(USTs higher / flatter on light volume)while WE slept; "Is 3 the new 2?" (DB); "Bond vigilantes will be back" (Dudley); 'BIG conviction in LOWER yields in 24' (BAML)

Good morning. MOST if not all of what follows will need a severe edit just after 830a and the CPI print.

Hard to believe that many out there are placing lots of weight on a single CPI print — today’s CPI — for narrative creation. Truth be known, most of them are armed and dangerous with Bloomberg and the ‘ole ‘economic workbench’ (I’m sure I’ll be posting some of those ‘workbenched’ charts here tomorrow to ‘prove’ one point or another) and can shape shift the narrative however they’d like.

In the meanwhile, there are websites and headlines like these …

Bloomberg: US Inflation Report to Keep Fed Leaning Toward More Rate Hikes

A monthly US government report on consumer prices due Tuesday is set to show slower progress toward the Federal Reserve’s 2% inflation target, keeping the central bank biased toward more tightening, according to Bloomberg Economics.

The figures are set to show the consumer price index excluding food and energy rose 0.3% for a second straight month in October, leaving the year-over-year rate unchanged at 4.1%, Bloomberg economists Anna Wong and Stuart Paul said Monday in a preview of the report.

Bloomberg: Asset Managers Warn of More Failed Trades as US Market Speeds Up

Bloomberg: Yellen Says She DisagreesWith Moody’s Negative Outlook on US

Thanks, Janet … saying nothing of government largess which is keeping the economy moving and so, in your disagreement you are totally acknowledging Moody’s point?

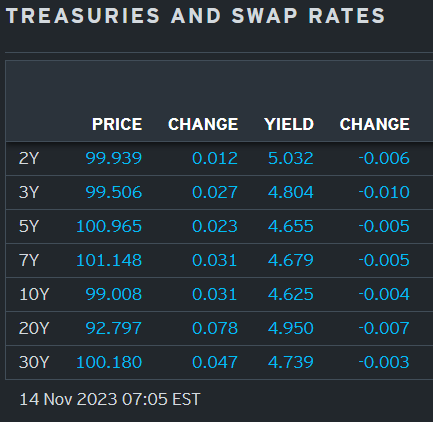

AND so, those armed and dangerous with a Terminal shall continue on into and THROUGH today’s CPI and be that as it may, I’ll simple defer to their PhD expertise while in meanwhile, I’d pass along a chart of the belly (5yy) as it strikes ME as important

RED LINE in / around that 4.65% (50dMA as well as local level of interest) shall be on the proverbial radar screen. Today and on into remainder of the week…

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher with the curve flatter ahead of this morning's CPI print. DXY is little changed (-0.07%) while front WTI futures are too (-0.15%). Asian stocks were mostly higher, EU and UK share markets are modestly higher (save for the UK's FTSE 100 at -0.45%) while ES futures are little changed here at 6:50am. Our overnight US rates flows saw another quiet Asian session with little flow to report on ~50% of average volumes. Overnight Treasury volume (including London's AM session) was ~75% of average with 20yrs (119%) seeing the only above-average turnover this morning (off a low base).

… and for some MORE of the news you can use » The Morning Hark - 14 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Monetary policy is tighter than it appears, but it may have peaked in July and started to ease according to our analysis of the Proxy Funds Rate, an analytical tool tracked and updated monthly by the Federal Reserve Bank of San Francisco. At the end of October, the rate was 6.7% compared with the official fed funds target of 5.25%-5.5%. It peaked at 7.1% in July and has declined through October. The rate recognizes that central bankers in the twenty first century use many tools (not just short-term interest rates) to meet their "dual mandate" of stable prices and maximum sustainable employment. The Fed uses forward guidance to communicate the direction of monetary policy and influence longer-term interest rates and broader financial conditions. The Fed also can expand its balance sheet through the large-scale purchase of Treasury and Mortgage Backed Securities, which is known as quantitative easing, or reduce its holdings, which is known as quantitative tightening. The Proxy Funds Rate uses the analysis of 12 financial variables, including Treasury rates, mortgage rates, and borrowing spreads, to translate the full range of policy actions into an analogous level of the funds rate, That can help assess whether policy is tighter or easier than the official funds rate suggests. In a November 2022 San Francisco Fed Economic Letter, the developers of the proxy rate noted the following: "As the FOMC increasingly used forward guidance and the balance sheet, the proxy rate has tended to lead the actual funds rate, reflecting the fact that financial markets are forward looking." It could be a good sign for conventional Fed watchers if the proxy rate peaked in July. The letter also noted that "combined policy tools have a more complex effect on the economy than the federal funds rate indicates." That suggests to us that Fed watchers should become even more diligent.

BNP: Quant Trades of the Week: Remaining upbeat on risk, with FCI in focus

KEY MESSAGES Market themes:

Our global risk premium index has moved higher over the past week, but risk appetite levels differ across different asset classes.

Medium term macroeconomic factors indicate a balanced outlook for risk as US credit spreads remain stable. We currently see US financial conditions as an important short-term risk driver.

With the recent loosening of US financial conditions supporting our short term outlook for risky assets, we keep our pro-risk bias hedged through higher rates.

… Highlighting rates and US financial conditions … Financial conditions keep loosening: Our US Financial Conditions Index (Figure 3) indicates that financial conditions have been loosening in past weeks, despite Powell’s relatively hawkish stance in his latest speech, with the main drivers lower volatility and tighter credit spreads. This we think indicates that the threshold for economic events to shift the FOMC from its wait-and-see stance is relatively high. Still, as tight financial conditions themselves are cited as one of the reasons in favour of the end of rate hikes, a loosening of financial conditions might see some push-back from Fed speakers throughout the week.

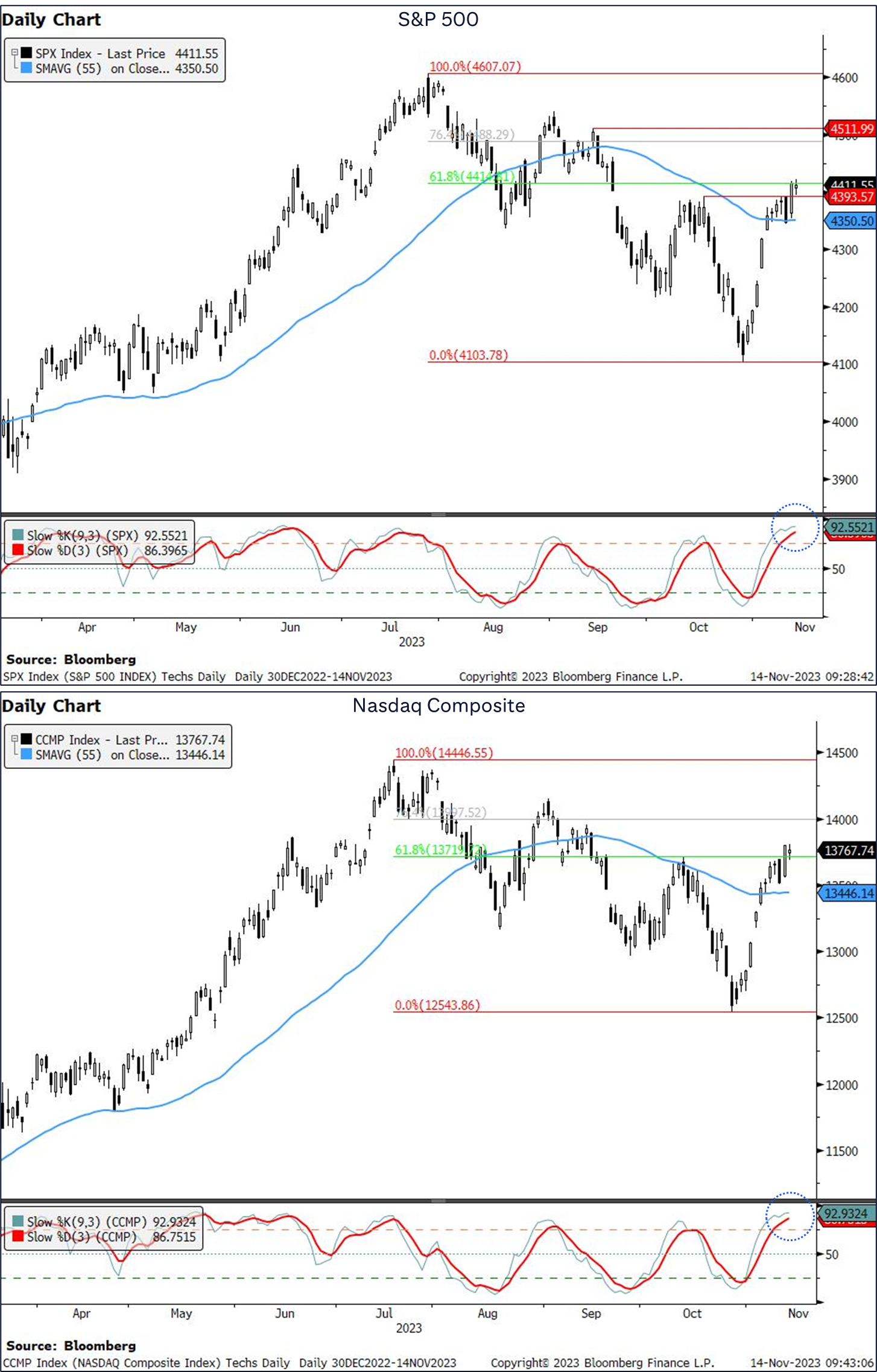

US stocks have broken above resistance of the October highs on a weekly basis.

Why it matters: This means that we have set a new higher-high, breaking the downtrend since late July. Lower lows and lower highs and a sign of a healthy downtrend, and vice versa.

The break in the downtrend series suggests that the upward momentum is set to extend. However, this heavily depends on the outcome of US CPI today. Weekly closes will be key in evaluating this view.

Levels to watch:

S&P 500: We are currently testing resistance at the 61.8% Fibo retracement of 4415. IF we break higher, the next key area to watch will be at 4488-4511 (76.4% Fibo, Sep 14th high). To the downside, 55-day MA at 4350.50 will be the first support.

Nasdaq Composite: A break above 61.8% Fibo retracement means that we could see an extension towards next resistance at 13998-14000 (76.4% Fibo retracement, Psychological resistance). To the downside, watch 55-day MA at 13446.14 …

DB: Early Morning REID (on CPI putting ALL the proverbial hike eggs in one basket … specifically today’s CPI)

… When it comes to the Fed, their next move will of course depend on today’s CPI print for October, which will be out at 13:30 London time. In terms of what to expect, our US economists see headline falling back to +0.14% given the decline in gas prices, but they think core will see an uptick to +0.39%, which would be a 5-month high if realised. In turn, that would see a decline in year-on-year headline CPI back to 3.3%, but core would move up by a tenth to 4.2%. So it would add to the recent signs that core inflation is proving stubborn, and if these forecasts are right, it would be the third consecutive month with core CPI running at +0.3% or more. See their full preview here, along with how to sign up for their webinar following the release…

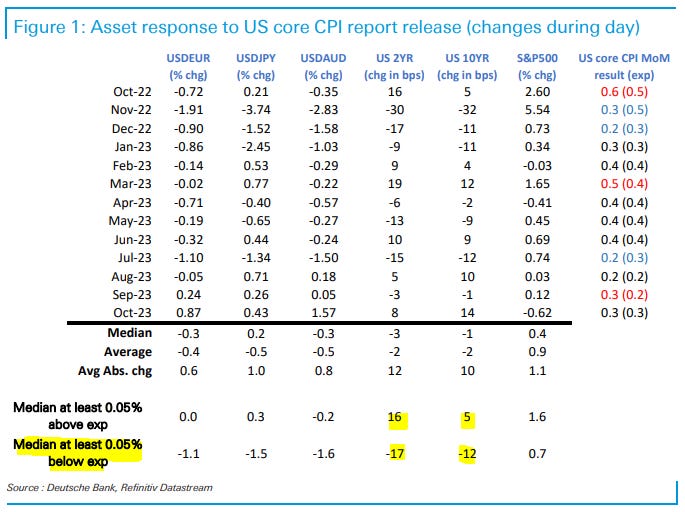

As the Fed is perceived to be at, or approaching its last rate hike in the cycle, the 2y yield has started to fail to respond by double digits basis points in yield terms, but the back-end has largely maintained its sensitivity to this data (see Figure 1). That likely fits with the market response to the October data as well.

Intriguingly, the last three times core CPI came in as expected, the Treasury bond market ended with higher front and particularly back-end yields, suggesting the market had either become overly excited about inflation decelerating, or found something in the data that smacked of 'sticky inflation'.

This time around it feels like as expected numbers are needed for the back-end to consolidate on recent gains, not least because an as expected 0.3% core data point, does not in itself give confidence that the data is on a firmly established track to the Fed's 2% target.

From that perspective, a breakdown consistent with an underlying 0.2% number, would likely set in train a 10y yield retest of the recent cycle lows near 4.47%. DB on the other hand sees greater risk of a 0.4% core thanks to air fares and lodging away from home. This would at a minimum extend the expected plateau before rate cuts, creating an ongoing drag for duration and potentially pulling 10y yields back above 4.7%. There is then close to a 25bp spread on the 10y reaction, between a not distorted 0.1% core CPI miss to the downside, versus the same miss to the upside …

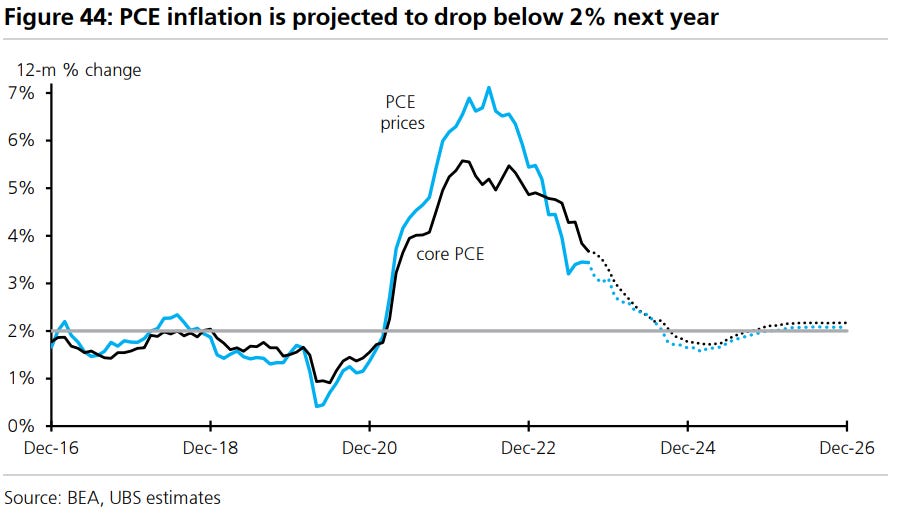

DB: Is 3 the new 2? (a question nobody asking or wants to hear answer to…)

Clearly the big event of this week will be tomorrow's US CPI release. Today’s CoTD comes from Matt Luzzetti’s latest chart book (link here) and shows that there’s some tentative evidence of core inflation settling around 3%. There’s some concern about this at the Fed too, with Dallas Fed President Logan echoing these thoughts last week…

… So we're at an important juncture. Is core going to be stuck around 3% absent a recession? If it is then this will be the 7th market attempt at pricing in a dovish pivot in this cycle…

Goldilocks: October CPI Preview: Residual Seasonality and Health Insurance Turn Around

We expect a 0.32% increase in October core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 4.13% (vs. 4.1% consensus). We expect a 0.09% increase in October headline CPI (vs. 0.1% consensus), which corresponds to a year-over-year rate of 3.29% (vs. 3.3% consensus). Our forecast is consistent with a 0.28% increase in core services excluding rent and owners’ equivalent rent in October…

… Going forward, we expect monthly core CPI inflation to remain around 0.3% in the next few months. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect a small offset from a delayed acceleration in healthcare. We forecast year-over-year core CPI inflation of 4.0% in December 2023 and 2.7% in December 2024

UBS (Donovan): Inflation reality and soft landings

October US consumer price inflation headlines have two significant factors. Health insurance calculations are changing and are likely to add to the inflation rate—but of course changing how inflation is calculated does not change inflation reality for consumers. And the fictional owners’ equivalent rent data should contribute less to inflation, again without changing reality.

The inflation reality is that middle-income homeowning US households face a lower inflation rate than the headline implies, and thus have better spending power than the inflation implies. Regional variations also lower the inflation experience for many consumers. That all supports a soft landing scenario. Recent durable goods price deflation and pressure on profit-led inflation suggest no inflation stickiness…

UBS: Inflation expectations look well-anchored (well that’s certainly good news … if only it can be borne out with this mornings CPI)

Forecasters' inflation expectations little changed, but raised odds of a 2024 contraction Projections for long-term headline CPI and PCE inflation were little changed in today's Q4 release of the Survey of Professional Forecasters. Forecasters surveyed by FRB of Philadelphia expect headline CPI inflation to average 2.4% over the next 10 years, flat from Q3's reading. The corresponding figure for headline PCE inflation printed at 2.22%, only 2bp above last quarter's estimate.

In addition, forecasters anticipate a marginally brighter growth outlook now relative to last quarter. On an annual-average over annual-average basis, respondents expect real GDP to grow 2.4% in 2023 and 1.7% in 2024. Respectively, these projections are 0.3pp and 0.4pp higher than estimated in August's survey. The employment outlook was little changed. However, relative to last survey, forecasters saw an increased risk of an economic contraction in 2024. For each of the four quarters of the year, they wrote down odds of mid-30 percent to 40 percent that negative growth would be recorded.

The quarterly survey is a key report for the Federal Reserve, as it is frequently cited by FOMC participants and its median long-term measure was the intercept of then-Chair Yellen's inflation model in a 2015 speech, Inflation Dynamics and Monetary Policy.

Consumers still feeling a credit pinch, says FRB of New York

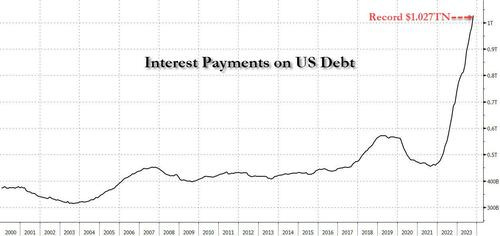

Slowdown ahead The US economy expanded 2.9% over the most recent four quarters, a brisk pace, sustained by the surprising resilience of consumers. Households entered 2023 with more liquid balance sheets than we had estimated at this point last year, insulating them from the Fed's tightening cycle. A year later, however, and lending conditions for households are tighter. Interest payments are a higher and still rising share of household income. Households have undone much of the deleveraging on credit card balances and continue to run down savings buffers built up during the pandemic. We expect households will need to rebalance by spending less. The business sector also faces tougher credit conditions, higher interest rates and margin pressure. As a derived demand, the labor market should cool along with final expenditures. Fiscal impetus looks likely to be weaker next year too.

Barely positive 2024 growth, rising unemployment rate … Inflation moderates faster than the Fed expects in 2024 …

Monetary policy moves from calibration to accommodation …

… And from Global Wall Street inbox TO the WWW,

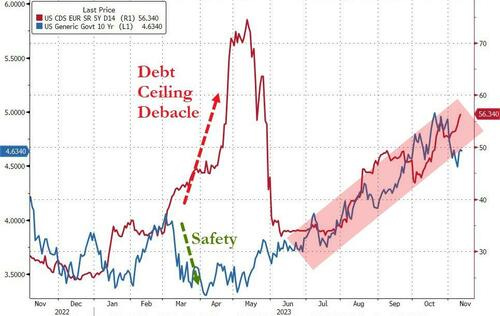

AFR: Bond vigilantes will be back, warns former Fed official (Bill Dudley speaks…)

… But Mr Dudley said the jump in bond yields – to 5 per cent in October from 3.5 per cent in May – simply reflected a shift in views about monetary policy, not funding concerns.

“It’s really about the Fed raising rates by more than people thought and then keeping them higher for longer,” Mr Dudley told the UBS Australasia conference in Sydney on Monday. The fiscal situation is “absolutely terrible” given the economy is at full employment, yet the budget deficit is about 7 per cent of GDP.

“The so-called bond market vigilantes are going to return,” he said. “Markets are going to balk at some point. Whether that happens next week or six months from now or two years from now, I really can’t say.”

Bloomberg: Moody's US Downgrade Shows Why Treasury Yields Are Sticky

… Moody’s itself offered a stark warning with its downgrade by commenting that “interest rates have shifted materially and structurally higher.”

Meanwhile, the possibility of a US government shutdown by the end of this week seems to be growing, but having been used to policy paralysis several times, traders are unlikely to lose sleep over the prospect.

Two-year Treasury yields have surged well more than 100 basis points since May to go past 5% as traders have recalibrated how long the economy can stay resilient.

At the margin, Moody’s action will keep it around there…

Bloomberg: Higher Bond Yields Mean Retirees Can Pull a Bit More From Savings

Morningstar says retired workers can now safely withdraw 4% a year, up slightly from a 2022 analysis.

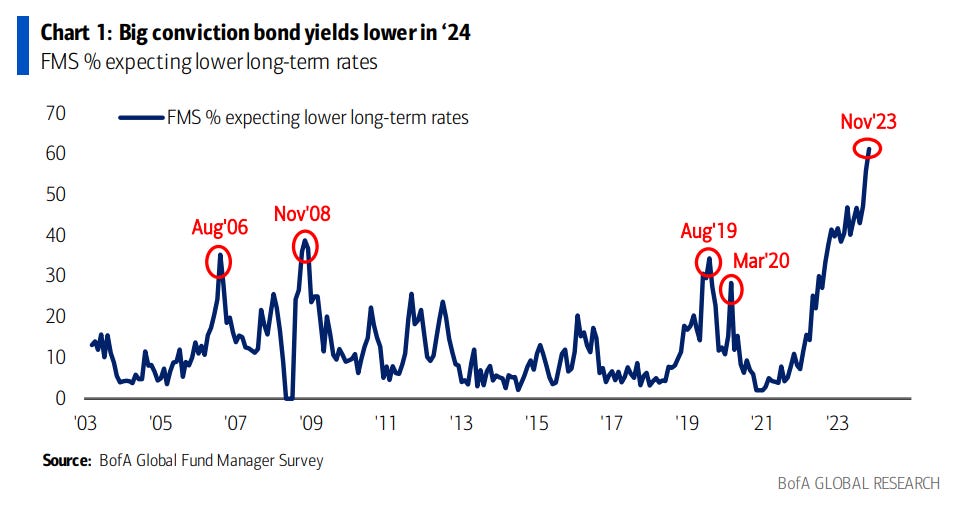

Bloomberg: 5 Things You Need to Know to Start Your Day (lower yields in ‘24)

… Hello and Happy CPI Day. As I've been writing lately, there's been a real shift in consensus toward the view that rate hikes are over and that cuts are now only a matter of timing.

I'll get back to CPI in a second. But first check out this chart from Bank of America's latest fund manager survey. An overwhelming number of recipients see long-term rates heading lower next year.

Ok, back to CPI. The expectation is that, on a headline basis, the number rises just 0.1%, whereas the core rises 0.3%. We've seen the tumble in gasoline prices, which will obviously weigh significantly on the main number. Of course the Fed and markets will look through that to various core and super-core measures that are expected to show a bit more heat.

A chart put together by Bloomberg economists Anna Wong and Stuart Paul shows that while 2023 has generally been a year of disinflation, recent months have shown a halt to the progress made in core measures.

Of course, the month-to-month trend is always going to be a bit noisy. But things could still get a little tricky. After today's number we get one more CPI reading (December 11th) before the next Fed meeting (December 13th). As Omair Sharif of Inflation Insights noted in a recent interview, it's very plausible that they walk into that meeting having seen four straight readings all rising at a faster rate than they're comfortable with. Obviously the data is TBD. And the widespread view is still that the hiking cycle is over, at least for the year. However, there's at least a possibility that things get a bit hairy between now and the end of the year in terms of the pivot and whether the Fed is ready to declare victory. Against a backdrop of the rush into bonds, and high conviction that long-term rates are going lower, there could be some interesting market tension on how things play out.

As for today's number, obviously people are going to slice it and dice it into a numerous different measures. A big thing to watch, as noted by Skanda Amarnath at Employ America, will be the Owner's Equivalent Rent number, which everyone expects will prove to be a drag in the months ahead, but which showed a mini-spike in September. Various market measures of rent have showed weakness in past months, and so part of the question here is the degree to which that shows up more strongly in the official data.

The federal government routinely uses government spending and taxes to help offset the highs and lows of the U.S. business cycle. While government spending typically increases during a recession, the magnitude of the fiscal expansion during the pandemic recession was outsized compared with the average historical pattern. This likely contributed to real economic growth and possibly inflation during the recovery. Over the next few years, U.S. fiscal policy is expected to be roughly neutral, providing neither a tailwind nor headwind to the overall economy.

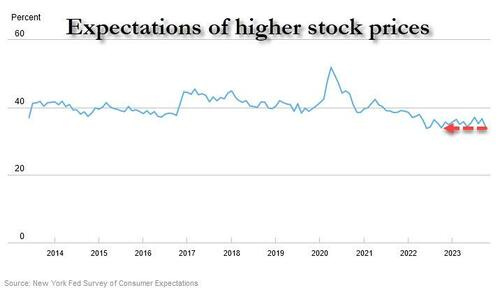

ZH: US Consumers Trim Inflation Expectations, Turn Most Bearish On Stocks In One Year (hmmm, interesting…but not too funny)

… One final notable point is that the mean perceived probability that U.S. stock prices will be higher 12 months from now fell by 2.5% to 34.2%, its lowest level since October 2022.

If this survey is even remotely accurate, it remains the case that for most households (and their generous credit cards) a recession remains far off into the horizon.