Good morning … Lots written about and declaring OF victory with regards to inflation and the DE or DIS inflating theme of 2023 this past weekend and now folks will have to deal with this,

… Additionally, less than two weeks after slashing its 2024 Brent price target from $100 to $94, Goldman done a full 180, and late on Friday raised its 2024 Brent forecast back to $100, and 2023 oil price target to $95 (from $90, and from $95 previously).

Nine members of OPEC+ announced today a surprise "voluntary" collective output cut totaling 1,66mn b/d which will take effect from May till the end of 2023.

As we have argued, OPEC+ has very significant pricing power relative to the past, and today's surprise cut is consistent with their new doctrine to act preemptively because they can without significant losses in market share.

As we already assumed that Russia cuts would extend into 2023H2, we are lowering our OPEC+ production end-2023 forecast by 1.1 mb/d. Incorporating this significantly lower OPEC+ supply, slightly lower demand, and the modest French SPR release, we have nudged up our Brent forecasts by $5/bbl to $95/bbl (vs. 90 previously) for December 2023, and to $100 (vs. 97) for December 2024.

Full STOP … asking for a friend … would someone PLEASE advise how it is possible for ZH to charge you for research of Goldilocks?

Oil Comment: Surprise OPEC Cut; Increasing Our December 2023 Brent Forecast by $5 to $95/bbl

BOTTOM LINE: Nine members of OPEC+ announced today a surprise "voluntary" collective output cut totaling 1.66mn b/d which will take effect from May till the end of 2023. As we have argued, OPEC+ has very significant pricing power relative to the past, and today’s surprise cut is consistent with their new doctrine to act pre-emptively because they can without significant losses in market share. As we already assumed that Russia cuts would extend into 2023H2, we are lowering our OPEC+ production end-2023 forecast by 1.1mb/d. Incorporating this significantly lower OPEC+ supply, slightly lower demand, and the modest French SPR release, we have nudged up our Brent forecasts by $5/bbl to $95/bbl (vs. 90 previously) for December 2023, and to $100 (vs. 97) for December 2024…

I am generally speaking, NOT a fan of SURPRISES and yet, we’re waking up TO one whereby OPEC+ announced production cuts of ~1.16m barrels per day and so, there should then be NO surprise which direction of travel bond yields are headed out of the starting gates here early on in Q2..

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve modestly flatter after quarter-end inflows morphed into selling on the surprise OPEC supply cut announcement over the weekend. DXY is UNCHD while front WTI futures are sharply higher (+5.3%)- though well-off earlier highs. Asian stocks were mostly higher, EU and UK share markets are mixed while ES futures are showing here at 6:30am. Our overnight US rates flows saw a sleepy Asian session after yields opened ~5bp higher, flat-lining on listless flows into the London crossover. We're too early for flow color out of London but overnight Treasury volume through 6:30am NY time was ~65% of average overall with 30yrs (96%) seeing the highest relative average turnover so far this morning...

… Treasury 2yrs, monthly: Scraped by on this one where we needed a Friday close <4.032% to confirm a bullish Outside Month. We barely got that close (BBG says it was 4.025%) but do note in the lower panel that long-term momentum finally confirmed a new long-term bull signal at Friday's close after being chronically and deeply 'oversold' over the past year of hikes and QT. The skew of long-term risks (next 6mo to 24+ months) looks bullish for 2's now.

Treasury 30yr yields, monthly: Bonds needed to close below ~3.50% to confirm a bullish Outside Month and that didn't happen for them or any of the other duration benchmarks besides 2yrs. That said, 30yrs and all the Treasury benchmarks from 2's out to the bond all confirmed bullish monthly momentum flips (lower panel, circled). The idea here is that since the spring of 2020... bond sellers have largely had their way (save for 2H 2021; the 'transitory' inflation months) until now. And now it looks like bond buyers are beginning to dominate price settings.

… and for some MORE of the news you can use » IGMs Press Picks for today (3 APR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS (in addition TO what was noted HERE … over the weekend):

First a bit of GOOD news on the ‘flation front from UBS

The oil cartel OPEC announced a one million barrel per day production cut (an announcement is not the same thing as reality). The oil price has risen in response, and at the moment is back to where it was 20 days ago. At these levels, energy prices remain a disinflation force, as the price is significantly lower than it was a year ago.

The other question: what happens to energy demand? This is driven both by the level of growth and the energy intensity of growth. The risk of a more dramatic US slowdown after the banking turmoil is important. Deposit churn seems to have faded, which might imply less need to tighten lending standards, and gives very tentative grounds for optimism.

Other disinflation forces at work—more of the US PCE deflator is below 2% annualised growth. However, with profit-led inflation, those sectors with pricing power are being more aggressive than in a normal pricing cycle, keeping the headline inflation rate above normal.

Business sentiment polls are due. The Japanese Tankan was slightly weaker—capital spending plans are subdued. The US ISM manufacturing survey comes with the normal health warning associated with surveys (the question asked is not necessarily the question answered), and the risk of political bias.

(perhaps this all is WHY nOPEC surprised the markets with that CUT IN PRODUCTION?)

Whether or not it’s INFLATIONARY or DISINFLATIONARY might very well be THE question of the day / week / month or QUARTER just ahead. Perhaps it’s more simple as to WHY. Bloomberg,

OPEC+ has stepped up to do exactly what cartels do, protecting prices with a surprise production cut. The implications for oil prices are probably far greater than for inflation, and by extension, shouldn’t be read as a turning point for rates. Nor is it a definitive recessionary signal of demand slowing in the wake of bank failures.

The organization announced a cut of more than one million barrels a day, abandoning previous assurances that it would hold supply steady. Describing this as either a shock or a risk to global growth seems a stretch. Consensus for oil prices rises as the year progresses -- particularly on China demand -- was the base case anyway.

The median Brent forecast among oil watchers was for the price to climb to $90 a barrel in the fourth quarter and our Macro View column at the start of the year argued that any temporary price weakness would lead to production cuts. More to the point, recent signs were that supply remained relatively tight -- with Brent remaining in backwardation and Goldman Sachs global head of commodities Jeff Currie arguing investors should buy the dip on Friday.

The point is that a recovery in oil prices was already widely expected. As such, the knock-on implications for inflation and rates should be limited, beyond short-term reactions. And the recent price action that prompted the intervention was more a reflection of macro traders getting nervous on US growth than it was of weakening demand.

Moving on from the surprising UN / DE / DIS inflationing and TO a few other items in the inbox … Next up will be a few words on stonks … MS asks,

What's the Message? With major stock indices holding up in the face of deteriorating growth and liquidity, we think the underlying message from broader markets is still defensive. The bigger question for investors is whether large cap tech fits that bill and can it continue to hold the S&P 500 up

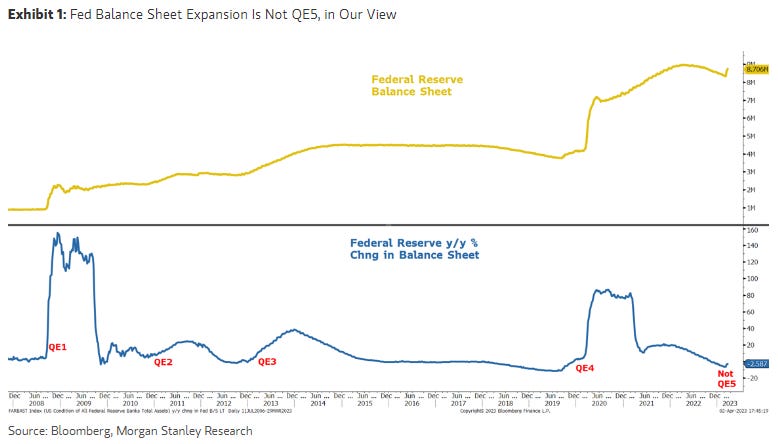

Recent increase in Fed balance sheet is not QE, in our view...Many investors believe the Fed's recent intervention to stabilize the banking system is the beginning of the next QE program. However, not all reserves are created equal and it appears to us like the velocity of money this time is more than offsetting the increase in the Fed's balance sheet. As a result, Money Supply (M2) growth is still decelerating and is now the lowest in at least 60 years. If this doesn't reverse, broader growth should soon follow in a way that is not priced into many equities.

Message from Mr. Market is still defensive...With the yield curve re-steepening sharply over the past month and regional bank stocks acting risk-off even after the Fed/FDIC intervention, we think investors should continue to position portfolios more defensively and focus on companies that exhibit high operational efficiency and high quality of earnings (high cash flow relative to reported earnings and stable accruals). We see little evidence that a new bull market has begun and believe the bear still has unfinished business.

Is tech defensive?...With tech's relative performance back to historical highs, we've fielded an increasing amount of client questions on whether tech is a defensive sector that belongs in the same conversation as staples, utilities and large cap pharma/biotech. Our work suggests it's higher beta and more pro-cyclical than the traditional defensive areas of the market. We also observe that tech's relative outperformance may have been aided by the perception that the recent increase in bank reserves is stimulative for risk assets—a dynamic we don't ultimately believe to be the case.

Same firm but from office of head economic thinker,

The Weekly Worldview: Marking Our Outlook to Market Two key themes from our Year-Ahead Outlook remain strong: we expect Asia to have the strongest growth, and the US and Europe to be weak, but not falling into recession.

… In contrast, we have nudged down our already soft forecast for the US for 2023—a tenth slower growth this year to 0.3% Q4/Q4. Developments in the banking sector have very probably caused credit conditions to tighten, and we are asked why the effect is not bigger. Funding costs for banks are higher and the willingness to lend is almost surely lower than before. But that restriction in loan supply is coming at a time where we were already expecting material slowing in the economy, and therefore, falling demand for credit. So, the net effect is negative, but banks' willingness to lend matters less if there are fewer prospective borrowers.

Where does all this leave us? The EM versus DM theme we have been highlighting continues, and if anything is stronger. The China reopening story remains solid, and the US is softening. Within DM, stronger growth within Europe compared to the US is notable both for its own sake, and because it will likely mean ECB hiking will look closer to the Fed’s hiking than was thought three months ago.

AND from a large shop from across the pond,

U.S. Equity Insights: Where We Stand 1Q earnings season is just around the corner, and equity markets remain improbably optimistic about EPS growth even as rates markets seem priced for a recession. We see plenty of room for consensus to catch down to our 2023 EPS target. Among sectors, we are cautious growth, and selective among defensives and cyclicals.

AND if you are still looking for, want or NEED more, HEREis what was compiled and sent yesterday