Good morning … Missed this over the weekend and MIGHT be of some funTERtainment value ahead of CPI Thursday …

RTRS: Fed's Bowman says more US rate hikes likely will be needed

"I also expect that additional rate increases will likely be needed to get inflation on a path down to the FOMC’s 2 percent target," she said in remarks prepared for delivery to the Kansas Bankers Association, referring to the Fed's rate-setting panel, the Federal Open Market Committee.

… BUT likely will NOT be of ANY use into DURATION SUPPLY in the week ahead which will put the FUN back into reFUNding … Before we get TO the (in)digesting of bond supply, a look at the front end …

DAILY momentum from overSOLD to about a push as yields hang around nearer the cheap side of the range. For somewhat MORE context, a MONTHLY look …

… where you can see some of the very same levels of interest (5.08 and above there just north of 5.25%) and here I’d note momentum remains OVERSOLD as rates pricing in a PAUSE. Here and NOW.

Something IN Friday’s NFP for everyone (some of the SPIN noted over the weekend HERE) and if I had to choose only ONE sellside weekly offered it would likely be MSs “Narrative Marketplaces” which notes,

If narratives can determine economic outcomes, then they can move markets, rightly or wrongly. And they have, wrongly. Higher rates post-BoJ, Fitch downgrade, and US Treasury refunding resulted from commonplace narratives that reflect misguided perceptions that became reality for the bond market.

Sidebar to note firm remains ‘max long USTs (staying long 5s, in FFV3H4 flatteners) and lookin’ to buy Feb 50 TIPS).

Many moving parts and not MUCH talk of which way the inflationary winds are blowing with regards to OIL and which way Fed goes next is, at the moment, anyone’s GUESS (despite what they think they think) … Meanwhile … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are cheapening led by the 5y point, light volumes and activity impinged by Canada/Australia holidays. Weaker EU Sentiment and German IP (-1.5%MoM) is compelling UST underperformance once again, bear-flattening paring back post-NFP gains globally. The bulk of the G10 FX complex is slightly weaker against the USD, JPY leading losses at -0.3% after the BoJ summary of opinions failed to reveal materially new details. The pop in US front-ends (1y1y +8.5bps) is coming despite rather dovish indecisiveness on the part of the Fed’s Williams (NYT interview link above), with supply concerns top of mind this week (103bn of 3s/10s/30s). Real yields are logically in charge of the back-up, TIPs BE’s largely unch’d this morning ahead of July CPI out Thursday. Citi economics expects another soft 0.196%MoM SA increase in core CPI based on a decline in used and new cars and a modest increase in airfares. Volumes are around 80% this morning, 3y cash trading a bit more active ahead of supply at ~120% the 30d average.

… and for some MORE of the news you can use » The Morning Hark - 7 Aug 2023 — to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use (and in addition TO all the NFP recaps and victory laps offered this past weekend) … here’s some of what Global Wall St is sayin’ and thinking …

We had two US payrolls and two inflation releases to get through before the next FOMC in September and although the first of these on Friday was a mixed affair, it did trigger a big rally across the US rate curve with 2yr and 10yrs -11.7bps and -14.1bps tighter, respectively, on the day even if yields were still higher at the long-end on the week. We'll review the main payroll highlights below but with that out the way we move on to the next big one, namely US CPI on Thursday. PPI follows fast behind on Friday alongside the University of Michigan consumer survey which contains the all-important inflation expectations series. In Europe, the focus will be on GDP numbers in the UK (Friday), industrial production in Germany (today), the ECB's Consumer Expectations Survey (tomorrow) and China CPI/PPI (Wednesday). Corporate earnings wind down quite sharply with 33 S&P 500 and 55 Stoxx 600 companies reporting this week…

… In conclusion there was no real conclusion from the report. There was something for everyone. Unless there's a sudden shock though, any path to a hard landing is likely to be via signs of a soft landing first but the bulls will say that's where it will stop. You pays your money and you takes your choice.

So next stop is US CPI on Thursday. One thing to bear in mind for inflation over the next few months is the +15.8% gain in the WTI crude price last month. Gasoline prices are rising fast too. Too early perhaps to make much inroads yet but a complication if prices stay elevated. In fact, for now, with seasonally adjusted gas prices down a bit from June, our economists expect a slightly weaker headline (+0.17% forecast vs. +0.18% previously) reading relative to core (+0.21% vs. +0.16%). This would equate to 4.8% YoY for core (though it is very close to rounding down to 4.7%), however, shorter-term trends should show significant improvement. The three-month annualised rate should fall by about 80bps to 3.3%, while the six-month annualised rate should fall by 40bps to 4.2%, both the lowest in over two years…

GS US Economics Analyst: The Corporate Debt Maturity Wall: Implications for Capex and Employment

The Fed’s tightening cycle has pushed marginal funding costs for businesses sharply higher over the past couple of years, with yields jumping almost 5pp for high yield bonds. If interest rates remain high, companies will need to devote a greater share of their revenue to cover higher interest expense as they refinance their debt at higher rates. We explore the magnitude of this looming increase in interest expense and the potential impact on capital spending and hiring.

The path for interest expense depends on future refinancing needs and interest rates. Refinancing needs will remain historically low over the next two years—about 16% of corporate debt will mature over the next two years. The interest rate on refinanced corporate debt will increase substantially because current market rates are roughly 1½pp above the average rate that companies are paying on existing investment grade bonds and 2pp above the average rate on high yield bonds.

We estimate that the average interest rate on the current stock of corporate debt will rise from 4.20% in 2023 to 4.30% in 2024 and 4.50% in 2025, based on our assumptions about the future path of Fed policy and market interest rates. This would imply that private sector interest expense as a share of current private sector gross output will rise from 3.35% in 2023 to 3.40% in 2024 and 3.60% in 2025, an increase of 0.25pp from 2023 to 2025.

We find that for each additional dollar of interest expense, firms lower their capital expenditures by 10 cents and labor costs by 20 cents. The increase in interest expense that we estimate would therefore reduce capex growth by 0.10pp in 2024 and 0.25pp in 2025 and labor cost growth by 0.05pp in 2024 and 0.15pp in 2025. Our estimates suggest about half of the reduction in labor costs comes from reduced hiring and half from lower wage growth, implying a 5k drag on monthly payrolls growth in 2024 and a 10k drag in 2025.

We see reasons why the hit from higher interest expense could be either smaller or larger than usual. On one hand, cash balances are historically high, which could help buffer the hit. On the other hand, the number of unprofitable firms has continued to proliferate, as the exit rate of unprofitable firms has declined since the start of the pandemic. In previous research, we have found that unprofitable firms disproportionately cut back on capex and employment when faced with margin pressure.

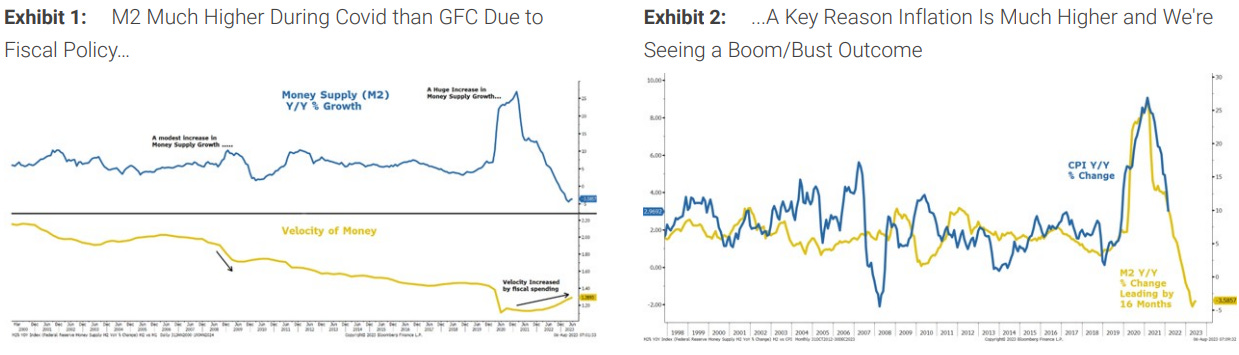

Fiscal dominance has been a key component of our boom/bust framework. This year, another strong fiscal impulse has reasserted itself but has it gone too far, too fast? Should it reverse, it could call into question the significant reacceleration in growth that is now priced.

… At the trough of the Pandemic Recession in early April 2020, we introduced our thesis that the crisis would usher in a new era of fiscal policy dominance (see Cyclical Bear Ending; Secular Bull to Resume April 6, 2020). The result would be the higher inflation that monetary policy had been unable to achieve on its own over the prior decade. In the first phase of this new policy regime, we called it “helicopter money,” a term Milton Friedman first used in the early 1970s and Ben Bernanke highlighted after the tech bubble as a policy that could be employed to avoid a deflationary bust. Of course, handing out checks is generally not politically acceptable, except in a true emergency. The COVID pandemic clearly fit this description.

The policy shift worked so well at keeping the economy afloat during the lockdowns that the government decided to double and triple down on the strategy. Excessive fiscal policy is why money supply growth exploded to a record level of ~25%Y in early 2021, and why we finally got the inflation central banks had been trying so hard to achieve post the Great Financial Crisis. After the GFC, the velocity of money collapsed while the Fed’s balance sheet ballooned to levels never seen before. The reason we didn’t get inflation in that initial episode of quantitative easing is that the money created remained trapped in bank reserves rather than flowing into the real economy, where it would drive excess demand and higher prices – a dynamic that has been very different this time.

The Fed has responded to this generationally high inflation with the most aggressive tightening in 40 years. But this is the definition of fiscal dominance – i.e., monetary policy is subject to the whims of fiscal policy. First, the Fed had to be overly supportive and help to fund the near-record deficits in 2020-21; then it had to react with historically tighter policy once inflation became too elevated. Back in 2020, we turned very bullish on equities on this shift to fiscal dominance. Subsequently, we also indicated that it would lead to a period of hotter but shorter economic and earnings cycles, mainly because the Fed would not have the same flexibility to proactively extend economic expansions (see This Cycle Could Run Hotter but Shorter, March 16, 2021). We also argued that catching these boom/bust cycles would be critical for equity investors to generate strong real returns. Part of the reason we’ve found ourselves offside this year is that the fiscal impulse returned with a vengeance and remained quite strong in 2023 – something we didn’t factor into our forecasts. In fact, we have rarely ever seen such large deficits when the unemployment rate is so low (Exhibit 3). A question to consider—if fiscal policy is showing such little constraint in good times, what happens to the deficit when the next recession arrives?

The hard-fought battle against inflation by central banks has climaxed in Latin America, with Brazil and Chile starting their easing cycle. We look at the read across LatAm and other markets as central banks start to pivot.

Last year, we released a three-report series that outlined a couple methods to predict recessions and monetary policy pivots. Today, all three major tools still signal a recession within the next year. Despite the odds of a soft landing rising amid resilient economic data, the framework aligns with our base case expectation for a mild recession in early 2024.

… The second tool is the spread on the 10-year and 1-year Treasury yields. Using a recession-prediction threshold of two consecutive months of inversion, the yield spread has predicted all the past 10 recessions, with an average lead time of 12 months. Through July, the spread has been negative for 13 straight months (Figure 2), signaling a recession is indeed on the horizon.

The final tool is a threshold method that uses the 10-year Treasury yield and the federal funds rate (FFR). In a rising interest rate environment, we found that when the FFR crosses the lowest 10-year yield in that cycle (the threshold), a monetary policy pivot is likely to ensue in the next 18 months. As shown in Figure 3, the FFR crossed the 10-year's current cycle low back in March 2022, when the FOMC kicked off its tightening cycle. The FOMC decided to hold rates steady in June, 16 months following the threshold breach. While the FOMC elected to hike the FFR by 25 bps to a target range of 5.25%-5.50% in July, the threshold approach suggests a pivot to an accommodative stance is in the offing, which historically occurs amid slowing economic growth.

In sum, all three tools signal a recession within the next year. Despite the odds of a soft landing rising amid resilient economic data, the framework aligns with our base case expectation for a mild recession in early 2024.

Finally, something of an issue — a wildcard, if you will — for those betting on the end of HIKES and for rate cuts soon

… Rising crude oil prices will add to upward pressure on global bond yields. Macro traders had probably given up on Brent futures returning to $90 a barrel this year. But that looks like the path it’s taking, with forecasts for crude at $100 starting to make a comeback after Saudi Arabia extended its oil production cut by another month.

The high for 10-year Treasury yields in this cycle coincided with Brent ~$93 back in October. That point is less than 30 basis points away and Treasuries still have to face a bumper auction schedule in the weeks ahead. With investors edgy about the path of the US fiscal deficit, adding higher oil into the mix could send Treasury yields into an altogether higher range.

The read across for the US dollar from rising oil and yields is more nuanced. Firm commodities have been a US dollar negative in the past, while inflated bond yields typically support the dollar. Near-term dollar direction may come down to which narrative looks likely to sustain. For now that appears to be rising Treasury yields as investors digest the grim outlook for the US with the risk of its debt-to-GDP ratio heading toward 130%.

Have a GREAT start to the day and week ahead and … THAT is all for now. Off to the day job…

I don't understand why this Sub doesn't get more comments/commenters. Over at Simplicius The Thinker, my word 100's of comments and some of the lengthy exchanges we've had of late! But then we talk Ukraine War and all it's moving parts entails. I guess War & Geopolitics get the blood flowing more than boring old BONDS. I don't find BONDS boring, quite the contrary. Some of those 25 bps moves last wk were rather Epic and Remarkable. Sure wasn't boring when BoE was in Panic Mode last October. Folks are asking for economic resources at Simplicius, I'm spreading the word. Sub RIA for your mornings 1st take and warm up, then buckle in for a good 15 mins at least w/the Bond Beat Man. Simp's been on the top 10 growing Substacks list, maybe we can lure a few good folks over here.

Good folks over there too, but some could use your/our economic expertise!

Excellent work !!

I don't understand why this Sub doesn't get more comments/commenters. Over at Simplicius The Thinker, my word 100's of comments and some of the lengthy exchanges we've had of late! But then we talk Ukraine War and all it's moving parts entails. I guess War & Geopolitics get the blood flowing more than boring old BONDS. I don't find BONDS boring, quite the contrary. Some of those 25 bps moves last wk were rather Epic and Remarkable. Sure wasn't boring when BoE was in Panic Mode last October. Folks are asking for economic resources at Simplicius, I'm spreading the word. Sub RIA for your mornings 1st take and warm up, then buckle in for a good 15 mins at least w/the Bond Beat Man. Simp's been on the top 10 growing Substacks list, maybe we can lure a few good folks over here.

Good folks over there too, but some could use your/our economic expertise!