Will ReSale TALES and PPI combine and matter MORE to any of the narrative creators or those running money or actively managing a P&L — theirs or someone elses? What IF they run counter to the RATE CUTS narrative expressed / reflexed with Tuesdays CPI? Did they add TO said narrative and the HOPE (for a soft landing — seen only ONE TIME in past 40+ years?

ZH: US Retail Sales Declined As Student Debt Payments Resumed In October

… Not exactly the 'great news' everyone was expecting but still a 'beat'.

ZH: Huge Gasoline Price Drop Sparks Biggest US PPI Plunge Since COVID Lockdowns

The GOOD news is PRODUCER prices were quite soft and SOME (Steno) point out its predictive capabilities through to CPI …

HOPE springs eternally, once again.

And yet, with all that HOPE, rates retraced UPWARDS some of their CPI induced euphoria and drops … A bit of context — 10yy DAILY back TO 2017

On the UPSIDE, 5.10% appears to be of some importance and 4.45% does appear to be an interesting level to watch on the downside … These as momentum (stochastics, bottom panel) appear to be overBOUGHT. Time at a price can / will resolve but to the point that yesterday’s move counter TO CPI day monster face ripping BID.

That’s weird … Or perhaps it isn’t at all. I suppose there is something TO short-covering nature of the bid (noted by BBG HERE

… The likelihood is that a rush to cover short positions and put on fresh longs overcharged the rally as investors rushed to anticipate a rapid Fed pivot toward rate cuts. That’s despite policymakers saying after the CPI data they still see a long, potentially hard road to get inflation back down to where they want it.

AND some more evidence of the ‘army’ nature of markets (ie LEFT, RIGHT, LEFT…)

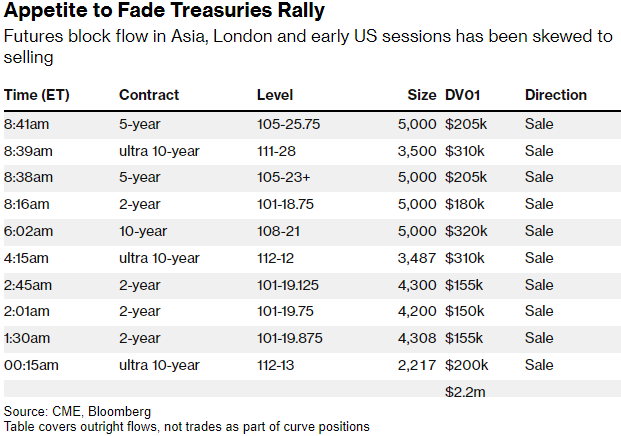

Bloomberg: Bond Traders Reload Bets on Higher Yields After Massive Rally

… Wednesday’s session kicked off in Asia with a flurry of large, privately negotiated transactions known as block sales in the futures market linked to Treasury bonds. Block sales in Asia’s session were followed by further short wagers on five-year and Ultra 10-year contracts in New York trading as yields rose after a stack of mixed economic data at 8:30 a.m.

The trades help explain Wednesday’s rebound in yields following Tuesday’s inflation-driven rally. The momentum shift has seen a climb as much as 10 basis points across 5- to 10-year rates, with the 10-year exceeding 4.55%.

Block trades, which are favored by asset managers, offer the ability to quickly establish large positions at a single price. They’re closely watched for signs of big bets on where the market is headed.

Bearish appetite was matched in the Treasury options market where heavy buying was seen in options on a two-year position targeting a 40 basis-point yield rise by the end of next week.

Similar action has also been seen in the options market linked to the Secured Overnight Financing Rate, where demand has emerged on hedges to fade the aggressive pricing of rate cuts for next year…

Got it. EBBS and FLOWS. It is what the bond market does and we can / will continue to debate soft or hard (or NO) landing — more on that below — but for now, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the curve modestly flatter with UK Gilts (see attachment) leading the charge this morning. DXY is UNCHD while front WTI futures are modestly lower (-0.3%). Asian stocks were mostly lower after China's 70-cities home prices say their biggest drop (MoM) in 8 years, EU and UK share prices are mixed while ES futures are little changed here at 6:45am. Our overnight US rates flows saw the Tsy rebound begin during Asian hours with an early block buy of TY futures setting the tone there. We saw some front-end selling with the rally seeing outperformance in intermediates and the long-end. Overnight Treasury volume was about average overall.

… Our first attachment this morning updates the daily chart of Treasury 10yr yields to show how yields have been bumping along (ghosted circles) the top of their well-defined bear trendline in recent days. The price action hints that we're not alone in drawing the bear trend (in place since May 4th) the way we did. If true, then when the trendline is taken out with a close (see next), a quick move back to key resistance near 4.34% (fmr rate range high dating back to October last year) might be expected. Indeed, we think both the bear trendline and the resistance near 4.34% will eventually be taken out; probably soon.

… and for some MORE of the news you can use » The Morning Hark - 16 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Retail sales edged down 0.1% m/m in October, mainly reflecting declines in the autos category. However, sales in the control group (+0.2% m/m) held up quite well, and estimates for the prior month were revised upward. This positions consumer spending for a solid gain in Q4, albeit slower than Q3's unsustainable pace.

Barcap: Slowing growth and diverging policy (big picture longer-term thought process here requires TIME to read / let sink in …)

We expect a slowdown in global growth to 2.6% in 2024, as the US finally decelerates, Europe stagnates and China continues to grapple with structural challenges. Disinflation will also slow, but higher-for-longer rates may still lead the ECB and BoE to ease ahead of the Fed. The BoJ should hike, at last.

Duration risk appetite has rebounded this month, supported by several factors, including a reversion towards trend-like economic growth and waning concerns that Fed policy may be insufficiently restrictive.

Softer inflation has lowered the bar to a shift in focus more firmly towards cuts, but intensifying cut pricing beyond what’s already in the curve requires a clearer nudge from growth. Even then, upside to received positions may be limited.

High front-end vol and rich receiver skew present an opportunity to offset some of the negative carry to front-end longs against a baseline of a contained rally from here. We favor receiving 6m2y against selling 6m2y A-50bp receivers.

We prefer steepeners less sensitive to the timing of cuts and more exposure to the potential that cuts could extend further than the ~3.75-4% terminal rate currently priced. We add 5s10s SOFR swap steepeners to our trade idea portfolio, simultaneously taking profits on our 5s10s30s fly idea.

CitiFX Techs - Stocks: A return to the top? (if so, then what for bonds…asking for a friend)

… Levels to watch:

S&P 500: Price is testing resistance at 4488-4511 (76.4% Fibo, September 14th high). Above this, next key resistance is at 4607.07

DB: Mapping Markets: The 7 times that markets have anticipated a dovish pivot (so, if I’m reading this right, MARKETS hoping / pricing it to be different this time)

After the downside surprise in yesterday’s US CPI report, there’s been growing anticipation about a dovish pivot from the Fed over the months ahead. For instance, futures are now pricing in an 87% chance of a cut as soon as the May 2024 meeting.

But this is at least the 7th time in this cycle that markets have seen a clear reaction to a potential dovish pivot.

On the previous 6 occasions, those hopes have been dashed, since inflation has remained too fast for the Fed to be comfortable cutting rates. Indeed, it’s been above their 2% target since early 2021, and the Fed's dot plot is still pointing to a more hawkish stance for policy relative to market pricing.

Clearly this situation could change quickly if unemployment rose or inflation fell further. But in light of this repeated pattern, we run through the 7 times that speculation has risen about a dovish pivot from the Fed. Much of this updates our previous analysis from last year here, where we pointed out the first 5 occasions.

….1. November 2023: Weak data releases and a downside surprise in the CPI lead… 2. March 2023: The banking turmoil following SVB’s collapse led to growing anticipation that central banks had finished cutting rates altogether… 3. Late September/Early October 2022: Major market turmoil centred on the UK leads markets to price in more rate cuts for 2023… 4. July 2022: Global recession fears and a weak inflation print sees talk of slower rate hikes resurface… 5.May 2022: Rising risks to global growth see investors take out expected tightening… 6. Late February/Early March 2022: Russia’s invasion of Ukraine sees the Fed commence hikes with 25bps rather than 50bps… 7. November 2021: Investors doubt how fast central banks can hike after the Omicron variant appears…

… with markets pricing a pivot for a 7th time, it's worth considering whether the conditions are actually in place for that to happen.

DB: Early Morning Reid (elaborating more on the above report)

… The stronger newsflow meant there was a bit more scepticism about the rate cuts being priced for 2024 after Tuesday’s CPI report. For example, the rate priced in at the Fed’s December 2024 meeting was back up by +10.8bps to 4.437%, which reversed almost half of the previous day’s -25.2bps decline. And in the near term, the likelihood of a cut by the May meeting came down from 86% on Tuesday to 73.5% by the close. So we’ve now got a slightly shallower pace of cuts priced in relative to 24 hours ago. Bear in mind this is now the 7th time in the last two years we’ve had a very clear example of markets getting excited about a dovish pivot, and on the previous 6 those dovish expectations have entirely unwound again. For reference, Henry has collated all the times we’ve seen this in an update yesterday (link here). It all started with the Omicron variant being seen as the reason the Fed wouldn’t be able to raise at all in 2022! It’s a a fascinating trip down memory lane of the last two years of the markets continually being fooled on rates. At some point there will be a dovish pivot, and this could be closer than the others to it, but be wary that we’ve now been to this well 7 times in 2 years.

Core CPI inflation well above target, but recent trends showing progress

… PCE trend measures of inflation showing some moderation as well

Goldilocks: Retail Sales Decline by Less Than Expected; Producer Prices Below Expectations; Boosting Q4 GDP Tracking to +1.7%

BOTTOM LINE: October retail sales declined 0.1%, above consensus expectations, while core retail sales rose 0.2%, in line with consensus expectations. Combining data from the latest retail sales and CPI reports, we estimate that real core retail sales rose 0.1% in October (mom sa). The producer price index (PPI) decreased by 0.5% in October, against expectations for a modest increase. Based on details in the PPI and CPI reports, we estimate that the core PCE price index rose 0.16% in October, corresponding to a year-over-year rate of +3.48%. Additionally, we expect that the headline PCE price index increased 0.05% in October, or increased 3.02% from a year earlier. The Empire manufacturing index increased by more than expected in November. Business inventories increased in line with expectations in September. We boosted our Q4 GDP tracking estimate by three tenths to +1.7% (qoq ar) and our domestic final sales growth forecast by three tenths to +2.0%.

ING: Pipeline pressures support the US soft landing view (decent visual on SPENDING)

After yesterday’s big reaction to the benign CPI data, which saw risk assets rally hard and the dollar come off as interest rate expectations fell sharply, it is the turn of retail sales and producer price inflation today. It once again feeds the soft landing narrative with subdued price pressures and resilience in activity

JEFF: Oct Retail Sales -0.1%, Control Group +0.2%... Consumers Hitting Pause Button After Breakneck Q3 (picture worth a thousand words … #MoarSTIMMY please)

■ Headline retail sales fell -0.1% in October, with the control group +0.2%. Looking at the individual components, it is difficult to find distinct sources of strength. ■ The consumer spent money like there was no tomorrow in Q3, and the retail sales data for October suggest that they broadly paused at the outset of Q4. In our view, the pace of spending in Q3 is unsustainable. While it is somewhat encouraging to see that spending did not fall off a cliff in October, the pause is likely a sign of further weakness to come. ■ The +0.2% increase in the control group is the second smallest increase since March, behind the +0.1% increase in August. This suggests that nominal PCE will be up +0.1% in October, with real PCE unchanged. ■ PCE was up +4.0% in Q3 and it was the main driver of the +4.9% q/q growth in Q3 GDP. Q4 is off to a much slower start, and we are not optimistic about the next two months given the resumption of student loan payments in October, and the lack of experiential spending opportunities in the Winter as compared with the late Summer.

UBS: Soft retail sales, PPI suggest weaker PCE prices

Retail sales soften significantly in October Retail and food services sales fell 0.1% in October, the first negative print since March and a notable softening in the pace of nominal spending after a scorching third quarter. Credit card data had pointed in that direction for October. Sales at the control group of stores decelerated to a 0.2% pace from 0.7% in September. Revisions to prior months were inconsequential. While the September strength initiated a much stronger trajectory for spending headed into Q4 than previously assumed, October tempers the momentum and changes our forecast little, coming both soft and in line with consensus and our expectation. Today's report suggests real PCE in Q4 tracking around 1.5% at an annual rate.

Most components logged negative prints or softer numbers than in September: auto sales traced back 1% in October, sales at gasoline stations dropped 0.3%, furniture sales posted their fourth negative print in a row and building materials sales their second. Bucking that trend, sales at food and beverage stores shot up to 0.7%. The catch-all miscellaneous stores swung from a 3% decline in August to a 4% increase in September, and then a 2% decline again in August, with no discernable trend going forward …

Yesterday’s US retail sales reinforced the resilience of the US consumer. That resilience depends on middle-income consumers, and middle-income consumer resilience depends on real spending power being better than headline data suggests. Inflation pressures continue to moderate, and today’s US import price data should show falling prices.

With inflation in retreat, why are central banks not making more of the peak of the rate cycle? Mainly because bond traders can do (some) of central bankers’ jobs, and policy makers do not want bond markets to ease financial conditions too much. We hear from several ECB speakers, including (inevitably) ECB President Lagarde, and a reiteration of “we could raise if we wanted” is likely to be heard and ignored.

US President Biden and China’s President Xi agreed on a few things—military talks and panda exports. Markets do not really care. The US Senate passed legislation to keep the government open a few more weeks—the whole saga starts again at the start of January.

US October industrial production data is due, and is expected to decline. The 2021 party for consumer goods’ demand is long since over, as people prioritize having fun. Apparently, going to a concert is more fun than buying a washing machine.

Wells Fargo: Despite Lost Momentum in Retail Sales, Consumer Resilience Still Intact (if you squint you can see slight decline in holiday sales f’cast…)

Summary Retail sales fell 0.1% in October, a modest dip relative to expectations. The subset of stores types more closely aligned with consumer spending in GDP saw sales rise 0.2% after upward revisions to prior data. Holiday sales are on track with our forecast for a 5.0% annual increase.

… Holiday Sales This is the last retail sales report before the official start to the holiday shopping season. Holiday sales is what gets spent in November and December and includes total retail sales less sales at auto dealers, gasoline stations and restaurants. We learned today that through October those categories are up 4.7%. We forecast holiday sales to increase 5.0% this year which, if realized, would be both above the long-term average, and yet also the smallest annual gain of the past four years (chart).

Another theme we are watching is how the current staying power comes at a price to the financial health of households in terms of both diminished savings and their ability to stay current on debt, a factor at play in the trend rise in credit card delinquencies. Income growth is the most important driver of spending, and as long as the labor market remains tight, households will likely continue to spend.

We expect current conditions to allow for a decent holiday sales season for retailers, but we are still likely to see the slowest pace of annual sales growth since ahead of the pandemic, and we remain cautious on the prospects for spending in the new year. We will provide updates to our holiday sales estimates as the retail sales data come in and keep you apprised on how the holiday sales season evolves.

… And from Global Wall Street inbox TO the WWW,

FRB ATLANTA: Market Probability Tracker Updated with October's CPI Data - November 15, 2023

Bloomberg: Pimco’s Ivascyn Warns of ‘Too Much Enthusiasm’ on 2024 Rate Cuts

… While relishing the boost to Pimco’s performance from the strength in bonds, which has erased the Bloomberg US Aggregate Index’s decline for 2023, Ivascyn warned “it’s going to be a bumpy journey” to see inflation truly moderate toward the Fed’s goal.

“Moving in the right direction is different than getting to the central bank target of 2%, give or take,” he said in an interview at Pimco’s headquarters in Newport Beach, California…

… Now in his 25th year at Pimco, Ivascyn, 54, said “there’s a risk that there’s going to be a little too much enthusiasm around around rate cuts next year. The central bank’s going to be very careful in cutting rates unless they see meaningful economic weakening, just because the inflation problem is far from being solved.”

For Ivascyn, the upshot is that he’s ready to trim Pimco’s interest-rate exposure if bonds rally too far, after the firm had “let our interest-rate risk go up as rates increased” last month to multi-year highs…

Bloomberg: Bonds are for turning, and turning again (Auther’s OpED … ONE chart worth repeating, but a good read overall)

Still thinking of a soft landing? There’s only been one during a period of rising rates in the post-Volcker era, and under very different circumstances.

… So why does hope of an imminent cut keep recurring? One big issue is that cutting inflation generally involves a slowdown in growth. Betting on falling price rises is thus usually a fairly direct way of betting on the economy to go into recession. That makes the bar for a true “Goldilocks” (not too hot, not too cold) scenario difficult to clear — and therefore suggests that big rate cuts to cushion a hard landing won’t be far away.

There are many definitions, but if we say that a soft landing is a period of rising rates that doesn’t lead to even a quarter of negative economic growth, then there has been precisely one in the post-Volcker era. That came in the mid-1990s, after the Fed under Alan Greenspan hiked unexpectedly hard in 1994, created a brief but brutal bond bear market, and sparked a series of credit and devaluation crises in the emerging markets. In the US, however, growth never went negative:

That soft landing came while globalization was taking hold as the Clinton administration feasted on the “peace dividend” from the end of the Cold War and moved the federal budget into surplus. None of those things apply now, so a soft landing looks implausible.

If the sheer unlikeliness of a soft landing spurs repeated market “pivots,” then the problem of reflexivity — the tendency of markets to create their own reality — helps end them. Jerome Powell of the Fed put great store earlier this month on the fact that financial conditions were tightening. This helps restrictive monetary policy have the desired effect, and means there’s less need for further rate hikes. The problem is that by acting on this, and buying bonds, so much risk appetite is back that financial conditions have eased. Using the Goldman Sachs US Financial Conditions index, a popular benchmark, Tuesday’s big rush into both stocks and bonds loosened things so much that conditions are now more lenient than the norm:

If we look at the past failed pivots, this dynamic is part of it. The Fed cannot tolerate substantially lower bond yields. If they fall, there is an incentive for governors to sound more hawkish. The bond market might just have pivoted for good, but with the Fed’s position still uncertain — and the small matters of a huge amount of bond issuance in the pipeline, and a House of Representatives that can’t be relied on to fund the government — it’s too soon to say that for sure.

Bloomberg: Poor Liquidity To Keep Bonds On Thin Ice After Positioning Rout

… Today’s retail sales number was better than expected (though a decline in headline), potentially wrong-footing the bond market after yesterday's strong gains.

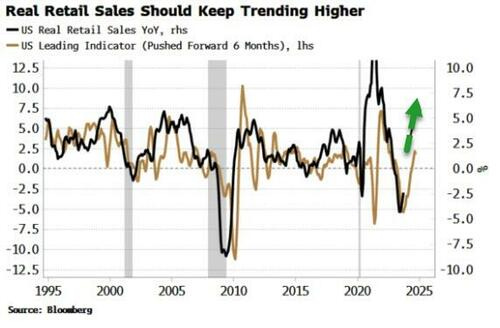

Leading data continue to be increasingly supportive for retail sales.

As is typically the case when positioning is the primary cause of a market move, the narratives play catch up, with only a 0.1% miss in core CPI largely being used to justify that the Federal Reserve is definitely done hiking, and that they will have to make an extra 25 bps of rate cuts next year. Go figure…

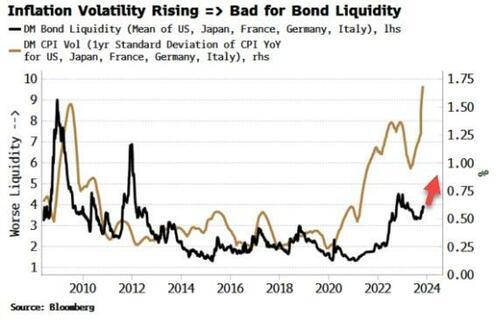

… It is the greatest current source of uncertainty. And contrary to the market’s view, there are compelling signs it will re-accelerate next year. Inflation volatility is already rising (blue line in chart below), and it will remain high if and when inflation reheats. As the chart shows, this means bond liquidity will continue to worsen.

Bonds, as their upside potential is limited, typically exhibit negative skew, i.e. they are exposed to greater moves to the downside than the upside. Combined with poor liquidity conditions and receding recession risk, it means investors will be more wary of downside rather than upside risk – starting with the possibility of stronger retail-sales data later today.

Bloomberg: 5 Things You Need to Know to Start Your Day (Asia edition with chart on inflation swaps and hikes / cuts pricing)

… There is at least one corner of the market which doubts the apparent consensus that the Federal Reserve has tamed inflation. Inflation swaps are quietly signaling concern that the US central bank may be going too easy on the economy.

The 5-year, 5-year inflation swap rate, a key measure that central banks and others use to judge the market’s expectations for future consumer price gains, has been climbing throughout 2023 as the Fed slowed the pace of its hikes. While this week’s modestly soft CPI set off some seismic moves in Treasuries and cash-rate futures, it failed to push swaps out of their uptrend.

These lingering concerns help to explain why some traders were busy resetting shorts on Treasuries overnight, spurring yields higher to unwind some of the post-CPI reaction. It also underscores the danger that a soft landing may elude the Fed. Unless those inflation expectations stage a sustained retreat, the central bank will need to hit the brakes again, which would increase the risks of a much harder endpoint for this business cycle.

Bloomberg’s Ira Jersey (out with 2024 outlook — feel free to make PDF and drop in the inbox :) contained a chart)

Bloomberg: Three Things to Prevent a Treasury Market Meltdown (Dudley’s latest OpED)

… First, someone with a highly expandable balance sheet must provide real, reliable liquidity. To that end, the Fed should allow all holders of Treasuries to access its standing repo facility, where it lends money against the collateral of government securities. This would allow hedge funds and others to raise cash quickly without needing to sell en masse. To ensure it would be used only as a backstop, the Fed should charge a slightly higher interest rate than what normally prevails in repo markets. Instead of trying to interact directly with the broader set of market participants, the Fed could employ primary dealers as agents, without burdening their balance sheets.

Second, the government should require that all Treasury transactions be routed through a central clearinghouse, which stands between counterparties and ensures that adequate collateral is collected. This makes it easier for a broader group of participants to trade directly, without worrying about one another’s creditworthiness. It also consolidates a complex web of bilateral obligations into a much smaller net exposure to the central counterparty, reducing the overall risk in the system.

Third, set initial collateral requirements for leveraged Treasury positions high enough so that they needn’t be increased during bouts of volatility. This would limit the potential for excessive hedge fund leverage and reduce the risk of vicious cycles in which rising collateral demands and forced selling compound one another. The right level would depend on how much regulators want to reduce the probability of distress. If my recommendations on standing repo and central clearing were adopted, the requirements presumably could be less stringent.

Calafia Beach Pundit: Inflation RIP (NO question whatsoever which way this commentator is leaning…)

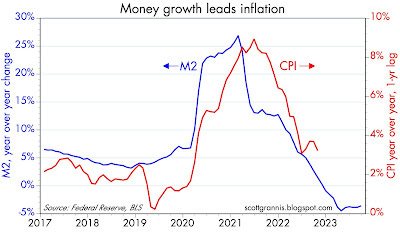

… Chart #4 shows that changes in the growth rate of the M2 money supply tend to show up in similar changes in the rate of inflation with about a 1-year lag. This is strong evidence that the recent bout of inflation we have endured had a monetary origin. As I've explained numerous times in the past year or two, the source of our inflation surge can be traced to the monetization of some $6 trillion in federal deficit spending in 2020-2021. Happily, there has been no further debt monetization since 2021.

… Inflation is dead, may it Rest In Peace.

Is there any reason at all for the Fed to hold off on lowering rates until May? Not that I can see.

Monetary policy is manifestly tight, as reflected in a variety of indicators: 1) a significant deceleration in the rate of nearly all price increases, 2) a 57% plunge in new mortgage originations since early 2022 (i.e., high interest rates have severely impacted the housing market), 3) a 20% decline in non-energy commodity prices since early 2022, 4) at 2.3%, real yields on 5-yr TIPS (an excellent barometer of how tight monetary policy is) are substantially higher than their 28-yr average (1%), and 5) the yield curve is still inverted.

If the Fed remains true to form, they will wait too long to lower rates, just as they waited too long to raise rates two years ago. And that, in turn, means that when they eventually do lower rates, they will have to lower them faster and by more than if they were to start now.

The good news is that there is still little or no reason to think that the economy is at risk. Swap and credit spreads are low, implied volatility is low, initial jobless claims are low, and liquidity is abundant.

Discipline Funds: Can the Fed Finally Declare Victory? (asking / answering RIGHT question and so a quick excerpt)

… Despite this, it’s still way too early to declare victory. Core inflation remains 2X over the Fed’s target rate of 2% and they can’t truly declare victory until they’ve eased rates back down to a more sustainable level. I suspect that level is somewhere in the 2-3% range because that would translate to a mortgage rate of about 4-6% and that’s a figure where the housing market can improve without sparking a speculative fervor and resurgence in inflation. And we’re likely a long way from rate cuts at this point. Historically speaking the Fed doesn’t cut interest rates until core PCE inflation is below 2.5% and we’re not there yet. So it’s all trending in the right direction, but the Fed won’t ease off their current rate positioning for some time. Which, paradoxically, will continue to put pressure on inflation, but will also increase the odds of a deflationary credit event and/or the Fed overshooting and driving unemployment higher than they’d like…

… This has been the most important chart of the year and it will likely be the most important chart in 2024 as well. It shows the peaking of shelter inflation and the way it’s slowly filtering into CPI. This chart was one of the main reasons why we predicted that 2023 would be “the year of disinflation” and it’s why we think disinflation has become entrenched. As we’ve discussed many times in the past the shelter component lags by 9-12 months because of the way the BLS calculates it on a biannual basis. And at a 35% weighting shelter is one the most important pieces of the puzzle here. The wild thing is that it’s still reading 6.7% year over year even though we know shelter has declined at worst and crawled sideways at best in real-time measures. So expect that 6.7% figure to slowly creep back towards something in the 3-4% range in all likelihood and perhaps even overshooting to the downside. And that process is going to take another year which means that barring a commodity surge or another government spending spree the inflation data will continue to have a disinflationary tilt.

LPL: Yields Plummeted on Benign Inflation Report (now a couple days old but…)

Key Takeaways:

Investor risk appetite could increase in the near-term after the October inflation report, similar to the market reaction after the jobs report from a few weeks ago.

Headline consumer prices in October were unchanged month over month, pulling the annual rate of inflation down to 3.2% from 3.7% last month.

Core inflation rose 0.2% from a month ago as housing costs, insurance, and medical care increased in October.

Hotel prices fell in October, likely on the heels of declining demand for travel.

Air fares fell in October as fuel costs declined and competition among airlines put downward pressure on tickets.

Bottom Line: The annual rate of core inflation decelerated to 4%, the smallest rate since mid-2021 and should keep the Federal Reserve (Fed) from raising interest rates at next month’s meeting. Despite the deceleration, the Fed will likely continue to speak hawkishly and will keep warning investors not to be complacent about the Fed’s resolve to get inflation down to its long-run 2% target.

Nautilus: U.S. 5-year Yields Fall -50 Basis Points From the High (yesterday’s notes on 2yy patterns good and today’s hit equally as funTERtaining IMO … and speaks to staying power of significant moves like ones we’ve just witnessed … like back in March)

Yesterday's significant drop in U.S. 5-year treasury yields, marking a decrease of -22 basis points, increased the downward trend initiated since the high point recorded on October 19, 2023, now totaling over -50 basis points. Historical data reveals a noteworthy statistical propensity for rates to sustain their descent. A comprehensive analysis presented in the table below illuminates this pattern, showcasing a tendency for 6-months forward projections of both 5-year and 10-year yields to experience additional declines, averaging -29 and -20 basis points, respectively.

WolfST: Surging “Mortgage Demand” and “Declining Spending,” Really? Let’s Have a Look at Reality (I hate when they do this really wanna believe all is well)

Home buyers “seize a dip in rates” and rush back into the housing market, LOL?

THAT....was Exhausting! And quite satisfying, thanks!

Calafia Beach Pundit Chart #4 would be a delight to Milton Friedman....

Shelter component of CPI, probably has significant measurement error and lag/latency to it.

For example, the statisticians would need to adjust for "get 1 month free on a 12 month lease" deal.

These are beginning to show up in Arizona....

At my apartment there are a lot of vacancies, the most in 5 years...people have moved out,

to live together with someone else......Rent Splitting....

One girl remodeled a van and is living in that, at a campsite...