sellside observations from the week that was AND which will be (Jan 16): "Highest Bond Inflows In 18 Months"; updated (LOWERED) rate calls; sell 10s (outright) but then, buy vs...

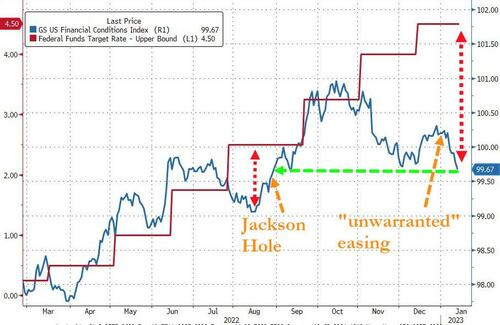

The world and his pet rabbit appear to believe that a 'soft landing' is imminent and 'peak inflation = peak Fed tightening' and so this week saw financial conditions loosen dramatically. This is very much not what Powell and his pals want to see, and specifically warned against "unwarranted easing" in the Fed's Minutes...

The last five days have seen one of the largest 'easings' in financial conditions on record.

Simply put, the market is calling The Fed's bluff...

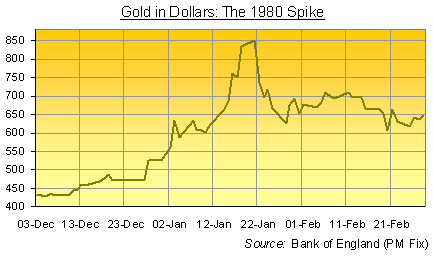

After being released from government control, gold reaches a new record price on January 14, 1980, exceeding $800 an ounce.

That is too far gone … important but digging deep.

HEREis what I was out sayin / thinkin just two years ago — I’m mentioning it because of the demand for long bonds which was visualized then

That was then and this (record indirect bidder just this past week — noted HERE) is now … Ok then … that was then and THEN and this is now. Stocks and bonds soar thanks to bad news being ‘good’ as far as rate hikes go. I hate that ‘anaylsis’ but easier financial conditions would then imply just the opposite.

Perhaps the bond (and other) market isn’t pricing or yet concerned with macro economic outcomes but rather its focused more personal economic ones.

Bonus season is coming and word of job cuts on Global Wall Street abound, perhaps a few good days / weeks and month or so leading UP to these conversations will preserve jobs and INCREASE chance of sharing some of the FICC profits?

DB: Investor Positioning and Flows - Highest Bond Inflows In 18 Months

JPMs VIEW notes, “… The backdrop for Fixed Income keeps improving”

MSon their updated (lowered) RATE forecasts : “… Given these developments, we think Treasury yields are likely to end 2023 lower than our current forecast of 3.50%. We revise our UST forecasts and now see UST 10Y ending the year at 3.15%, 35bp below our previous forecast. We see 2y yields ending at 3.20%, 30bp below our previous forecast of 3.2%. We see the 5s30s curve on a steeper path than our previous forecast.” — stayin’ LONG 5s and in steepeners, fwiw

TD rates weekly recommends having cake (SHORT 10ys outright) and eatingit too (LONG 10s vs short BUNDS) so in other words, no matter WHAT happens, they’ll have some sort of ‘winner’ to help offset and work themselves out of something less winning. Heads they win, tails WE lose (if we don’t listen to them?)

Ok then … After allsellside / global wall street narrativesyou’ll kindly note couple / few things from the week that was, via the internet … First there’s U-MISS-AGAIN,

ZH: UMich Inflation Expectations Plunge To 20-Month Lows

And for the somewhat LESS good (but expected) news (using that term loosely),

ZH: Yellen Warns US Will Hit Debt Limit Next Thursday, Will Take Extraordinary Measures To Avoid Default

For more, check out UBSs Mike Cloherty on the debt ceiling drama in this weekends sellside PDF … Bah humbug!

Back to the GOOD — er, um, ‘news’

ZH: Credit Loss Provisions Soar As Banks Brace For Pain

… What about other banks? Well, as the chart below shows, it wasn't just JPM. In fact, all the Big 4 banks saw their reserve provisions surge, and as shown in the chart below, the total for the 4 largest US banks was $6.2 trillion, which - if one excludes the outlier covid period - was the largest reserve build quarter since the start of 2013.

Other side of the coin …

ZH: Americans Finding It Difficult To Pay Credit Card Dues On Time; Delinquency Rises Amid All-Time-High Interest Rates

…Climbing interest rates are poised to dampen consumption. While easing inflation and strong wage growth have given way to modest gains in real income over the past few months, we suspect consumers will face tougher financial decisions this year as excess savings from the pandemic lockdown days run dry and as borrowing becomes costlier. Separately-released data from the Federal Reserve Bank of New York suggest consumers are already starting to dial back their spending plans. In December, the median household expected their spending one year from now to be 5.9% higher, down from a 6.9% prediction the prior month. Access to credit may be weighing on consumption expectations; the share of households reporting credit is harder to obtain relative to a year ago remained near its series high in data going back to 2014.

I’m having a hard time feeling badly for banks and loan loss provisioning given the rates being charged on what appears to be ridiculous outright NOMINAL LEVEL of REVOLVING …

BANKS ARE — in my extremely UNPROFESSIONAL — not Zoltan Poszar — VIEW going to be just fine.

Oh the gloom and the doom … lets get back on track with some 3d weekend happiness where Dr Ed VIGILANTE Yardeni offers a question,

Last year, we thought that the S&P 500's bear market might have bottomed at 3666 on June 16, when sentiment was as bearish as it was when the index bottomed at 666 on an intraday basis on March 6, 2009. We were wrong. It fell to a new low of 3577 on October 14. We viewed that as a successful retest of the June low.

So far so good…

? Never mind … came across following OBIT from the bond market … one which I believe is particularly important for any / all of us so-called ‘global macro tourists’

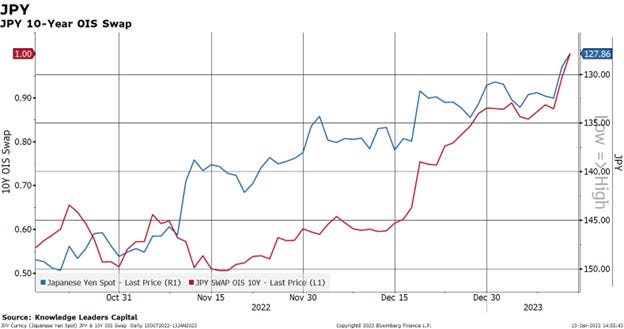

… We are thinking more and more that the YCC as a whole may get scraped in the not-too-distant future. Just today, the FT ran a story “Bank of Japan under pressure over next move as bond yields and yen surge,” writing, “For Kuroda, next week’s monetary policy meeting will be the second to last before he steps down in April. That has fueled speculation that we will end the YCC framework to smooth the transition to his successor.”

As the largest creditor nation in the world, a surging currency and rising JGB rates will likely draw exported capital home and cause some real pain to any carry-trader who has been free-riding on the delayed reaction of the BoJ to the global inflation surge.

Plenty more HEREon Japan, the BoJ, JGB yields and impact on USTs — largely expected to be more muted than middle Dec surprise.

From the death of YCC to a steel caged death match being noted,

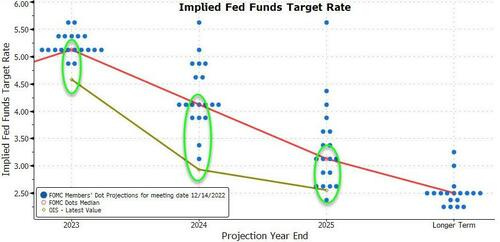

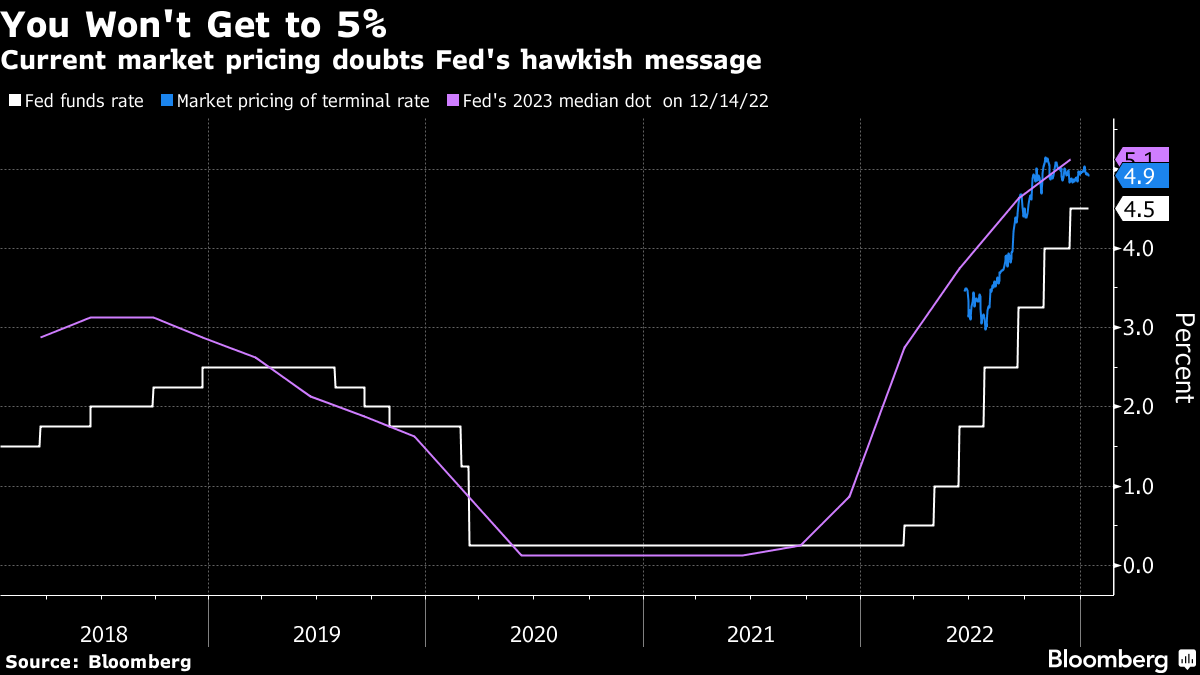

An as-expected cooling in US inflation further fanned the flames of a fight between the market and the Federal Reserve.

Short-dated Treasury yields plunged Thursday in the wake of a 6.5% reading for year-over-year December consumer prices — down from a peak of 9.1% in June — with swaps markets now pricing in a peak Fed rate of 4.9%. That’s out of step with the policy makers’ projections of a destination above 5% — which was reiterated by St. Louis Fed president James Bullard in the aftermath of the data.

So who wins? In the eyes of DoubleLine Capital LP chief investment officer Jeffrey Gundlach, the obvious answer is the bond market.

“My 40 plus years of experience in finance strongly recommends that investors should look at what the market says over what the Fed says,” Gundlach said on a webcast Tuesday. That builds on a tweet he sent last week: “There is no way the Fed is going to 5%. The Fed is not in control. The Bond Market is in control.”

And if we’re listening to the bond market, it’s also worth noting that traders are pricing in about a half-point worth of rate cuts next year in addition to a lower ceiling. Again, that’s at odds with the Fed’s projections which indicate they plan to hold rates through the end of 2023 after reaching terminal.

Perhaps unsurprisingly, Minneapolis Fed president Neel Kashkari thinks you should take the central bank’s side. In a New York Times profile, author Michael Steinberger asked Kashkari about the fact that markets are pricing in rate cuts:

“I’ve spent enough time around Wall Street to know that they are culturally, institutionally, optimistic,” Kashkari replied. I said it seemed almost as if the markets were playing chicken with the Fed. Kashkari laughed. “They are going to lose the game of chicken, I can tell you that,” he said.

We’ll find out soon enough who blinks first.

Why Not Both?

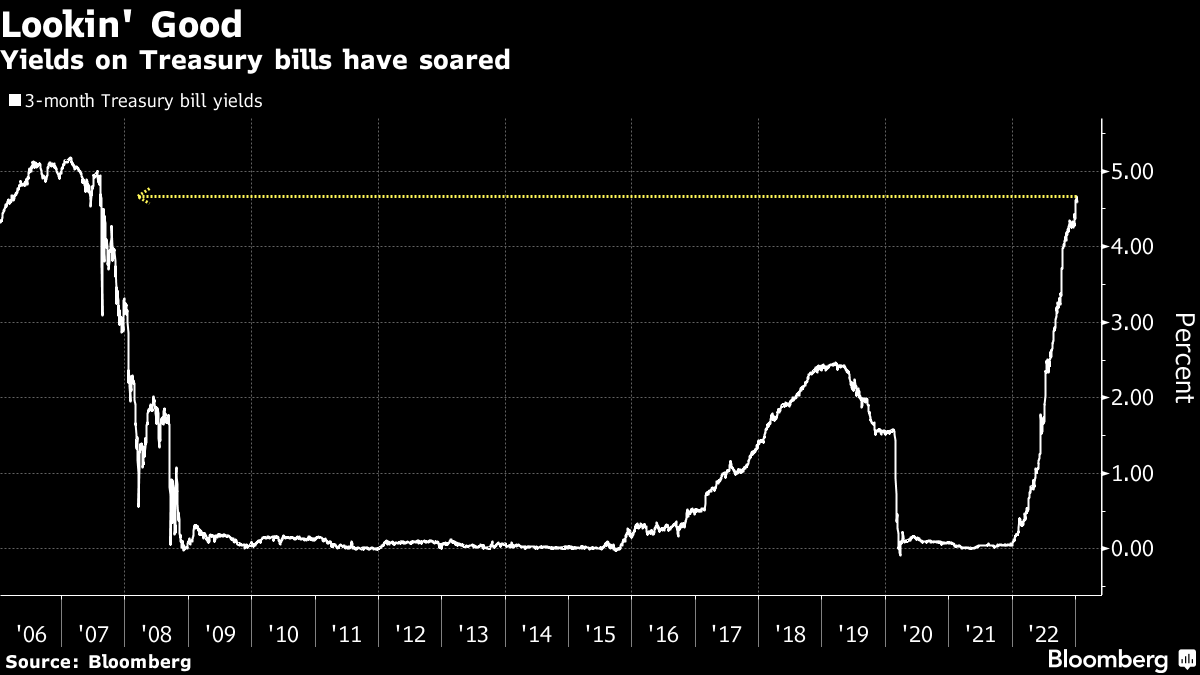

Steady income streams were all the rage in 2022, turning dividend funds into one of the hottest destinations last year. But now that bonds actually offer decent yields, those strategies are facing some worthy competition from the fixed-income market.

“The Fed has been keeping rates very low for an extended period of time, they’re rolling off their balance sheet, we’re probably entering a recession, what does that tell us? I like fixed-income in the short-end,” Kathryn Rooney Vera, Bulltick Capital Markets head of global macro and chief investment strategist, said on Bloomberg Television. “I think that T-bills — 4.6%, 4.7% 3-month T-bill — is pretty attractive when you’re considering that versus the dividend yield in the equity market.”

It makes sense — buying a Treasury bill brings virtually zero credit or duration risk, while even the most reliable dividend-payers in the equity market come with potential earnings upsets and stock volatility.

Should more investors get on board with that view, it could rearrange the leaderboard in the $6.8 trillion exchange-traded fund market. Dividend ETFs took in a record last year, while JPMorgan Equity Premium Income ETF (ticker JEPI) — which employs a call-writing strategy to generate payouts — attracted nearly $13 billion, shattering the annual record for active ETF inflows.

To Nancy Tengler of Laffer Tengler Investments, appealing yields don’t necessarily dim the appeal of dividend stocks — one just has to be choosy.

“The dividend growers will continue to do well because they’re trading on fundamentals, valuation and income stream growth, which you don’t get in fixed-income,” Tengler, the firm’s chief investment officer, said on Bloomberg Television. “The highest-yielding cohort of the equity market — they aren’t raising their dividends very quickly, and that’s usually because they’re trading at a high yield for a reason.”

I’ll spare you ANY attempted view of TERMINAL and whether or not we ultimately get up to / above / near whatever terminal IS (and stay there) as folks jumping on board, buying USTs (and stocks, gold, crypto) and EASING FINANCIAL CONDITIONS, well, would once again bring me back TO earlier point — the easier financial conditions get the more work JPOW & Co. will have to ultimately do.

Or at least die trying to convince THE MARKET it WILL do …

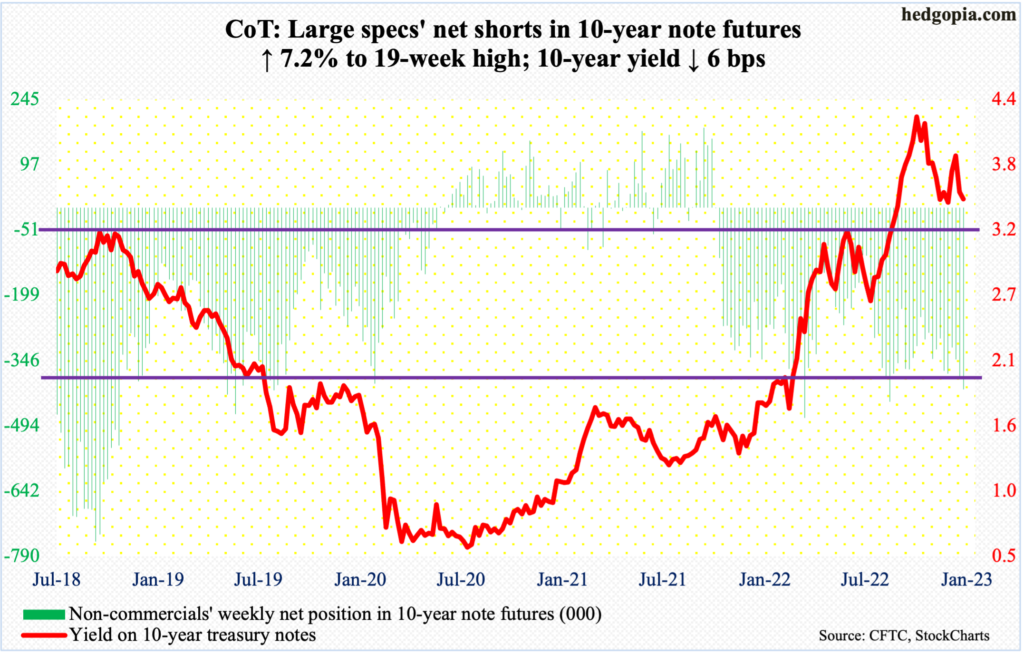

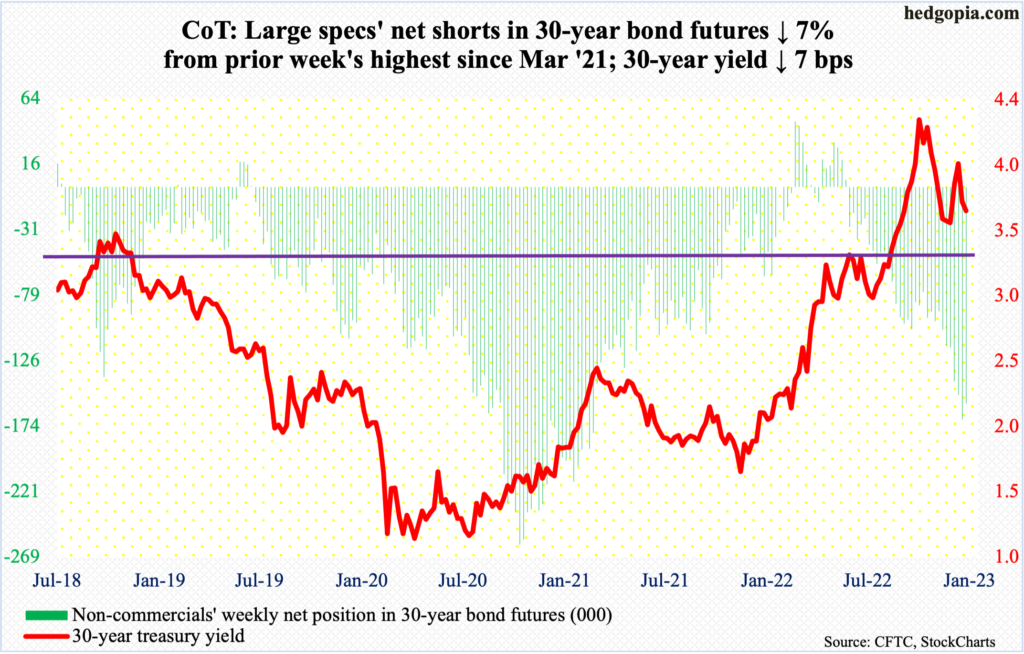

Finally an in effort to wrap this all up and bring back to what matters — think UST POSITIONS (futures) were apparently tidied up ahead of CPI report .. Meaning shorts covered, to some degree.

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

{kind=link}

{kind=link}