Good morning / afternoon / evening (please choose whichever one which best describes when ever is is you are stumbling across this weekends note.

I’d like to being by once again extending a warm welcome to all who’ve recently stumbled upon this spot on the intertubes and with deep gratitude sent out TO the folks at Harkster.com (and the WEEKLY HARK — HERE).

I’m grateful to Harkster folks as well as you all slowing down to read and occasionally reply. I appreciate any / all dialogue, comments and criticisms …

Keep yer friends close and as far as the enemies, well, they’ve already hit UNSUBSCRIBE so, to heck with ‘em!!

I’m continuing along my way here and am still not 100% certain as to WHY OR how this all works, to be clear.

I’m doing this to VENT and as way to kid myself into thinking i’m still ‘marginally attached’ TO fixed income markets which I continue to love.

Yes, its true.

I love bonds MORE than they ever loved me.

That said, I have gathered a few links / excerpts from Global Wall Street’s inbox and this weekend I’d highlight,

Barcapon USTs and “The Liquidity Question” Citi(tech) — 2yy — lower long term BUT … some levels to watch NOW

JPMsBUYIN BELLY MSsMike Wilson continues hatin’ stocks, lists several reasons he’s wary of rally AND econOqueen (Zentner) lays out a “Roadmap TO a JUNE HIKE” and finally, head of global MACRO (Hornbach) remains LONG 5s TDsBUYIN BELLY SocGENremains SHORT BELLY (via 2s5s10s as ‘rallly seems a bit overdone for now’

AND MORE… Global Wall Street cannot WAIT for a turn of events in DC which then changes ALL the facts and forced global macro RETHINK as narratives of yesteryear (last week) become outdated and irrelevant and this as the ink hardly dry…

A quick recap AS far as what happened Friday, well in all the noise, there was a few things to note,

ZH: "They're Just Unreasonable": Debt Ceiling Talks Collapse As Republicans "Abruptly" Walk Out Of Negotiations

and then there was this,

ZH: Bank Stocks Puke As Yellen Reportedly Warns Of 'More Mergers' Ahead

And moving along then TO a few OTHER links which I found funTERtaining and which you might too … and SO in case you missed,

… This all might be problematic if inflation was also reaccelerating—but today’s signs suggest the opposite. Taking a cue from last week’s U.S. CPI report, shelter prices finally seem to be slowing, the Fed’s “supercore” core services ex-shelter measure (which is closely tied to the labor market) saw its softest gain since last July, and outside of used autos, core goods inflation saw its slowest pace in over two years.

Better growth with cooling inflation is a “chef’s kiss” backdrop for stocks. A closer look suggests it’s not all just tech, either. Almost 80% of S&P 500 companies reported earnings that were better than expected (the highest beat rate since 2021 and above the 10-year average), and estimates for earnings in the year ahead are broadly increasing. There are also 35 companies in the S&P 500 that are currently within 1% of their 52-week highs, and only five (Alphabet, Apple, Microsoft, Meta and NVIDIA) are in the mega-cap tech category.

In all, it’s now been over seven months since the S&P 500 hit its lows back in October—that tends to mean the lows are in, and it also tends to bode well for future returns. When the S&P 500 has made it seven months or more without a new low in the past, it’s been higher 86% of the time over the following year.

This much time without a new 52-week low has historically implied that the lows are in

JPM should then out to read Mike Wilsons reasons to be ‘wary of current rally’ ?

Moving away from stocks and looking at USTs — specifically TBILLS

WolfStreet: Six-Month Treasury Yield Begins to Price in One More Rate Hike

The US housing market is currently experiencing a downturn, with home prices declining in 75% of major cities. This article examines the distribution of these price declines, compares them to past downturns, and discusses the duration and magnitude of the current correction.

… Summary In summary, the US housing market is in the middle of an ongoing downturn, with prices declining in 75% of cities. The declines are not evenly distributed. Some cities are showing substantial declines before any significant crack in the labor market, which is concerning, but some cities have only just seen the momentum slowdown without any sizeable reductions in price.

Where the housing market bottoms in relation to past economic downturns remains an open question, but there is no debate that the market hit a clear peak in 2022, and the broad momentum remains to the downside.

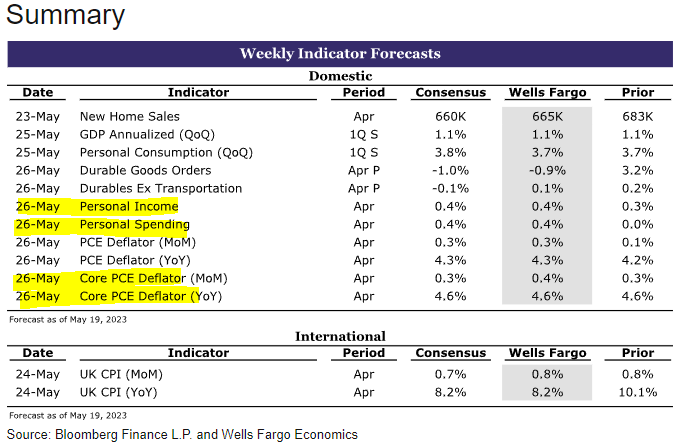

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

… THAT is all for now. Off to enjoy what’s left of the weekend but first some chores and weeding to do!!

AND we’ve reached the point of this note where I’d like to offer my sincere gratitude and condolences for anyone who has managed to make it this far … (h/t BMOs Ian Lyngen and his gang for putting out terrific weekly podcasts, Macro Horizons which I enjoy via Google HERE)

… THAT is all for now. Enjoy whatever is left of YOUR weekend …

You definitely deserve to be showcased on the weekly Hark! You provide great insights daily on my personal favorite asset class fixed income. Along with sharing research from the Street which I really enjoy reading and otherwise wouldn’t have access to. Thank you for the great newsletter!

You definitely deserve to be showcased on the weekly Hark! You provide great insights daily on my personal favorite asset class fixed income. Along with sharing research from the Street which I really enjoy reading and otherwise wouldn’t have access to. Thank you for the great newsletter!