I spy with my little eye some momentum (stochastics) crossing and bearisly so … may appear at first to be a concession but … at / near some important levels of ‘support’ (up nearer 4.00%) so … the plot thickens ahead of NFP tomorrow and next weeks CPI.

… here is a snapshot OF USTs as of 713a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries embraced a quieter session overnight after what's been an active past few days, with Treasuries seeing minimal (50-65% 30d ave) volumes aside from the front-end (which saw a 3.8 block TU seller in late-Tokyo time). Still, the curve finds itself modestly steeper and reversing yesterday’s actions with 2s10s +3bp steeper. Franchise flows were minimal overnight, with some light RM sellers seen in intermediates. It was a quiet day x-market too, overall FX volumes down 20% in comparison to 30d averages according to e-trading data ahead of Claims, BOJ, NFP events/catalysts. Tomorrow will be the last BoJ meeting for our current governor, Kuroda-san, with expectations tempered for policy alteration (no change given fiscal year-end). S&P futures are -10pts here at 7am with the DAX -0.5%, DXY -0.3% and CL +0.1%.

… and for some MORE of the news you can use » IGMs Press Picks for today (09 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

First up an eye-catching ZH HEADLINE from BBG as source of recon

Authored by Ven Ram, Bloomberg cross-asset strategist,

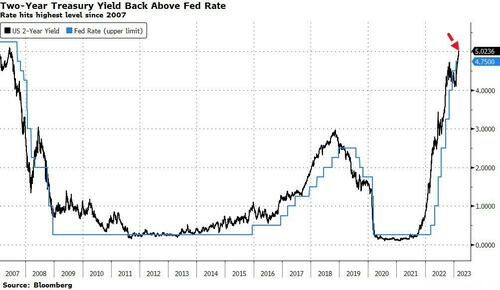

Back in October, we contended that Treasury two-year yields would surge past 5%.

For a time after after that - especially from November through January - it seemed the market winds had changed direction.

But after Fed Chair Jerome Powell vowed to re-accelerate the pace of tightening, the bearish mood was in full display, sending the two-year Treasury yield past 5%.

It wasn’t, therefore, any surprise to see stocks slump, the dollar flex its muscles and gold tumble.

But the most important reaction was the surge in US real rates, which has key implications for pretty much every asset.

Still, this movie may have some way to go (h/t to Daniel Curtis for chart).

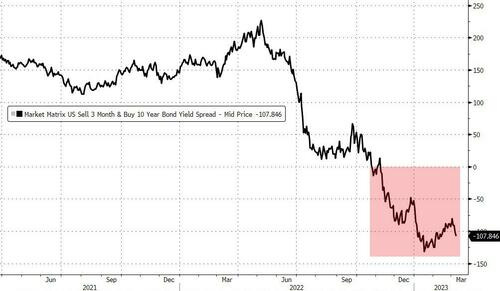

Here’s why: the tell-tale three-month/10-year Treasury curve has been in a consistent inversion since November, and typically, recessions have followed between 11 and 14 months.

That would suggest that any inflection point in the US economy may be unlikely before October at the earliest - meaning the Fed may be raising rates all through the summer. That may mean that a 6% terminal rate is no longer just a tail risk but a real prospect….

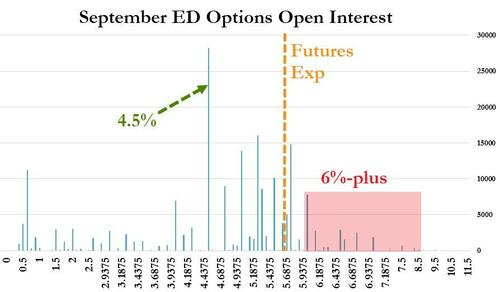

… [ZH: As an aside, Eurodollar options traders have a number of bets out there for rates being 6% or above by September...]

… Away from zero day to expiration options (0DTE), everyone in the market (and beyond) seems fixated on 2-year yields. There are about 100 iterations of the following question:

Shouldn’t I just put my money into 2-year treasuries? They are yielding 5%, after all?

Where to invest on the yield curve is always on my mind, but suddenly everyone seems to be talking about the 2-year. Not just bond “geeks” but mom and pop investors. Not just about where on the yield curve, but as part of every asset allocation conversation. Bob Pisani and I spoke last night for this CNBC piece on “tech and quality stocks” and he also mentioned he was being inundated with calls, from unlikely corners about the investment merits of the 2-year Treasury.

To me, there are several questions that need to be answered, to determine how much weighting you should have in the 2-year Treasury relative to normal:

What is the right mix between stocks and bonds.

Within bonds, what is the right mix between credit risk and rate risk.

Within rate risk, where on the curve do you want to be.

I feel compelled to discuss this, because on major thesis making its way around market is that:

Everyone will sell equities to buy the 2-year Treasury.

I feel compelled to fight against that…

… Bottom Line

The 2-year treasury above 5% makes for some great headlines and is an easy one for the nightly news to glom on to. There is an appeal to 5%, but it is a bearish trade.

Does it impact how I position my portfolio? Yes, but only at the margins. It is not a panacea.

Maybe it will turn out to be the “right” trade, but this is setting all of my contrarian alarm bells off, and is another reason I’m comfortable being long risk here, hoping for another leg higher as people get forced into the market. And yes, I might be buying the 2-year at 4.75% in a week with stocks down 5% and my tail between my legs, but that is the positioning I’m most comfortable with right now.

If the US is a Ferrari (now brake hard, now accelerate), the Euro Area’s handling is more like a Ferry. A less aggressive approach to turning inflation around is appropriate for the ECB. That may mean lower peak policy rate, but more persistence. Despite that, the Euro front end has been following the US closely since mid-February, bearish-flattening on the way. Such unimaginative dynamics may change next week. The new ECB macro projections set the tone for Governing Council for the coming months and they’re likely to ease up substantially on the inflation assessment.

The risk is now that the market realises the ECB path, as priced, is too aggressive. A bullish-steepening correction is our base case. If we’re wrong and the ECB prefers the bull-in-a-china-shop strategy to breaking inflation, further inversion is likely. The steepener in receiver swaptions attempts to sidestep that risk.

2s10s steepeners in 3m receivers. …

… The Euro curve has been strongly driven by US dynamics and hawked-up governing council members, still channeling December’s economic assessment…

CURVES (here/there) aside and now in as far as JPOW 2.0, Paul Donovan/UBS

The economic story for 2023 might be summed up by the mixed narrative of the Federal Reserve’s Beige Book. Talk of a “hard” or “soft” landing misses the complexity of the economy. Some parts of the US may get a hard landing, and others no landing. Thus, housing activity was weak (it is sensitive to the relentless rate increases). But consumer demand for leisure travel is so resilient that vacations may have to be considered a consumer staple, not a cyclical purchase.

Fed Chair Powell scaled back expectations for a more aggressive March rate hike in comments yesterday. Today, we get initial jobless claims data, which is based on reality, not a survey of reality, and thus does not have the quality problems of other data…

Hard. Soft. Complex. Sounds like Paul was talking ‘bout NFP … since HE wasn’t, a large French bank (and their new team of BBG analysts) IS,

US February jobs preview: Cooler than January, but hot enough for a 50bps hike in March?

KEY MESSAGES

We expect the “totality” of the US employment situation data released on Friday to confirm Fed Chair Jerome Powell’s assessment that “the labor market remains extremely tight.” The chair’s hawkish testimony to Congress (see US: Powell puts 50bp hikes back on the table, markets take note, dated 7 March) means the bar has been lowered for a 50bp rate hike at the March meeting.

We estimate a solid payrolls print (240k versus 225k consensus), even after accounting for a reversal of some temporary factors, which inflated the January result. If realized, our forecast would be a strong reading, yet a downshift from the 291k average posted in Q4.

Wage growth could accelerate (0.5% m/m vs.0.3% consensus). We are concerned the trajectory of average hourly earnings growth will mirror that of the recent re-acceleration in PCE inflation.

The risks are tilted to the downside around our estimate for no change to the 53-year low for the jobless rate.

Leading indicators, including low initial claims filings, an increase in the “jobs plentiful" component of the Conference Board confidence survey, and the ISM services report all pointed to labor market resilience in February.

I see ‘resilience’ and I’m frankly right back to ‘GOOD news = BAD’ (ZH yest??) AND … i’m done. It is ‘moving day’ — the day between ADP and NFP with markets pinned to UNCH on light volumes, I’m gonna just quit while I’m behind and so … THAT is all for now. Off to the day job…