Given so many out with calls to BUY ‘em, I thought a fitting way to start the day and week and as Mom always said, if you don’t have anything NICE to say, then don’t say anything at all, right? SO … have a look at that overSOLD momentum rolling over and crossing BULLISHLY? Dunno. I’m unconvinced and can’t help but think there’s gonna be much more to the day and week ahead (supply, X-Dates, speakers, etc) and so make of the charts whatever you will …

In as far as SPEAKERS are concerned, well you know how they say that ALL opinions are created equally but we know in practice, some opinions are, well, MORE equal? WSJ

Essentially detailing how / why Kashkari(V), is open to skipping a rate hike next month … And so, NOT A PAUSE but one can’t help and ask ‘bout that roadmap to a June HIKE … Never mind … lets get on with it and so, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher this morning after Yellen and others have warned that Treasury was unlikely to make the mid-June tax payment date while Fed hawk Kashkari, a voter, said over the weekend that he might be talked into skipping a hike next month (link above). Also interesting was that in Yellen's X-date warning she broached the topic of payment prioritization (rather than default) for what we think is the first time this debt ceiling cycle (see in text below). DXY is lower (-0.12%) while front WTI futures are little changed here at 6:15am. Asian stocks were mostly higher, EU and UK share markets are mixed while ES futures are showing UNCHD here at 6:15am. We were too early for the flow color from the regions but overnight Treasury volume was ~85% of average overall with 5's (118%) again seeing some relatively high average turnover among the Tsy benchmarks.

… Treasury 2yrs, daily: Solve for 2's and you solve for most benchmarks in US rates right now? We put this in to show our marked-up 2y chart and why we said above that we saw risks for false bearish breakouts late last week. Note that daily momentum in the lower panel shows the oscillator lines are beginning to merge (hint of more balanced flows after the multi-week sell-off) while sitting at 'oversold' levels. No bull/Buy signal in 2's yet but we sense that we haven't seen the last of 3.99% prints in 2yrs yet, lol.

… and for some MORE of the news you can use » IGMs Press Picks for today (22 MAY) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

In the case you missed YESTERDAYS note with THIS LINK thru to sellside weekly narratives, well, start there.

In as far as here and now goes, a few items from this mornings inbox starting with the dismal science, economics

Wells, Oh, the Places You'll Go: Inflation Edition - Since the Fed embarked on its tightening campaign a little over a year ago, the inflation picture has in some ways improved and in others ways grown more concerning. It is clear the rapidly rising price environment is not "transitory" as the Fed thought in 2021, but just how sticky might inflation prove to be? To help navigate the uncertain road ahead, we lay out three scenarios for inflation over the next 12 months … Baseline: A demand-sapping recession and gradual unwinding of pandemic-era supply issues help put inflation firmly on a downward path, but are not enough to get core inflation back to the Fed's target on a sustained basis by Q2 of next year.

From some of the places you’ll go TO a very worldly outlook,

MSs Seth Carpenters latest Weekly Worldview: What's Eating You? Food inflation in the UK is set to fall quickly, but the decline will likely be much slower in the US

… Very recently,however, it seems those margins are compressing anew,giving rise to greater disinflation for food. In the US, initially, less of the spike in commodity prices was passed through to consumers,and now, the margins appear to be catching up….

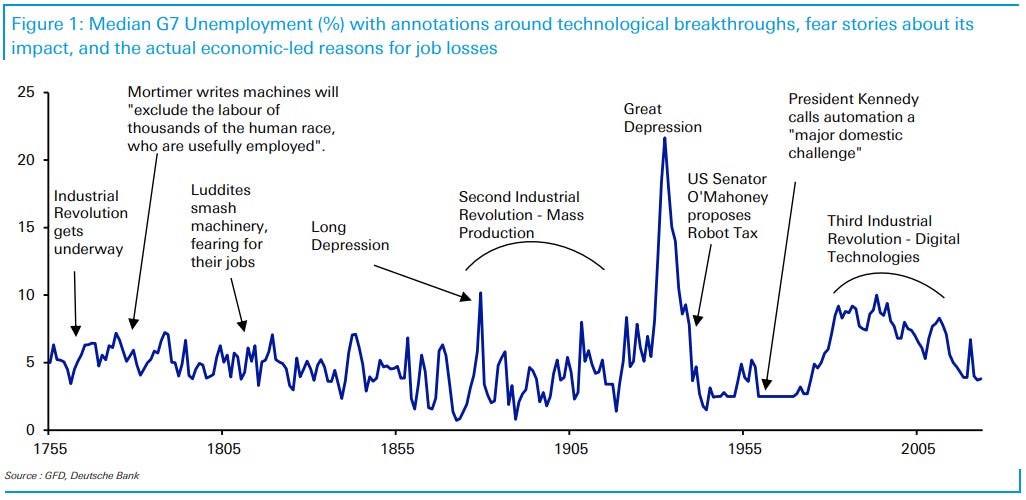

And a most interesting ‘take’ on AI and how history (doesn’t repeat but often rhymes) will CREATE not destroy jobs,

DB: History suggests AI will ultimately create not destroy jobs

… So contrary to the rolling fears of the last several hundred years, history tells us that technology does not create unemployment. We can illustrate this by looking at long-term unemployment data, using the median of the G7 countries. At first there's just data for the UK, but the others are gradually included as they become available. It clearly shows that unemployment has oscillated based on economic cycles, rather than any technological waves. In fact, today's median G7 unemployment rate of 3.8% is beneath the 5% UK rate at the start of the series in 1755. So even though most of the jobs of 1755 no longer exist, the automation of different tasks did not lead to an ever-increasing spiral of unemployment.

And on STOCKS,

MSs weekly kickstart: Great Expectations - With the S&P 500 testing the upper end of its trading range, are we on the cusp of a breakout that confirms a new bull market? We don't think so and present technical and fundamental evidence to support our view. The debt ceiling remains a key risk even if a deal is made—i.e., sell the news.

… Exhibit 4: 3800-4200 Range on the S&P 500 Being Tested to the Upside on Potential Debt Ceiling Deal—We Think It's a Bull Trap

On debt ceiling,

Barcap: U.S. Equity Strategy: The U.S. Debt Ceiling: Here We Go Again … Risk of a default appears low, and overall impact is likely to be modest if a deal is reached. We introduce 5 tracker baskets of exposed names and recommend 2 hedges.

AND … on earnings,

Barcap: U.S. Equity Insights: Earnings Learnings: Not so Great Expectations - Earnings quality in 1Q23 improved from 4Q22, although beats were helped by substantial downward revisions into the print. Overall, we think expectations for 1Q23 were too negative, but remain skeptical around full-year estimates as there has been little flow-through of current quarter beats and margins remain under pressure

AND … I’m done. Fed and fiscal policy makers cannot WAIT for data which echoes out the following in real life terms,

AND the risk is it’s NOT happening as soon as they’d like (?) forcing hikes and matters to become much worse, then, before they can be made less worse. Election season is coming and so, don’t forget to get those votes in early and often ?