Update (0910ET): We hate to be the ones to steal the jam from the exuberant consumer's donut BUT on a non-seasonally-adjusted basis, retail sales actually crashed 5.4% MoM in September - that is the biggest drop for September since 2019...

On a YoY basis, it's not as dramatic - as one would expect, with retail sales up 3.4% NSA (vs 3.8% SA)...

MORE from Global Wall Street in the form of recaps and victory laps below. We also got a look at Industrial Production …

ZH: US Manufacturing Production Lower YoY For 7th Straight Month

Not new news, per se but a story from BBG to consider ahead of supply …

BBG: Long-End Treasuries Hit by Wildest Swings Since 2020 Pandemic

US 30-year yield moves averaged 13bps in last five sessions

Long-dated yields remain near highest levels since 2007

… “If the front-end is pegged with the Fed not moving, these moves are going to be hitting longer-end yields,” said Blake Gwinn, head of US rates strategy at RBC Capital Markets. At the same time, “focus on supply and deficits has gone up massively.”

The daily yield fluctuations that occurred in March 2020 were caused by a global flight to cash at the onset of the pandemic. Shorter-maturity Treasuries earlier this year experienced daily yield shifts that rivaled or even exceeded those, as several US regional bank failures cast doubt on Fed interest-rate increases…

If you loved ‘em at 5% then you’re gonna love ‘em nearly 5.25% (see above, not really that far away) AND… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are bull-steepening in a quieter London morning, px-action complicated by a worse geopolitical tone (CL +2.6%, XAU +1.5%). USTs are outperforming EGBs on the announcement of Austria’s syndication tomorrow and UK Headline CPI marginally exceeding expectations (6.7%YoY vs 6.6% exp). A 340k/01 FV/US steepener and several small FV block buys in the Asia session set the tone for re-steepening overnight, 5s30s +4.5bps, as a crowd of Fed speakers come to bat prior to the comms blackout (Waller, Williams, Bowman, Barkin, Cook, Harker again). The DXY is unchanged here at 7:15am, S&P futures off by ~18pts.

… and for some MORE of the news you can use » The Morning Hark - 18 Oct 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in a similar sorta way you’ll find content if you pay for ZH PREMIUM? except … they are SELLIN other folks data where as I’m just point it out and links provided — should work IF you have permission and should NOT work if you don’t … HOW can THEY do that?? askin’ for a friend as I never understood how they do it…)

ABNAmro- China - Q3 GDP and September data confirm bottoming out

China Macro: Quarterly GDP growth picks up in Q3. September activity data: Property sector weakness continues.

Apollo - P/E Ratio for S&P7 vs S&P493 (i’m not now and never have been an equity ‘analyst’ but seems pretty straight forward and common sensical here to ME … what say YOU degenerates reading this note today :) ?)

The P/E ratio for the S&P493 has fluctuated around 19 in 2023.

And the P/E ratio for the S&P7 has increased from 29 to 45, see the first chart below.

The bottom line is that returns this year in the S&P500 have been driven entirely by returns in the seven biggest stocks, and these seven stocks have become more and more overvalued.

What is particularly remarkable is that the ongoing overvaluation of tech stocks has happened during a year when long-term interest rates have increased significantly. Remember, tech companies have cash flows far out in the future, which should be more negatively impacted by increases in the discount rate.

The conclusion is that tech valuations are very high and inconsistent with the significant rise in long-term interest rates, see the second chart.

In short, something has to give. Either stocks have to go down to be consistent with the current level of interest rates. Or long-term interest rates have to go down to be consistent with the current level of stock prices.

Source: Bloomberg, Apollo Chief Economist. Note: 12-month trailing P/E ratio used.

BAML - US Rates Watch: Inflows accelerate, fund performance suggests modest repositioning (the ‘ole Curve-O-meter, eh…)

Auction block Fund inflows remain intact across the UST curve and funds overall appear to be curbing short duration views based on relative performance. However, most recent auction data shows a modest reduction in the dominance of investment funds. This week’s 5y TIPS and 20y bond auction will be watched for any signs of a bid pullback as observed at last week’s 30y auction. While nominal UST funds have overall seen very strong inflows, TIPS funds have observed persistent outflows.

Positioning points to continued bias for steeper curve…

BAML - Global Fund Manager Survey: Reverse Leverage

… 75% of FMS investors expect the yield curve to steepen in the next 12 months in Oct’23 (vs 77% last month), a proportion on par with the highs observed in Nov’08 (GFC), Nov’16 (US presidential election), although below the record high of 87% in Feb’21

56% expect bond yields to be lower, the highest share of respondents on record (back to 2003)

Barclays - September retail sales: Shop 'til ya drop

Retail sales defied expectations with a large September gain, putting consumer spending on very strong footing entering into Q4. The latest print comes on top of a series of stronger-than-expected readings for nearly all major indicators since the September FOMC meeting, so pre-blackout FOMC communications will be in focus.

Barclays - China: Target is within reach, but devil is in the detail (always in details)

Higher-than-expected official Q3 GDP data implies this year's ~5% growth target is within reach. However, we see signs of moderation in sequential momentum, with softer m/m sa growth in IP and retail sales. We note some discrepancies in official data that may not be fully capturing underlying developments in the economy.

… First, housing data could be worse than official data suggests…

Second, there appear to be some discrepancies between official m/m growth (or q/ q) and y/y growth rates…

Third, price indicators paint a more gloomier picture than September/Q3 activity data …

We think the ingredients are in place for a potential extension higher in inflation breakevens following the recent rally to the top end of the range.

The Fed’s renewed focus on financial conditions coupled with firm fundamentals can allow for more breakeven upside. Importantly, for now the burden of tightening seems to have shifted towards market forces responding to the evolution of the cycle (rather than the Fed moving proactively to increase restriction).

The risk of a negative supply shock amid geopolitical uncertainty further strengthens the case for real over nominal exposure.

Bloomberg BNP - US: Tighter financial conditions allow Fed to be patient

KEY MESSAGES

Recent tightening in financial conditions reduces the need for the Fed to hike again, and at minimum allows the central bank to be patient at coming policy meetings.

The latest move in the BNP Paribas US Financial Conditions Index (if it persists) may equate to 40bp of tightening via the fed funds rate -- or 10bp per 0.1 point move in our index.

Higher Treasury yields are a key factor behind the move in our index, a development the Fed will see as keeping the brakes engaged.

We remain of the view that lagged effects of past tightening will coincide with other negative catalysts (dwindling excess savings, restart of student loan payments) to drive a sharp reduction in the pace of economic activity starting in Q4.

DB- China Macro - Q3 GDP beats as consumption strengthens

China's Q3 GDP growth came out stronger than expected at 4.9% YoY, higher than consensus forecast of 4.5% and our forecast of 4.6%. Sequential growth accelerated to 1.3% QoQ in Q3 from 0.5% in Q2. Consumption and services sector were the main drivers of growth, while investment and property sector activities still lagged.

The latest data confirms that that China's economy has passed a bottom. We revise up Q4 GDP growth forecast to 5.3% (from 5%) and 2023 annual growth forecast to 5.2% (from 5.1%). As the government's 5% growth target is now within reach, the urgency of additional stimulus is likely reduced in the near term. The government may still need to do more in the next few months to boost property demand and prevent price deflation. Other than those, it is time to look beyond this year and think about the policy goals for 2024.

Goldilocks - Retail Sales Rise Further; Industrial Production and Business Inventories Above Expectations; Boosting Q3 GDP Tracking to +4.0%

BOTTOM LINE: September retail sales rose 0.7% and core retail sales rose 0.6%—both above expectations—and spending was revised higher in prior months from already-strong levels. Combining data from the latest retail sales and CPI reports, we estimate that real core retail sales rose 0.7% in September (mom sa). Industrial production rose 0.3% in September and manufacturing production increased 0.4%, both above expectations. Business inventories increased in August, slightly above expectations. The September retail sales report was stronger than our previous assumptions. We boosted our Q3 GDP tracking estimate by three tenths to +4.0% (qoq ar) and our domestic final sales growth forecast by four tenths to +2.8%.

ING - US retail sales confirms 4% GDP growth is on the cards

A robust US retail sales report for September plus upward revisions to August's report reinforce the view that the US economy likely expanded at a 4% annualised rate in the third quarter. Headwinds are set to intensify, but for now the US consumer continues to defy the odds

… Data surprises keeps the upward pressure on borrowing costs So why have economists got it so wrong, yet again? Well, the weakening trend we are seeing in consumer confidence is one factor as households continue to worry about the economic outlook and what might happen in the jobs market at a time when spending power is under pressure from lingering inflation. Another reason is that the Bureau of Economic Analysis now publishes weekly credit card spending transaction usage and this was down sharply in September. Given this is how most people typically spend money, especially on-line, this should give a good read through for general spending patterns. For auto sales it will obviously be different, but this discrepancy is surprising as it is doubtful we will all suddenly be using cash again.

JPM - The J.P. Morgan View: Adding marginally to bonds and gold (noted)

Cross-Asset Strategy: Markets remained under pressure over the past month, but rebounded from their lows near the start of October. Following the recent sell-off, we expect the market to trade in a broader range, but medium term remain negative as headwinds for markets are getting stronger and tailwinds weaker, in our view. Stillrich equity valuations face increasing risk from high real rates and cost of capital, while earnings expectations for next year appear overly optimistic. Weakening PMI momentum suggests that Q3 earnings growth is likely to be negative, while softening corporate pricing could lead to a squeeze on margins. Lags in the impact of high rates are longer this time, but we believe most of the negative effects are still to come. Delinquencies in consumer loans and corporate bankruptcies are starting to move higher, and this trend is likely to continue absent a cut in rates. The flare up of geopolitical risks adds another headwind and increases tail risks for markets and economic activity. Our outlook is likely to remain cautious as long as interest rates remain deeply restrictive, valuations expensive, and the overhang of geopolitical risks persists.

Given the above, we maintain a defensive allocation in our model portfolio, with an UW in equities and credit vs. OW in cash and commodities. This month, we reverse last month’s well-timed cut to our model portfolio’s duration exposure. While it remains uncertain whether bonds have bottomed, we add back 1% to our government bond allocation given geopolitical risk, cheap valuations, and less pronounced positioning. We additionally increase our allocation within commodities to gold, both as a geopolitical hedge, and given an expected retracement in real bond yields…

… Last week’s Fed speak gave a consistent message that the Fed is likely to stay on hold in November (Figure 9Last wek’onfrm Fedspch turnedls hawki). Last week opened up with some notable speeches from Logan and Jefferson which focused on the tightening in financial conditions related to higher bond yields. These comments were later reinforced in another speech by Governor Waller where it was noted that rising yields will do some of the Fed’s work, and that the Fed is in a position where “we can kind of watch and see what happens on rates.” Against this backdrop, the minutes from the September FOMC meeting looked somewhat stale. The minutes largely reiterated the hawkish bias towards tightening and also reinforced previous communications that monetary policy should remain “restrictive for some time” until the Committee is confident inflation is moving back to target.

MS - The Real Drivers of the US Treasury Bond Market Rout (questions answered. no, not really but I was hopeful)

Explanations for the recent US Treasury curve bear-steepening and increased term premiums include technical and fundamental factors. The FOMC rarely enters the discussion - specifically, its reactions to data and subsequent forward guidance, both of which we think explain the majority of the rout.

Bottom line: Without the Fed's more hawkish reaction function to recent growth and inflation data, in the context of a deeply inverted yield curve; other technical and fundamental drivers would not have contributed that much to higher Treasury yields, in our view…

… Supply falls flat: If the supply of US Treasury duration drove the yield curve steeper, we would expect to see nominal Treasuries substantially underperform overnight index swaps (OIS) that tie directly to the effective fed funds rate - especially in longer maturities/tenors, i.e., we would expect the UST-OIS spread curve to steepen. But that didn't happen either…

… Reasons to buy or sell: In spite of the negative carry that comes with an inverted yield curve, investors still might buy Treasury notes and bonds for a few reasons (detailed within). However, the Fed's reaction to economic data and consequent forward guidance negated each reason to buy and, instead, provided reasons to sell: the risk of more and longer-lasting negative carry.

MS - US Housing: What If Mortgage Rates Stay Higher for Longer? (NOW yer talking … but really only asking more good questions…)

Mortgage rates have approached 8% for the first time since 2000. The resulting affordability pressures are weighing on both supply and demand. If rates remain here, we think the impacts on the housing market will differ in the short term and the long term.

Affordability Pressure: Mortgage rates have reached their highest level since 2000. When combined with the resiliency in home prices, the impact on affordability has been severe. By our calculations, the monthly payment on the median priced home is up 27% over the past year. If mortgage rates were to stay at 8%, affordability deterioration would return to the most severe we have seen in decades, the 2022 experience notwithstanding….

Exhibit 1: Affordability has resumed deteriorating, and if mortgage rates were to reach 8%, the deterioration would once again be at its highest level in decades

Retail sales post a chunky upside surprise in September … Among the components, decent gains were spread across several categories. Non-store retailers (on-line sales) climbed 1.1% in September continuing a brisk pace averaging over 1% increases per month the last six months. Eating out perked up, rising 0.9% in September. Sales at gasoline stores rose 1%, likely helped by the nominal sales of gasoline, whose price had risen in September. The catch-all miscellaneous stores swung from a 4% decline in August to a 3% increase in September. Electronics, building materials and supplies, and clothing retailers saw over the month declines in September.

UBS - September & Q3 Data Beat, Upgrade China's Growth Forecast

September & Q3 growth better than expected… Upgrade 2023 GDP growth forecast to 5.2% from 4.8%… More policy support is in the pipeline but big stimulus unlikely… Revise up 2024 GDP growth forecast to 4.4% from 4.2% Better growth momentum in Q3 2023 will also push up 2024 GDP growth to 4.4% even with no change in next year’s sequential growth forecasts. Consumption should continue to experience a post-Covid recovery in 2024 as services activities rebound further, household income grows, and some excess saving is released. However, property weakness will continue to weigh on overall growth, albeit with narrower declines and less of a drag. Household confidence will likely remain subdued, and local government finances will remain challenged, limiting their capacity to boost government spending and infrastructure investment. Even though we expect the government to set a higher headline fiscal deficit and larger quota of special LG bonds than 2023, we expect infrastructure investment to decelerate slightly.

Wells Fargo - Surge in Retail Sales Reflects Consumer Living Large

Consumers are spending more at bars & restaurants, at auto dealers and online. That's true on both a monthly basis and on trend over the past year. Consumers are looking for nothing but a good time, and it is hard to resist seeing the upside risk to the outlook.

Yardeni - Good News Is Bad News (oh boy, here we go again…)

Today's September reports for retail sales and industrial production were better than expected. The Atlanta Fed's GDPNow tracking model shows real GDP grew 5.4% (saar) during Q3, up from 5.1% on October 10. Leading the estimate higher is real consumer spending with a 4.1% increase (table).

That's good news for the stock market. It confirms our forecast that S&P 500 earnings per share probably rose to a record high during Q3. The economy has been resilient because consumers have continued to spend despite fears that they were running out of excess saving accumulated during the pandemic. However, they haven't run out of job openings.

Meanwhile, inflation has continued to moderate despite the strength of the economy. That should be good news too. However, bond yields rose today since most investors and investment strategists are skeptical that inflation can continue to decline without a significant economic slowdown. Even better would be a recession, in their opinion. In our opinion, inflation can continue to moderate in a growing economy, especially if productivity growth makes a comeback, as we expect.

… And from Global Wall Street inbox TO the WWW,

Bloomberg (via ZH) - Treasuries Pain Can Get Much Worse, Term Premium Dynamics Show (don’t care WHAT shows it, possibilities are REAL and more so than Ivory Tower and Transitorian’s had suggested …)

Treasuries’ recent slump owed plenty to the return of the so-called term premium as investors became more concerned about the risks of holding longer-dated debt. Even as US bonds get some help from geopolitical uncertainty, there’s plenty of scope for yields to march considerably higher on the same dynamics that helped drive September’s spike.

For one thing there’s little chance that the supply outlook is going to improve noticeably, no matter how the Middle East conflict and the US House speaker situation are resolved. For another, an examination of the relative yields for Australian and US debt signals there’s potential that US term premiums have further to go to.

Australia’s 10-year term premium has tended to align closely with the US gauge, but it’s been going through a relatively rare period since the pandemic with the two diverging. At first, it was the US term premium that swelled, perhaps representing the impact of extreme QE or lingering liquidity concerns after Treasuries froze as the pandemic broke out. That script flipped from early 2022 as the Fed started what would prove to be a far more aggressive hiking cycle than the RBA.

Still, as inflation slows in both economies and traders anticipate and end to rate hikes, that term premium gap closed dramatically even as September’s selloff drove steep losses for both Treasuries and Aussie bonds. Term premiums are tough enough to measure, let alone predict, but there’s a case to be made that one potential guide for the way for this to develop would be for the US term premium to close much of the remaining spread to Australia, which stood at about 60bps at the end of last month.

Bloomberg - Authority doesn't always win. Take markets, for example (Authers OpED with updated ‘ish look at SPY / TLT)

… Unyielding Higher Yields

It takes more than a terrifying atrocity followed by the real risk of an escalating land war in the Middle East to put off the bond market. By mid-session on Tuesday, 10-year Treasury yields were back up above their level on the eve of the Hamas attacks. The buying that followed the increase in geopolitical risk had been completely counterbalanced after barely a week of trading. (The bombing of the hospital in Gaza, a tragedy that also makes escalating war look more likely, happened after New York trading, but early indications from Asia are that even this has not prompted a major rush to the shelter of bonds.)

Meanwhile, there was an easy way to dodge the losses in bonds; sell them short relative to stocks. The outperformance of Bloomberg’s index of 20+-year Treasury bonds by the S&P 500 has continued almost uninterrupted since the pandemic summer of 2020:

The trend continued Tuesday, with stocks wobbling between small gains and small losses all day as bond prices plummeted. So, why are bond yields rising so much, and how can equity investors be so calm about it?

If you are surprised that yields continue to rise, maybe you are focusing too much on the chatter about them peaking and focusing too little on the underlying trend which shows the most persistent rise in yields in the past half century.

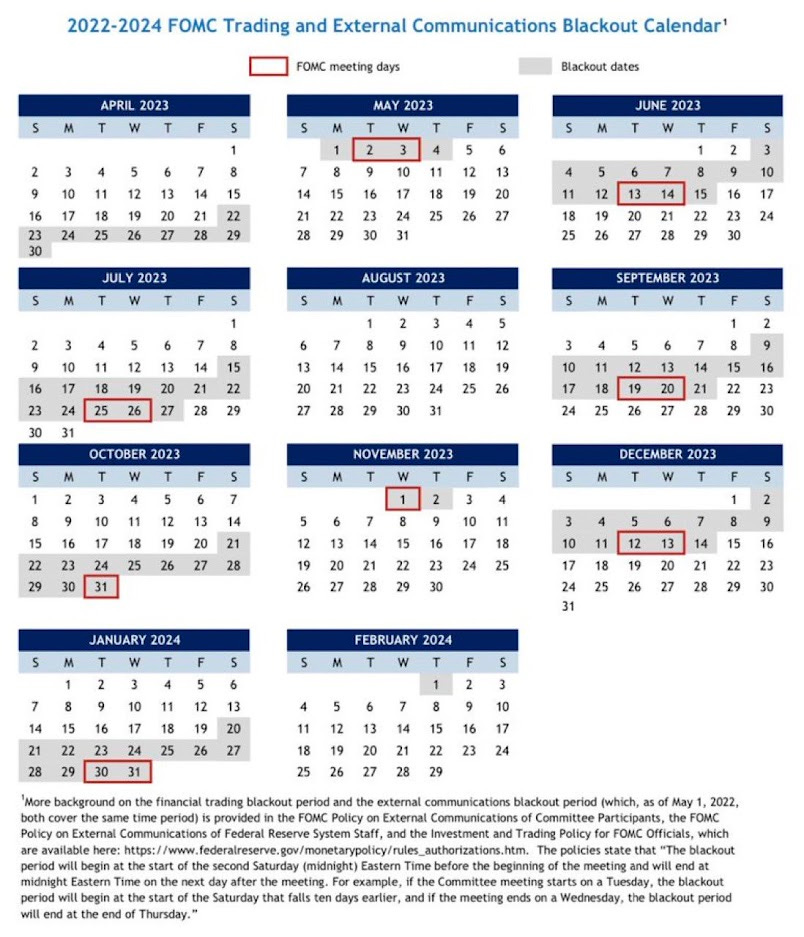

Before hitting SEND I’ll note / tip hat to ton of FEDSPEAK today which lined up ahead of PRE FOMC BLACKOUT PERIOD — Saturday — which was noted / mentioned HERE

… I’ll ADD a visual calendar I found on fintwit which helps detail the FOMC ‘BLACKOUT’ period (The period before FOMC rate-setting meetings, when Fed officials aren’t allowed to make public statements covering monetary policy, banking, or economic issues)

This degenerate says Value Investing isn't dead, but merely on a lengthy hiatus. At least I'm hopping!

PS-you have any odds of the 'recession' being delayed until after 2024 'election'?