Good morning … 2yy are UP 10d in a row and today there is finally some stability BUT it is early …

Watching momentum (crossing BULLISHLY) and will check back in over weekend with a WEEKLY look (which continues to have more bearish momentum look) and while yields have been climbing it IS interesting to note stocks have yet to ‘look down’ (ala Mike Wilson)

And yet … this week has produced the unlikely 3-fer,

ZH: Solid 7Y Auction Stops Through After Jump In Foreign Demand

Even MORE stunning as it comes on heels of HOT PCE

ZH: Q1 GDP Revised Higher As Core PCE Comes In Hotter Than Expected

But then again, somewhat lower gross domestic INCOME (more below) and so, NVDA

ZH: NVDA Adds Record Market Cap; Everything Else Dumps As Debt-Ceiling Idiocy Continues

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…in a morning comment, “Early Close Considerations”

… Overnight Flows Overnight volumes were fairly typical ahead of the long weekend as rates pulled off the recent extremes ahead of this morning’s data. As has been the case all week during the overnight session, we’ve seen better buying across the curve.

WHILE YOU SLEPT Treasuries are higher and the curve slightly steeper ahead of today's PCE data and early close. DXY is lower (-0.27%0 while front WTI futures are higher (+1%). Asian stocks were mixed, EU and UK share markets are mixed/higher while Es futures are showing +0.15% here at 7:15am. Our overnight US rates flows saw real$ buying in intermediates and the long-end during Asian hours with Tokyo's weaker CPI (link above) putting a bid in long-end JGB's. In London hours our desk saw limited flows with some fast$ selling in intermediates on this morning's uptick. Overnight Treasury volume was subdued at ~80% of average across the curve.

… Next and last we take an updated look at the long-term chart of the Treasury 2s5s10s 'fly. This 'fly has come up in so many conversations this week so we thought we'd post this picture to put a frame on the discussion. The belly still looks super 'overbought' on a long-term basis and, in recent months (including this month) 2s5s10s has respected major range support near the -64bp area. Fade the belly on pushes to -60bp and below?

… and for some MORE of the news you can use » IGMs Press Picks for today (26 MAY) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ and thinkin’ bout … Since it sources everything from the ‘sellside’, I’ll begin with a question (and ZH link).

How is it that yields are what, half way back UP from Marchs DROP concluding that the banking ‘crisis’ is OVER … when you have FACTS (with some snark) like this,

ZH: Bank Bailout Facility Usage Hits New Record High As Money-Market Fund Inflows Soared Again Last Week

… This huge resurgence in money market fund inflows strongly suggests tomorrow's H8 deposit report will show the bank walk/run is continuing...

$$ continues to chase YIELD. It is either a feature OR a flaw and sum of ALL policies emanating from the goat rodeo in DC.

Moving as far away from DC and OUR clowns to some other developments worth noting and watching closely as Japan — leaders in as far as QE, negative rates, etc — making some waves overnight,

Reuters: BOJ's Ueda says targeting shorter-duration bond yield among future options

BOJ could tweak YCC if benefit, cost balance shifts - Ueda

Various ways to tweak YCC though must avoid premature tightening

Japan's inflation to slow ahead on falling raw material costs

If BOJ's inflation projection proves wrong, it will act swiftly

Policy review will include surveys, hearings and workshops

The Treasury’s “early June” deadline looks very accurate, in our view. Over the last few days, the outlook for Treasury’s room under the debt limit has deteriorated slightly, though this might also reflect daily fluctuations in tax receipts that could reverse in coming days. That said, at the moment our central scenario is that by June 2 the Treasury’s room under the debt limit will barely exceed $30bn (the minimum cash the Treasury has targeted in prior debt limit projections) and that funds will run dry by June 9…

… Negotiators appear to be closing in on an agreement. While it is hard to predict when an announcement could come, we think the odds are highest that a deal is announced late Friday (May 26) or on Saturday (May 27). If so, this would likely allow a House vote late Tuesday (May 30) or Wednesday (May 31). The Senate also needs to pass the deal, though procedural obstacles there are unlikely to be what prevents timely enactment …

… The core of the debt limit deal is likely to be spending caps. We estimate that the real reduction in spending next year would vary from around -0.1% of GDP (under a freeze at 2023 levels) to -0.5% (under the House-passed bill). A compromise that sets 2024 spending at the 2022 level indexed for inflation would result in modest cuts of around -0.2% of GDP in 2024. Regardless, the spending cuts under consideration do not appear likely to meaningfully affect the macroeconomic outlook.

It is amazing to me just how much time, energy, manpower and INK spilled on something that will be utterly useless in something like 24hrs or whenever it is the next tape bomb hits…

Turning away from the ceilin’ as the clowns in DC hash out details in effort to raise the roof, a quick look back at yesterday’s data

Barcap: 2023 Q1 GDP revised higher in second estimate, alongside negative GDI growth

The second estimate puts Q1 GDP growth at 1.3% q/q saar, up 0.2pp from the first estimate, lifted by upward revisions in multiple categories and a smaller drag from inventories. Meanwhile, real GDI fell notably for a second consecutive quarter.

… real Gross Domestic Income (GDI) registered a second consecutive quarterly decline, reflecting a notable drop in profits. The two consecutive drops in real GDI point to lower income growth than conventionally thought, and to more risk of slowing momentum …

For MORE on GDP,

Wells: Revised GDP Data Show Contractions in Income and Profits in Q1-2023

The modest upward revision to first quarter GDP growth does not really change the overall narrative of an economy that is losing momentum. The new data in this release come on the income side of the national accounts, which revealed more weakness over the past couple of quarters.

… Consistent with this narrative of sub-trend growth were the data on gross domestic income (GDI), which were released for the first time for the first quarter. In theory, real GDP and real GDI should be equivalent, but they usually differ somewhat in practice due to data omissions. In that regard, real GDI contracted at an annualized rate of 2.3% in Q1, which follows the drop of 3.3% that was registered in the last quarter of 2022. On a year-over-year basis, real GDP was up 1.6% in Q1-2023 while real GDI fell 0.9% (Figure 1), signaling the widest gap between the two measures on record. This weakness in GDI suggests that real GDP growth in recent quarters may be revised lower in subsequent data releases. Although one side of the National Income & Product Accounts (NIPA) may be contracting, we would stress that the U.S. economy is probably not in recession at present. Notably, incoming data continue to show resilience in the labor market.

This may just be the sort of ‘good’ news Fed and pivot’istas are hoping for BUT not sure this can be ‘good’ enough, quickly enough … without INCOME, becomes incrementally harder to SPEND therefore, ‘flation could very well continue to decrease.

OR we’ll continue to see references to SHRINK in earnings calls.

Why or when it became a cool thing to do (substitute the words SHRINK for THEFT) is beyond me … are we all, collectively, that stoopid? Marketing is powerful and whatever you do, DONT say we’re losing money ‘cuz, you know, laws that protect sellers of things (ie STORES) from shoplifting, are there BUT we’re not going to enforce them?

What the actual F?

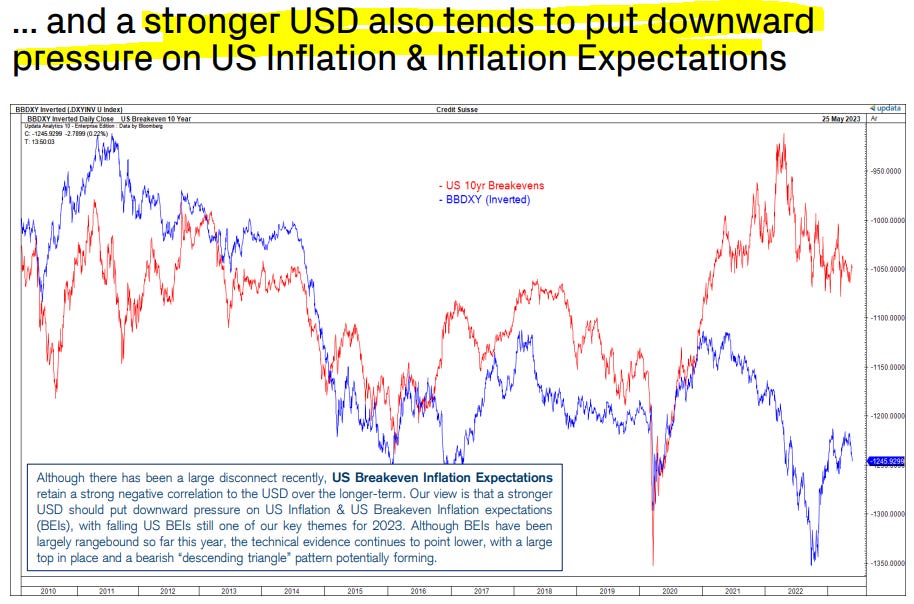

Sorry for that … back TO markets and a couple CHARTS / links of interest. A new note from a large SWISS operation,

The USD continues to appreciate on a broad basis and we continue to see growing evidence that we may be witnessing the construction of a large and important “double bottom” base in the DXY $ Index.

At present, the key driver of USD strength has been rising US Bond Yields and we expect this to persist further in the short-term following the completion of a near-term base in US 10yr Yields. As we move into the 2nd half of the year though, our call for lower equity markets and lower yields over the medium-term is likely to benefit the USD as strength moves away from being driven by higher US Yields towards safe haven flows.

And the REASON I’m passing along or pausing to consider implications OF bullish USD move,

Perhaps those in control and pulling the levers (while at same time trying to sell the idea they are NOT concerned with and will NOT speak to the currency — ie THE FED) are not so stoopid after all? Tightening policy leading to firmer USD (and whatever else may / may not happen — still TBD) is a feature not a flaw?

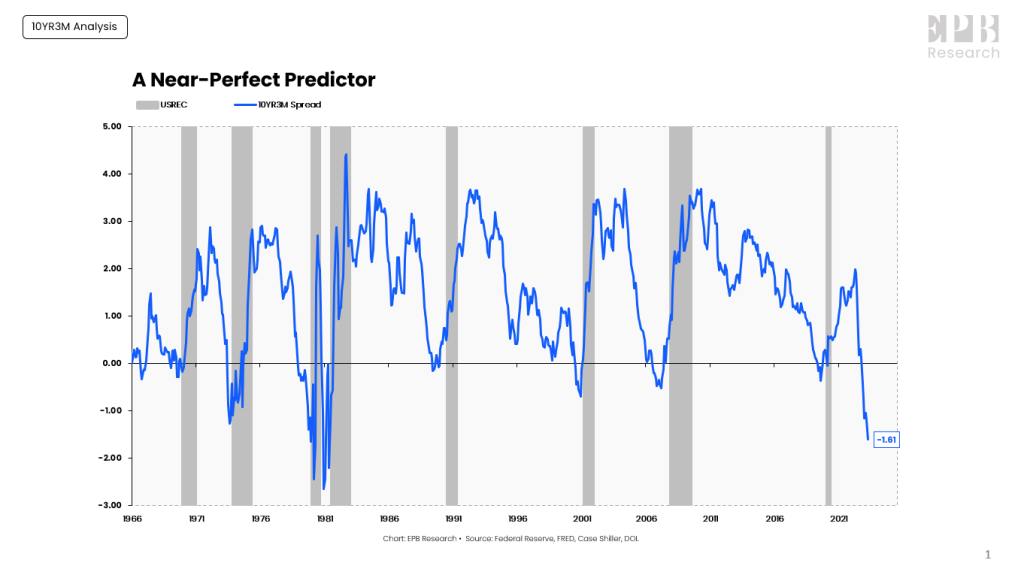

Fed policy and STRONG USD in mind, a note from EPB

EPB: Painfully Accurate: The 10YR3M Recession Indicator

This article is about the 10YR3M spread, which is a reliable leading indicator of business cycle recessions.

The spread between the 10YR Treasury Rate and the 3-Month Treasury rate, often referred to as the 10YR3M spread, is one of the most reliable leading indicators of business cycle recessions.

The 10YR3M spread has inverted or before every recession since the late 1960s with virtually zero false signals, particularly in the last five decades. The only modern false signal occurred in late 1966.

Today’s yield curve inversion is historic in terms of depth, only rivaling the double 1980 recession.

Read on and note in mind along the way, the path or ROADMAP to a JUNE HIKE (and beyond), anyone?

That in mind, a few signs / things to consider along the way, on the ‘route map’ / guide (WAZE for financial markets, if you will) is this next note from St. Louis FED

A new analysis suggests that the food expenditures category of the consumer price index could be a useful signal of future headline inflation.

… Food Now Has the Highest Predictive Value for Headline CPI In the first figure, we see that the energy SNR is the second lowest among the six CPI components, continuing its trend since the mid-1970s. In 2011, the SNR of food prices was higher than that of energy, transportation and clothing but lower than that of health care and shelter. This is no longer the case: Food now tops the chart with the highest SNR (0.09), followed closely by health care (0.07). This means that food has the highest predictive content relative to noise among all the components. At least in the case of CPI, the SNRs suggest that food is a useful predictor of future headline inflation and should not be excluded vis-à-vis core inflation. Moreover, since 2011, health care has become a more important player.

The note cites 2011 research paper and also suggestive of idea that Food SERVICES has highest predictive value among PCE components … this all in context of SIGNAL-to-NOISE (SNR) ratio, they conclude note,

…Conversely, the SNR of clothing, as well as that of gas and energy prices, remains at the bottom of the chart, mirroring the case with the CPI. Also consistent with the CPI components, the SNR for transportation services is slightly higher than those of clothing and energy, but the ratio is still very low, indicating little predictive significance for future headline inflation. Also near the bottom are financial services and other nondurable goods.

Um … so is this note / idea / concept more signal or noise? I will clarify my question and offer half an answer - this stack is NOISE and those bloviating over at St. Louis FED are likely somewhat less so but…

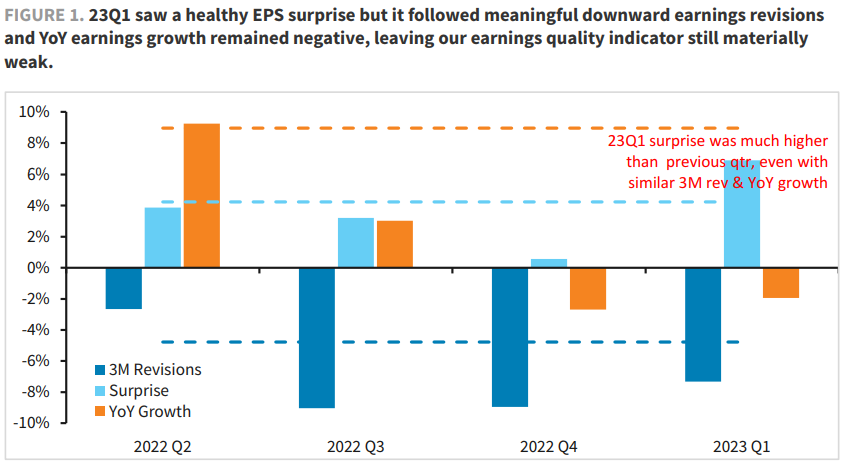

These next notes are from a large UK shop and this one takes a look at US equities,

Earnings quality improved sequentially in 1Q23, but YoY growth is still negative and QoQ comparisons only look good because 4Q22 was among the worst seasons on record. Negative operating leverage remains a challenge for most sectors and we think it's too early to call a margin recovery.

… and this next one takes us ‘round the world in 60sec, with a more global focus

Weak Chinese data has prompted profit taking on Europe and Cyclicals, while UK is stuck in stagflation. In contrast, US activity is holding up well, so real rates are rising again but without hurting stocks much. Liquidity drain, if debt ceiling is lifted, is the new worry now, yet impact on markets is not straightforward.

Finally, while I’m not a stock jockey, it’s worth mentioning that on this day in history (1896), via Encyclopedia.com

...Dow Jones & Company, Inc. published its first Dow-Jones industrial average on May 26, 1896 which has been kept up to date every day since by The Wall Street Journal. On that day, the market closed at 41 based on Dow's method, which was based on the stocks of 12 well-known and successful smokestack firms. Dow added up the prices for these companies stocks and then divided that number by twelve. Today, the market regularly exceeds a level of 8,000 based on the same methods used at the turn of the century. Only now, the stock prices are divided by 0.33839549 because of the sheer volume of stocks traded.

Happy 127th !! AND … THAT is all for now. Off to the day job…safe LONG weekend. Updates of some sort are HOPEFUL but family (and yardwork FIRST!!)

This the first and only place I have ever heard anyone talk about GDI and it's relationship to GDP.

Thanks for the Education...