Good morning … what did I miss? Besides the BoE just now — I’ll leave this alone until tomorrow and for now, I think I’ll study all the FOMC recaps / victory laps below “CAREFULLY” (in a way that deliberatelyavoids harm or errors; cautiously.)

Chair Powell in his press conference,

“We’re in a position to proceed carefully in determining the extent of additional policy firming that may be appropriate,”

… he said in the prepared remarks to set the tone. And,

“Given how far we have come, we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks.”

Meanwhile, stocks were lower and bond yields are, well, higher, pricing in the what next … here are 2yy for some context

LOG scale back as far as Investing.com will allow and you can see just how close we ARE to 5.50% … surely something will break and something MORE than what broke in March of this year?

If / WHEN it does, we’ll be right back at the narratives marketplace researching and buying (back) into rates CUTS and bullish UN-FLATTENING trades, right?

… Here is my defiantly low-tech graphic of where the FOMC’s projections for the fed funds rate have moved over the last 12 months. It’s amazing what you can do by screen-shotting the press release and then scribbling on it with the Paint program. The predictions for next yearonward are shown; September 2022’s dots are on the left, the latest are on the right. The direction of travel is clear, and dramatic:

(To be clear, none of my colleagues in the graphics or data visualization departments bear any responsibility for this chart. I will take the blame.)

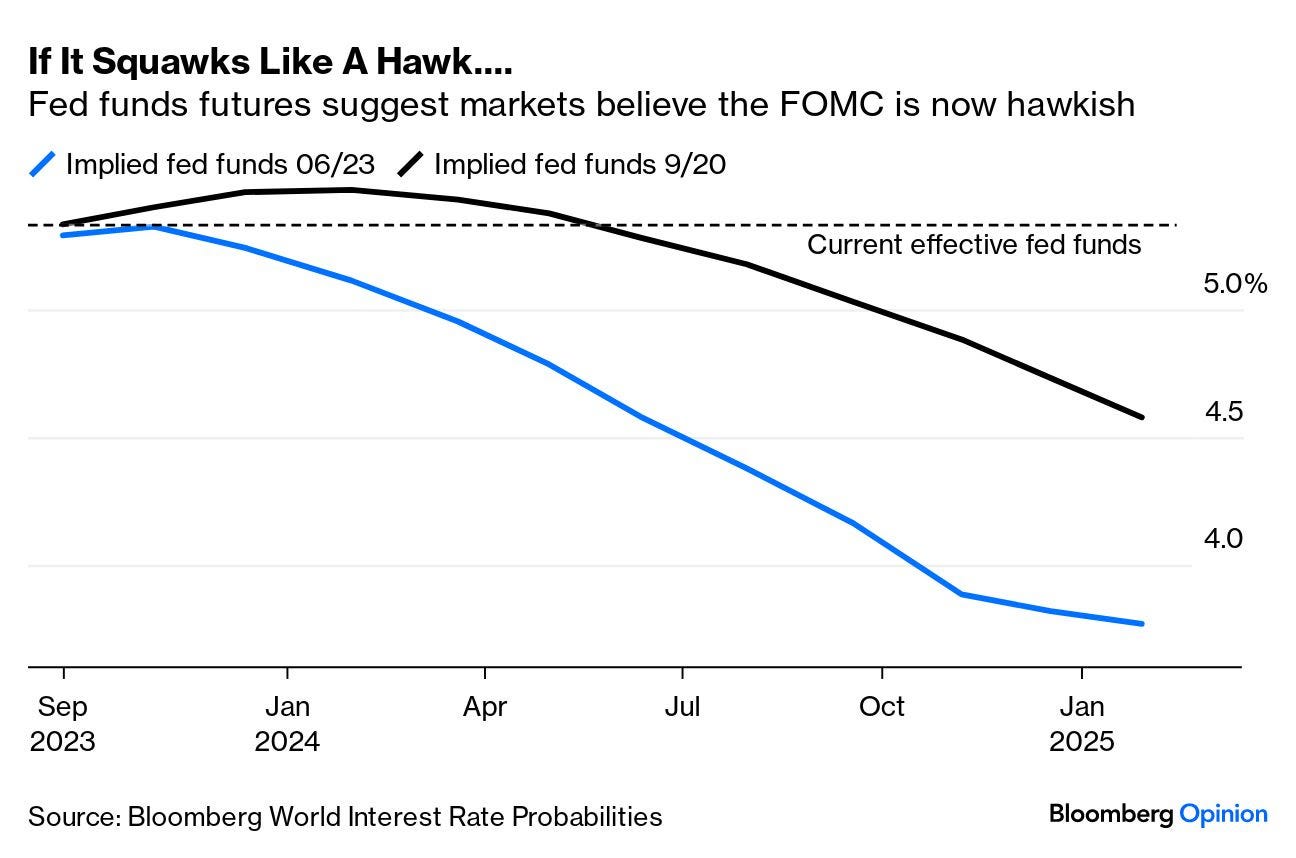

Judging by fed funds futures, the possibility of another hike this year still gets short shrift. The betting in the market is that rates will be significantly lower by the end of next year than the FOMC members appear to believe. Ahead of the announcement, Bloomberg’s World Interest Rate Probabilities function was predicting a 4.57% rate at the end of 2024, which subsequently rose to 4.76%. The shift in the course for the fed funds rate implicitly predicted by futures over just the last three months has been dramatic:

However, even after that steep move, the market is still collectively dubious that the Fed will really keep rates high for as long as they’re saying. A 4.76% rate next December puts the market in line with the most dovish of FOMC members; the median estimate for the wider group is now 5.1%. That’s illustrated in another low-tech graphic:

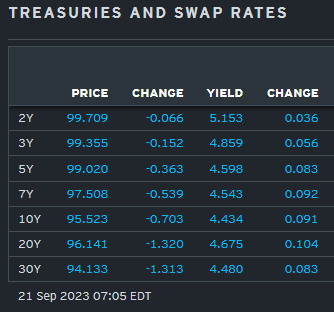

AND from yesterday’s DOTS TO … a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting sharply steeper (2s30s +6bp) as long-end rates took out their well-established range highs overnight. DXY is higher (+0.16%) while front WTI futures are lower (-0.9%). Asian stocks were down almost across the board (Nikkei -1.37%, SHCOMP -0.77%), EU and UK share markets are sharply lower (SX5E -1.4%, IBEX -1.7% but FTSE 100 near flat after BOE hold) and ES futures are showing -0.6% here at 7am. Our overnight US rates flows saw a continued leak lower in Treasury prices during Asian hours though our desk saw net better buying into the dip (real$ mostly in intermediates). Volumes were high then but afternoon activity in cash markets was limited. In London hours the desk also saw prices sag again with flows weighted toward better selling out the curve (10's struggled on 'fly). There was also a strong whiff of heavy paying in the belly this morning, they noted. Overnight Treasury volume was very solid at ~225% of average overall with 5yrs (278%) seeing the highest relative average turnover among benchmarks, matching our flows.

… Well, if there is any good news from the bond market over the past hours it is that no benchmark has a flat top anymore. That's because the long-end joined the bearish breakout party overnight (See 30yr Tsy yields, chart 1).

The other kinda decent (not yet good) news is that market sentiment has shifted dramatically in recent months where, for example, market pricing for rate cuts has slashed about 80bp in expected 2024 cuts since July- as implied by the SFRZ3Z4 curve (chart 2).

… and for some MORE of the news you can use » The Morning Hark - 21 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up, some post FOMC thoughts …

Barclays - Federal Reserve Commentary: September FOMC: Long way to go (miles to go before they rest? so, rate cuts in 2024, though, right?)

The FOMC kept the policy rate unchanged but maintained a tightening bias, continued to project another hike before yearend, and revised up the 2024 dot, as we had expected. The median SEP dots were revised up 50bp in 2024 and 2025 reflecting a significantly more optimistic economic outlook.

The Fed left policy rates unchanged -- as expected. The biggest surprise was the narrowing between the '23 and '24 dots to 50 bp vs. the expectation for 75 bp in cuts forecasted next year. As a way to deliver the hawkish hold, the more aggressive dots should continue to push cut pricing further into 2024. Only one dot made the difference between 50 bp and 75 bp in cuts in 2024. This makes it much closer to the consensus; which is what has tempered the market's response and left 10-year yields lower on the session. There was no change to the longer run dot at 2.5%.

The FOMC statement was effectively unchanged with the exception of the characterization of employment. In the last statement, "Job gains have been robust in recent months" -- this was updated to "Job gains have slowed in recent months but remain strong". In addition, economic activity was upgraded to "solid" from "moderate" -- a shift that was reflected in the SEP where the 2023 GDP estimate was increased to 2.1% vs. 1.0% prior. 2024 GDP gained 0.4 pp to 1.5% and 2025 was 1.8% -- as was the longer run forecast. Not surprisingly, the 2026 growth estimate matches the longer run at 1.8%. The Fed is doubling down on the soft-landing assumption via the 2023 unemployment rate forecast of 3.8% -- i.e. assuming there will be no further increase in the unemployment rate from August's level (that seems remarkably optimistic).

BloombergBNP - September FOMC: Fed leans in to higher for longer amid the softest of landings (but whatever will become of the soft landing narratives, then? back TO the marketplace?)

KEY MESSAGES

Though the FOMC passed on a rate hike, the overall messaging – most notably the dot-plot – was hawkish, in our view.

The median FOMC participant still expects one more 25bp hike this year and just 50bp of cuts next year, but these projections are predicated on growth, employment, and inflation forecasts that we think will prove too strong.

Our base case remains that the Fed already reached terminal fed funds of 5.50% in July. We think a weaker growth profile in H2 as well as faster deceleration of inflation pressures relative to the Fed will give policy-makers, who are clearly striving for a soft landing, the incentive to refrain from hiking rates further.

… Interest rates strategy: The removal of two rate cuts in the 2024 median dot drove a hawkish initial rates market response to today’s Fed statement, with the yield curve pivot flattening amid higher front-end real yields and tighter breakevens. While a surprise versus market pricing (which implied ~3.5 cuts next year), we think the context of the economic projections that underpinned those revisions is ultimately key to the market takeaways, with the FOMC now projecting a materially better growth profile and a contained rise in the unemployment rate.

For the rates market specifically, this solidifies the notion that “soft landing” baselines should be viewed as comparatively weak drivers of (bullish) curve steepening; the FOMC has signaled that it will be cautious in cutting rates if the labor market proves resilient, even if inflation is making progress towards target. The case for front-end longs is, therefore, heavily geared towards the type of clearer cyclical deterioration that would give the Fed comfort in cutting rates sooner and/or more quickly than their projections imply. We continue to think our economic baseline over the coming quarters will justify such an outturn, with a loss of momentum into year-end followed by a period of mildly negative growth supportive of lower yields, particularly at shorter maturities. Near term, the combination of the UAW strike, resumption of student loan repayments, and the risk of a government shutdown are potential stumbling blocks that could derail the prevailing perception of robust US economic momentum, supporting the first phase of a move in this direction.

DB - Fed Notes - September FOMC recap: Embracing the soft landing story... "carefully"

The broad contours of the September FOMC meeting were in line with expectations: The Committee held rates steady, continued to indicate that another rate hike is likely this year, and signaled that rates may need to be even higher-for-longer in order to achieve their objectives over the forecast horizon. That said, the details were more hawkish. The SEP moved significantly further towards a soft landing view as evidenced by the 40bp cuts to the 2024 and 2025 unemployment rate projections (to 4.1%). This upgrade, in turn, motivated a 50bp increase to the 2024 and 2025 median fed funds forecasts.

Despite the median dot showing another hike this year, the Chair's presser expressed limited conviction in that view. Instead, Powell emphasized the ability to "proceed carefully" and a Committee that are meaningfully split on whether they have already achieved a "sufficiently restrictive" stance. Moreover, the projections set a relatively low bar for skipping that final hike, as the year-end forecasts for unemployment and inflation are likely too low and high, respectively. As such, we continue to expect no further rate increases.

Further out, Powell emphasized significant uncertainty about the timing and extent of rate cuts in 2024. Although the median long-run dot did not rise, there was continued updrift in participants' views of long-run neutral. Supporting this migration, Powell was more willing to entertain the idea that short-run r-star has risen.

FirstTrust - You Know It When You See It (and this wasn’t IT)

While the Fed kept rates unchanged at today’s meeting, between the press conference and forecast updates, Powell and Co. gave plenty of ammo to keep the financial press busy speculating about what may come at the next FOMC meeting this Fall.

Today’s Fed statement itself was a non-event, with minor wording changes noting that the economy is growing at a “solid” rather than “moderate” rate, and employment gains have “slowed” but “remain strong”. It’s in the updated economic projections (the “dot plots”) – which give a peek at how the Fed expects the economic and rate landscape to evolve moving forward – that things got interesting…

… For now, each FOMC meeting should be considered “active,” meaning the Fed is ready to raise rates further if the data suggests more work to be done. But without a clear path forward the looming government shutdown, resumption of student loan payments, slowing employment growth, and higher oil prices could cloud the Fed’s vision as 2023 comes to a close. Where’s the finish line? Nobody knows for sure, but we aren’t there yet.

Goldilocks - September FOMC Recap: A Higher Bar and a Later Start for Rate Cuts

The FOMC’s interest rate projections were somewhat more hawkish than expected today, with a solid 12-7 majority showing another hike in 2023 and the median penciling in 50bp of rate cuts in 2024, down from 100bp of cuts in June. We did not take this as a strong signal about a hike in November, in part because these projections came alongside an inflation forecast that still looks too high. We continue to expect that better inflation news, progress on labor market rebalancing, and a likely Q4 growth pothole will convince the FOMC not to hike again this year.

We do, however, think that today’s meeting raises the bar for rate cuts next year, and we have pushed the first cut in our forecast back from 2024Q2 to 2024Q4. We have long had mixed feelings about the likelihood of cuts because we are skeptical of some of the arguments that FOMC participants have made for them. Today, participants appeared to move away from the view that monetary policy tightening could weigh on growth with a long lag next year, which weakens one argument for cutting. We think this means that inflation will have to fall further than we previously assumed for the FOMC to cut.

The median longer run rate dot remained unchanged at 2.5% today, against our expectation that it would rise to 2.75%, but FOMC participants do appear increasingly open to rethinking neutral. The average longer run dot moved up again to 2.76%, and Chair Powell volunteered that neutral might have risen and that the short-run neutral rate could be higher than the longer run rate shown in the dot plot, as a recent New York Fed blog post concluded. A further shift toward that view could further weaken the case for rate cuts next year.

ING - Fed holds US rates steady, but markets are reluctant to buy into the more hawkish messaging

The Fed has left the Fed funds target range at 5.25-5.5% and continues to indicate the prospect of another 25bp hike this year. Longer term, the Fed is signalling less prospects of rate cuts and a diminishing chance of a recession as it guides inflation back to 2%. Given the challenges the economy faces, the market is understandably sceptical

JEFF - FOMC Leaves Rates Unchanged, Powell Commits to "Higher-for-Longer" (is it me or does it seem thematic whereby the bright minds here on Global Wall Street are in fact ‘getting it’ AND the narrative is shape shifting from soft landing and CUTS to … something else?)

Key Points ■ The Fed left all target and administered rates unchanged, as expected. ■ The policy statement was virtually unchanged from July, aside from an acknowledgement that payroll growth has slowed modestly. Overall, the assessment of the economy and labor force remains positive, though inflation remains unacceptably high. ■ Powell was appropriately vague in the press conference about future rate hikes, and reiterated the data dependent nature of the outlook. When the press offered scenario analysis to try and get a sense of the reaction function, Powell said that they would be looking at the "totality of the data", maximizing their flexibility. ■ Powell also seemingly admitted that the Fed underestimated the real-time neutral funds rate over the last 2 years. One interpretation of this admission is that policy rates may need to rise further from current levels to push down inflation, but the Fed is leaning more towards "higher-for-longer" rather than "higher-and-higher".

MS- FOMC Reaction: Proceeding Carefully (hawkish hike — make sense — so, staying LONG … hmmm, okie dokie …)

A hawkish statement and projections doubled down on the higher-for-longer message. Powell balanced it with a more careful tone, again playing down the importance of the projections and pointing to "significant declines in core inflation". Our strategists stay long 5y UST, long 30y TIPS, and long SFRZ4 on SFRU3Z4Z5 fly.

Nordea - FOMC Review: Still searching for the right level (not there yet)

The FOMC kept rates on hold while projecting one more hike this year. Growth projections were higher, and members now only see 50bps of cuts next year, half the June amount.

RBC - U.S. Fed skips September rate hike (an underwhelming note, IMO, but … they are Canadian and so, still reelin’ from their own CPI?)

…Bottom Line: Chair Powell reiterated that monetary policy is already at 'restrictive' enough levels to push inflation pressures lower over time, and that has let policymakers shift to a more 'data-dependent' approach to future interest rate decisions. To-date, easing inflation pressures have come without significant increases in unemployment, but labour demand (job openings) has continued to slow, credit conditions have tightened, and the growth backdrop is showing more significant signs of slowing in the rest of the world as headwinds from higher interest rates build. We continue to expect that economic growth and labour markets will soften, but the Fed is also still clearly willing to hike interest rates further if inflation were to show signs of reaccelerating.

UBS- The curse of the dot plot (if you don’t like it then stick with BOE ‘analysis’, please)

The Federal Reserve left rates unchanged (quantitative policy continues to tighten). Fed Chair Powell implied higher rates for longer at the press conference, but investors have little (or no) reason to trust Powell’s forward guidance. Data, rather than pontification, will guide expectations.

The curse of the dot plot marred the policy presentation. The Fed’s dot plot charts lack subtlety and complexity. A individual member’s 50:50 call on a rate increase is presented as an absolute certainty. In theory, a majority of the Fed think rates could rise one more time. This likely overstates the conviction. Subdued inflation and softer employment mean future US tightening should be by quantitative policy and real rates—nominal rates do not need to go higher.

The Bank of England decision today is a difficult call. Yesterday’s data shows profit-led inflation under pressure, but some of the inflation drop was due to volatile components. Economic growth has been revised significantly stronger, but that also means labor costs should be lower. If I had a vote (I haven’t been made governor yet), it would be for unchanged policy, but that may not be the majority decision today.

Elsewhere, there are US initial jobless claims and the Philly Fed business sentiment poll. Sweden and Switzerland also offer rate decisions.

Wells Fargo - Message from FOMC Meeting: Higher for Longer (straight forward?)

Summary

As widely expected, the FOMC kept its target range for the federal funds rate unchanged at 5.25%-5.50% at today's policy meeting. The decision to keep rates unchanged was unanimously supported by all twelve voting members of the Committee.

The statement noted that job gains remain strong, and it continued to characterize inflation as "elevated." The Committee also reiterated in the statement that "additional policy firming may be appropriate."

The Summary of Economic Projections, which highlights the macroeconomic forecasts of the Committee members, was more optimistic than in June. Specifically, median forecasts of GDP growth for this year and 2024 were revised higher, while forecasts of the unemployment rate were revised lower.

The so-called "dot plot" showed that 12 of the 19 Committee members believe that another 25 bps of rate hikes would be appropriate by the end of this year. Furthermore, the dot plot shows that only 50 bps of policy easing would be appropriate next year, considerably less than the 100 bps of rate cuts that were forecasted in June.

WolfST - In Very “Hawkish Hold,” Fed Keeps Rates at 5.50% Top of Range, Sees One More Hike in 2023, Only Two Rate Cuts in 2024, to 5.25%. QT Continues

… Higher for longer. A series of rate hikes are generally followed by plateaus before rate cuts begin. The Fed signaled that the plateau has not been reached yet, and that there may be another hike or two. And it indicated in the dot plot that when the plateau finally starts, it will be longer than previously indicated:

Statement leaves the door open for additional rate hikes. The statement repeated the language of the prior statements, which leaves the door open for more rate hikes:

“In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

WolfST - “Carefully,” Dude: Powell at the Press Conference

The FOMC’s latest Summary of Economic Projections (SEP) released today shows that the median forecast of the federal funds rate (FFR) for 2023 is 5.6%, unchanged from June’s SEP (table). The 2024 forecast was raised to 5.1% from 4.6%. As we expected, the FOMC’s message is that the FFR might be lowered next year by 50bps rather than 100bps…

… So why did the committee raise the FFR trajectory to holding-for-longer? The economy has been stronger than expected. The committee boosted this year’s estimated real GDP growth rate from 1.0% to 2.1% and next year’s from 1.1% to 1.5%. As a result, the trajectory of the unemployment rate was lowered to 3.8% this year from 4.1%, and to 4.1% next year from 4.5%.

AND a few OTHER … NOT FOMC related … things

Barcap - State of the US Consumer: Is the Consumer Cracking or Stretched (maybe NOT FOMC related — at least not DIRECTLY SO — still worth slowing down to have a look)

Our analysis shows consumption patterns are changing. As headwinds for the US consumer pick up, this could forebode slowing consumer spending later this year. Anecdotal evidence from retailers supports this, as commentary indicates consumers trading down with increased promotional activity.

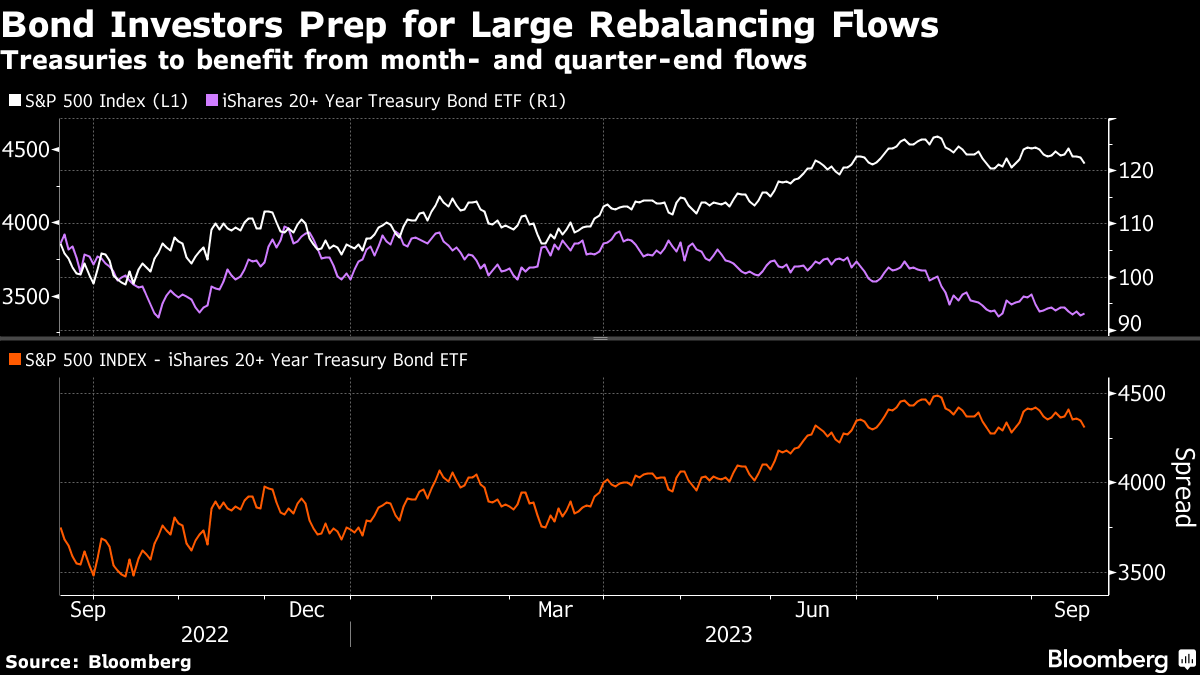

Bloomberg’s Five Things You Need to Know to Start Your Day (ASIA — where smart folks have moved ON from FOMC and looking TOWARDS … rebalancing flows)

… Treasuries are poised to draw demand thanks to investors who are rebalancing their portfolios as the quarter comes to a close.

Traders note there has been a widening of the gap between the S&P 500 Index and the iShares 20+ year Treasury Bond ETF even as both have fallen, driven by an outperformance in equities. The spread suggests investors will have much greater demand for bonds than stocks.

While a select group of fund managers are mandated to execute rebalancing only on the last day of the period, it is typical that some investors start rebalancing about two-thirds of the way through the period. That period, which can last for a few days, coincides with about now.

CitiFX Techs - As The Sun Rises: US yields break higher (alerted the other day on levels to watch … )

US 2y yields: We broke through resistance at 5.12%, setting a new YTD high post a hawkish FOMC. This also completes a breakout of the ascending triangle formation, which indicates potential upside.

However, we prefer to wait for a weekly close above the 5.12% level to add on to this view, given the packed agenda for the remainder of the week.

IF we do see this weekly close, we think we will see further upside, with little notable resistance till 5.2750% (2006 high).

Other US yields: We also see breaks above resistance for US 5y and 10y yields. US 30y yields approaching resistance at 4.47%.

It’s been little over a month since rating agency Fitch downgraded U.S. government debt from its highest rating (AAA) to its second highest rating (AA+). Among other reasons, the agency cited “a high and growing general government debt burden” as a reason for the downgrade. If hoping the downgrade would serve as a wake-up call to Washington, it hasn’t. Since the debt ceiling debate was resolved back in June, the Treasury department has steadily increased the amount of Treasury debt outstanding. As of September 18, total debt outstanding stood at $33 trillion, which is up from the $31.5 trillion right before Congress gave the Treasury Department unfettered borrowing capacity until January 2025. Now, to be fair, only $26 trillion of that is held by the public (with the rest held within the U.S. Government). But the congressional budget office expects total Treasury debt held by the public to grow to over $46 trillion by 2033. With so much Treasury debt expected to come to market over the next decade, it raises the question—who is going to buy all that debt?

As seen in the chart below, the current Treasury buyer base is diverse, with non-domestic buyers and the Federal Reserve (Fed) serving as the largest owners of Treasury securities. However, the Fed is in the process of shrinking its sizable balance sheet and is letting $60 billion of Treasury securities roll off each month (though debt that matures above the $60 billion threshold is currently being reinvested in Treasury securities). And the two largest non-domestic holders, Japan and China, have been reducing their holdings with both countries seeing their share of Treasury securities shrink by $100 billion and $256 billion, respectively, since 2020. And while Japan ($1.1 trillion) and China ($821 trillion) are still sizable holders of Treasury debt, it’s unclear if either country will be buyers of Treasury debt anytime soon.

That said, household investors and mutual funds (both areas with a pattern shade) have both been increasing their ownership in Treasuries. Additionally, according to the most recent Treasury data, foreign investment in Treasury securities have increased since 2020, despite the largest holders reducing their share. The United Kingdom (added $212 billion since 2020) and Canada (+$136 billion) have both been meaningful buyers of late.

Bottom line, as long as U.S. Treasury securities are regarded as risk free securities, there is always going to be demand for Treasuries. And with Treasury yields at the highest levels in decades, we could see that demand increase as well. In fact, it has to, otherwise the Treasury department could have a supply/demand problem on its hands.

And as all this ‘analysis’ and narratives re-settle back in, here’s an alternative view of the Fed yesterday TO the markets,

Agree with your Comments on the 10 year.....

You have a great talent for both understanding the financial markets and investors and

being able to write such an interesting newsletter.

Very Impressive....a wealth of knowledge

Absolutely fantastic coverage of the FED Decision !!!!

Loved the opening Historical 2 year chart !!!

I have to Laugh at Wall Street, sometimes....

Everyone in the World knew it would be Higher for Longer.

Who was Surprised ???

I guess some Poor Blokes were...

Chairman Powell is hitting his Stride....

"Carefully" crafting a Financial Constraint that is exquisitely Cloudy, exquisitely Patient and with a

Pot of at the End of the Rainbow.....

He was Masterfully Vague, yet with a Velvet Touch.

Revealing just enough Information to keep everyone guessing.

Did the 10 year Yield Breakout ???

I think so.....but not going past 5%, unless we get a REAL Surprise, from Left Field.

Great commentary on the US Debt and Funding predicament.

My guess is the US Treasury will continue to have to PAY UP, in order to Sell the massive

amount of Debt Paper, they need to move...

Reading The BondBeat makes me feel like I'm on Wall Street.....

That's a great feeling !!!!!!!!!

Thanks...