Good morning … USA avoided a shutdown giving boost TO equity futures CONFIDENC (? … and yields) despite / because of short-term nature of the deal AND governance / LEADERSHIP questions in The House chamber, Chinese data mixed over weekend, EZ factories stuck in the mud while Fed shines a path …

CNBC: Stock futures rise LITTLE CHANGED after lawmakers avert government shutdown Reuters: China's factory activity recovery slows in September Reuters: Euro zone factory activity stuck in steep downturn Reuters: Fed shines light on path to US bank capital relief trades

AND here we go. Meet the new quarter, same as the old one where selling of FI seems to be quite a popular theme overnight … 10yy DAILY …

… with not much in way of ‘good’ here to point out — momentum (stochastics) remain overSOLD and can resolve in a couple ways — time at a price OR become SO oversold, cross and higher yields attracting buying resulting in LOWER yields. That does not appear to be any sort of imminent threat (but that’s why ‘they’ are called ‘surprises’ I suppose).

On a weekly (log scale) basis …

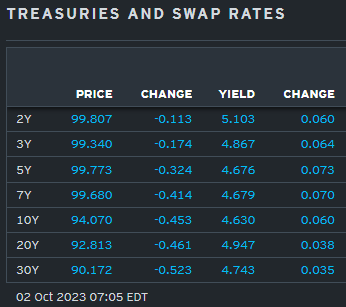

… and depending upon thickness of the crayon YOU choose, there appears to be some level of ‘support’ up nearer 5.00% and then … <gulp> nearer 5.50% … shocking as that may seem. I’ll dazzle with more charts and crayola work at a later time but for now, well … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower after a US government shutdown was averted at the 11th hour while overseas bond markets (back-end Japan notably) remain pressured too. DXY is higher (+0.3%) while front WTI futures are too (+0.8%). Asian stocks ex-China (out for Golden Week until October 6th) were mixed, EU and UK share markets are modestly lower on balance while ES futures are UNCHD here at 7am. Our overnight US rates flows saw a 'risk-on' Asian opening with desk flows seeing better real$ selling in the longer-end. During London's AM hours our activity was subdued with duration pressured with no evidence of dip-buying seen amid quiet volumes there. Overnight Treasury volume was ~105% of average overall…

… Treasury 30yrs could, or should, continue to respect major range support near 4.80% (2.417% the equivalent support for 30yr reals), going forward. In the main, monthly chart you can see how we've derived support near the 4.80% level (range highs 2008-2011) and last week's test of it. Note too in the lower panel that long-term, monthly momentum, while still 'oversold,' guides to higher rates still with bear trends still in place. But the zoomed-in shadow box shows last week's Shooting Star rejection/blow-off(?) of the 4.80% level- a strong hint the level could remain a decent support for 30's having found solid buying/covering there a few days ago. So more tests of the 4.80% support level could be in store coming days..

… and for some MORE of the news you can use » The Morning Hark - 2 Oct 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use (GMOs quarterly, some shops thinking long bond yields to DROP while other shops sticking with LONG 5s and looking to buy 2s on bit more of a ‘dip’ … all noted over the weekend) … here’s SOME of what Global Wall St is sayin’ …

ABNAmro - China - Mixed signals from September PMIs

China Macro: Both manufacturing PMIs above the neutral mark again. Caixin's services PMI weaker than expected.

Apollo - Price of Orange Juice (first Earl, then milk, eggs etc … now this?)

Bad weather has pushed the price of orange juice to the highest level ever, see chart below.

Apollo - US Banking Sector Outlook (from OJ to BANKS … this 139p report worth saving and reading couple / few times)

A portion of the recent rates move appears to be capitulation on the notion that elevated real rates will prove especially damaging to the economy. A loss in US economic momentum can arrest this charge towards ‘higher forever’ rates.

… The recent oil move poses risks to a range of our key macro views; our new baseline supports lowering our EURUSD target to 1.07 from 1.10 for the year end, but we note that this is still above current spot.

CitiFX Techs - As The Sun Rises: Swift, speedy steepening

US 2s10s: … we completed a weekly close above resistance at the 55-week MA, completing a 55-200 week MA setup …

Welcome to Q4 with the markets relieved to see the end of September, and for that matter Q3, after a tough latter half to a quarter that promised a lot after a buoyant July. Henry has just published our monthly and quarterly performance review (see here) but in short, of the 38 non-currency assets we look at, only 11 were up in total return terms in Q3 and only 7 in September making it the worst month of 2023 so far. Some highlights were the +28.5% increase in WTI oil and the +73.5bps rise in 10yr US yields over Q3. 30yr USTs were +83.9bps, the largest move since Q1 2009. The S&P 500 was -4.8% in September and -3.3% in Q3 on a total return basis. YTD the index is still at +13.1% but with the equal weight only up +1.8%, a handful of stocks are providing nearly all the gains. See Henry’s piece for more…

… The damage in bonds has been more severe and more sustained than for equities and you can’t help wondering where the real damage is. You can’t have this much value destruction in bonds without there being some stress somewhere. However, it’s near impossible to work out where exactly it might come to the surface…

… When it came to financial assets, the biggest story of Q3 was the massive bond sell-off, which sent yields up to multi-year highs around the world. For instance, the 10yr Treasury yield ended the quarter up +73.5bps at 4.57%, and at the intraday peak on September 28 it was as high as 4.686%, which we haven’t seen since 2007. Yields moved higher across the curve but there was also a clear steepening. That left yields on 2yr Treasuries up +14.8bps to 5.04%, whilst those on 30yr Treasuries saw their biggest quarterly increase since Q1 2009, with a rise of +83.9bps to 4.70% …

… Which assets saw the biggest losses in Q3? Sovereign bonds: It was the worst quarterly performance for sovereign bonds in a year, with losses for US Treasuries (-3.4%) and Euro sovereigns (-2.5%). The moves mean that both are negative on a YTD basis again.

In a surprise move, House Speaker McCarthy reversed course and brought a “clean” extension of spending authority up for a vote on Sep. 30, after avoiding this course of action for weeks. Now that this extension has become law, federal agencies have funding until Nov. 17. A shutdown at that point is still a clear risk, though we think the odds of a shutdown at the next deadline are lower than they seemed heading into the Sep. 30 fiscal year end …

… The outlook is likely to become at least somewhat clearer over the next several days. The timing and probability of a vote to change House leadership is likely to become more apparent once the House comes back into session on Oct. 2. Over the coming week, we also expect congressional leaders formulate a strategy for moving forward on passing full-year spending bills, though this is likely to take at least several more weeks to complete.

MS - Sunday Start | What's Next in Global Macro: The Market Says Late Cycle; We Agree

Since mid-July, stocks have experienced a distinct change in personality. As noted in prior research, second quarter earnings season proved to be a "sell the news" event, with day-after-reporting stock performance nearly as poor as we have seen in over a decade. In retrospect, this makes sense given weakening earnings quality and negative year-on-year growth for many industry groups, coupled with the strong price run-up into mid-July on extended valuations. Those valuations look even more extended today, with the equity risk premium falling below 100bp to new cycle lows, as both nominal and real interest rates have risen amid supply/demand imbalances and the Fed’s affirmation that it’s serious about keeping rates "higher for longer." …

… Higher rates have pressured growth factor relative performance

MS - The Weekly Worldview: Last to Lift Off (as goes BoJ so goes … global carry trade?)

The BoJ is now expected to lift-off from NIRP earlier than expected. We take a look at the indicators that policymakers may be watching carefully.

The US government shutdown has been delayed—but in the meantime, journalists and (more importantly) economists have had to waste time analyzing this nonsense. The uncertainty the fiscal farce periodically creates also carries an economic cost.

One consequence of the delayed shutdown may be a challenge to House Speaker McCarthy. Investors do not care too much about McCarthy’s fate—the speaker probably gets the same attention as a minor regional Federal Reserve president. But if McCarthy were replaced by someone closer to the far-right, this would reduce any lingering hopes of bipartisanship.

China’s Golden Week holiday is ongoing as the World Bank offers a dour outlook for the Asian economy (with changing global demand patterns and structural change). Be careful what data is used to analyze the economy—in the past, China’s consumers have been eager to take trips, but tended to spend less per person when travelling. It is the latter data that matters most.

Fed Chair Powell is speaking on a round table, and is unlikely to offer any policy insight. Fed President Williams, who is worth listening to, is speaking on climate change. There are some assorted business sentiment polls crying for attention, but like most attention seekers these are best ignored.

UBS - Is the slump in Treasury demand permanent? (important question asked and answered)

Demand for Treasuries has been lower than we anticipated We had thought would be more value buying as real yields crossed 2% and nominal 10s got to 4.25%. But investors seem to have been wary of stepping in as yields have moved to levels last seen before the 2008 crisis.

But we think that this demand slump is temporary rather than permanent Forward yields are pricing as if the demand lull will persist, with the low point in the FF rate at 3.85%…

… And from Global Wall Street inbox TO the WWW,

BCA (via LINKEDIN) with long-term look at long bonds, annotated, and it’s a more bond BEARISH thought than not — ie the move HIGHER not yet done,

… I did so regarding today’s most vital investment question: How far will US bond yields rise, and what are the implications for other financial markets? Our takeaways: · Even cyclical bond bear markets in 1982-2021 ended only after an eruption of financial turmoil. · It would be strange if the current US bond bear market - the largest on record - ended without significant casualties in the global financial system. · In short, US Treasury yields are set to overshoot before topping out. The bear market in US bonds will likely end with a bang rather than a whimper…

AT Charlie BIELLO — finTWITTING best on bond market selloff

… The biggest risk to our optimistic outlooks for the economy and stock market is that the Bond Vigilantes may be about to send a very loud message to Washington: “Cut the deficits or we will raise bond yields until they cause a credit crunch and a recession."

The Wild Bunch has already sent the 10-year US Treasury yield up to 4.59% on Friday (chart). In a matter of three years, they've managed to fully reverse the drop in the yield to historical lows during the "New Abnormal" from the Great Financial Crisis (GFC) through the Great Virus Crisis. Before the GFC, the old normal bond yield was around 4.50% (+/- 50bps). We think that's where it should be now, assuming as we do that inflation will continue to moderate in coming months.

AND happy Monday (said nobody, ever) … THAT is all for now. Off to the day job…

on investment securities for banks, as of 2023Q2")

was thinking maybe a video rather than a name

https://youtu.be/Lo0MIUrrNpc?si=BXJQ_UyBzeU6fEDc

Great work !!!!

Half to agree with the Bond Vigilante's POV..

I'm a Conservative and the Federal Gov't as completely Out of Control.

McCarthy has been Ousted...

We to come up with a Credible Path toward a Balanced Budget, albeit 10 yrs out.

We're staring down 40-45 T in Debt, by 2030.

At what could be 10+% Interest Rate...

People need to regain the "Fear of God" or the Fear of Financial Armageddon...

I support the Bond Vigilantes 100%

Our UniParty Politicians has sold us down the River, while the Media applauds....

Please continue your Fine Work...........IT HAS NEVER BEEN MORE IMPORTANT.

The "Bond Market" is at the Center of the World's Attention.

I take comfort in that in 5.44%, 10 yr Trendline.

I think we're with weeks of a Intermediate Top..

Buyers may try to come in above 5%, but somewhere between 4.75 - 5.25, we hopefully reach

an equilibrium resting point.