Good morning … 2yy down 30bps from yesterday afternoon CHEAPS (just north of 5.06%)?

Um okie dokie … The GOOD news is Bank of Japan left things unchanged » interest rates and yield curve control » in Kuroda’s final meeting, ALSO says output and exports are now “moving sideways” rather than increasing. Um … that’s not good.

Speaking of NOT GOOD … while I’m no banking expert (among large list of other things I’m NO expert on) but … You down wit SVB (Yeah you know me) …

Ok, well, a bit of a shock with regards to jobs and then stocks all combining to MASK … er, um, I mean produce,

…Despite the average performance of the tail, the sudden flight out of stocks and into bonds managed to mask the disappointing buyside demand, and yields remained near session lows following the break.

Perhaps this was all related TO Silvergate?

ZH: Bank Bloodbathery Sparks Widespread 'Risk Off'

Anyways, what it all means is that there was nothing behind ‘crossing bearishly’ or anything ELSE I might have suggested that led to any sort of thickening plot or a scare of 4% … That leaves us BID, flatter still and heading straight into JOBS today and ‘flation next week…Perhaps SOME of the bid was related to a SQUEEZE of sorts?

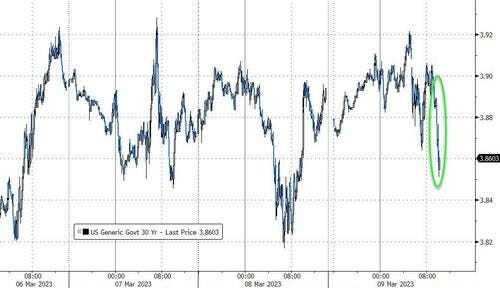

AND … here is a snapshot OF USTs as of 710a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are holding onto half of the solid overnight bull-steepening gains, FTQ activity driving 5y yields as low as 4.07% in Tokyo trading on heavy volumes (220-250% across curve) before a fade into European hours. Liquidity and flow has dried up into London trade however, all eyes on NFP and the regional bank sector (KBE ETF -1.4% in pre-market trade). Kuroda’s last BoJ Meeting went by without much fanfare, policies left unchanged. After losing >30pts overnight in SPX, e-minis are now back to UNCH at 7am. The DXY is a tad weaker -0.2%, BCOM -0.6% as well. Long-end curves are holding modestly steeper, 5s30s +3bps, 10s30s +2.5bps while 2s10s and 2s5s are slightly flatter. Long-end spreads are tightening, 30y SOFR -1.4bps, while real yields are pacing the nominal decline (5y RR -7bps).

… and for some MORE of the news you can use » IGMs Press Picks for today (10 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

In our recent Approaching a turning point publication, we compared the excess Fed policy tightening across cycles.

Our excess tightening metric is based on comparing the peak in real federal funds rate with the estimated level of neutral real rate (R*). The real fed funds peak in the current cycle is based on market pricing (fed funds futures and inflation swap pricing), while R* is assumed to be at 1% (as suggested by the bond/equity correlation estimate and confirmed by our joint analysis with our US economists). The excess tightening (Peak real FF - R*) currently stands at the top end of the range (50-125bp) observed since the 70s, with the notable exception of the late 70s. In particular, the degree of excess tightening currently priced is very similar to the late 80s, when both realized and (short-term) inflation expectations were higher than today.

Overall, if market and consumer inflation expectations are correct, monetary policy seems restrictive enough relative to history.

Click through HEREfor chart comparing / contrasting various hiking cycles, peak FF, avg (core)PCE and ‘flation expectations.

Ahead of today’s jobs data, prolly best to start with a note from ‘best in show’,

Anecdotes for February’s payrolls report are encouraging with eight positive proxies and four negative ones. On the plus side, there is the widening of the labor differential, the upside surprise in ADP, and the improvement in ISM Services employment that all suggest another strong month of hiring in February. Conversely, several manufacturing gauges dropped last month including Philadelphia Fed, Empire, and ISM.

Powell’s comments on Capitol Hill earlier this week have reintroduced uncertainty on the size of March’s rate hike, and as the final payrolls report that will be revealed before the Committee convenes, it is difficult to overstate the importance of Friday’s numbers. January’s NFP release represented an inflection for the Treasury market after 10-year yields reached 3.33%, and the strength of the labor market has been traded as a green light for the Fed to continue hiking to a higher terminal rate, and keeping policy restrictive throughout the entirety of 2023 and into 2024. Barring a sizeable disappointment in February’s data, we anticipate Tuesday’s CPI report holds the necessary weight to return the Fed to half point hikes if the data comes in above expectations. In outright yield terms, we’ll be eager to see the degree to which any selloff beyond 4% 10s is again viewed as buying opportunity, or if a disappointment drives yields back through the bottom of the range at 3.90%….

They go on to list positives and negatives where the positives out number negatives by 8 to 4 … Moving along and sticking with the theme of trying to explain, Paul Donovan of UBS knows,

Putting aside the sensationalism that surrounds a US employment report, what is really happening to the US labor market? First, it is hard to describe nearly two years of catastrophically negative real wages as a “tight” labor market. Tightness should be judged by outcomes. Second, the defining feature of the US labor market has been churn. Only one third of California’s “temporary” unemployed workers returned to their original employer. Filling vacancies with external workers is more difficult, but hiring rates are near record levels. Third, structural changes are creating relative changes (fewer checkout operators, more delivery drivers), and mean some jobs are unreported (TikTok content creators, small business start-ups).

The forecast range for non-farm payrolls is quite wide, reflecting uncertainties around seasonal adjustment, unseasonal weather, and the general declining quality of the data (the payrolls survey has a below 50% response rate). The expectation is for a slowdown in job creation.

Food for thought next time you Doordash (drive or order)? For some further food for thought on all topics (SVB, NFP, CPI), this mornings early morning REID,

… We'll have to see how this story develops but something always breaks hard during or after a Fed hiking cycle. Is this another mini wobble on this front or the start of something bigger? Tough to tell but I would be stunned if there weren’t many more casualties of this boom-and-bust cycle. Don’t forget, we haven’t been in recession yet. Imagine superimposing that on the leveraged world we live in.

It's fair to say a new payrolls Friday comes at a fraught moment with today's probably up there with the most closely anticipated in recent times. This is before we see US CPI next Tuesday and what both imply for the March FOMC the following week. With such an outsized beat last month (+517k vs. 189k expected) it’s fair to say no-one has any real idea of what random number will be churned out today. Having said that, both 25bps and 50bps are in play for the FOMC and today and Tuesday will probably be swing factors with Fed Chair Powell stressing that “no decision has been made on this” earlier this week. SVB has to be thrown into the mix too.

As we look forward to the jobs report, the recent momentum behind a 50bp hike actually stalled slightly yesterday even before the SVB story spread. This was driven by the latest round of weekly jobless claims data coming in beneath expectations. In terms of the specifics of the release, initial jobless claims came in at 211k over the week ending March 4 (vs. 195k expected). That’s their highest level so far in 2023, and marks an unusually large surprise on the upside as well, having come in above every economist’s estimate on Bloomberg. In absolute terms, the surprise of +16k above consensus is also the biggest weekly surprise on the upside in 9 months, so this isn’t the sort of report we see often. There was some weather distortions, with California (+10k) seeing a spike following massive snow storms and making up nearly a third of the increase in NSA claims (+35k). We will see how this evolves over the next couple of prints. And at the same time, there was a negative story from the continuing claims release as well, which came in at 1.718m over the week ending February 25 (vs. 1.660m expected).

With the labour market appearing softer than otherwise expected, investors moved to dial back the amount of rate hikes priced for the months ahead. Looking on an intraday basis, expectations of the terminal rate had been at 5.67% immediately prior to the claims report, but fell to 5.61% shortly after, before ending the day -15.9bps lower at 5.515% for the July meeting after the SVB story. At the highs of the day, there was a 74% chance of a 50bp rate hike later this March, before the risk-off sentiment took the probability of a 50bp hike back down to 56% by the close…

Same shop with a note from a different stratEgerist suggesting we are,

The risk reward for bearish front-end positions is becoming more tenuous for a few reasons.

First, the decline in the (private sector) quit rate is consistent with further easing in the labour market. Indeed, the quit rate is now close to the 2.7% level we had pencilled in to enter outright steepeners in the US.

Second, the forward real policy rate relative to (upwardly revised) estimates of neutral exceeds all previous tightening cycles with the exception of the late 70s. Unlike the late 70s, inflation expectations have remained broadly anchored. Therefore, it is not clear that a more restrictive monetary policy stance is required.

Finally, the risks to US fiscal policy posed by the debt ceiling are likely to become more prominent in the months ahead.

Strategically, a UST2s10s steepener is attractive as there is 100bp+ gap between our current forecast and the forwards. Tactically, there is enough uncertainty around the stickiness of underlying inflation that we choose to wait before initiating the trade…

And one for our inner stock jockey — this from NOT MS but a rather large British operation,

Barclays: U.S. Equity Strategy: Food for Thought: Head Fake or First Step?

Equities' recovery from the October 2022 lows seems to fly in the face of stubborn core inflation, rising rates, and growth uncertainty. The magnitude and the duration of the recovery make the current rebound one of the biggest bear market rallies in history — unless we are witnessing the emergence of a new bull market.

In closing, today is the day AFTER THE yield lows (so far) thanks to COVID where 10yy got as low as .3137 and long BONDS as low as .6987 on March 9th, 2020 …