Reuters: China's frail Q2 GDP growth raises urgency for more policy support

GDP grows 0.8% q/q in Q2, vs 2.2% in Q1, shows slowing momentum

GDP expands 6.3% y/y in Q2 due to low base effects

Frail data raises urgency to unveil more policy steps

Policymakers seen avoiding aggressive stimulus due to debt risks

Then again, it likely doesn’t matter, right? (UBSs words, paraphrased, more details below) but for now, an unprofessional look at 3yr yields as an attmepted reflection of the recent BID,

… here is a snapshot OF USTs as of 655a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the belly of the curve modestly outperforming after China's data dump for June was disappointing (see link above). DXY is modestly lower (-0.10%) while front WTI futures are lower too (-1.45%). Asian stocks were mixed (ex-Japan which was on holiday and ex-Hong Kong which was closed for a typhoon), EU and UK share markets are all lower (SX5E -1.1%) while ES futures are showing -0.1% here at 6:45am. In terms of overnight flows, the London AM session was pretty tame with the market closures in Asia. We saw modest real$ demand for intermediates at the lows but it was enough to lift prices to current levels with Bunds (10's -6bp) trading well too. Overnight Treasury volume was ~45% of average with the market closures with 10's (60%) seeing some relatively high average turnover this morning.

… we've girded for a long stay near current levels for the coming weeks- perhaps into Jackson Hole at the end of next month, and maybe beyond. Our first attachment this morning could reflect this emerging reality(?) as 1y1y vol slides steadily back toward its post-spring banking crisis low.

… and for some MORE of the news you can use » Finviz « worth a point and click …

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ … these first couple notes were sent yesterday morning,

Lower inflation in the US confirmed our expectation that the next big USD move was lower, but positioning could be an important driver of performance.

Q2 earnings season could see European earnings revisions underperform the US for the first time since the Covid reopening.

With little top-line US data this week, inflation in Canada, New Zealand, the UK, and Japan will be key to respective FX performance.

… In rates, the July steepening theme continued, albeit with a bullish flavour that has unwound the early month selloff. A softer inflation trajectory should allow markets to relax about two key risks: the potential need to take policy into ever more restrictive territory and the inability to cut rates on evidence of labor market weakness. We think the front-end rally reflects such a distributional shift.

But the Fed has been vocal in expressing its caution around prematurely easing policy, which leaves us in turn hesitant to chase these inflation-driven steepening moves. We see limited scope for a sustained steepening beyond the forwards for now, as softer-landing outcomes, such as that implied by last week’s data, comparatively weak drivers of curve steepening. Clearer evidence of labor market weakening is needed, in our view, to confirm a shift towards a sustainably bullish rates market regime here …

AND then there was this note detailing the Fed’s journey ahead,

…begins with one step, as the saying goes. The first step in policy normalization for the Fed started over a year ago when the FOMC ended quantitative easing (QE) and started raising rates. The journey to a peak – which looks like the July meeting – has been a bit of a Two-Step, to reprise the dance theme from my piece “Music to My Ears” a couple of months ago. Last week’s CPI print indeed was music to the ears of the Fed and markets. So…what happens next? In particular, when will the Fed start cutting rates and what happens to quantitative tightening (QT)?

On the former, we have pencilled in March 2024, when we think the trend down in inflation will give the Fed enough comfort that we are bound for the target. But if rate cuts come early in the year, what about the balance sheet? Dallas Fed President Lorie Logan made comments recently about how far QT may go.

The Fed has laid out general principles for QT. It is letting $65bn in Treasuries and up to $35bn in mortgage-backed securities run off its balance sheet each month. In conversations with my colleagues and clients, I have heard a frequent refrain that, because the Fed ended QT in July 2019 when it started cutting interest rates in that cycle, it is natural to infer that this time the Fed will end QT when rate cuts start. President Logan’s comments gave policymaker support to my contrarian view that QT will continue.

We should note that Logan was previously portfolio manager at the New York Fed, and consequently knows more about the mechanics of monetary policy implementation than anyone else on the FOMC. In her speech, she made it clear that she does not see QT ending anytime soon, and in the Q&A she was explicit that rate cuts can precede the end of QT.

At the July 2019 FOMC meeting, the Fed cut rates by 25bp and ended QT early. The Committee fretted a bit about the “appearance” of inconsistency in using tools that moved policy in opposite directions. The clinching argument, it turns out, was that the FOMC had already decided to end QT in two months’ time, so it felt that it was close enough. Perhaps as important, the FOMC thought that it was easing policy because inflation was too low, so continuing QT would be moving in opposite directions. But the FOMC does not view the reduction in the federal funds rate expected next year to be policy easing. Rather, against a backdrop of falling inflation and inflation expectations, it sees lowering the nominal policy rate as maintaining a restrictive setting of policy, a point made by former Vice Chair Lael Brainard among others. Through that lens, there is no inconsistency in continuing a passive runoff of the balance sheet while maintaining a restrictive policy stance. Of course, if our baseline view of a soft landing is wrong and the economy falls into recession, then outright easing would be warranted, and I suspect the Fed would stop QT.

I think that President Logan’s remarks emphasizing a desire to contract the reverse repo facility (RRP) are important for another reason. In noting that funding market pressures could arise, and in fact would be desirable to help reduce the RRP, she went on to say that she is comfortable relying on Fed tools like the standing repo facility and the discount window to manage any such pressure. The translation is that the Fed will not be looking to restart QE if repo markets experience stress, as they did in 2019…

MSs Seth Carpenter then offered a bit MORE detail in a longer-from GLOBAL view

Last week's US CPI print confirmed the pattern for falling inflation that we have been looking for, and showed us that the inflation we have seen was frictional, and should resolve itself over time, leaving us with a soft landing.

… It's fair to say that if there was a soft-landing ETF it would have soared last week after soft Manheim auto prices, soft US CPI and PPI, and weekly jobless claims that are edging back down after a recent move higher. It would be crazy to deny the good news however it's worth highlighting that it's still very early in the Fed hiking cycle for a recession to occur and quite early in the yield curve window. There is plenty of time for the usual lags to work before you would say that this cycle is acting massively different to what you would expect given the tightening of policy. This time could indeed be different but it's far too early to say that with any confidence. Until there is something to dispute the soft-landing narrative though, it will undoubtedly be in the ascendancy.

This may be as good a time as any to insert a few words and a visual FROM Bloomberg

… Narratives can flip very quickly. We’re nearing the end of the most dramatic Federal Reserve monetary-policy tightening cycle since the early 1980s. Very few people still active in financial markets can remember trading the Volcker Fed. That’s going to make assets very susceptible to changes in mood over the next few months.

Last week was a great example. Inflation came in lower than expected, which led traders to abandon their previous idea that there might be two more rate increases still to come. The dollar fell and everything else climbed.

Traders now see a much faster easing of monetary conditions on the premise that inflation has been defeated. That means we now need to worry about a coming recession. But the Citigroup US Economic Surprise index is the highest since March 2021, as repeated data points stymie the -- entirely rational -- expectation that a series of huge, rapid rate increases would break something serious in the economy.

CPI fixing swaps suggest that CPI will rise back up to peak at 3.35% in August -- so that second Fed rate hike may end up getting priced back in. The expectation isn’t for a smooth downward glide, but there is a risk that future bumps may cause the dominant narrative to flip again.

This week will be dominated by earnings from both big and regional banks as well as Netflix and Tesla. Morgan Stanley and Goldman Sachs report on Tuesday and Wednesday, respectively. Morgan Stanley has been reducing headcount in its banking and trading group, which doesn’t seem like a good sign. And Goldman has been preparing investors for disappointment and warned of a big writedown from the sale of its ill-starred consumer unit.

Seems to me folks are prepared for and are spiking the football … and when I read stuff like this where EVERYONE, every where, seems ready to declare victory, I can’t help but pause, fearing of becoming this guy … again

AND this on Chinese data overnight,

ABNAmro China: More weakness, more support China Macro: Quarterly growth slowed in Q2, annual growth picked up on base effect. June activity data a bit better than expected. Beijing keeps playing the support card, but in a piecemeal and targeted way.

AND,

Goldilocks - China: Q2 year-on-year GDP growth missed, although June activity data beat (low) expectations

Bottom line: Q2 year-on-year GDP growth surprised markets to the downside, although June activity data beat (low) expectations. Industrial production growth rose modestly in June, against market expectations of further moderation and amid falling export growth. Retail sales and the Services Industry Output Index both reported lower year-on-year growth in June, as base effects became more unfavorable. Fixed asset investment growth beat expectations, thanks mainly to stronger infrastructure and manufacturing investment growth on the back of more policy support. Property-related activity growth broadly weakened in June, suggesting the ongoing (modest) housing easing appears insufficient to offset the strong and persistent headwinds. Despite stable nationwide unemployment rates, the youth unemployment rate rose further in June and we expect it to tick higher in July amid the graduation season. In our view, Q2's meaningful slowdown in sequential GDP growth was driven by the shorter-than-expected reopening impulse, and payback effects from rapid inventory accumulation in Q1. However, some negative factors may fade in Q3 and policymakers have stepped up their easing measures. We slightly revise down our Q3 GDP growth forecast to +5.5% qoq sa annualized from +6.5% previously, with other quarterly sequential growth forecasts unchanged. Accordingly, our 2023 full-year GDP growth forecast remains intact at 5.4%.

… China’s import demand is expected to be rather stable in the coming months. This implies that net exports are expected to contribute negatively in China’s GDP growth.

But wait, before taking ALL of this negativity on CHINA to heart,

China’s second quarter GDP growth was mixed—it slowed as expected, compared to the first quarter, but was quite a bit weaker than expected, compared to the second quarter last year. Does this matter globally? A weaker China may impact the global growth aggregate, but the global growth aggregate is a meaningless statistic. Because China’s domestic demand has been quite service-sector focused, fluctuations in that demand have limited spillover to other economies...

Oh, OK … nothing to see here, then, folks. Simply move along back to your cars. Shows over…there’s simply no THERE there.

With China and EARL in mind, a note from a large German operation attempting to incorporate both,

There was some positivity last week about China’s soft producer price index, which printed lower than forecast at -5%yoy. The hope is that if China returns to exporting disinflation, it could help tame inflation in other countries. Per figure 1, G10 headline inflation has moved closely with China’s PPI over the past 25 years.

But it’s not at all clear that China’s PPI delivers especially insightful information – it simply tracks global commodity prices (a lofty 88% correlation), which can be observed in real time (figure 2). And if anything commodities have been a bit firmer in the past couple of months. Achieving the required disinflation still requires some moderation on the services side, and that's complicated by the robust wage picture, as evidenced most recently with beats in the UK and Japan (figure 3).

Most encouraging on the disinflation front is the notable drops in core CPI for the US and Canada (figure 4). Both are now down 150bps from their respective peaks, boding well for others who are lagging the cycle. Still, there's risk the market becomes over-excited, with US core PCE inflation unlikely to drop as much. And the BoC wasn't getting carried away last week, opting to hike again and noting underlying inflation was appearing 'more persistent than anticipated'.

Moving along through the inbox, a few words on China

BNP Oil: Bearish sentiment on Chinese oil demand is overdone

Current sentiment on Chinese oil demand is too bearish, in our view, reflecting inaccurate reading of monthly oil data and an overreaction to excessively bullish expectations not coming to fruition.

While we think China’s oil demand growth will moderate in H2 from H1’s healthy 1.4 mbd y/y, we continue to assume full-year growth of about 1mbd y/y, supporting our constructive narrative for oil for the balance of 2023.

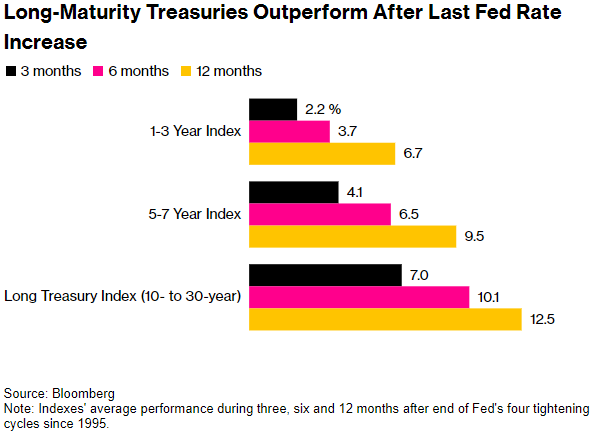

Investors loading up on long-term bonds have history at their back.

For decades, Treasuries maturing in 10 or more years have consistently outperformed shorter-dated sectors immediately following the last in a series of interest-rate increases by the Federal Reserve. On average, they returned 10% over six months after the fed funds rate peaked.

Of course, only in hindsight is it known whether a rate increase is the last one. But investors have embraced the view that an expected quarter-point hike in the target range for the federal funds rate on July 26 will conclude the epic series that began in March 2022. And surveys by Bank of America Corp. and JPMorgan Chase & Co. have found that investors digesting the price action have jacked up their exposure to long-dated bonds.

“We like the idea of extending and adding duration at this point in the cycle,” said Nisha Patel, a managing director of SMA portfolio management at Parametric Portfolio Associates LLC. “Historically, over previous tightening cycles, yields have tended to decline” during the period between the last hike and the first rate cut, she said.

Bonds this week logged their biggest gains since March — when the failure of several regional banks unleashed haven demand — after a report showed consumer prices increased at the slowest pace in two years. Swap contracts that as recently as last week assigned more than 50% odds to another Fed rate increase after this month repriced that to around 20%, and added to wagers on rate cuts next year.

The sentiment shift kneecapped the dollar, which suffered its biggest weekly loss since November. With the European Central Bank and other major monetary authorities expected to remain in tightening mode, there’s probably more downside in store for the greenback, according to strategists at ING Bank N.V.

In bonds, the biggest moves in yield were in short- and intermediate-maturity tenors where expectations for Fed policy are expressed. The five-year rate tumbled nearly 35 basis points, compared with just 13 basis points for the 30-year.

But long-dated bonds’ greater price sensitivity to a given change in yield means investors can reap bigger rewards. On average, Treasuries maturing in 10 or more years have gained 10% in the six months after a Fed policy-rate peak, compared with 6.5% for bonds maturing between five and seven years and 3.7% for those due within three years, according to data compiled by Bloomberg. In 12 months, the longest-dated bonds returned 13%, outpacing the other sectors.

“There is finally income to be earned in the fixed-income market,” BlackRock President Rob Kapito told analysts Friday, calling the higher yields a “remarkable shift” and a “once-in-a-generation opportunity.”

As an end-of-cycle theme, it’s proven more reliable than wagering on relative changes in yields such as the one that occurred this week as two- to five-year rates dropped more than longer-dated ones, producing a steeper yield curve.

The difference between two- and 10-year yields increased in the six months after the Fed concluded a tightening cycle in December 2018, but it narrowed following the end of one in 2006.

“Going long duration at the end of the hiking cycle is a more consistent trade than the steepener, which is more conditional on a harder landing outcome from the Fed,” Bank of America’s strategists including Mark Cabana and Meghan Swiber wrote in a note.

A Bank of America investor survey conducted monthly since 2004 found that respondents had amassed a record amount of interest-rate risk relative to their benchmarks in June before trimming a bit this month.

“I love duration here,” said Eddy Vataru, a fixed-income manager at Osterweis Capital Management. Inflation, which cooled to 3% last month, its 12th straight drop from a peak of 9.1% last year, has scope to fall below 2%, he said.

To be sure, Fed policymakers remain on guard. Their quarterly forecasts for the policy rate released in June had a median expectation for two additional increases this year. Fed Governor Christopher Waller Thursday said he agreed with that even after the latest inflation reading as the labor market remains very robust.

Even if employment strength induces the Fed to keep tightening beyond July, investors may pile into Treasuries because yields are high enough to be a compelling hedge against a possible recession, said Michael Franzese, head of fixed-income trading for New York-based market-maker MCAP LLC.

“You have a lot of investors looking now to make a bet and buy” if yields move back up, he said. “We may see a wave of new buying coming in, as Treasuries are an asset that could start to accrete really well for investors when the Fed does eventually start cutting.”

Interesting food for thought…

Ultimately it all comes down TO the Fed and for some further CLARIDA-FICATION (highlight OF the nearly 3min clip about half way in … where Rich talks about the Fed not wanting to BE Charlie Brown — again).

Clicking on visual SHOULD open up clip but if not, HERE is link … AND a reminder, posts to become few and far between (likely AFTER tomorrow) AND … THAT is all for now. Off to the day job…

Trading the Volker Fed...has a nice ring to it! Rumor has it US markets haven't traded the same since that fateful 1987 late October "flash crash"; after which the Presidential Commission of Markets (aka PPT) was created. Something like that anyways. Thanks for the great read!

Trading the Volker Fed...has a nice ring to it! Rumor has it US markets haven't traded the same since that fateful 1987 late October "flash crash"; after which the Presidential Commission of Markets (aka PPT) was created. Something like that anyways. Thanks for the great read!