Good morning … economy VS banks OR banks + economy = PIVOT (or NO pivot)? While I (we all) continue to noodle the new mathematical equation(s) of our times and in addition TO what little I had to offer over the weekend, an updated look at the 2yy which appears to be leading term structure HIGHER this morning on a very quiet May Day holiday (UK closed),

Momentum is BEARISH while 50dMA is declining (and so, bullish?) and support @ 4.165% … in other words, an economic inkblot test where YOU are free to see and interpret whatever it is you’d like …

… here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and the curve flatter this morning as duration benchmarks begin to relieve some deep 'overbought' readings that emerged late last week (see attachments). DXY is modestly lower (-0.13%) while front WTI futures have built on Friday's rebound (+2.3%, see attachment). Asian stocks were mixed, EU and UK share markets are mixed/higher while ES futures are showing +0.13% here at 6:50am. Our overnight US rates flows were unavailable and maybe that's because overnight Treasury volume was super weak at ~40% of average overall.

… and for some MORE of the news you can use » IGMs Press Picks for today (8 MAY) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

Beginning with one which was noted YESTERDAY morning

It has been an eventful week. The much-debated resolution of First Republic finally materialized, but investor angst around regional banks persisted, resulting in a week of losses – the KBW Bank index had fallen 11% for the week by Thursday. While the resolution was clearly a “an important step toward drawing a line” under banking sector volatility, to quote Fed Chair Jerome Powell, investor fears have not dissipated, with concerns now focused on regional banks’ capital and operating models. The collapse of four US banks in the last few months with over US$500 billion in combined assets is hard to dismiss, especially in the context of a slowing economy, reined in by policy rates that have risen sharply over the last year and capped by this week’s 25bp hike. While the Fed has not signaled the direction of its next move, it "won't cut rates" this year if inflation is in line with its outlook, implying a conditional pause that our economists expect to be lengthy.

In the short term, we will monitor the evolution of borrowings from the different Fed facilities to gauge the extent of liquidity stress in the regional banks…

How these regional banks realign their business models will have a major bearing on overall credit formation in the economy and thus on the markets…

Over the long run, how credit formation through the regional banks evolves depends on the trajectory of bank regulation…

What are the market implications? We expect to see bank demand for Treasuries increase relative to other assets under higher LCR requirements. Both shortening deposit duration and implementing LCR requirements suggest that banks will favor shorter-dated over longer-dated Treasuries. More long-term issuance due to TLAC drives higher long-term yields in fixed income, supporting curve steepeners for Treasuries and credit spreads over the medium term. For longer-duration securities such as agency MBS, these changes should result in less demand from banks and consequently wider spreads, which is our rationale for being underweight agency MBS. Similarly, bank demand for senior tranches of securitized credit, key enablers of credit formation through securitization, will likely remain tepid. Thus, in our view, the volatility in the regional banking sector is likely to result in lower credit formation, due to both lingering liquidity stress and regulatory changes to come. The former is already playing out and the latter is likely to weigh on economic growth over the longer term.

So, wait … what yer sayin is that when there’s known UNKNOWNS, USTs are going to be desired and, for accounting purposes, will make some amount of sense? Throw in to the equation (which many / most are, NOW), the fac they ARE acting as an alternative (RIP TINA), and … oh, yea, 60/40 isn’t dead …

AND moving along TO another note from YESTERDAY morning,

With May likely to be the last Fed hike of the cycle, we think that US yields will be asymmetrically reactive to weaker data.

Debt ceiling risks, weakening macro data and seasonality make Sep VIX call spreads attractive.

We think this will also be the last BoE hike of the cycle and lean short GBP into the risk event.

Seems fairly bening and standard stuff … Those who miss BBG eco team should learn to speak French and / or open trading / investing account for some coverage.

The US Senior Loan Officer survey summarizes the attitude of US banks to lending. While this is just survey evidence, it is conducted by the Federal Reserve as the regulator of banks. As such the responses are more likely to be taken seriously and filled in objectively, than is the case with other surveys. This data matters because lending standards were already tightening, and the recent banking turmoil raises the risk that this tightening accelerates.

US consumers have been dependent on credit and savings to prop up spending. Tightening credit standards would, with a lag, limit the ability to spend. Lower income households would be hurt disproportionately, increasing divisions in an already divided economy…

In as far as some research directed at those who generally are funding source OF the borrowing and, you know, the funders OF the business cycles (at least the positive portion of said cycle),

Renewed stress in the banking system has renewed interest in potential policy support for banks. However, the obstacles are the same as they were nearly two months ago when the failure of Silicon Valley Bank and Signature Bank first raised these issues.

The main focus is deposit insurance. While only Congress has authority to increase the $250k limit on FDIC deposit insurance, the Treasury’s Exchange Stabilization Fund (ESF) has the financial capacity to backstop deposits. The Treasury has authority to engage in a wide variety of financial transactions via the ESF and, in theory, the Treasury could probably use it to structure a deposit insurance program.

However, the political hurdle to using the ESF to back deposits would be high…

The FDIC recently recommended expanded deposit insurance for business transaction accounts, but notwithstanding emergency Treasury action, this would take an act of Congress…

… Regulators might revisit restrictions on short-selling bank shares. The authority to take this step is fairly clear and regulators used it temporarily in 2008 to prohibit short-selling the shares of nearly 1000 banks. However, the benefits are questionable—in 2008, it appears to have briefly supported bank shares but reduced liquidity—and for now a move along these lines looks unlikely, particularly as a stand-alone solution.

Oh no, not again?? I cannot imagine and hope never to see an imposition of rules where a free market is no longer free … one cannot sell short shares of a company one deems fit to lose. The binary choice, in theory, is a very personal one, no?

And speaking of a PERSONAL choice, it is yours whether to continue reading here or not and it’s a personal VIEW which comes next … not mine but a view of the world from MSs chief econ Seth Carpenter,

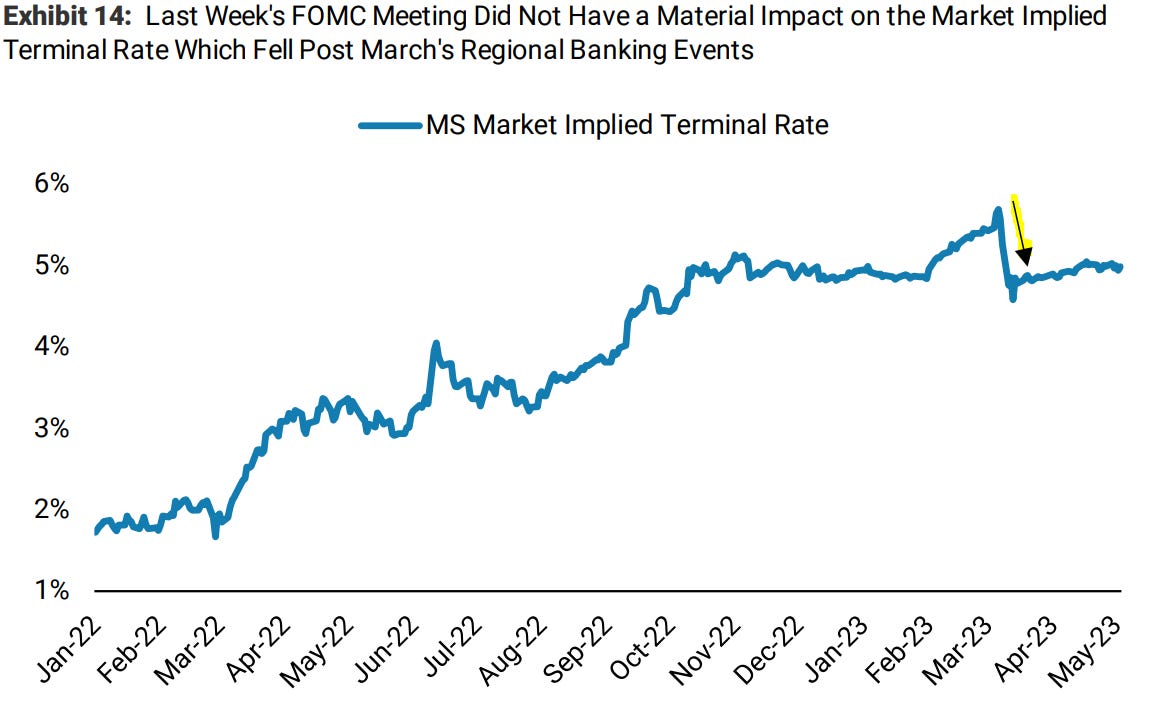

The Fed decision was in line with our expectations, but now starts the hard part - navigating a pause. We look at the global central bank landscape to frame the data dependency that will dictate policy decision making in coming months.

… We expect the Fed to hold rates at these levels for the rest of the year against a backdrop of weak economic growth and elevated but declining inflation. But the examples of Australia and Brazil highlight the need for contingency in communication. When the FOMC said “the extent to which additional policy firming may be appropriate” they were trying to be hawkish if needed but not too hawkish, much as I discussed last week.

Exhibit 3: We expect the Fed to hold rates for the rest of the year

For another input on economics, the latest hit by John Authers’ of BBG is written for you IF you,

… The two-year inflation breakeven (derived from the difference between inflation-protected and fixed-income bonds) suggests that inflation will average almost exactly 2%, the Fed’s official target, into the first half of 2025. It’s worth remembering, though, that breakevens can be wrong, particularly in the bizarre conditions created by the pandemic, which have made fools of us all. This chart shows the two-year breakeven and the actual consumer price inflation number with a two-year lag, so at each point it compares the bond market prediction with the actual outcome. The peak in inflation, above 9%, came almost exactly two years after breakevens had suggested that there would be outright deflation by that point:

The almighty shock of Covid-19 has made it very easy to be wrongfooted, so there’s no necessary embarrassment in this. But with the shockwaves still moving through the system, it seems odd to bet with quite such confidence that inflation will be back under control two years hence.

… The Fed has a mandate to maintain full employment, and conventional measures suggest we’re there at present. It’s hard to see much reason to expect rate cuts from this. Meanwhile, the labor market is impacting inflation through wage increases, which put pressure on corporate costs while raising demand. Average hourly earnings rose by almost 0.5% month-on-month in April, which is right at the top of the normal range (the following chart excludes the two or three extreme months from the pandemic in 2020 for legibility). This isn’t evidence of a terrifying “wage-price spiral”; but it certainly doesn’t suggest the Fed will feel comfortable to relent on rates any time soon:

As for the very short term, there’s very little anticipation of a significant decline for inflation when the April numbers are revealed Wednesday. Both the Cleveland Fed’s “Nowcast” and the average respondent in Bloomberg’s survey of economists expects core CPI to be virtually unchanged. A big drop would validate the current rate calls — a surprise in the other direction might be harder to deal with:

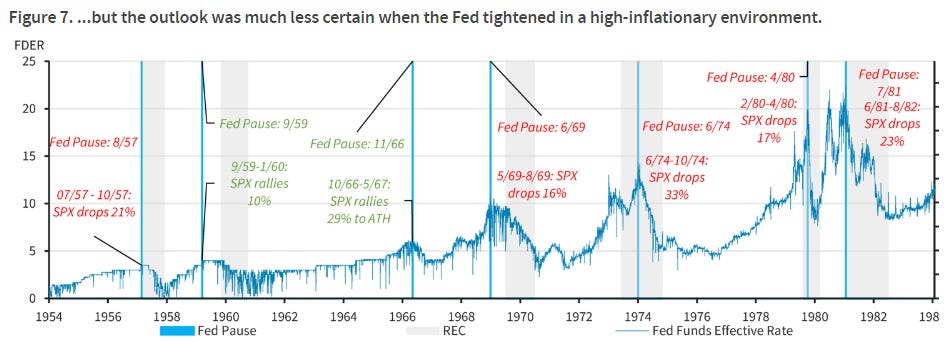

For another hot take and directed at us all — PIVOT / NO pivot folks, Dr Ed makes a great point,

Yardeni: Hard to Have a Hard Landing When Employment Is Growing

The S&P 500 rallied on Friday following yet another stronger-than-expected employment report. In his press conference on Wednesday, May 3, Fed Chair Jerome Powell observed: “It’s interesting [that] we’ve raised rates by 5 percentage points in 14 months, and the unemployment rate is 3½% pretty much where it was, even lower than where it was, when we started.” On Friday, we learned that the unemployment rate fell to 3.4%, matching its lowest rate since May 1969 (chart).

It's true that the jobless rate has always bottomed just before or at the start of recessions. However, it is showing no signs of bottoming so far. During April, nonfarm payrolls increased 253,000 m/m and 4.0 million y/y to a new record high of 155.7 million.

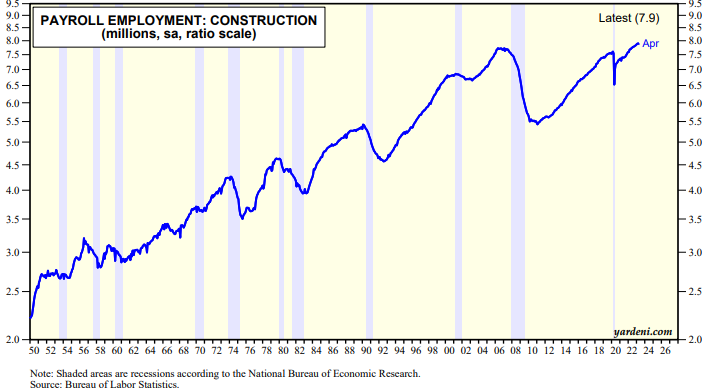

The economy has been experiencing a "rolling recession" since early last year. But you wouldn't know it from the employment numbers. Notwithstanding the recession in the single-family housing market, construction employment rose to a record high in March and April (chart).

While the rest IS behind that paywall, the point IS — I think — clear.

Now with THAT in mind, a couple VISUALS from today’s Chart of the Day.

Better than expected earnings guidance continues to roll in, but a 2H '23 EPS rebound is contingent on a solid macro backdrop. This week, we further explore this theme, highlighting leading EPS surprise and margin gauges as well as our latest AlphaWise Consumer Survey.

… We think it's worth pointing out that falling inflation implies that pricing power is beginning to erode for corporates. Exhibit 9 shows PPI on a year-over-year basis against the NFIB "Percent of Businesses Planning to Raise Average Selling Prices" series. Note the strong relationship over time and the fact that PPI growth is falling in line with pricing power intentions more recently. In Exhibit 10, we then show the NFIB pricing power series versus S&P 500 sales growth—top line growth is likely to slow further if pricing power fades. This is likely to be true for a cohort like the S&P 500, in particular, which is heavily exposed to discretionary goods from a revenue and market cap standpoint—the subcomponent of inflation that's slowing at a more notable pace.

…Over the past several weeks, we've flagged the idea that equities appear to be discounting rate cuts but without the growth downside. In contrast, the rates market appears to be pricing in rate cuts because of growth downside risk following the regional bank events in March. In Chair Powell's press conference last week,he pushed back on the likelihood of rate cuts given the Committee's forecasts—"if that forecast is broadly right, it would not be appropriate to cut rates,and we won't cut rates." While equities faded after the press conference, they closed the week flat relative to where they were into the meeting. In other words, the equity market continues to expect the best of both worlds—rate cuts and stable growth. We view the likelihood of both of those outcomes playing out in concert this year as low given that resilient growth implies a tight labor market and stickier inflation, dynamics that likely would not prompt the Fed to cut rates in 2023. As a reminder, our economists do not expect rate cuts in 2023. In contrast, in the event deteriorating growth conditions do prompt the Fed to cut rates this year (which,again, is not our economists'view), that would likely be risk off for equities anyway from a tactical standpoint. The bottom line from our perspective is that equities are priced for an optimistic and lower probability outcome on this front.

One last note on stocks — a large UK shop relaying which 5 questions its clients are asking

Barclays: U.S. Equity Insights: Five Questions We're Hearing

We address a few key issues that have been top of mind for investors, including upcoming catalysts, how equities will react to the next phase of Fed policy, what's been behind the recent multiple expansion, unusual calm in equity volatility, and how best to play the current environment.

What will be the likely turning point to break the market higher or lower? Markets have handled a series of risk events with remarkable composure; well-hedged positioning and responsive policymakers make it unlikely for a tail event (absent a true liquidity crisis) to substantially derail equity values and break the market lower. Trough earnings are a reasonable catalyst to break the market higher but we don’t think we are there yet given the deteriorating macro backdrop.

When is the Fed likely to start cutting and how will equity markets react? Rates and equities are pricing divergent outcomes in 2H23 Fed policy. We view the “higher for longer” outcome as more likely and also as the lesser of two evils, as the Fed is unlikely to cut this year unless responding to a fairly severe recession or liquidity crunch, which obviously does not bode well for equities.

Based on our client conversations, the buy side is probably closer to our $200 EPS estimate, but if that’s the case why are equities rallying?

Why is equity volatility so low and what does that say about risk?

How do you play the current environment? Recent choppiness in Tech and Financials highlight individual sector risks in a late-cycle environment dominated by macro uncertainty and tightening credit. We think thematic plays offer better risk/reward, preferring Large-Cap to Small-Cap, less-expensive Quality names, stocks with high sensitivity to services PCE and US companies with revenue exposure to China.

In the end, I’m not sure WHICH equals a pivot or rate CUTS other than something of a shock to economies / markets which we’re clearly NOT priced for. Markets APPEAR to my now very unprofessional view, to be very much at peace with CUTS and so what isn’t priced is continued STRENGTH economically speaking (and so, the ‘flation).

Treasuries short Leveraged funds supercharged their bearish Treasury bets to record levels in the week ending May 2, according to the latest available data from the Commodity Futures Trading Commission. That was just days before the US banking turmoil took a turn for the worse, spurring a rally in Treasuries amid bets the Federal Reserve would soon pause its tightening cycle. Sentiment flipped again after Friday’s better-than-expected jobs data, however. Some of the positions may not be due to the rising popularity of the so-called basis trade, a strategy where investors buy cash Treasuries and short the underlying futures — pocketing any difference in pricing…

Interesting … some food for thought as we know when folks on one side of the boat, well, it tips. POSITIONS were noted / mentioned over weekend and I should quit while I’m behind and so … THAT is all for now. Off to the day job…