(USTs lower, underperforming globally on above avg volumes)while WE slept; CPI recaps and vicotry laps; based on analysis of the past, patterns suggest 2yy goin' down...

Good morning. This mornings note difficult to write given the magnitude of the move in bonds relative TO the ‘good’ news.

Clearly the TREND in CPI moving the the right / good direction for the Fed and I get that BUT the move in markets (both stocks AND bonds) seems to be conveying a message of clear and present danger of RATE CUTS and, well, I cannot help but think about HIGHER STOCKS + LOWER RATES = EASIER FINANCIAL CONDITIONS which then would work against the narrative AND, perhaps more importantly, against the Fed inflation fighting credibility …

Bloomberg: Ken Griffin Says Fed’s Credibility At Risk If It Cuts Rates Too Soon

Whatever. HE’s the billionaire … and speaking of wealthy US individuals, how about that historic photo op and meeting set to take place later on today?

Coincidence that SanFRAN streets are clean as a whistle on the day Xi / Biden set to have an HISTORIC photo op and announce some HISTORIC DEAL?

Coincidence that on this same day, China data showing the powerhouse economy regaining its stride …

Reuters: China's factory output, consumption beat forecasts but property still a drag on economy

Good morning!

Especially for those continuing to price in rate CUTS in 2024 and a special shout out to all those involved IN the markets between 825a and 835a (who helped put the jerk in KneeJERK) …

ZH: Wall Street Reacts To Today's CPI Shocker Which Was The Biggest "Market Surprise" Of 2023

… for now, I’d like to check back in on the belly of the beast … an update TO yesterday’s visual …

… wishin’ I’d drawn in that longer-term TLINE at 4.45 as that is precisely where we’d traded TO and are are now putting in some TIME AT A PRICE … This time can work off the now overBOUGHT conditions (red arrow, bottom panel)…

AND for more on those helping create the kneeJERK markets reflex see some of Global Wall St victory laps and CPI recaps below. For now, though,

Bloomberg: US Yields Slide as Traders See Rates Falling Half Point by July

Bloomberg: Bond Traders Shift to Aggressive Bets on 2024 Fed Cuts After CPI

… Bond Funds Boost Longs In data through Monday, JPMorgan’s latest survey of Treasury clients showed a jump in long positions to the biggest since November 2010, in a shift out of neutral positioning. The timing came just ahead of Tuesday’s bond-market surge after October’s inflation report. The survey shows net long positioning was the highest since June.

Hedge Funds Extend 2Y, 5Y Shorts In the week up to Nov. 7, hedge funds added to net short positions in 2- and 5-year note futures by a combined $10.3 million per basis point in risk, taking these levels to a record short. Asset managers were notably bearish 10-year note futures, liquidating around $8.4 million per basis point in risk of net long. Overall on the week, asset managers cut net longs by around 29,000 10-year note futures equivalents, while hedge fund net shorts were covered by roughly the same amount.

ZH: Yields Plunge, Stocks Soar, Dollar Tumbles As Fed Hikes Are Officially Over, Countdown To Cuts Begins

AND SO with a single confirming CPI print where those with a Terminal who can economically workbench the data and show 3mo, 6mo and on a 12m basis, "Disinflation proceeds in October”

(source below…but you get the picture) … a couple / few more CPI related links

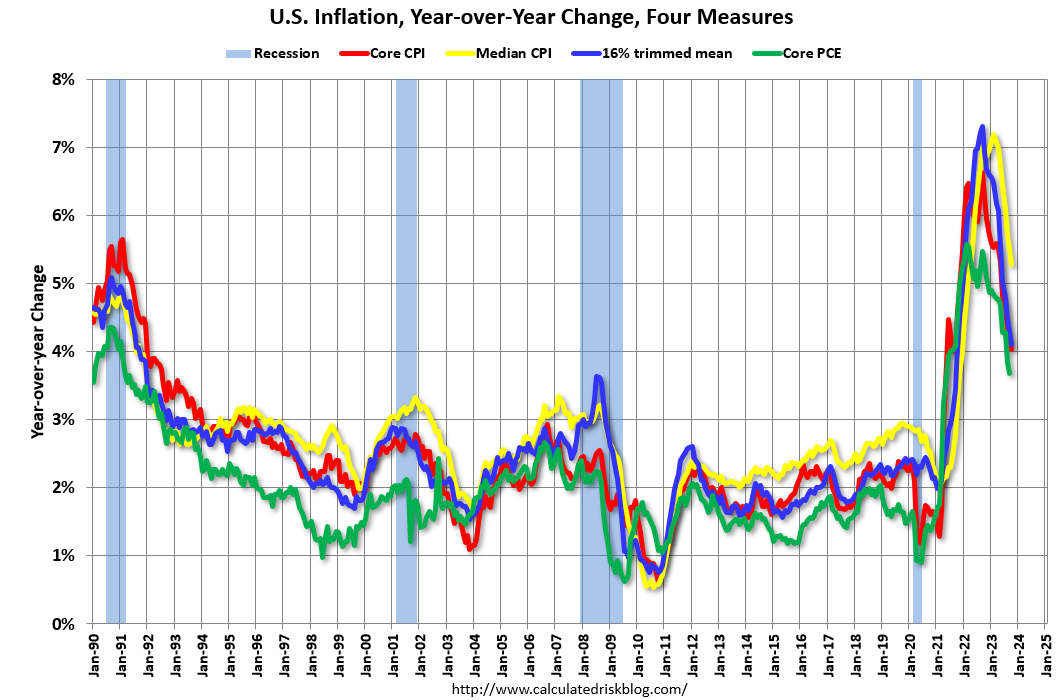

CalculatedRISK: BLS: CPI Unchanged in October; Core CPI increased 0.2%

CalculatedRisk: Cleveland Fed: Median CPI increased 0.3% and Trimmed-mean CPI increased 0.2% in October

ZH: CPI Unexpectedly Misses Across The Board, Core Inflation Lowest In Over 2 Years

… Other indexes with notable increases over the last year include motor vehicle insurance (+19.2 percent), recreation (+3.2 percent), personal care (+6.0 percent), and household furnishings and operations (+1.7 percent).

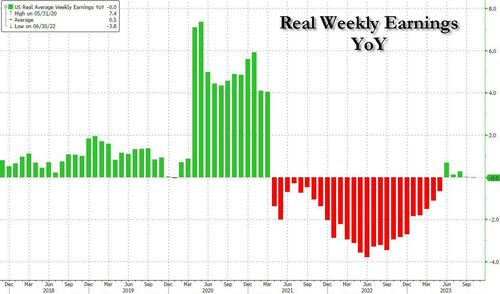

So what does this drop in inflation mean for US Consumers? Well, it means that in real terms average hourly earnings were... unchanged in October as YoY inflation effectively destroyed all wage gains over the past year.

Finally, we bring your attention to a chart we posted one year ago, showing the correlation between M2 and CPI, when we predicted that CPI was about to collapse…

… One year later we were right, and there is much, much more to go.

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower, mildly underperforming their UK and German peers ahead of retail sales/PPI and after weak UK CPI, weak German IP and mixed data out of China (see above). DXY is modestly higher (+0.12%) while front WTI futures are modestly lower (-0.5%). Asian stocks rallied sharply after a surge in NY yesterday, EU and UK share markets are all in the green (SX5E +0.75%) while ES futures are showing +0.43% here at 7am. Our overnight US rates flows saw solid Asian volumes concentrated in the belly of the curve after numerous futures block trades posted (outright and on curve). In London's AM hours our desk reported a reluctance to chase higher prices with some profit-taking noted in the belly (on 'fly) and the long-end (outright). Overnight Treasury volume was decent at ~150% of average with futures seeing even higher relative average turnover, amid good block activity.

…Our first attachment this morning looks at the long-term, monthly chart of Treasury 2-year yields. After holding major range support where it should have last month (5.27% area- see shadow box for a zoomed-in look), long-term momentum in the lower panel is now threatening a bull flip with evidence of bullish divergence (higher highs in yields this year, lower highs in momentum) to boot. What's also interesting is that the price pattern since September may be tracing out a potential Evening Star, bullish trend reversal candlestick pattern too. So our two most favor/reliable trend reversal signals are evident here and the only thing missing is a monthly close to confirm everything. If confirmed, next major resistance for 2's appears to be back near 3.00%- the 2018/2019 cycle peak left behind last year.

… and for some MORE of the news you can use » The Morning Hark - 15 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

ABNAmro: More good (inflation) news for the Fed | Insights newsletter

CPI inflation for October came in a touch weaker than consensus, though in line with our forecast at 0.0% m/m, while the core CPI also surprised to the downside at 0.2% (consensus/ABN: 0.3%). In annual terms, disinflation therefore continued, with headline inflation falling back to 3.2% y/y from 3.7% and core inflation down one tenth to 4.0%.

ABNAmro: China: Decent October data on day Xi meets Biden | Insights newsletter

China Macro: October data confirm bottoming out, but with headwinds remaining. Government continues with targeted support. Biden and Xi meet in San Francisco.

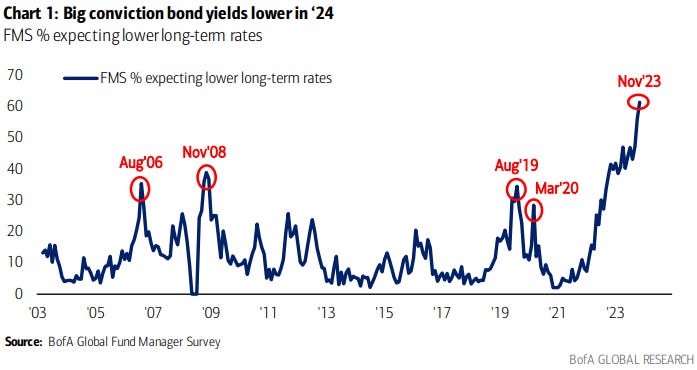

BAML: Global Fund Manager Survey - Bonds have more fun (alluded to HERE YESTERDAY and worth another look / chart)

… The big change in the November FMS was not the macro outlook, but rather the conviction in lower inflation, rates, and yields…

…as evidenced by the 3rd largest overweight in bonds in the last two decades (only in Mar’09 and Dec’08 were investors more overweight bonds).

Core inflation was softer than expected, at 0.2% m/m, led by a sharp pullback in OER inflation and a sizable drop in lodging costs. Beyond these categories, there were other, albeit smaller, pockets of disinflation. All told, we think the FOMC is likely to draw comfort from this report and hold rates unchanged in December.

Barcap: China: Taking October data with a grain of salt (perhaps these folks didn’t get the memo — ALL IS WELL — ahead of the HISTORIC photo op meeting today)

October activity data overall painted a still-subdued picture on domestic demand. Sequential momentum in retail sales stagnated for the second straight month, and indicators for the housing sector mostly deteriorated. We maintain our view of a growth slowdown in Q4 before rebounding in Q1 on stepped-up policy support.

BMO: CPI 0.0% as core-inflation moderates further; Treasuries Rally

Headline CPI was unchanged in October versus +0.1% consensus and +0.4% Sept. This brought the YoY pace to +3.2% compared to +3.7% Sept and +3.3% forecast. Core-CPI MoM surprised on the downside at +0.2% vs. +0.3% prior and +0.3% forecast. Core-CPI YoY slipped to 4.0% vs. 4.1% Sept and 4.1% forecast (matching the lowest since May '21). Core services ex-shelter came in at 0.344% from 0.461% in September while core-CPI services ex-rent/OER was 0.216% versus 0.611% prior. This print was good news for the Fed and offers evidence that monetary policy is still effective and impacts the real economy with a lag -- the fundamental things apparently still apply. This takes a rate hike off the table in December and reinforces our call that July was the last hike of the cycle and the process will now shift to the Fed attempting to delay cuts as long as possible.

The Treasury rally that followed the release has been significant with 10-year yields dropping as low as 4.477% and have stabilized at 4.50%. The front-end of the curve has put in a solid performance as well with 2-year yields slipping to 4.863%. We anticipate that incoming Fedspeak will seek to reiterate the waitand-see stance, but it will be difficult for monetary policymakers to dissuade investors from penciling in a more aggressive series of cuts in 2024…

The downside surprise in October core CPI was not just a goods and shelter story – non-housing services (aka “super-core”) inflation finally started to moderate as well.

While we remain of the view that a weaker labor market will be required to bring non-housing services inflation all the way back to target-consistent levels, the October report raises the notion that we could see elements of “immaculate disinflation” in the category, particularly when coming off such high levels.

Core PCE inflation looks on track to undershoot the Fed’s 2023 forecast comfortably, which should give policymakers added confidence to abstain from further rate hikes.

Preliminary November forecast: 0.1% m/m headline and 0.3% core.

The October CPI data came in much weaker than anticipated with headline remaining roughly unchanged (+0.04% vs +0.40% in September) while core only rose by 0.23% (vs. +0.32%). The major surprises relative to our forecast were in volatile categories, namely lodging away and airfares, with the former declining by 2.4% and the latter by 0.9%. Taken together, the year-over-year rate for headline fell by five-tenths to 3.2%, while that for core fell a tenth to 4.0%.

Our forecasts are little changed. We expect November core CPI to come in at +0.33% m/m and 4.0% y/y. Our Q4/Q4 forecasts are 4.0% for 2023 (unch.), 2.6% for 2024 (down a tenth), and 2.5% for 2025 (unch). Our Q4/Q4 core PCE forecasts have similar changes: 3.5% for 2023, 2.3% for 2024, and 2.2% for 2025. The analogous headline numbers are 3.2%, 1.8%, 2.3% for CPI and 2.8%, 1.5%, 2.0% for PCE.

Today's data largely support the Fed's narrative around inflation. Specifically, goods inflation seems to be largely "solved", rental inflation is set to moderate as slower asking rents work their way through into the rental stock as a whole, and core services ex housing inflation will come down as the labor market is brought into better balance. Indeed, the market took out nearly all of the pricing for any future hikes in the wake of the CPI data. While we previously saw significant risks the Fed might need to raise rates further, today's data give us greater conviction that the Fed is likely done tightening.

DBDaily: A miss on US CPI; hike pressure off the Fed:

…Driving sentiment, a miss on US CPI, headline flat in October, consensus looked for a 0.1%mom rise. Core up 0.2%mom, consensus at 0.3%mom. Year-ended headline dropped to 3.2%yoy, core dropped to 4.0%. In the details, 'lodging away' and airfares' contributed to the weakness, down 2.5%mom and 0.9%mom respectively.

Justin Weidner's take on the US CPI. While DB's US team previously saw significant risks the Fed might need to raise rates further, this print has given them greater conviction that the Fed is likely done tightening

DB: "Never underestimate the US consumer" has been underestimated

The maxim "never underestimate the power of US consumer" has plainly been lost on the collective wisdom of street economists, for there has not been a downside surprise to retail sales control since the December '22 data released in January '23.

What a time it would then be to see core retail spending come in below expectations, at just the moment when the market has swung firmly in the direction of trading "peak US interest rates".

A weak retail trade number that hinted at the consumer rolling over, has all the capacity to drive the 10y yield back to the original yield break-up point around 4.34%, and with it EUR/USD to near 1.10. We could see those levels initially rejected, and a loss of momentum near there, precisely because at that point the market will have to consider that risk-reward has swung firmly in the more bearish direction on short-term rates - whether it be because pricing in zero chance of a rate hike in January provides good risk reward for the chance that Dec data prints very strong; or, better still fading the pricing of a near 1 in 3 chance of a rate cut in March '24, that looks to have severely underestimated the extent to which the Fed wants to secure the 2% inflation target projections before embarking on a cutting cycle. Even if the core retail sales data is weak, it is unlikely to change the above view on the March FOMC date, and it will provide better levels to play for a plateau in US rates that extends beyond Q1.

DB: Early Morning REID (lucky 7s … this DOVISH PIVOT gonna be THE one)

What a difference a tenth of a percentage point makes as markets have staged a remarkable rally across the board after the US CPI release. A (small) downside surprise led to increasing confidence that the Fed were done hiking rates, and that a cut was now more likely than another hike. Will this be seventh time lucky in this cycle in terms of pricing a dovish pivot? The other 6 have failed to materialise and although one will obviously do so at some point, is this it? The market thinks so and front-end Treasury yields saw their biggest daily decline since the banking turmoil in March, with the 2yr yield down by a massive -19.9bps on the day. And the prospect of lower rates proved great news for equities as well, with the S&P 500 (+1.91%) posting its strongest advance since April with the Russell 2000 (+5.44%) having its best day for over a year. Watch out for US retail sales today and the Xi-Biden meeting at around 7pm London time with a press conference 11:15pm London time.

FirstTrust: Data Watch - The Consumer Price Index (CPI) Was Unchanged in October

… Implications: … Taking a deeper look under the inflation hood, rental inflation – both for actual tenants and the imputed rental value of owner-occupied homes – continues to run hot, up 0.4% for the month and running close to or above a 6% annualized rate over three-, six-, and twelve-month timeframes. Meanwhile, a subset category of inflation that the Fed is watching closely – known as the “Super Core” – which excludes food, energy, other goods, and housing rents, rose 0.2% in October. This measure is up 3.7% in the last twelve months but has been accelerating of late; up at a 4.9% annualized rate in the last three months. No matter which way you cut it, inflation is still not where the Fed wants it to be. With interest rates now above inflation across the yield curve and the M2 measure of the money supply down 3.6% in the past year, money is tight. But it remains to be seen how quickly this will translate into bringing inflation down to the Fed’s 2.0% target. It’s important to note that even when the inflation target is eventually reached, prices will remain permanently adjusted versus their pre-COVID level. For example, food prices have now risen thirty-nine months in a row and are up 24% since before COVID, owing to the significant money creation over the last few years. As for the economy, we continue to believe a recession is on the way. Equity investors should remain vigilant as we navigate these unprecedented times.

BOTTOM LINE: October core CPI rose 0.23%, below expectations for a 0.3% increase, and the year-on-year rate edged down 0.1pp to 4.0%. The composition was mixed on net: while today’s reading was flattered by a sharp decline in hotel prices that we wouldn’t expect to persist, the stickier OER and medical care services categories were softer than expected and trimmed measures of inflation similarly slowed. The health insurance component swung from its -4% per month pace of the last 12 months to +1% as the BLS incorporated new source data on insurer profitability, and should remain at this new pace through April 2024.

Goldilocks: Congress Punts Shutdown Risk to January 2024 (shutdown risk gone but not forgotten?)

BOTTOM LINE: Tonight (Nov. 14) the House passed a bill that would extend government funding at current levels until Jan. 19 or Feb. 2, 2024, with no other policy changes attached. The Senate is likely to pass the bill ahead of the Nov. 17 deadline, and President Biden looks likely to sign it into law. The risk of a shutdown increases in January, as reaching a long-term funding deal looks difficult but another short-term extension is likely to face greater political resistance.

ING: US inflation slowdown has much more to go (‘scope for SIGNIFICANT easing in 24’)

US consumer price inflation slowed more than expected in October. Higher borrowing costs will increasingly weigh on activity and corporate pricing power while slowing housing rents will be the main driver of disinflation over the next two quarters. With 2% inflation looking possible by next summer the pricing of rate cuts will intensify …

… Housing slowdown will increasingly depress core inflation

Scope for significant Fed policy easing in 2024 With growth concerns likely to increase over the same period, this should give the Federal Reserve the flexibility to respond with interest rate cuts. We wouldn’t necessarily describe it as stimulus, but more a move of monetary policy to a more neutral footing with the Fed funds rate expected to end 2024 at 4% versus the consensus forecast and market pricing of 4.5%.

JEFF: Oct CPI Flat, Core +0.2%... Finally, a Step in the Right Direction (finally…)

■ The October CPI was unchanged (+0.0449% unrounded) with core up 0.2% m/m (+0.2266% unrounded). Both the headline and the core came in a tick below consensus. ■ Looking through the surface-level measures to the so-called "super core" of core services ex-housing, inflation decelerated sharply from September, to +0.216% from +0.611%. Our more preferred super core measure, which also removes medical care services and public transportation, was even softer as it rose +0.187% compared with +0.716% in September. ■ For a change, there's no secret here with the data. a handful of different components remain extremely firm, but most showed signs of softening in October. The story we see in the headline is consistent throughout the details. This should be a comforting sign for the Fed, and it should eliminate any expectation that they will raise rates again in December or thereafter.

JPM: The J.P. Morgan View - Global Asset Allocation. Shift from government bonds to commodities (so, to paraphrase, FROM disinflation TO INFLATION theme…? at the very least, putting some hay in the barn … )

… This month, we take profit on our long duration exposure in government bonds given their strong rally, increasing supply, dovish Fed pricing and increased investor positioning. We use the cut in bond allocation to fund an increase in our commodity allocation given still high geopolitical risk, and the significant sell-off and weaker positioning in energy, and we incrementally shift our within-commodity allocation into energy…

… A second indicator is based on our framework for momentum traders such as CTAs. This indicator shown in Figure 11Proxies fCTA/moentu radespoitng is based on the average of the z-scores of our shorter-term and longer-term momentum signals. This indicator has shifted to negative territory, suggesting that momentum traders are currently short in oil futures.

… In the bond space, the combination of a lower than expected Treasury refunding announcement, a less hawkish message at the FOMC meeting and the softer than expected payroll report has brought some relief from the seemingly relentless sell-off in bonds since May as 10y UST yields have declined by more than 40bp from Nov 1st to Nov 8th. We had added some bullish exposure in our last GAA, which benefited from this decline in yields. However, the poor 30-year UST auction highlights that, while coupon issuance is not increasing as much as feared, net Treasury bond supply is nonetheless increasing sharply from around $450bn in 2023, excluding the increased supply from Fed QT, to $1.3tr even as there has been a shift towards more price sensitive sources of demand. Fed pricing has also turned more dovish, with more than 20bp of a cut priced in by mid-2024. Moreover, there remains a significant long base in positioning among real money investors, as indicated by both our Treasury Client Survey that saw an increase in net longs to close to their mid-2023 highs as well as the elevated total duration betas of active US bond mutual funds …

… This means that the backdrop for yields has turned less bullish over the past few weeks, and our US rates strategists have tactical shorts in 7y USTs. In addition, the combination of increased net supply and the shift to more price sensitive demand points to continued upward pressure on term premia at the long end. This, combined with an on-hold Fed means we see further steepening pressure on curves and add 10s/30s steepeners.

Reduced energy and food costs brought headline inflation down, but core price pressures also eased.

The Fed’s favored inflation gauge posted a small (0.2%) increase in October but is still high over the last three months

Still, the breadth of inflation pressures showed signs of moderating

Slowing labour demand, leading to moderated wage growth.

A drop in rental market rate foreshadowed a further dip in Rent CPI.

… Bottom line: The October CPI data should calm concerns that inflation was reaccelerating after an upside surprise a month ago. Fed policymakers are wary of a reacceleration in price growth, but evidence is building that economic momentum is fading. GDP growth remained exceptionally resilient through Q3, but the unemployment rate has begun to edge higher - the 0.4 percentage point increase over the last three months is small but an increase of that size typically only happens at the start of a labour market slowdown and wage growth has slowed. Policymakers at the Federal Reserve are still willing to push interest rates higher if necessary, but that looks increasingly unlikely to be necessary. We continue to expect the Fed to leave the fed funds target range unchanged until pivoting to gradual cuts in the second quarter of 2024.

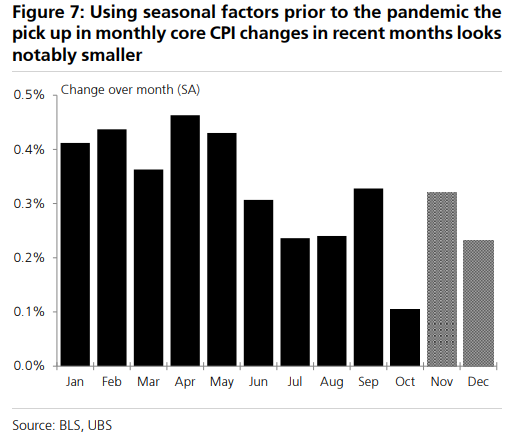

Headline CPI +0.04%: Weaker than expected… Core CPI +0.23%: Hotels lead the slowing and OER reverses uptick… … Notably, we believe that even the 23bp increase this month was held up by seasonal factors that have swung around during the pandemic. Using pre-pandemic seasonal factors the monthly October core CPI change would have been only 10bp. (Figure 7)

October core PCE prices +0.20%… Moderate headline/strong core CPI likely in November…

Summary October's softer-than-expected CPI print is an encouraging development for the FOMC and reinforces our view that the FOMC has ended its hiking cycle. But, we do not see the latest data as a game-changer for inflation's path ahead. With inflation in October held down by volatile components like gasoline, travel services and autos, we expect inflation's return to 2% will continue to be a slow grind.

Wells Fargo: NFIB Small Business Optimism Down in October

Summary Economic Headwinds Weigh on Small Business Sentiment Small business owners have remained broadly pessimistic through an apparent period of U.S. economic resilience. The Small Business Optimism Index ticked down slightly in October to 90.7, marking nearly two years that the index has remained below its longerterm average. The outlook for near-term business conditions also remained depressed, reflecting a mix of deteriorating sales traffic, reduced credit availability, lower earnings and limited availability of labor. As small businesses struggle to find the workers they need, compensation pressures appear to be mounting, which may present a challenge to the Fed’s goal of achieving sustained 2% inflation.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Five Things to Start Your Day (Asia commentary noting rally in bonds looks OUT OF PROPORTION TO CPI MISS …)

…The Treasuries rally that followed a modest miss on inflation data looks too good to be a true reflection of where the economy is heading. Five-year US yields dropped 23 basis points as traders focused on the shorter end of the curve. That’s the most since March, when a banking crisis raised concerns that the US could rapidly tip into a recession. Considering that core annual inflation came in at 4.0%, rather than holding at 4.1% as expected, Tuesday’s move looks excessive.

A consideration of what went on in the rates market underscores that perception. Traders erased the small remaining bets on hikes, while the fourth-meeting dated OIS — which currently covers the May 2024 meeting — went from pricing in about 20% odds of a cut to signaling an 80% chance. That seems impressive, but it’s a far cry from March, when the fourth-meeting OIS flipped from pricing in at least four hikes to signaling two rate reductions.

The likelihood is that a rush to cover short positions and put on fresh longs overcharged the rally as investors rushed to anticipate a rapid Fed pivot toward rate cuts. That’s despite policymakers saying after the CPI data they still see a long, potentially hard road to get inflation back down to where they want it.

Bloomberg: Investors better hope this disinflation stays immaculate (Authers’ OpED … section on BONDS and UPTREND being ‘toast’ catches ones eye)

… Bonds… Before looking at the bond market’s emphatic reaction to the news, it’s important to grasp that many investors were just waiting for a good opportunity to buy. The latest fund manager survey conducted by Bank of America was published a few hours before the inflation data. It showed the biggest conviction on record that long-term yields are heading downward:

With so many predisposed to buy bonds, it’s not surprising that good news on moderating inflation could spark a drastic reaction. The steady upward trend in 10-year yields since markets emerged from the shock of the March bank failures looks like it might at last be over. (I drew the trend lines myself on the terminal, and there are doubtless other ways to look at it — but it’s hard to deny that yields have followed a clear path upward for a long time, and that that now appear to be over):

The enthusiasm for bonds is strongly tied to the Fed, and to a continuing reluctance to believe that inflation is back as a fact of life. That’s clearest if we break down the 10-year yield into two components — the expected inflation over the next 10 years, and the “real yield” payable over and above the rise in prices. The current rate-raising cycle started at the turn of last year, at which point the fed funds rate was still virtually at zero and inflation was rising ominously…

… By the end of the day, some Wall Street big guns were trying to rein in the enthusiasm. Ken Griffin, the founder of Citadel, warned that the Fed risked losing credibility if it declared victory over inflation. Jamie Dimon, CEO of JPMorgan, repeated that inflation “might not go away quickly.” None of this stopped the emphatic move in the bond market.

FRB of Atlanta: Atlanta Fed's Sticky-Price CPI Remained Elevated in October - November 14, 2023

The Atlanta Fed's sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—increased 4.3 percent (on an annualized basis) in October, following a 5.5 percent increase in September. On a year-over-year basis, the series is up 4.9 percent.

On a core basis (excluding food and energy), the sticky-price index increased 4.3 percent (annualized) in October, and its 12-month percent change was 4.9 percent.

The flexible cut of the CPI—a weighted basket of items that change price relatively frequently—decreased 8.0 percent (annualized) in October and is down 0.3 percent on a year-over-year basis.

LPL: Why the Bond Market Doesn’t Care About the Moody’s Downgrade… Yet.

…In our view, the bond market’s collective shrug for the outlook change affirms that rating agencies are only catching up to the fiscal policy challenges that the bond market has been pricing in for several quarters. In fact, until recently, the market has been trading primarily on the expected increase in Treasury supply to fund budget deficits expected over the next several years. Per the Congressional Budget Office, the U.S. government is expected to run sizable deficits over the next decade in the tune of 5%-7% of GDP each year, which means a lot of Treasury issuance is coming to market.

That is obviously a lot of supply that needs to find demand. However, since we know the U.S. rarely (if ever?) actually pays its debts off, there is also a lot of existing debt that needs to be rolled over as well. Over the next 13 months, the U.S. will need to refinance over $9 trillion of debt with over $3 trillion due this year. The additional supply comes at a time when price-insensitive buyers are stepping back from the Treasury market. The supply/demand imbalance will likely mean interest rates are going to be higher than they otherwise would be absent sizeable deficits.

These refinancings will take place with interest rates among the highest in over a decade. So, with the recent announcement that interest expense on existing debt hit $1 trillion, interest expense is likely only headed higher—concerns that were outlined by Moody’s (and Fitch in August). So, frankly, it’s no surprise that rating agencies, in general, have started to sound the alarms that fiscal risk is rising. Importantly though, in our view, the downgrades do not suggest the U.S. will have trouble paying its debts; we think there is currently a very low probability of default. But, until the U.S. government gets its fiscal house in order, we’re likely going to see additional downgrades and likely higher interest rates in the Treasury market.

Nautilus Research: Pure Past Pattern Analysis Suggests Lower 2-year Yields (better than average analysis, follow this STACK if you can and if not, know that I will …)

… The three-month average, which irons out the month-to-month ups and downs, rose by 0.36%, or 4.4% annualized, with October and September values being the biggest increases since November 2022:

Core CPI, month-to-month rose by 0.23% in October from September, a slower increase than in the prior month, pushed down by the drop in durable goods, and helped by the moderate month-to-month rise in core services (blue line).

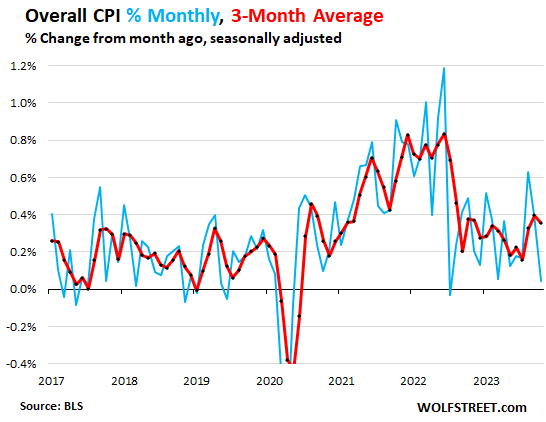

The three-month moving average rose by 0.28%, the biggest increase since June (red):

According to Harkster, 20 FOMC talking heads on deck to spew their 4th Reich propaganda. Man I miss the bygone Briefcase Indicator era!

Outstanding coverage of the October CPI report !!!!!