Good morning/noon/night (please choose one depending upon where you reside and whenever it is you maybe stumbling across this spot on the intertubes … I’m gonna be real quick this morning …

Don’t Look Now, But Bond Seasonality Is Turning Bullish The summer months tend to deliver stronger-than-average returns for bonds.

I know I know … it’s gonna be DIFFERENT this time … More on the quarter ahead as we wake up tomorrow and have at Q2 at our doorstep, I’m going through my inbox here and NOW for some of what Global Wall St is sayin / thinkin’ and ultimately, SELLIN and I thought this recap from Barry Knapp of Ironsides worth a mention,

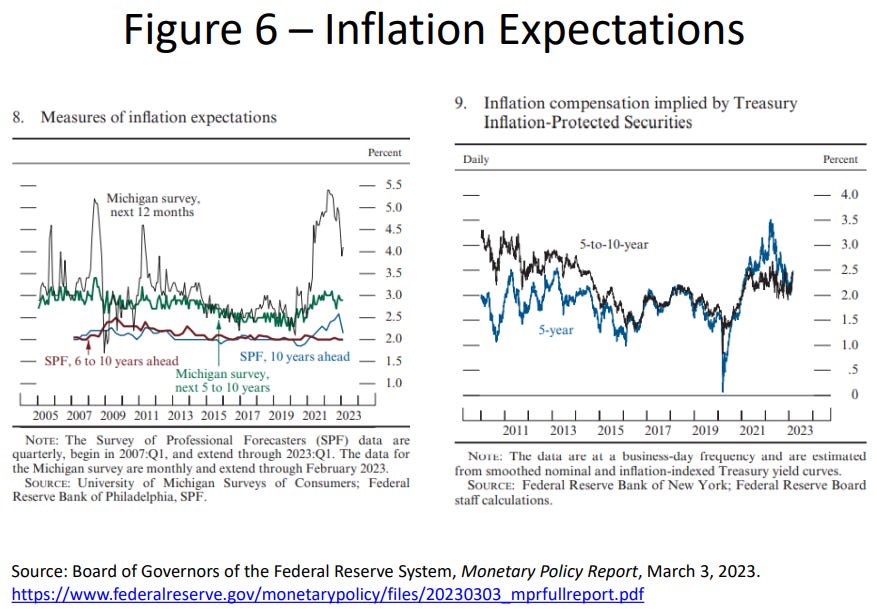

…As a glimpse of year-to-date performance, the S&P 500 +7%, 2-year UST yields -40bp, 5s -43bp, 10s -41bp, a parallel shift lower, and investment grade and high yield CDX spreads tighter by 6 and 21bp, is what we expected despite the Fed’s overreaction to distorted January data that triggered the banking crisis. The 2s10s breakeven curve is 39bp inverted from flat at year-end ‘22, the Fed 5y5y forward breakeven inflation (long-term market expectations) is 2.27%, little changed in 1Q23, and household inflation surveys eased in 1Q. Markets and the public are on board with the disinflation theme.

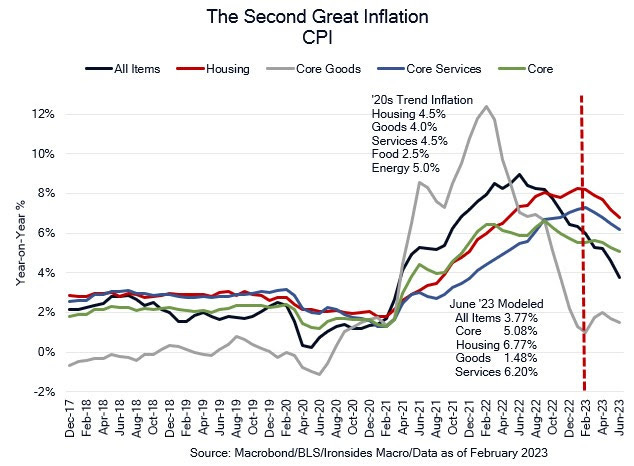

The upshot is that nothing that occurred in 1Q23 dissuaded us from our conviction that the central theme of 2023 is disinflation, but there is no viable path back to sub 2% trend all items CPI or PCED. Deglobalization and the most expansionary federal government outlays and deficits outlook since the ‘60s and ‘70s implies trend inflation above 3%. The best we can hope for is a low standard deviation of inflation, like the ‘90s when CPI averaged ~3.5% with an annual standard deviation of 40bp.

Lets go TOnarrative creation machine known as Global Wall Street. This weekend you’ll be greeted by lots of funtertaining narratives which — like opinions — are said to ALL be created equally. SOME, however, are more equal than others and so I’ll leave you with this — a visual from MS on what is next in global macro, a note which greets you with,

…We think risk/reward is poor for global equities relative to high grade bonds, and remain underweight the former and overweight the latter. From here, we believe risky assets would prosper in a scenario of better-than-expected growth, rather than even weaker growth with easier policy. Asia ex Japan, the one region where we see growth strong and accelerating this year, should be a relative outperformer.

AND there’s plenty more …

Moving right along and in addition TO Global Wall Streets ‘official’ narrative creation machine which again, follows the price action (are you catching the message here?), there are a few OTHER things / LINKS to some items from the intertubes I will spend some more time with ahead of this evenings market open …

First up a CHART (of the Day),

Chart of the Day: Decision time -- Dow Jones Chart since 1900 (Inflation-Adjusted)

Dow at a critical juncture … right, OK. Got IT. Which way MIGHT it go? Well, to not answer directly, I’ll turn to Dr. Ed BOND VIGILANTE Yardeni who recently noted,

The Fed has the banks' backsides covered. The Fed can't insure deposits, but it can guarantee that the banks have access to plenty of liquidity to meet deposit outflows without having to sell securities from their bond portfolios at a loss as happened to Silicon Valley Bank (SVB), forcing it into receivership on March 10 . The banks are required to put up bonds as collateral for their Fed loans, but the bonds are priced at par rather than at depressed market values.

In the past two weeks through the March 22 week, banks' borrowings jumped by $570 billion to$2.52 trillion (chart). Borrowings by large and small domestically chartered banks r0se $266 billion and $300 billion over the latest two weeks!

We can track the activity of the Fed's liquidity facilities by simply subtracting the central banks securities holdings from its total assets. From Wednesday, March 8 through Wednesday, March 29, this figure rose by $386 billion to $830 billion (chart). The Fed flooded the banks with liquidity to extinguish the banking crisis fire.

AND … I’ll spare you the balance sheet laid on top of stocks or more falsehoods (?) like that…which way might the Dow go!? Cannot WAIT to find out what next…

IF one was going to keep digging, though, one MIGHT find this chart from KIMBLE of particular interest …

Econoday’s Consensus Divergence Indexes moved higher on net in the week to indicate that global economic data are exceeding projections at an increasing pace. Emerging strength in Japan, outstanding strength in Canada and especially acceleration in China are key positives for the global outlook. Evidence of a credit squeeze tied to banking failures has yet to appear; concerns seem to be fading before they developed. Another key positive is moderation underway in many inflation readings, at least headline readings that reflect declining trends for oil and gas. Yet core readings are showing less if any moderation, a fact that the European Central Bank will not overlook.

Finally as this portion of the programming comes to a close AND in the case you are having any troubles at all sleeping at night (hey, if you’ve made it THIS far you’ve really got issues — which is why I like you), central planners speaking and so, I’m reading,

… My topic tonight is “The Unstable Phillips Curve.”1 This is not intended to be a deep academic analysis but rather to present some thoughts for discussion. I know that I am walking into the Phillips curve lion’s den, given the number of researchers in the Bay Area who work on Phillips curve estimation. But in my current job, I am used to people disagreeing with me.

The Phillips curve, a relationship between price or wage inflation and some measure of economic slack, has been the foundation of monetary policy for decades. A common way to estimate it is to look at output price inflation and the unemployment rate. One theory, or story, is that as aggregate demand increases, labor demand will increase as well. As a result, prices of goods and services will rise and firms will hire more workers, as long as there is some stickiness in nominal wages. Consequently, this story implies that the unemployment rate will fall. So, there is a negative relationship between price inflation and unemployment.

Another story, based on the New Keynesian model, is that monopolistically competitive firms set prices for some period of time. Firms may have “sticky prices” because of menu costs. That is, firms face costs to adjust their prices and so choose to reset their prices only when the benefits outweigh the costs. Because firms are not identical, only a share of firms adjust their prices each period. So, when aggregate demand increases, firms with set prices agree to supply the goods demanded at their current prices. Firms that find it worthwhile to adjust their prices will increase their prices. As a result, inflation will arise from the firms that adjusted their prices. Meanwhile, higher employment will come from the sticky price firms, and, implicitly, higher employment goes along with lower unemployment. Once again, we obtain a negative relationship between output price inflation and unemployment. The slope of this relationship hinges on the fraction of firms adjusting their prices in response to the aggregate demand shock. Put another way, the frequency of price changes determines the slope of the Phillips curve.

… To conclude, it may not surprise you all that I like story number two a lot better. But we will need more data to conclude which story is right—which is what a datadependent central bank does to implement appropriate monetary policy. With that, I will stop talking, and I look forward to a robust discussion with lots of good arguments telling me I am wrong.

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

")