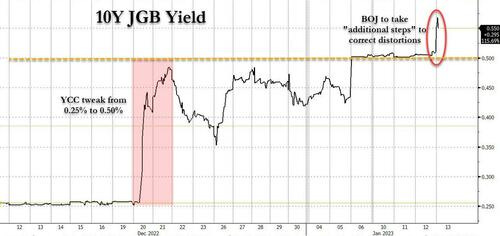

Treasuries are steeper and modestly cheaper after the BoJ failed to arrest a slide in 10y JGBs over 51bps, despite a record amount of (JPY 4.6tn) purchases across regular and fixed rate ops…

For more on this, see Citi just below and / OR,

ZH: BOJ Loses Control Of Bond Market As New YCC Band Breaks Amid Selling Panic

Overnight the Japanese yen soared (if not quite as much as it did last month when the BOJ unexpectedly doubled the trading band of its Yield Curve Control to +/- 0.50% sparking the biggest surge in the Japanese currency since LTCM and the 1998 Asian Crisis), after Japan's Yomiuri reported that the BoJ is to review the side effects of its massive monetary easing at its policy meeting next week and may take additional steps to correct distortions in the yield curve due to skewed interest rates despite last month's tweak in its bond yield control policy. Translation: there is a chance the BOJ will once again "surprise" the market with yet another YCC tweak. The news predictably unleashed a surge in the yen as it would mean outgoing BOJ head Kuroda will need to buy even less bonds, inject less liquidity, and implicitly prop up the currency; as of 8:00pm ET, the USDJPY had tumbled as low as 128.66 from 132 yesterday, before bouncing modestly just above 129…

… Of course, the offset within Japan's impossible dilemma - which as regular readers know states the BOJ can have a strong yen or bond market stability but not both at the same time - is that a stronger yen means not only weaker exports and less inflation (which may be good for Japan now but will be anything but once deflation returns in a few months), but also bond market chaos.

And sure enough, moments after the JGB market reopened on Friday, the 10Y yield soared above 0.50%, rising as high as 0.568%...

... before recovering some losses after the BOJ announced yet another unlimited fixed-rate bond buying operation intended to stabilize the selloff.

There is just one problem: these operations are starting to pile up quite ominously: on Thursday, the Bank of Japan spent ¥2.81 trillion ($21.3 billion) on its fixed-rate bond-buying operation as yields stayed at the upper end of the trading range that it permits. The amount surpassed a previous record high of ¥2.21 trillion set on June 14. And with the BOJ about to go into overdrive it will surely blow another record amount tonight to prevent an all out collapse of its bond market.

… What happens next? Well, if the BOJ is unable to restore confidence to the bond market - and its ongoing strategy has demonstrated it has no idea what it is doing - and it is indeed forced to dump TSYs, sending yields sharply higher, the Fed will have no choice but to once again step in and offset BOJ bond buying. That's right: the Fed may have to restart QE not so much to prop up US stocks but to avoid a bond market rout just as Zoltan Pozsar already predicts that the Fed will have to restart QE anyway (see "A "Checkmate-Like" Situation: Zoltan Pozsar Says Fed Will Restart QE By The Summer Of 2023"), and for a far simpler reason: a massive supply/demand imbalance in the US TSY issuance market this year, once which leads to market chaos and brings the Fed out of hibernation.

At that point, a printing orgy will commence between the Fed and BOJ, one which will inevitably drag in every other central bank, as the new normal race of outprinting everyone else reasserts itself now that inflation is apparently no longer a big concern to the Fed.

I lead with this tidbit of recon as I cannot help but think this may be one of the largest developments end of last year which will impact global macro in 2023. It may be part of what many out there are perceiving to be the NEXT greatest trade of yield curve UN-INVERTING (ie, the steepener).

That said, nothing like a ‘good’ CPI report …

ZH: Services CPI Soars To Highest In 40 Years, Real Wages Shrink For 21st Month In A Row ZH: Stocks, Bonds, & Gold Surge As Rate-Hike Odds Tumble After CPI Decline ZH: "Third Straight Month Of Good News On Inflation": Wall Street Reacts To The CPI Report

… And another way in which Global Wall Street reacted was to ignite a UST buying panic …

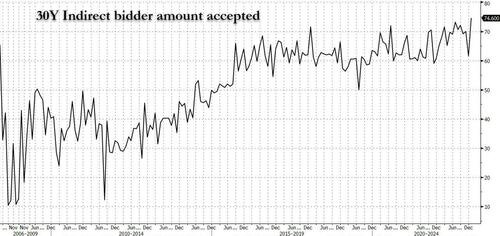

ZH: Record Foreign Demand For Blowout 30Y Treasury Auction Sends Yields Tumbling Across The Curve

… But it was the internals that were blowout, with foreign buyers, or Indirect bidders including central banks, private investors and sov wealth units, awarded a record 74.63%, the highest on record (and far above last momth's 61.57%) as foreigners just couldn't get enough.

… to help spur a bid for … stonks? And bonds … whatever.

Forget that, stocks merely reflecting present value of future cash flows, right?

ZH: Small Business Optimism Slump Signals Profit Margins Poised To Plunge

Profit margins ≠ stock prices … repeat after, oh never mind and … here is a snapshot OF USTs as of 727a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are steeper and modestly cheaper after the BoJ failed to arrest a slide in 10y JGBs over 51bps, despite a record amount of (JPY 4.6tn) purchases across regular and fixed rate ops. The ECB’s Kazak’s also did his best Kashkari impression (‘no rationale for market’s pricing in cuts’) this morning, to little avail from outperforming EGBs (10y German -4bps, 10y BTPs -5bps tighter to Bunds), while market’s continue to digest the post-CPI climate. SPX futures are slightly off at time of publishing (-0.3%), while energy (CL +0.9%, NG +0.9%) remains buoyant amid the technical weakness in USD crosses (DXY broke 103 figure y’day, ADXY has retraced half of 2022 decline). APAC stocks (ex-Japan) caught up to US-risk assets overnight, authorities pledging further property rental support (SHPROP +0.4%, SHCOMP +1%). USTs volumes are running ~130% the 30d ave, with block and cash activity tilting towards front-end selling and belly sector buying (4k in TU sales, 4.5k FV buyer).

… and for some MORE of the news you can use » IGMs Press Picks for today (13 JAN) to help weed thru the noise (some of which can be found over here at Finviz).

From news to some (Global Wall Street) VIEWS you might be able to use,

ABNAmro: Falling US inflation paves way for 25bp Fed hike

Here is a revision TO a view

Barclays: Revisions to our near-term outlook With incoming data on activity and employment continuing to look resilient through December, we are revising up our near-term GDP trajectory in Q1 2023, and maintain our FOMC call for a 50bp increase in the funds rate at the February meeting, followed by a 25bp increase in March….

Which was then followed by a revised revision …

Forecast change: We expect the FOMC to hike 25bp in February In response to the latest Fedspeak and data, we now expect the FOMC to slow the pace of hikes from 50bp in December to 25bp in February. We continue to expect the FOMC to set the peak rate for the cycle at 5.0-5.25%, after two additional 25bp hikes in March and May. These latter hikes remain dependent on data developments…

And here’s a view which reminds ME the bond market which lost one of its all-stars,

GUGG: Inflation Release Adds to Good News for the Fed…and Bonds

… In conclusion, moderating inflation, along with last week’s data that showed labor market pressures subsiding, should give the Fed more confidence the data are moving in their direction and that the need for substantial further tightening is reduced.

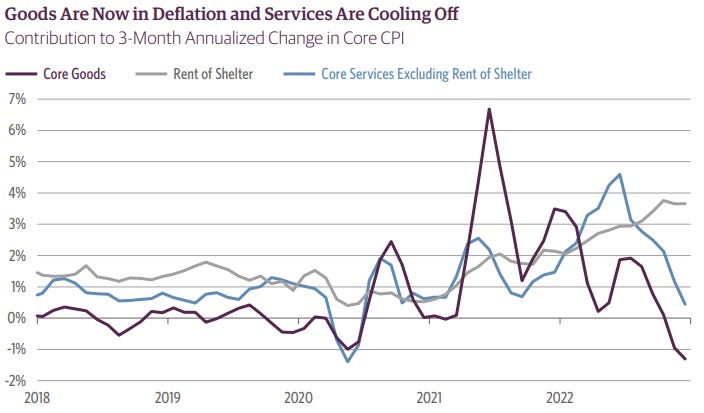

Yesterday’s US consumer price data does not mean inflation is over, but it does signal that the transitory inflation of 2021 is over. The 2021 surge in durable goods demand normalized, and the resulting collapse in durable goods price inflation was stunningly fast. The commodity wave of inflation is fading, and that leaves the profit margin expansion in focus.

Durable goods are now in deflation—this is increasingly important in 2023, as durable goods will have a higher weighting in the calculation of consumer price inflation. The fantasy price of owners’ equivalent rent is the main driver of core inflation, and that means that the cost of living reality for most US households is lower than consumer price inflation suggests—hinting that consumer may be less damaged by inflation this year…

KEY MESSAGES Main takeaway: US CPI data for December showed that inflation is cooling, but the details indicated continued upward pressure in categories where wage-price dynamics are most likely to play out, namely core services excluding rents.

More policy restriction still needed: Wage pressures are moderating, but increases are still stronger than would be consistent with the Fed achieving 2% inflation. With the unemployment rate still at its cyclical low of 3.5%, the risk is that pay gains stay hot.

Changing our Fed call (+25bp in February): Consistent with recent Fed messaging, policymakers are more focused on the level and duration of the peak fed funds rate than the pace of hikes. The latest Fedspeak suggests officials are content to proceed more gradually, even though financial conditions and CPI details point to the need for further restriction. As such, we continue to anticipate a terminal fed funds rate of 5.25%, but we now see the February move at just 25bp.

Changing calls aside, here’s another recap and this one is for somewhat more (less, really as I’m NOT bespoke subscriber) on mkt moves in regards TO CPI

… today’s inflation data was a decisive confirmation of the trend of disinflation (and in many cases outright deflation) that we have seen in recent months. Treasury yields initially popped in response to the in-line print, but the correct read was a result weaker than the top-line numbers. Rates traders eventually figured that out.

The result was a double-digit basis point yield decline across the curve as the two year note yield fell below its recent range; a very strong long bond auction also helped (more on that later).

Three Fed speakers today tried to hold the FOMC party line that just because inflation may be pulling back, the FOMC isn’t going to cut rates. But that’s hard to believe; Richmond Fed President’s claim that he expects inflation to be “more persistent” rings hollow, but St. Louis Fed President Bullard’s view that there is “too much optimism in markets that inflation will fall” explains why the Fed refuses to acknowledge progress.

If they do, rates will plunge and risk premiums will evaporate, sending stocks into a new bull market and credit spreads into collapse.

So the Fed is trying to forestall easier financial conditions by talking tough on inflation even as the data screams out that inflation is improving rapidly. The 34 bps gain in the S&P 500 today understated the positivity of the backdrop that inflation data imparted on markets.

A somewhat less optimistic view via John Authers of BBG

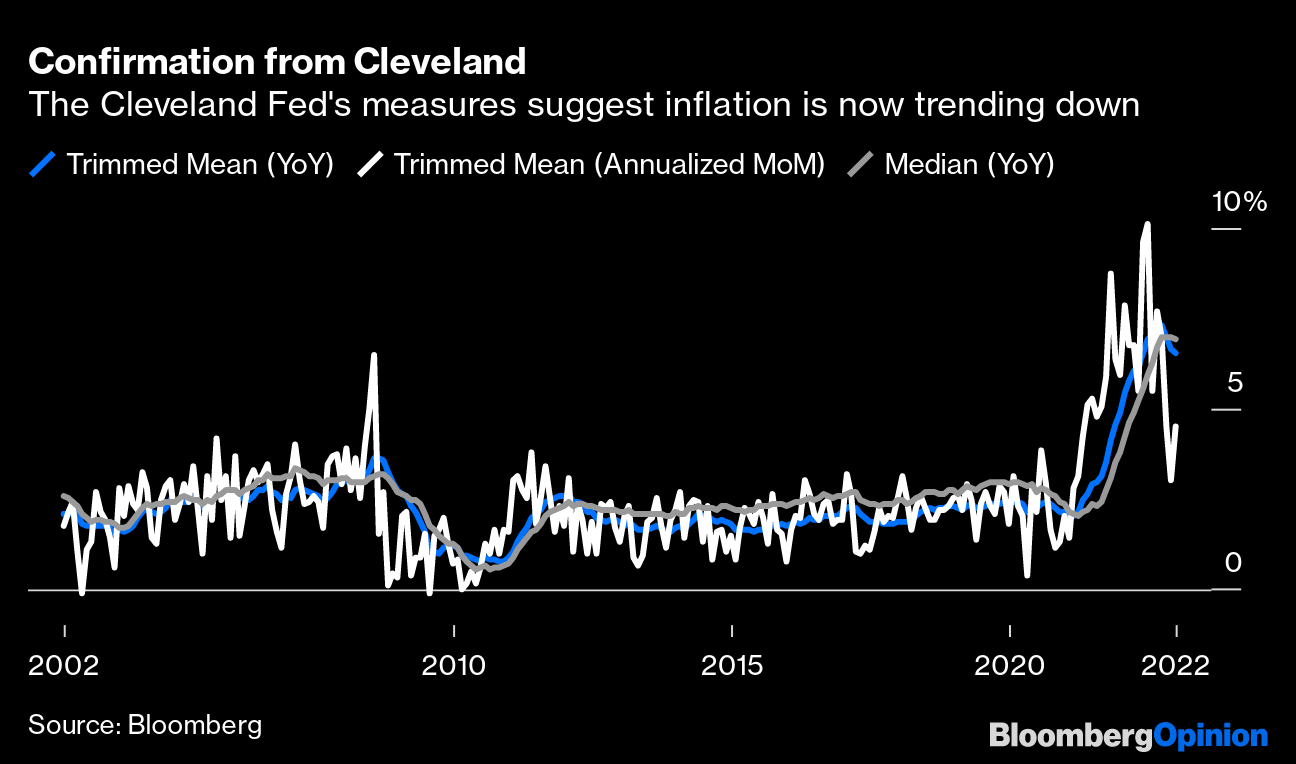

… The Fed’s favored statistical measures for underlying inflationary pressure all confirm a decline, although the fall is less than it appears from the headline data. The Cleveland Fed publishes trimmed mean (in which the main outliers in both directions are excluded and an average taken of the rest) and median series for consumer price inflation. Both have turned down, although not by a lot. On a month-by-month basis, the trimmed mean grew more last month than it had in December, but continues to be at a level that gives the Fed more comfort.

…Meanwhile, the measure that “Team Transitory”adopted in 2021, excluding food, fuel, shelter and used cars (a combination that happened to include several blatantly transitory elements), has also at last started to decline. Its sharp rise since the summer of 2021 turns out to have been another good signal that the inflation problem was spreading:

… Viewed together with prior months’ cooler-than-forecast readings, the December print may indeed pave the way for the Fed to downshift to a quarter-point hike at its next meeting ending Feb. 1. And the Bloomberg World Interest Rate Probabilities function, which derives fed funds probabilities from the futures markets, shows that traders are now almost certain that the next hike will be only 25 basis points. Previously, they had seen the odds as evenly balanced between 25 and 50 basis points:

The growing confidence that Fed tightening is near to its end helped push down Treasury yields, with the two-year US yields tumbling 11 basis points at one moment. Overnight index swaps even suggest a slight chance the central bank may skip a hike altogether in March…

… Overshadowed somewhat by the inflation numbers, Thursday also saw publication of the increasingly followed Atlanta Fed Wage Tracker numbers, which are based on census data and allow a more granular analysis of pay data than the BLS numbers. This showed overall inflation declining slightly, but still above 6% — a level it had not reached in its 25-year history until 2022. But real wage inflation is still negative:

From less optimistic TO Another update comes from a large German bank and as a former bond guy I could have sworn this one was directive for ME personally,

Consumer confidence globally fell to all-time lows last year, more than three sigmas below the long-term average (Figure 1). Business confidence by contrast stayed quite resilient and dipped only mildly. The divergence between consumer and business confidence was even more historically extreme than the collapse in consumer confidence itself. As leading indicators for the global cycle, therefore, the confidence surveys were at odds. In the fourth quarter, however, the gap began to close. Business confidence continued to decline while consumer confidence bounced a little. The convergence has been remarkably synchronous across major economies.

Here’s one for us ‘visual learners’ and our inner technicians — 1stBOS on how / why,

… As we noted in our Q1 Technical Outlook, risky assets have started 2023 strongly and we see scope for this risk-on phase to extend further in the early part of Q1. Key to determining how far this risk-on rally can extend in our view is the outlook for Credit markets, where we see an important turn in many trend following indicators and very well-defined resistance levels close to being broken.

* The US 5yr CDX HY Spread has seen a cross lower in key moving averages and weekly MACD is now negative. This leaves the market very close to crucial “make or break” technical resistance at 417.5bps, below which would complete a large technical topping structure.

In particular, USD Rates Vol has been a key driver of wider Credit Spreads over the past year and as we noted yesterday, we see scope for a material fall in rates vol over the next few months. This should help to further encourage income orientated investors back into Credit markets, especially at more elevated yield levels.

If we do see credit spreads continue to tighten and complete tops, then this would be seen as a further support to the US Equity market. Whilst we have been looking for the S&P 500 to hold below its downtrend from early 2022 and December high at 4101, these resistances would be seen increasingly at risk to a break if Credit Spreads do top out.

US CDX 5yr IG Spreads are already below crucial and well-defined resistance at 73/71.5bps. A weekly close below here would reinforce the turn in trend following indicators and point towards further tightening.

Even if Credit Spreads fail to break the aforementioned levels, we believe the total return outlook for Credit has improved markedly. As we noted in our Q1 outlook, any spread widening should be offset by our bias for falling government bond yields, as market concerns shift from inflation to growth, meaning the total return outlook for IG Credit is neutral at worse…

…and if Credit Spreads do top out, we could see a steady grind higher. With this in mind, the Bloomberg Barclays Corp Investment Grade Index is threatening a clear potential basing structure and is now already above the “neckline” to this base.

Happy 3d weekend ahead — will try to organize something more of an update BUT … THAT is all for now. Off to the day job…