(USTs lower, steeper on about avg volumes) while WE slept; CHINA: blowout Q4 data; BoJ next source of global macro risks; "Bonds Over Stocks: The New 60-40 Portfolio" -WSJ

Good morning … Not sure WHY this (simple, sans BBG) view of 30yy slows me down,

Momentum (stochastics — bottom panel — crossing from overBOUGHT extremes) are adding some BEARISH momentum. At the very least, rates will need some TIME AT A PRICE to work that off. That bigger picture somewhat less granular view in mind,

ZH: "A Historic Turning Point": China Reports Blowout Q4 Economic Data As Population Falls For First Time In Decades

… Here is what China's National BS (which stands for Bureau of Statistics of course), reported moments ago for a quarter when Covid Zero was still all the rage (before China mysteriously called time on the worst economic policy of the past three years):

Q4 GDP +2.9% y/y; down predictably from the Q3 +3.9% as zero Covid policies hammered growth for most of Q4 (China was mostly locked down during the quarter), but smashing the estimate of +1.6% and not far from the highest forecast (range -1.1% to +3.5% from 28 economists).

2022 cumulative GDP +3% y/y; also beating expectations of +2.7%; curiously this was unchanged from the estimate of the first 9 months which was also at +3%

Dec. industrial production +1.3% y/y; beating expectations of +0.1%, and down from Nov's +2.2%

Dec. retail sales -1.8% y/y; smashing expectations of a -9% plunge, and a big improvement from Nov's -5.9% plunge.

Jan.-Dec. fixed-asset investment excluding rural households +5.1% y/y; also beating expectations of +5%, and a modest slowdown from the Jan.-Nov. print of +5.3%

Dec jobless rate 5.5%, down from 5.7% in Nov.

… here is a snapshot OF USTs as of 710a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and the curve steeper (5s10s at range resistance again, see attachments) this morning after a data dump from China (links above) and amid high tensions over this week's BOJ decision. DXY is higher (+0.2%0 while front WTI futures are too (+0.3%). Asian stocks were mixed, EU and Uk share markets are modestly lower (SX5E -0.2%) while ES futures are showing -0.25% here at 6:55am. Our overnight US rates flows saw muted activity during Asian hours while our London AM client activity was focused on the front end with decent 2-way flow in 2yrs noted. Overnight Treasury volume was a hair above average (~110%) with 3's and 10's seeing a lion's share of the turnover at ~145% of average volume each…

… Next up we show how Treasury 10's have so far respected resistance (~3.42%) derived from their 10-month-long bear trendline.

… and — SPORTING A NEW LOOK — for some MORE of the news you can use » IGMs Press Picks for today (17 JAN) to help weed thru the noise (some of which can be found over here at Finviz).

Before I head TO the Global Wall Street inbox chock full of narratives, something from WSJ on the NEW 6 0-40 portfolio

… Bond yields rise when their prices fall, however, and the index’s yield has doubled to around 5%—enough that many investment firms are now pushing bond-heavy portfolios.

BlackRock has advertised the unorthodox approach through research reports, podcasts and posts on social-media platform LinkedIn. J.P. Morgan Asset Management has been making a similar push, and the bank’s short-term bond ETF has grown by about 30% over the past 12 months to $24 billion. The fund yields 4.5% after expenses and took in $1.5 billion last month, a record monthly inflow, according to FactSet.

“We’re seeing increased interest recently, and we anticipate that to continue,” said the ETF’s manager, James McNerny. “We think the yield of the fund is likely to go over 5%.”

A good read and not ALL bonds are created equally … From news to some of Global Wall Street’s VIEWS … HERE is a link back to what little I had to offer — a few views of my own intertwined with links to some of Global Wall Streets finest (MSremains a fan of fives and steepeners while BMO suggests, “…For a new trade, we’ll look to 5s/30s and a quickly inflecting momentum backdrop in favor of a larger flattening retracement …)

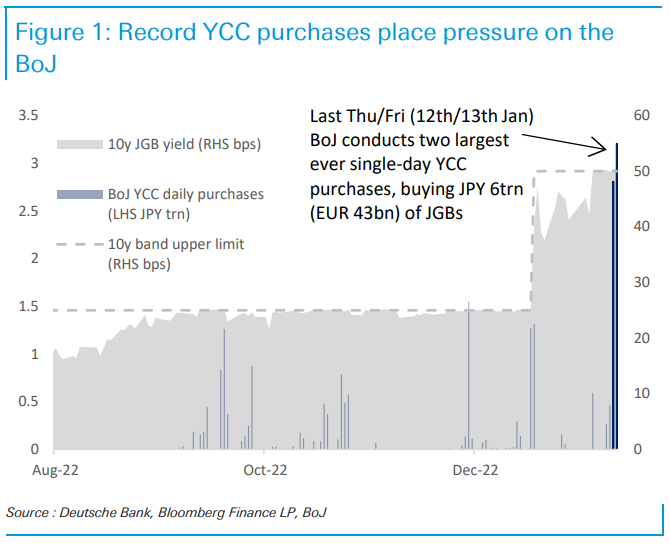

First up, I did NOT realize that last Thurs and Fri (12th/13th) the BoJ conducted 2 largest ever single day ‘control’ purchases. So says DB HERE

The Bank of Japan holds their Monetary Policy Meeting (MPM) on 17th/18th Jan. Our trades for BoJ tightening are Treasury/Bund tighteners, sell OATs vs swaps, higher EUR and USD 5s10s term premium (TP) and higher EUR 10s30s TP. We discuss the broader direction of travel, the recent market pressures, and the best trades for BoJ tightening.

For somewhat MORE on this BoJ risks,

Saravelos: A few thoughts ahead of the Bank of Japan meeting overnight.

1. Don’t be afraid. When the EUR/CHF peg broke in 2015 it was a very large VaR shock to the market. No one was expecting it and the market was very long EUR/CHF. This time, the market has been preparing for an end to yield curve control for nearly a year now. We would argue that the BoJ's huge JGB buying operations since December and the widening of the band are precisely aimed at de-risking the domestic market of stale JGB long positions. In other words, Governor Kuroda has engineered a huge transfer of duration risk from the private to the public sector balance sheet in recent weeks to ensure that the eventual policy adjustment does not become a systemic event. If yield curve control is suspended overnight we would expect global risk appetite to ultimately digest it positively as a major risk event will be out of the way.

2. The best trade is to be long JPY, not short JGB…

3. An end to YCC is only the beginning. We should not assume that a lifting of yield curve control will be the end of Japan’s monetary policy adjustment. The next step will be to start preparing for the end of negative rates with our economist arguing it could come as soon as mid-year. As Japanese investors start returning, the Bank of Japan will have to start thinking about QT as well to provide supply to the market. All of the above should have an even more positive impact on the currency than the current adjustment to back-end yields. Add in all the other JPY positive developments we highlighted in our FX Blueprint, and whatever happens overnight, the direction of travel for yen strength seems strong.

AND now from a different shop — Barclays

Setting up for the BoJ meeting The BoJ's MPM this week will likely be the most important macro development this month. With possible outcomes around yield curve control balanced on a knife edge, we discuss how investors should position going into the meeting.

From Japan right TO China where,

ABNAmro: China slowed in late 2022, but less than expected

China’s economy had 2.9% y/y growth in the fourth quarter—better than expected, but China’s economic data is expected to do better than expected. The composition of the data suggests a declining consumer share of GDP. Generally, consumer-led growth in China is thought to be better quality, so this has signals for trend growth.

China’s population fell in 2022, which emphasizes an important point in international economics. GDP is about how many people a country has, and how hard they work (population growth and productivity growth). Falling populations make negative growth more likely, and that applies to China, Japan, Germany, and Italy today….

Barclays weighs in with good news AND the less good,

Milder slowdown in Q4 GDP, large hole to fill China's Q4 GDP, and December retail sales, IP and FAI were better than expected, assuaging some concerns of significant disruptions to the economy in the reopening phase. High-frequency data suggest the worst has passed, but activity is still well below pre-COVID levels. We maintain our 4.8% 2023 GDP growth forecast.

Bottom Line: The ongoing "exit wave" on the back of China's faster-than-expected reopening has taken a heavy toll on economic activity in recent months, due to surging infections, a temporary labor shortage and supply chain disruptions. Despite continued weakness, Q4 GDP and December activity data broadly beat (low) market expectations. Q4 GDP came in at +2.9% yoy vs. consensus expectation of +1.6%, leading 2022 full-year GDP growth to be 3.0%. Industrial production growth slowed to +1.3% yoy in December from +2.2% in November. Automobile production growth in volume terms fell to -16.7% yoy in December from -9.9% in November. Year-on-year growth in steel product output and cement output both fell into negative territory in December, while power generation growth improved. Retail sales growth rebounded to -1.8% yoy in December from -5.9% in November, but Covid-sensitive catering sales contracted more sharply by 14.1% yoy in December (vs. an 8.4% yoy decline in November) on lower mobility. Fixed asset investment growth rose to +3.6% yoy in December from +1.0% in November on a single month basis. Nationwide and 31-city surveyed unemployment rates both declined in December. It is very surprising in our view that the reported numbers for December were not worse, given the large Covid wave in the month and the fact that many high-frequency indicators were even worse than during the Shanghai lockdown earlier in 2022.

To our surprise, China's economic activity improved in December despite a Covid exit wave that infected a large share of its population, owing to better than expected performance in its retail and services sectors. We estimate China's real GDP growth improved to 1.7% in December from 1% in November. Official Q4 GDP also came out higher than expected at 2.9% YoY, ~1ppt higher than the market had expected.

This suggests China's economy has likely already passed a turning point in Q4 and will strengthen from Q1 onwards. We therefore revise up our 2023 GDP growth forecast to 6% from 4.5% previously. Effectively, the previous upside scenario has now become our new base case.

From a not so close risk TO a more academic risk-related exercise by MSs Seth Carpenter,

Weekly Worldview: A Risk When Peeking at the Peak The Fed's peak policy rate is just around the corner. Globally, the story is roughly similar, but could that view be wrong? Is there a risk that rates go higher?

… We remain convicted in a near-term fall in inflation. Core goods inflation was negative in Thursday’s print. But housing inflation—about 40% of core CPI—stayed high, so we are relying on the fact that spot rents have stopped rising to bring that inflation down in the second half of the year, while other services inflation is not cooling much at all. It is easy to imagine our base case being realized through the end of Q1 with the Fed pausing its hiking cycle, only to find that at midyear, the disinflationary trend grinds to a halt. And if at that point, we get a couple of months of upside surprise to nonfarm payrolls like we have the past two months, the Fed could signal a re-initiation of rate hikes.

Ok SO there’s somewhat more HERE on risks that rates go HIGHER and as something of an offset Goldilocks discusses,

… The global FCI tightening in 2022 is a main reason why growth has slowed sharply in major economies. But because most FCI tightening occurred in 2022H1, our frame work implies that the growth drag in G10 economies peaked in 2022Q4 (-1.1pp annualized rate) and should diminish to under half that in 2023.

We see five additional factors that could limit the drag on activity in 2023. First, the low share of corporate debt maturing in the near-term suggests that companies are more insulated from higher rates. Second, the drag on household finances from higher mortgage rates appears lower than normal because a larger than normal share of mortgages in the US and Europe are locked into low fixed rates, although exposure is greater in the UK and Canada. Third, the extreme imbalance between job openings and available workers should weaken the effect of tighter policy on employment, especially in the US. Fourth, the substantial excess savings accumulated during the pandemic should cushion the impact of higher rates on spending. Fifth, the effects on foreign trade from currency appreciation may be smaller in a global monetary tightening campaign…

… We therefore continue to forecast that no major economy will enter a monetary policy driven recession, and that global growth will run above consensus in 2023.

In this note we want to highlight why we’re still tactically positive on risk assets whilst maintaining our (very) bearish view for H2 2023. This was our view in our 2023 Credit Outlook published back in November (link here) with a further update published last week (link here). However, with markets rallying hard in 2023 so far, it’s worth outlining why the two aren’t mutually exclusive.

In essence, we think that since October we’ve been experiencing a sweet spot for global assets. We’ve passed peak concern about inflation and where rates might need to go, but we haven’t yet reached the likely US recession. In Europe, possible stagnation rather than a near-term recession, and the much lower risk of gas rationing is also helping.

This sweet spot could last until we get closer to the US recession that we’ve long predicted for H2 2023. The timing of that recession is the biggest risk to this view in both directions.

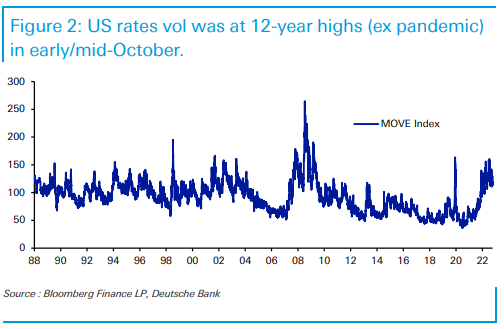

… . Terminal rate assumptions have been very stable as a result, and likely as a function of this, the MOVE index that measures implied bond volatility started to decline from a post-2009 high (see Figure 2) with the exception of a single day at the height of the pandemic in 2020.

Ok, so MOSTLY good news. NOW. Lets NOT worry ‘bout H2 … Unless, of course, yer just wired for worry … like MSs stock jockey who writes,

The Hall of Mirrors Requires a Strong View and Clear Vision Bear markets are like a Hall of Mirrors, designed to confuse investors and take their money. Trust YOUR fundamental process. For us, margins/earnings are likely to significantly disappoint whether there is a recession, or not. We double down on that view today with more evidence to support it.

The Hall of Mirrors…many investors share a bearish fundamental view but are questioning whether it's already been priced into stocks. China's recent reopening push and the precipitous fall in natural gas prices in Europe have provided the narrative to get more bullish, if only tactically. The strong rally in low quality and cyclical stocks has served to support that conclusion as price often causes investors to question their process. Bear markets are like a Hall of Mirrors, designed to confuse us. We advise staying focused on the fundamentals and ignoring the false reflections.

Weaker margins/earnings is our highest conviction call…the spread between our earnings model and consensus forecasts is nearly as wide as it's ever been and suggests a drawdown in stocks for which most are not prepared. The main culprit is the elevated and volatile inflationary environment which is likely to play havoc with profitability. Our negative operating leverage thesis remains underappreciated and will likely catch many off guard starting with this earnings season.

Identifying industry level earnings risk using our heat map...defensive groups screen more attractively. Many of these cohorts have less volatile margins and more conservative forward estimates. Meanwhile, many cyclical groups appear more at risk amid a combination of optimistic EPS estimates, volatile margins, and higher cost vs. sales growth. The higher risk groups represent a large weight (~60-65%) in the S&P 500 in terms of both consensus EPS and market cap.

Macro meets Micro...we held our meeting with lead US analysts and our economists/strategists. Several analysts pointed to a slowdown in hiring/hiring freezes but commented that companies are still trying to avoid large rounds of layoffs. Supply chain bottlenecks have largely cleared, and order backlogs are easing. Visibility on '23 is poor for many cyclical companies/industries. Expense management and operational efficiency remain a focus...

… While the cyclicals/defensives spread is suggesting macro growth is about to reaccelerate, the S&P 500 has simply rallied right back into the resistance thathas defined this bear market all along (Exhibit 2)

As good a chart as this is (as well as others) along with his train of thought,

Hedgopia: With 4Q Earnings Season Underway, Major US Equity Indices Rally Last Week Right Into Make-Or-Break Resistance

Ok, leaving stocks behind attempting to stay in my lane, a few words and visual of a very specific yield curve from BBGs 5 things,

… It's been a good start to the year for risk assets. After getting clobbered in 2022, the S&P 500 is up over 4% so far in January. For the NASDAQ the gain is closer to 6%.

One chart I can't take my eye off, however, is the 3M-2Y yield spread, which is in a deep inversion, signaling that before too long, the Fed's hiking is to turn into rate cuts.

So what are the circumstances that would merit rate cuts? An extremely rapid cooling of inflation. A hard landing/recession? Perhaps. That seems to be one of the big worries at Davos right now. Two thirds of economists polled by the World Economic Forum expect a worldwide recession in 2023. Another poll of global executives conducted by PricewaterhouseCoopers registered its worst growth reading since the poll started being conducted in 2011…

There is NO shortage of good ideas, visuals and narratives ‘out there’ … I’ll continu to try and help connect some dots here in effort to help as YOU plan your trades and trade your plans!