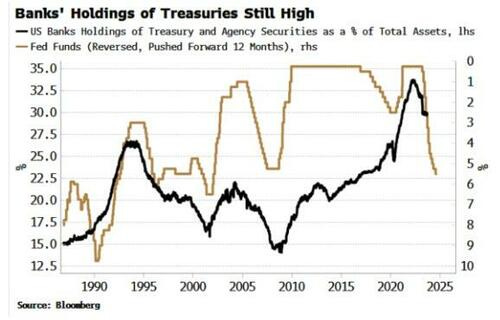

The JPM client survey of Treasury long positioning is in the top part of its range, while asset managers are very long, based on COT data. But it is hedge funds and banks that could pose the biggest risks.

US banks’ holdings of USTs have fallen from their peak, but remain historically elevated at over 30% of assets. They generally reduce their holdings when rates rise, but this time they may not have moved fast enough.

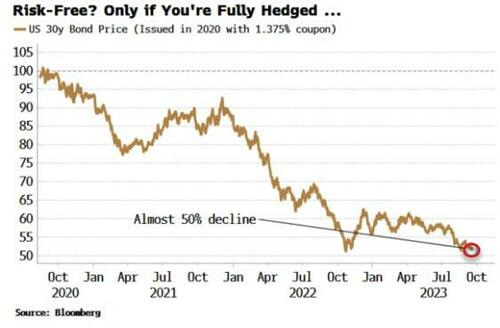

Hedging will help, but that can’t always be taken for granted. Anyway, with e.g. 30y USTs issued three years ago down almost 50% in value, hedges may not be sufficiently sized to cope with such big moves in what is supposedly a risk-free asset.

If recency bias is wrong in informing us about how stocks and bonds now behave, it may end up being salutary in reminding us that banks, such as SVB, can fail when bond prices fall sharply.

Bloomberg’s Five Things You Need to Know to Start Your Day (ASIA — with reminder of how NAZ linked to 10yy)

… Tech is set for its worst month this year as traders yet again come to terms with the Fed staying higher for longer, which includes elevated bond yields.

Tech companies Amazon.com, Nvidia, Alphabet and Tesla were among the biggest S&P 500 decliners Thursday in terms of market cap as the prospect of still-higher yields sinks in. The S&P 500 info tech index is by far the worst-performing sector for September. Both it and the Nasdaq 100 are posting the biggest monthly losses since December.

Chip bellwethers such as Intel, Nvidia and AMD have had a tough week. It hasn’t helped that chip designer Arm fell below its IPO price after just a week, with analysts cautious about its valuation and benefits from the AI boom. This suggests that perhaps the AI frenzy industry-wide has faded and that tech valuations remain elevated given the yield backdrop.

WolfST - Treasury Market Gets Memo with Subject Line: “Higher for Longer” but Someone Scribbled next to it, “Maybe Forever?”

… The 40-year bond bull market ended in August 2020, when the 10-year yield kissed 0.5%. With hindsight, we can say that predictions at the time of the 10-yield yield dropping below 0%, as it had done in Europe, were rather silly. But on that day, we were biting our nails, because crazy things were happening all over the place, with central banks were printing trillions of dollars and throwing them at the markets.

At any rate, that zoo is over now, thank-goodness. The 10-year yield has jumped by 400 basis points since then. The world is normalizing – maybe even the “neutral rate.” And that’s a good thing.

Turns out, historically, the 10-year yield is still relatively low. We’re just not used to it anymore:

Bond bloodbath at the long end…

AND with all THAT in mind, one final look at what may way heavily on the Feds decisions as well as all of US

Excellent work !!!!!

Yogi Berra: When you come to a Fork in the Road.....Take it.......

That was highly educational :)!