Yesterday, I was asked where ‘rates will be at years end’ and this conversation was largely focused on the front-end — say 2yrs and IN — and I had to admit I didn’t really have a good GUESS. As the conversation wore on, I had to pick a side — heads or tails — and thought rates were likely to remain more elevated than some who are betting on rate CUTS might think.

Said another way, I suppose I’m leaning WITH those (evil specs) who are SHORT 2s, at least for now and with so many cross currents (dealin’ with the ceilin’, historic pace of rate HIKES, rapid decline of the supply of money, ODL, liquidity conditions), well, plenty of reasons to pause and consider …

Lets jump right in and rip the bandaid off this morning and get to it. As the clowns in DC are both the arsonists AND the firemen (IMO), well, here we go again

For somewhat MORE (including cursory USA CDS visual and SNARK, see ZH HERE). Said another way,

The GOOD news is, welp, we’re 2 fer 2 in as far as good auctions go,

ZH: 5Y Auction 2nd Best On Record Thanks To Painful Short Squeeze, Near Record Foreign Bid

Hmmmm I seem to recall at least a passing mention of positions (short) this past weekend (HERE) and there’s absolutely NO way to connect dots to short squeeze or foreign bid for 2s and now 5s with whatever MAY or may NOT happen with 7yy a bit later on today and so,

Momentum remains overSOLD and this can resolve by a sideways trade (time at a price) and / OR a bullish cross if, lets say, something were to ultimately ‘break’…

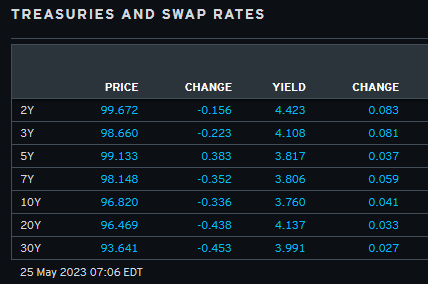

As we await further guidance … here is a snapshot OF USTs as of 706a:

AND … HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and the curve is flatter this morning after a ratings agency put the US' AAA rating on watch for downgrade (link above). DXY is higher (+0.15%, see attachments) while front WTI futures are lower (-2%). Asian stocks were mostly lower, EU and UK share markets are mixed while ES futures are showing +0.6% here at 6:50am. Our overnight US rates flows saw better real$ buying (intermediates) into the early Asian dip before 'heavy' fast$ selling in the belly was seen after the London crossover. Overnight Treasury volume was ~95% of average all across the curve (10's the leader at 122%).

… Our next attachment of 30yr Treasuries shows their 3.985% to 4.05% support band and, like 2yrs and the other duration benchmarks, deeply 'oversold' short-term momentum (lower panel) hints of a crowd of [probably in-profit] tactical shorts. A bull momentum turn could come at any time; best to wait for it to emerge as the late February experience shows that momentum can stay pinned at oversold levels for a while and many BPs... At least that's how we're approaching things.

… and for some MORE of the news you can use » IGMs Press Picks for today (25 MAY) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

First a link thru to web in light of recent FOMC MINUTES …

ZH: FOMC Minutes Show "Some" Fed Officials Push For More Hikes, Sees "Mild Recession In 2023"

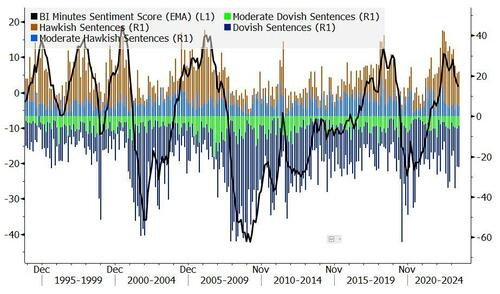

Bloomberg's Ira Jersey says the BI Fed Minutes Sentiment Indicator showed slightly more hawkish and dovish sentences, causing a slight dovish move in the exponential moving average compared with the March meeting.

AND for somewhat more detail ON said FOMC MINUTES,

The May minutes provided useful color about the divergent views recently expressed by participants regarding the extent of additional policy firming that will likely be needed. In our view, there is potential for upcoming decisions to deviate from our pause baseline, depending on the evolution of the data.

AND from that UK based shop we then turn TO France (OR BBG 2.0),

BNP - End of hikes in sight for ‘several’ but ‘some’ favor more

KEY MESSAGES

The minutes of the 2-3 May FOMC meeting seemed intentionally vague in describing the split between policymakers favoring an end to rate hikes (“several”) versus those calling for additional restriction (“some”).

Policymakers generally saw downside risks to growth and upside risks to inflation, amid a backdrop of only mild easing of tight labor conditions. However, there was significant concern regarding the forthcoming impact from both previous rate hikes and the fallout from ongoing stresses in the banking sector.

More recent Fedspeak has recast the debate around the June policy action as a choice between a “hike” or a “skip” instead of a “pause”. In our view, this is a more forceful tightening bias compared to merely pausing, as it leans with more conviction to future action.

We continue to anticipate a pause at the June meeting; further, we expect deteriorating economic conditions to obviate the need for additional restriction later this year. However, we cannot rule out the prospect that upside surprises in economic data—particularly the labor and inflation prints—might spur Fed officials to re-engage with further rate hikes. The risk of re-engagement appears greater than a quick pivot to cuts, in our assessment.

BOTTOM LINE: The minutes to the May FOMC meeting noted that the extent to which further monetary policy tightening was appropriate “had become less certain.” While “some” participants noted that additional policy tightening would likely be needed given the slow progress on returning inflation to the FOMC’s target, “several” participants noted that “if the economy evolved along the lines of their current outlooks, further policy firming after this meeting may not be necessary.” The Fed staff continued to expect the economy to enter “a mild recession” later this year, while FOMC participants expected below-trend growth in 2023. Participants once again characterized inflation as “unacceptably high,” and participants commented that the declines in measures of core inflation had been slower than they had expected. Since the FOMC’s May meeting, the Fed leadership, including Chair Powell, have emphasized that monetary policy is restrictive and that risks to monetary policy have become more two-sided, consistent with our expectation for a pause at the FOMC’s June meeting. But consistent with the divisions noted in the minutes, Fed officials have voiced a range of views on the near-term policy outlook.

For another view,

ING: Federal Reserve splits highlighted by May FOMC minutes

The minutes to the 3 May FOMC meeting when it hiked rates by 25bp echo the comments we have been hearing from officials. "Some" members clearly think there is more work to do to constrain inflation, but "several" think they may have already done enough. The market pricing of a 30% chance of a June hike seems fair, but volatility looks set to continue

I could continue but … would then risk MORE hitting the UNSUBSCRIBE button. But hey, lets remember, you get what you pay for?

Nvidia — noted in the title — was simply put there to catch our collective attention. Did it work? Nvidia shares surged over a quarter after its earnings smashed estimates and it issued guidance for higher sales than expected due to AI chip demand.

That is the extent of it and so … finally, a couple charts / links for us visual learners and fans of the techNOwizadry,

Kimble: Nasdaq Reaches Important Technical Price Resistance!

AND with some prices AT RESISTANCE, here’s a look at mojo,

Momentum picked up steam for the S&P 500 last week until overhead resistance came into play at 4,200. Stocks have once again struggled to surpass this hurdle, although it shouldn’t be too surprising given the ongoing debt ceiling drama in Washington.

While last week’s rally wasn’t enough to clear resistance, it was enough to flip the Moving Average Convergence Divergence (MACD) indicator back into a buy position.

What is the MACD? MACD combines momentum and trend following into a single indicator and, as the name implies, is based on convergences and divergences between a long- and short-term exponential moving average (EMA).

How does it perform? Historically, MACD buy signals have generated above-average returns, with a relatively high frequency of positive returns occurring across most timeframes over the following year. Returns tend to improve when buy signals occur when the S&P 500 is trading above its 200-day moving average (dma)—as was the case last week.

Sell signals on the MACD indicator are not as ominous as they sound, as they tend to produce below-average, but still positive, returns when the S&P 500 is trading below its 200-dma.

#Got7s? Get those bids in early and often and … THAT is all for now. Off to the day job…

Asking for a friend: Is there Momentum without Mo' MONEY? As in Mo' MMT-QE? Funny coincidence that rising 14 year channel arrives with the advent of 2009's initial launch of QE. And stock buy-backs later. I'm sure it's all 100% natural organic growth of course!

Asking for a friend: Is there Momentum without Mo' MONEY? As in Mo' MMT-QE? Funny coincidence that rising 14 year channel arrives with the advent of 2009's initial launch of QE. And stock buy-backs later. I'm sure it's all 100% natural organic growth of course!

I can't see Rate Cuts in 2023....

Could be 2 more Rate Hikes in 2023 ???? 50-50% chance