(USTs bid/flatter -- long JGB sqeeze)while WE slept; 'data response index' SAYS; 'Higher for longer; the FED is not cutting rates before July, and certainly not five times in 2024'

Before I jump in, a quick mention that due to ‘travel’ schedule (heading in TO NYC, (work, meetings, parties), I will NOT be sending off anything tomorrow — Thursday — morning, after the FOMC meeting. I’ll be monitoring markets (and Global Wall Street) reflex TO FOMC, presser and the price action. This commentary will attempt to benefit from hindsight (20/20) as the dust will have settled by Friday morning, when you should fully expect spammation to resume…

Now with that in mind, I’d like to begin with an updated look at 5yy ahead of the Fed…

First, I cannot help but note the month (and a bit) of November saw yields DROP by nearly 90bps. Yes, stonks (S&P500 or 493, whatever) were ALSO UP about 10% and regional BANKS up about 20% … all of this just SINCE last FOMC meeting.

Let that sink in as it IS stunning. I’ve attempted to emphasize the current TLINE / downtrend in yields and how they may be (loosely?) associated with extremely overSOLD momentum. Yields did attempt to correct as momentum (which was recently overBOUGHT) is working itself out AND yields are, in the process, respecting the TLINE / downtrend. Count ME as impressed (if not a skeptic). This is now fully up to the Fed to either put PAID to the price action or attempt to guide it in a different direction …

I’ll say how pleased I was to see Harley Bassman (below) talk about HIGHER for longer and NOT 5 cuts in 2024 and certainly NOT a cut before July … much easier to say I’m with HIM than attempt any pretense I could now say / illustrate why / how.

Now with that little in mind (more from HIM below), the CPI set the table for the bond auction which set the table for this afternoons FOMC and tomorrows ReSale Tales.

All this talk of setting a table, I’m hungry and will be brief so I can go grab another gallon of coffee and some breakfast.

CalculatedRISK: BLS: CPI Increased 0.1% in November; Core CPI increased 0.3% CalculatedRISK: YoY Measures of Inflation: Services, Goods and Shelter CalculatedRISK: Cleveland Fed: Median CPI increased 0.4% and Trimmed-mean CPI increased 0.3% in November

WolfST: Beneath the Skin of CPI Inflation, November: Core Services Inflation Accelerates on Rents, Insurance, Healthcare

ZH: Core CPI Hotter Than Expected As Used-Car Price Rise Offsets Energy Drop

… Goldilocks? Or does this mean Powell will have to push back harder against the exuberance in the market for rate-cuts?

For more recaps and victory laps from Global Wall Street, keep scrollin’ …

Meanwhile, from the trenches of the bond market, some ‘good’ news on heels of <CPI, TLINE — noted YEST — sticksave, position squaring ahead of year end, SOMETHING ELSE> — please pick one …

ZH: Stellar 30Y Auction Has First Stop Through Since June, Sparks Algo Buying Frenzy

AND … here is a snapshot OF USTs as of 659a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are richer and flatter after long-end JGBs got squeezed (30y traded ~9bp stronger at one point) with flows tilted supportive of the 20y space. Cash buying was seen as pretty light, though a number of UST future flattener blocks were seen throughout the Asia session, the latest being a ~230k/01 TU-UXY block flattener at 5:04am. A well-bid 31y Gilt auction and unexpected contraction in 3Q UK GDP also saw core markets extending recent strength into Fed day. UST volumes are ~90% across futures, SPX futures are +8pts here at 6:45am, and real yields are leading the compositional rally (5y RY -2.3bps).

… and for some MORE of the news you can use » The Morning Hark - 13 Dec 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … and these on heels of yesterdays CPI and just ahead of this afternoons FOMC …

ABNAmro: US Outlook 2024 - Could Trump throw Goldilocks off course? (operative word here is “COULD” and oh, this shop — with all due respect — offering an opinion … a VIEW from very far away — Netherlands — and to say perhaps NOT a Trump supporter, well, maybe understatement?)

Strong household balance sheets and improved labour supply have helped stave off a recession. The economy is expected to slow to an average 1% annualised growth over the next three quarters, but a timely pivot to rate cuts by the Fed in June 2024 should keep the slowdown contained. The main risk to the rather Goldilocks-like scenario is a potential Trump victory in the 2024 election. This could herald sweeping new tariffs that put disinflation into reverse, triggering a new hiking cycle.

Apollo: Chapter 11 Bankruptcies Rising (ruh roh, RelRoy … unless of course, yer in Camp Rate Cut which in THAT case, GREAT JOB … #Winning)

Data for November shows that Chapter 11 bankruptcy filings are trending higher, and Fed hikes continue to bite harder and harder on highly leveraged firms with little or no cash flows in tech, growth, and venture capital, see chart below.

Barclays: November CPI: Firmed core supports tightening bias (wait, what?)

Although further weakness in the gasoline category kept a lid on headline CPI, the core firmed from 0.23% to 0.28% m/m, with acceleration in core services more than offsetting softness in core goods amid aggressive discounting. The services category was boosted by a strengthened reading for OER, and by firmed supercore.

BMO: CPI +0.1%, Core-CPI +0.3% (0.285%) -- TSY off the session highs (it’s the ‘IF ANYTHING’ quote which stopped ME …)

Headline CPI came in at +0.1% during the month of November vs. +0.0% consensus and +0.0% in October. This brought the YoY pace to +3.1% vs. +3.2% Oct and +3.1% anticipated. More importantly, Core-CPI increased +0.3% as-expected (+0.285% unrounded) versus +0.2% prior. The YoY pace was unchanged, as-anticipated at +4.0%. Core services ex-shelter came in at 0.505% from 0.344% in October while core-CPI services ex-rent/OER was 0.440% versus 0.216% prior. Airfares were -0.3%, New cars -0.06%, Used Cars +1.6%, and apparel -1.3%. Medical Care gained +0.6%, and OER +0.5%. There is nothing within the details that will immediately impact the Fed's thinking. If anything, the super-core figures reinforce the need for a hawkish pause and offset calls for more dramatic cuts signaled via the 2024 dots…

Resilient services prices drove an uptick in core CPI, which rose to 0.3% m/m in November versus its 0.2% average over the prior five months.

We think November’s pace of core inflation is likely to prevail over the next few months, translating to core PCE inflation running closer to 3% annualized than its recent 2% clip.

The Fed will likely view the report as evidence that despite progress on the inflation front, it still has some way to go before declaring victory.

Preliminary December forecast: 0.2% m/m headline and 0.3% core.

DB: November CPI recap: Good on goods, less so on services (so, nothing to the report, then … )

The November CPI data came in almost exactly in line with our expectations, with headline up +0.10% (vs +0.04% in October) while core rose by 0.28% (vs. +0.23%). Taken together, the year-over-year rate for headline fell by a tenth to 3.1%, while that for core remained steady at 4.0%. Shorter term trends in core show continued progress on disinflation, with the six-month annualized rate dropping below 3% for the first time since March 2021. That being said, most of this progress can be attributed to large declines in goods prices somewhat offsetting sticky services inflation.

Our forecasts are largely unchanged. Our initial read on the November core CPI data is that it should come in at +0.31% m/m and 4.0% y/y. Our Q4/Q4 forecasts are 4.0%, 2.6%, 2.5%, and 2.4% for 2023-2026 (all unch). Our Q4/Q4 core PCE forecasts are similarly unchanged: 3.4%. 2.3%, 2.2%, and 2.1%. The analogous headline numbers are 3.2%, 1.8%, 2.3% for CPI and 2.8%, 1.5%, 2.0% for PCE.

Today's data largely support the Fed's narrative around inflation, though some potential challenges to the story are beginning to emerge. Specifically, while goods inflation seems to be largely "solved", the large price declines in this sector are papering over still elevated services inflation. Further, while the labor market coming into better balance should reassure the Fed that core services ex housing will cool, substantial rental disinflation so far remains elusive. Ultimately, today's CPI data reaffirms our view that, although the SEP and press conference should maintain optimism on inflation, the FOMC is likely to maintain a soft hawkish bias to preserve their optionality in case upside inflation risks reemerge (see "December FOMC preview: Early '24 rate cuts? Bah humbug!").

DB: Early Morning Reid (on CPI rate cuts reprucussion)

… With the CPI generally a bit stronger than expected, that built on the narrative from the jobs report on Friday, and investors moved to dial back the chance of near-term rate cuts again. For instance, the chance of a cut as soon as March was down to 43%, the lowest in two weeks having peaked at 76% on December 5. In turn, sovereign bond yields saw a decent turnaround following the release, with yields on 10yr Treasuries ending the day down -3.2bps at 4.20%, having been as low as 4.14% just before the CPI came out. Similarly, there was a sharp reversal at the front-end, but with the 2yr yield ending the day up +2.2bps at 4.73%. Overnight, 10yr yields are down half a basis point…

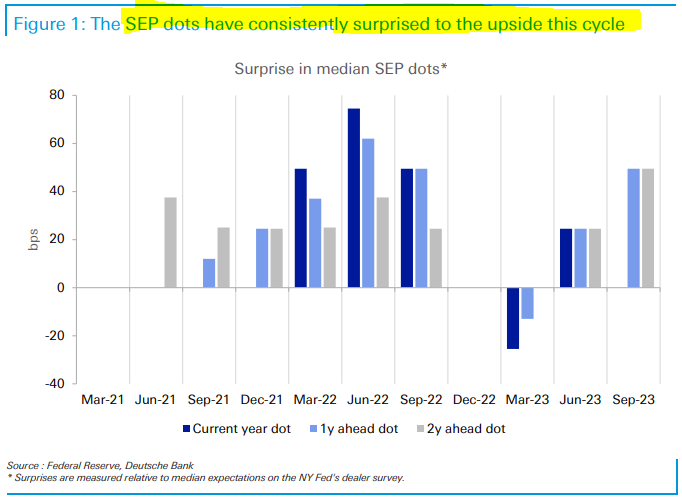

DB: A surprising SEP? (enter Gomer Pyle GIFs here?)

Focus at this week’s FOMC meeting will be on any indications of the Committee’s strategy and timeline for eventual rate cuts. Given that the Chair said less than two weeks ago that it was premature to speculate on when policy might ease, we don’t anticipate targeted communications around this tomorrow. That said, the updated SEP should provide some signal. (See our economists' meeting preview here.)

One notable feature of this SEP is that it will be the first time the median fed funds rate projection (or “dot”) at any horizon has fallen this hiking cycle, as the Fed is set to hold rates unchanged and thus forego the final 2023 hike that was in the September SEP. In line with that, the median 2024 dot is also likely to decline.

Of course, the market impact of any shift in the dots will depend on where they land relative to expectations. To bring context to this, today’s chart looks at surprises this cycle in the median SEP dots for the current year, 1y ahead, and 2y ahead. Surprises are measured relative to median expectations for the median dots in the NY Fed’s primary dealer survey.

The key thing that jumps out is that, not only have the median dots consistently increased over this cycle, as noted above, they have also consistently surprised to the upside. Specifically, over the past three years, the only instance in which a median dot came in below expectations was March this year, when the survey was conducted in the eye of the banking storm just days after the Fed unveiled a slew of emergency measures; respondents were likely just waiting for that dust to settle.

For this week’s meeting, our read on consensus is that the median 2024 dot is expected to shift down 25bp to continue to imply 50bp of cuts next year (we won’t know the dealer expectations until three weeks after the meeting when the survey results are made public). However, the 2024 median is fragile; it would take little in terms of underlying shifts for it to move down by more, raising the prospect that it could imply 75bp of cuts next year. Today’s chart shows that sort of SEP surprise would be very surprising for this cycle.

DB: Top-10 themes for 2024 (the one ‘bout how REALZ under appreciated…)

… To start, geopolitics and elections will be a theme that pervades through everything else in 2024. While it is hard to draw from history, we note the similarities between today and the 1980s. Following this, and against the background of upcoming fiscal spending promises, we highlight how positive real yields are an underappreciated risk for sovereigns. Yields are also a key part of our brief dive into Japan's policy conundrum for 2024 and how the country may deal with higher inflation …

The danger of high real yields is underappreciated

The cost to borrow money in real terms is around the highest it’s been since the financial crisis, and the effects of this increase are still widely underappreciated…

… On both sides of the Atlantic, real yields have risen substantially over the last couple of years. For instance, the US government now pays around 2% in real terms to borrow at a ten-year horizon, up from -1% at the end of 2021. Nor is that confined to long-term borrowing, since real yields are now around or above 2% at all maturity lengths. Similarly in Germany, ten-year real borrowing costs are now in positive territory, having been less than -2% at the end of 2021. And because this increase is in yields that adjust for inflation, this will not mechanically reverse once inflation returns to target levels.

… What is more concerning is how governments will deal with the next economic shock. Policymakers no longer have the advantage of historically low real interest rates, along with inflation that was broadly stable for many years. And following the pandemic, debt-to-GDP ratios also stand at their highest level in decades. That means next time, the economic backdrop is likely to prove much more constraining. That, itself, will be a surprise for those who have seen big bailouts in the past…

FirstTRUST: The Consumer Price Index (CPI) Rose 0.1% in November

The Consumer Price Index (CPI) rose 0.1% in November, above the consensus expectation of no change. The CPI is up 3.1% from a year ago.

Energy prices declined 2.3% in November, while food prices rose 0.2%. The “core” CPI, which excludes food and energy, rose 0.3% in November, matching consensus expectations. Core prices are up 4.0% versus a year ago.

Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – rose 0.2% in November and are up 0.8% in the past year. Real average weekly earnings are up 0.5% in the past year.

Implications: … With interest rates now above inflation across the yield curve and the M2 measure of the money supply down 4.5% from the peak in July 2022, money is tight enough to bring inflation down. More important, we continue to believe that a monetary policy tight enough to bring inflation down is also tight enough to induce an eventual recession. How the Federal Reserve responds to that economic weakness could determine whether we repeat the inflationary 1970s.

BOTTOM LINE: November core CPI rose 0.28%, 2bps below consensus expectations and compared to +0.23% in October. The year-on-year rate was unchanged at 4.0%. The composition was somewhat firmer, as the stickier OER and medical categories exceeded our expectations, and a 4bp drag from the volatile apparel category is likely to reverse after the holidays. Nonetheless, the trend in trimmed inflation continued to fall, and we tentatively expect core PCE prices rose just 0.14% in November (mom sa). We will update our estimate after tomorrow’s PPI data.

Goldilocks: Global Rates Insights: Gauging bond market sentiment via our Data Response Indicator (DRI)

… Our metric is derived by cumulating the ‘reactivity’ of yields to economic data surprises relative to an expected ‘baseline’ response. This Data Response Indicator (DRI) filters noise in observed yield changes, and produces clear separation in ex-post distributions of yield changes, with a score of +3 corresponding to extremely bullish sentiment, and -3 corresponding to extremely bearish sentiment, and scores in between characterizing the rest of the spectrum of sentiment.

We find that since 2012, 10y yields have both fallen and risen in the subsequent six months 66% of time after our DRI has scored -3 or +3 respectively. While the scores ‘work’ in generating a separation of ex-post change distributions over both 3m and 6m windows, they are more reliable over 6m windows. Our indicator’s performance is also materially improved over both change windows when using a shorter, more recent sample period (last five years).

At present, our indicator produces a DRI score of 0.07, which suggests a score of +1 (mild bullish sentiment).

JEFF: Nov CPI +0.1%, Core +0.3%, More Encouraging Signs of Lower Prints to Come

■ The November CPI rose +0.1% (+0.0967% unrounded) with core up 0.3% m/m (+0.285% unrounded). The headline came in a tick above consensus while the core was as-expected. ■ Looking through the surface-level measures to the so-called "super core" of core services ex-housing, inflation ticked back up after slowing in October. Core services ex-housing rose +0.4%, up from +0.2% last month. Outside of shelter, inflation pressure broadly eased, however. ■ The upside surprise relative to consensus came from firmer prints on used cars and shelter (both OER and rent of primary residence). Outside of these components, which won't likely be firm on a sustained basis, overall inflation looks like it is continuing to slow.

It’s that time of year when bond analysts are busy reassessing what informs their views, crunching numbers, and ultimately making forecasts for rates and yields. Some might be influenced by momentum behind recent moves, and more than a few will follow closely central bank guidance.

Fuelled by a big swing in US rate expectations, the debate about where bond yields will be in 2024 is heating up. Most market participants accept that the rate increases are now behind us, with the last hike having been in July, so the outlook for the upcoming decisions has become somewhat binary: unchanged or down.

Is the market pricing in too much or too little? In this bond letter we explain why it is better to understand what’s driving the difference in the numbers, before making a call on whether numbers are too high or low.

First, a forecast is not to be confused with a forward rate. The forward is a probability weighted estimate of where rates will be at a given point in the future. So, the 1Y1M – the forward for one-month money market rates starting one year in the future – captures all possible outcomes.

If, for example, the US forward is 125bp below today’s policy rate, it does not mean that markets are forecasting this amount of rate cuts. Rather, it is the aggregate of all views expressed in the market. In a simple two scenario model, it is the aggregate of a 50% probability of 250bp in rate cuts and the same weighting for unchanged.

Forecasts, on the other hand, reflect a baseline for the path and destiny of rates over a given time. The Federal Reserve gives us a median expectation from its “dot plot” in the quarterly Summary of Economic Projections, with the next update coming at the meeting on 12-13 December. Individual forecasts by market practitioners are complemented with a median consensus, but this is not probability-weighted and invariably looks very similar to central bank projections.

… Some market participants will see the recent extreme moves in our chart as a sign that the world has changed, such that equilibrium neutral rates will have to be a lot higher. A similar argument is that the term premium needs to increase in compensation for an uncertain future. Our view is that market yields incorporate a sizeable risk premium on the possibility that the world has changed, not the certainty that it has.

At some point in 2024, rates are likely to be heading down. How much longer key policy rates stay where they are depends on the data or some kind of surprise event.

Forecasts are not the same as forwards, neither have a stellar track record in predictions, and a lot of these are in any case clouded by high risk premia. The key message is that markets know that the outlook for rates has become binary and are prepared to attach a higher weight to a large downward move.

…Bonds The move higher in yields in 2023 was unrelenting, rising alongside a U.S. economy that continued to outperform expectations. With a still resilient economy to date, we think Treasury yields could stay relatively high in the near term, although rates may subside a bit versus the volatility seen in 2023. Issuance of Treasury securities to fund budget deficits and the potential for the bank of Japan to finally end loose monetary policies in 2024 could keep some upward pressure on yields. However, the big move in yields may have already taken place, and with a potential directional change in interest rates likely coming in 2024, we believe bonds offer compelling value.

RBC: Moderating US inflation pressures extended in November

… Bottom line: The November CPI data largely extended trends of normalizing inflation pressures as seen in October’s CPI as well as core PCE data. It should have little impact on the Fed’s decision tomorrow, where a no-change in the fed funds target range is widely expected to be delivered. The Fed will retain the option to push interest rates higher – economic growth has remained resilient and Chair Powell has actively pushed back against rhetoric around rate cuts in 2024. But labour market conditions have looked softer on balance, and slower wage growth is adding to evidence that inflation pressures are easing. With inflation and labour markets (both ends of the Fed’s dual mandate) moving towards target levels, we continue to expect the Fed to stay on hold, until pivoting to gradual cuts in the second quarter of 2024.

UBS: November CPI recap: Core goods weak (ex cars)

… Moderate headline/strong core CPI likely in December We currently project headline CPI prices will increase 26bp in December seasonally adjusted (-18bp not seasonally adjusted) amid a continued decline in gasoline prices, and core CPI prices will increase 31bp seasonally adjusted. These changes would see 12- month inflation tick up to 3.3% for the headline CPI and tick down to 3.9% for the core CPI. Looking further ahead, we expect 12-month core CPI inflation to trend down through next year amid increasing goods supply (particularly for motor vehicles), the pass-through of slower new lease rents into CPI rents, and a general easing in the economy. As always, we will update our inflation forecast as we go through the details of today’s release and additional data becomes available.

UBS (Donovan): The Fed, inflation, and deflation (?)

The Federal Reserve should leave policy unchanged. The meeting will be followed by Fed Chair Powell delivering the full benefit of his economic insight at the press briefing (this should not take long). Powell will try to prevent markets from expecting earlier rate reductions. This task would be a lot easier had Powell not trashed the Fed’s reputation for forward guidance.

Yesterday’s US consumer price inflation data hint deflation may become a bigger threat. Durable goods prices (in deflation for 12 consecutive months) shows just what transitory inflation looks like. Core inflation excluding shelter has been around 2% y/y for three months (as so much of shelter is a fantasy price, this gives a sense of real world underlying inflation pressures). Producer prices are due today…

Summary The November CPI report was relatively uneventful. Falling gasoline prices and modest food inflation restrained the headline CPI to just a 0.1% increase in the month. Excluding food and energy prices, core CPI was up 0.3%, in line with consensus expectations. Core goods prices continued to decline even as the drivers of the dip changed, while core services inflation was a bit stronger in November compared to October due to faster inflation for shelter, medical care and transportation.

The November CPI data probably do not move the needle much for the FOMC this week. Doves looking for a downside surprise did not see one materialize, but a nasty upside shock was also avoided. Looking through the month-to-month volatility, inflation continues to move back toward the Fed's 2% inflation target. That said, price growth remains far enough away from 2% that the central bank likely will not declare victory just yet. We suspect the FOMC will keep monetary policy in a holding pattern and look toward the Q1 labor market and inflation data to determine its next move. Our base case for the first rate cut remains June 2024.

Wells Fargo: NFIB Reveals Ongoing Weakness in Small Business Optimism. Labor Quality Remains the Top Concern in November

Summary Receding Inflation Not Enough to Brighten Outlooks The narrative of U.S. economic resilience does not appear to be reaching small business owners on the ground. The NFIB Small Business Optimism Index dropped to 90.6 in November, the fourth consecutive dip. As we come up on nearly two years of optimism running below the long-term average, outlooks for business conditions remained firmly in negative territory. Receding inflation was the silver lining of November’s report. Echoing today’s Consumer Price Index (CPI) report that demonstrated progress on inflation, the net percent of owners raising prices fell to 25%, tied for its lowest level since early 2021. Yet, the NFIB survey is also flashing warning signs about price pressures that could complicate the road back to 2% inflation. In addition to an uptick in small business plans to raise prices over the next few months, owners continued to highlight hiring challenges and compensation pressures even amidst retreating labor demand.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Bond Market’s Big Rate-Cut Wager Faces a Reckoning From the Fed

Fed officials quarterly rate projections are keenly in focus

Chairman Powell may push back on rate cuts at press gathering

… “If we get a message from the Fed that the timing” of expected rate cuts “is simply going to shift, but there is maybe three or four cuts in the cards over the next 18 months, the market can deal with that — and it will deal with that well,” David Lebovitz, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “What will give the market indigestion is if the Fed sends a hawkish signal that we will not get those three or four cuts.”

… “We are really in a path from the Fed of either a slow cut or a quick cut next year,” Rob Waldner, head of macro research at Invesco said on Bloomberg Television Tuesday. “And both are pretty good for bonds. We think we are in a slow growth, disinflationary, environment.”

Bloomberg: The Fed Isn’t Ready to Speculate on Rate Cuts — Yet

Investors will be focused on dot plot forecasts for 2024 rates

Powell is not ready to speculate on when rate cuts will start

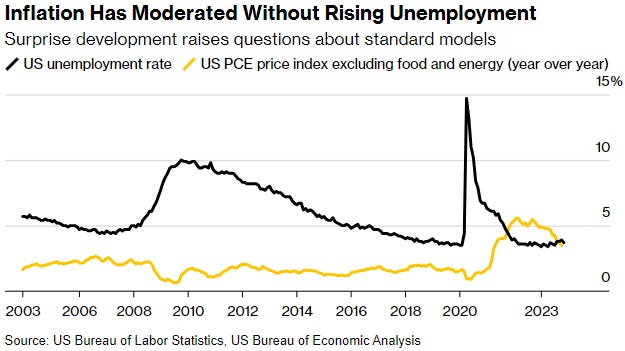

Bloomberg: Fed Enters Last Leg of Inflation Fight With Little ‘Pain’ So Far

Inflation has receded quickly with minimal employment impact

Surprise development will fuel debate over pandemic takeaways

Federal Reserve Chair Jerome Powell said pain would be necessary to quell inflation. It’s looking increasingly likely that won’t be the case.

At 3.7%, the unemployment rate is right about where it was when the Fed began raising interest rates in March 2022. Meanwhile, the pace of inflation’s descent — which has left it now only a percentage point above the central bank’s 2% target — has also surprised policymakers, just as it did on the way up.

That combination of trends, provided it persists, is sure to fuel debate among central bankers over key takeaways from the pandemic experience.

“It’s really important to broaden the framework out, so that you’re not just relying on these ridiculously simplistic macro models that lead central bankers to conclude their trade-offs are pain or more pain,” said Julia Coronado, president of MacroPolicy Perspectives…

… The change of tune comes amid a swift moderation of inflation this year that economists inside and outside the Fed have widely attributed to improvements on the “supply side” of the economy, as businesses have adapted to supply-chain bottlenecks in product markets created first by the pandemic and then the Russia-Ukraine war.

Meanwhile in the labor market, many have cited a resumption of immigration to the US that has made it easier for businesses to hire. Other pandemic-related labor-market disruptions have receded further into the rearview mirror as well, supporting workforce participation and helping to curb upward pressure on wages.

“In the midst of what was a high-churn, high-turnover, hot-hiring economy, there probably were some one-time strains on search costs, and that probably did push up wages on a one-time basis,” said Skanda Amarnath, executive director of Employ America, a think-tank that supports pro-labor policies. “So wage growth went up and wage growth went down, even though unemployment largely stayed in the same spot.”

Bloomberg: Markets aren't doing Jerome Powell's work anymore (OpED)

Slightly disappointing inflation data will give the central bank no reason to bring rates down early in the new year.

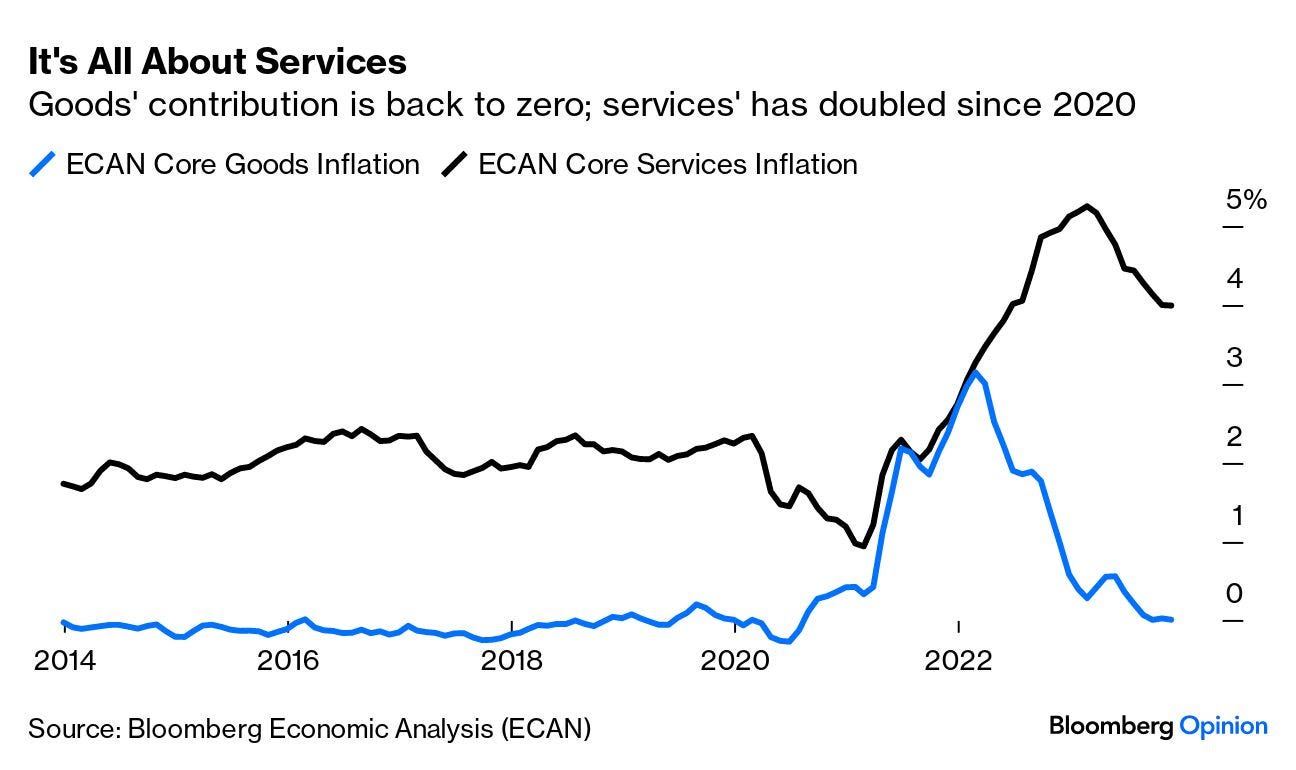

…We can see that more clearly if we look at the contribution to core inflation of goods and services over the last decade, again using the ECAN function. For years, services ran at about 2% per year, while goods inflation was zero. They spiked together in 2021 and 2022, but now goods is back to zero (so there’s certainly an argument that this element of inflation was transitory), while services is still at roughly double its pre-pandemic norm. Annual core services inflation was unchanged in November compared to the previous month:

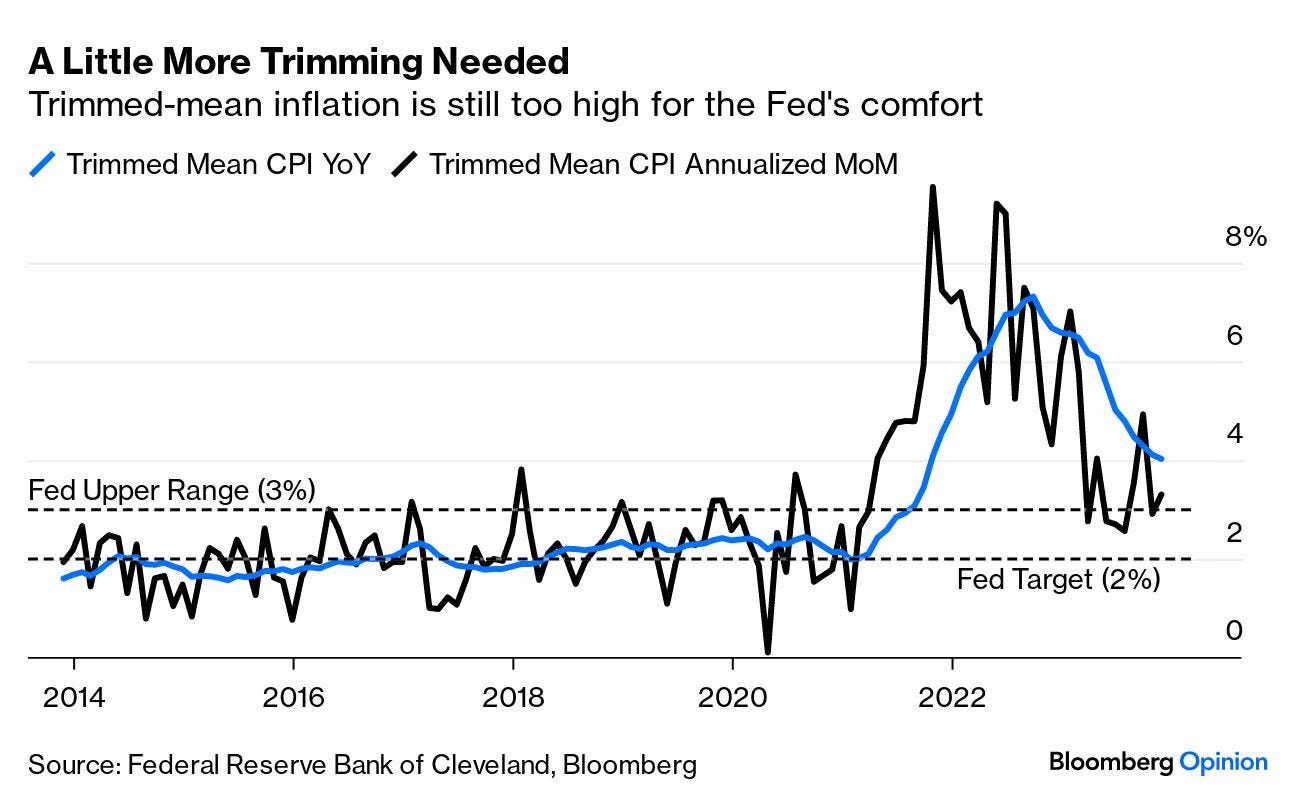

The underlying notion of an improving situation that doesn’t yet allow central bankers to relax also shines through from the special statistical measures that different research teams within the Fed use to track different definitions of underlying inflation. The “trimmed mean” (in which the biggest outlying components in both directions are excluded and an average taken of the rest), continues to decline, but only slowly. Its latest year-on-year reading was 4%. On a month-on-month basis, it’s lower than that, and has touched the 3% upper band of the Fed’s inflation target, but it ticked up very slightly last month. Such numbers don’t force the Fed to hike rates again; but they also give it little or no cover for cutting them:

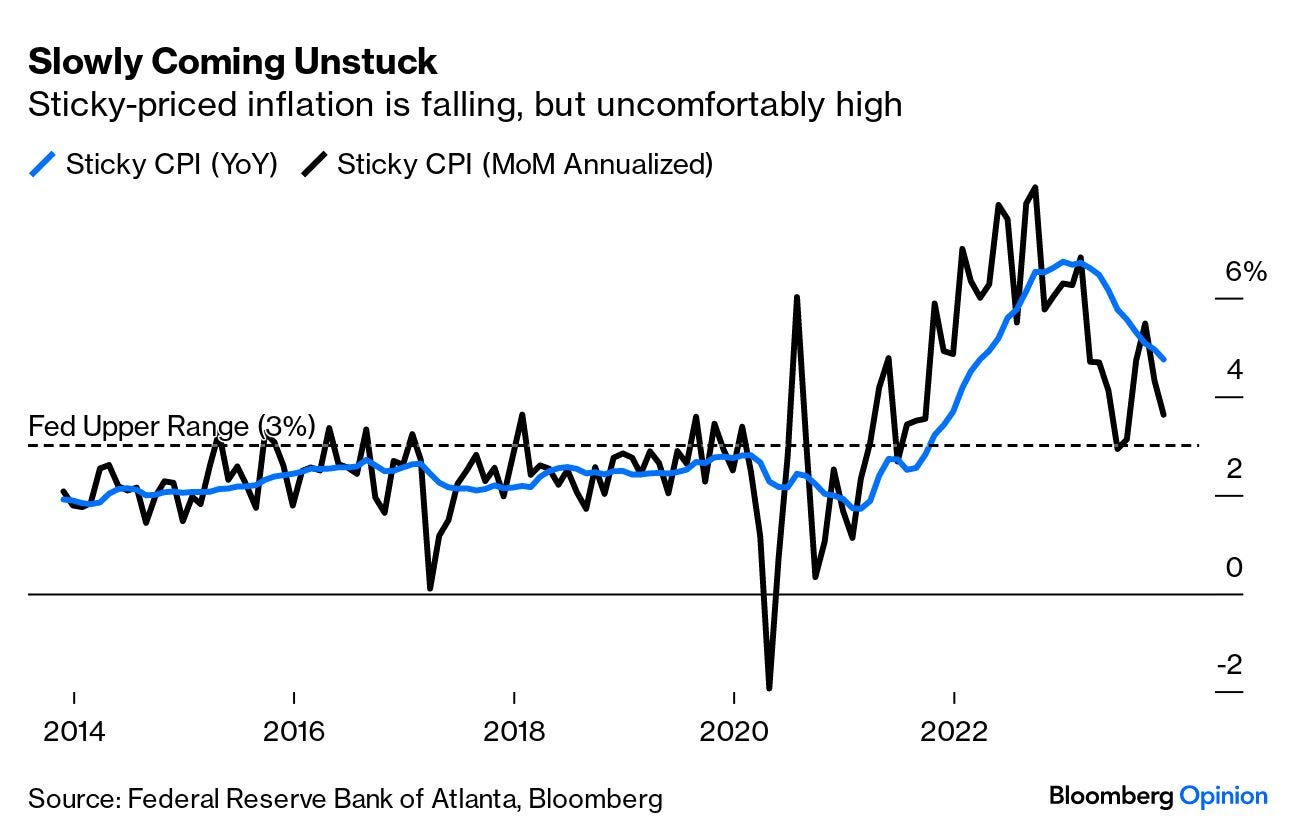

The Atlanta Fed produces separate inflation figures for sticky prices (which take a while to move and generally only go upward), and flexible ones, which can vary in either direction at short notice. What the central bankers want to avoid is a steady increase in sticky price inflation, as by definition it’s hard to reverse. This measure again clearly shows a declining trend, but one that has a lot further to go before the Fed will feel comfortable. November saw a dip, but it still ran at an annualized clip of more than 3% for the month:

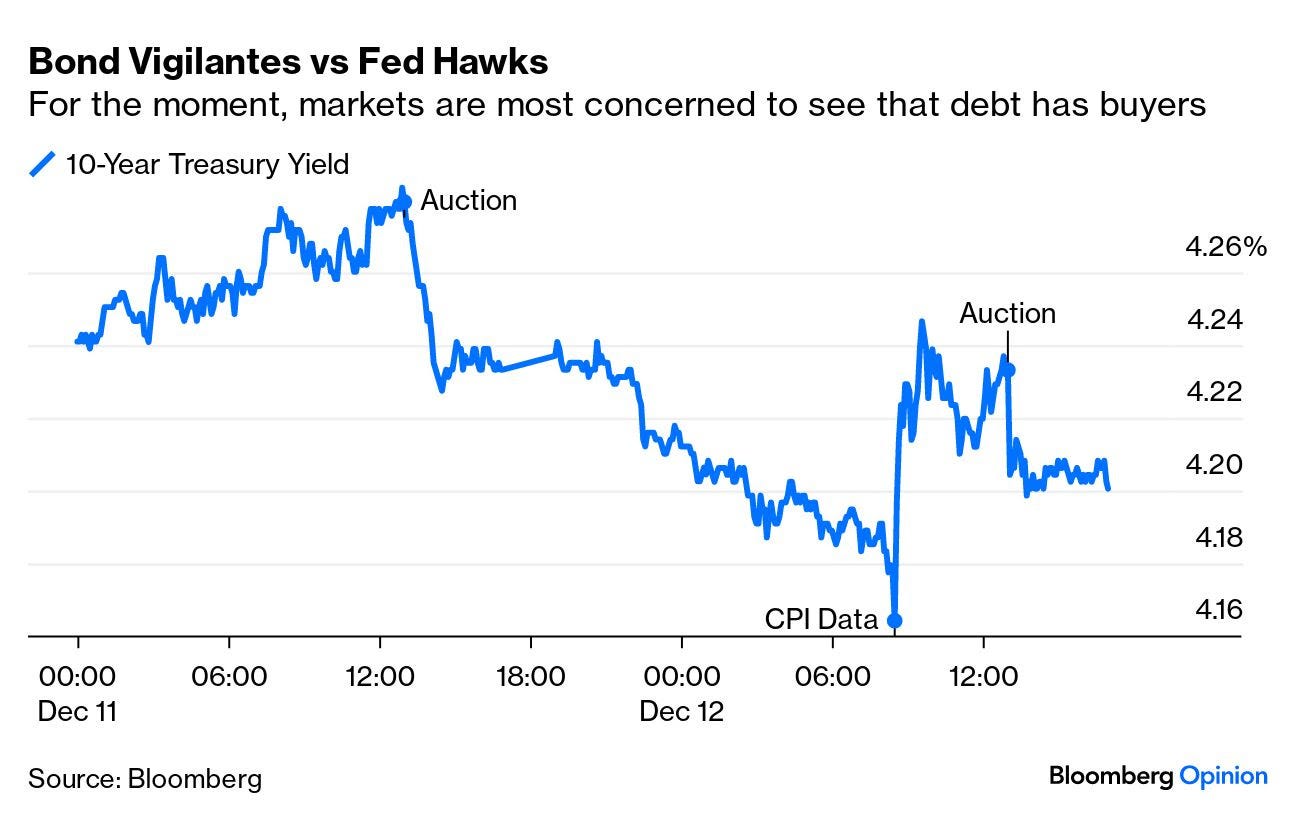

… At this point, markets are more alarmed by bond vigilantes, who might refuse to buy Treasury debt and send yields soaring, than they are by the prospect of the central bank hawks who might send rates up. So that explains how 10-year yields fell over the first two days of the week despite inflation news that would usually send them upward:

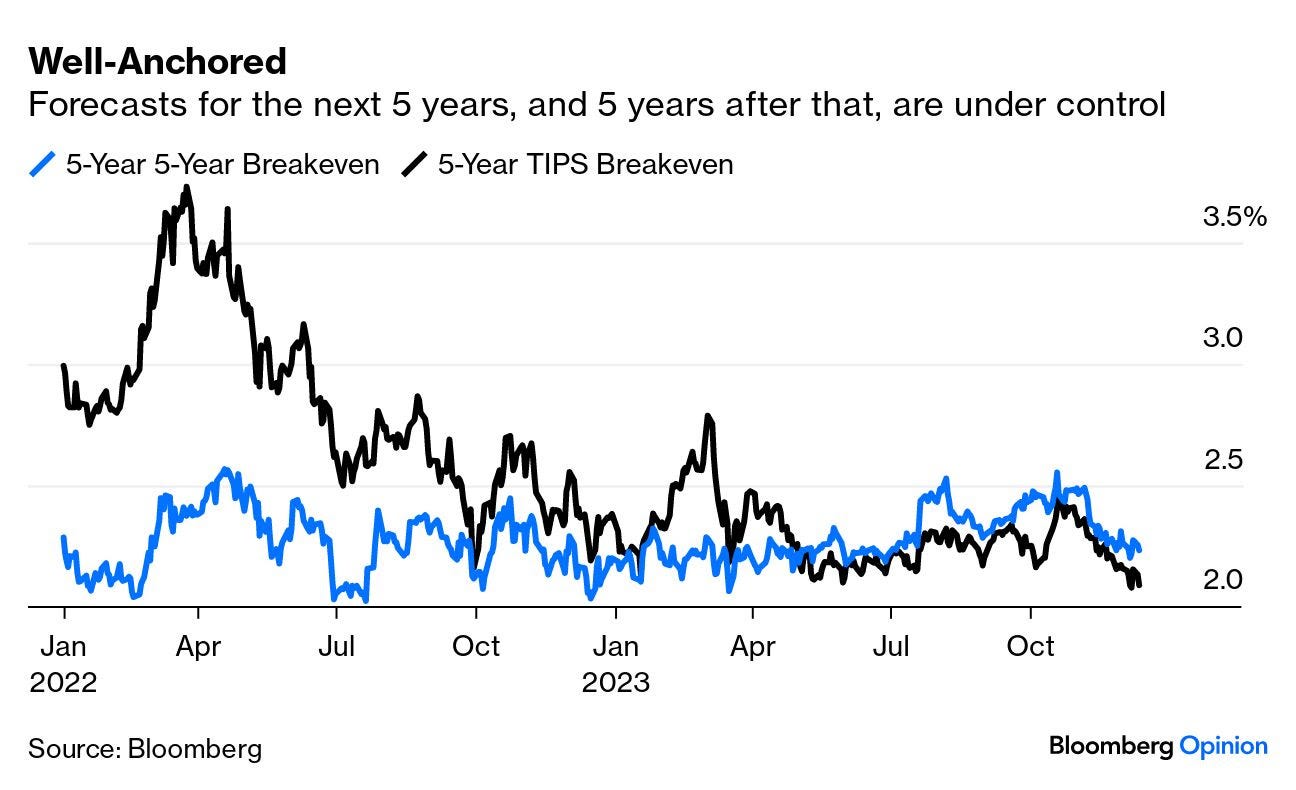

If there is one signal from the market that the Fed must treat with unalloyed delight, it comes from inflation breakevens, the implicit projections of future rate increases that are baked into bond prices. It is a part of the central bank litany that inflation expectations should be “well-anchored,” and that they certainly are. Breakevens spiked above 3.5% last year in the aftermath of the Ukraine invasion. For the next five years, they’re almost back down to 2.0%. The so-called five-year/five-year breakeven, which measures the expected average inflation for the five years starting in five years time, is also falling again. This metric has been under control throughout the inflation scare, showing that markets have always had some degree of faith that the Fed wouldn’t allow a new era of higher inflation to take shape. That confidence showed some signs of shaking two months ago as the figure rose above 2.5%. Hopes for rate cuts also created fears of longer-term inflation. But now both these measures are at levels with which the Fed should feel comfortable:

The prevailing opinion in the bond market appears to be that “Team Transitory” was right all along…

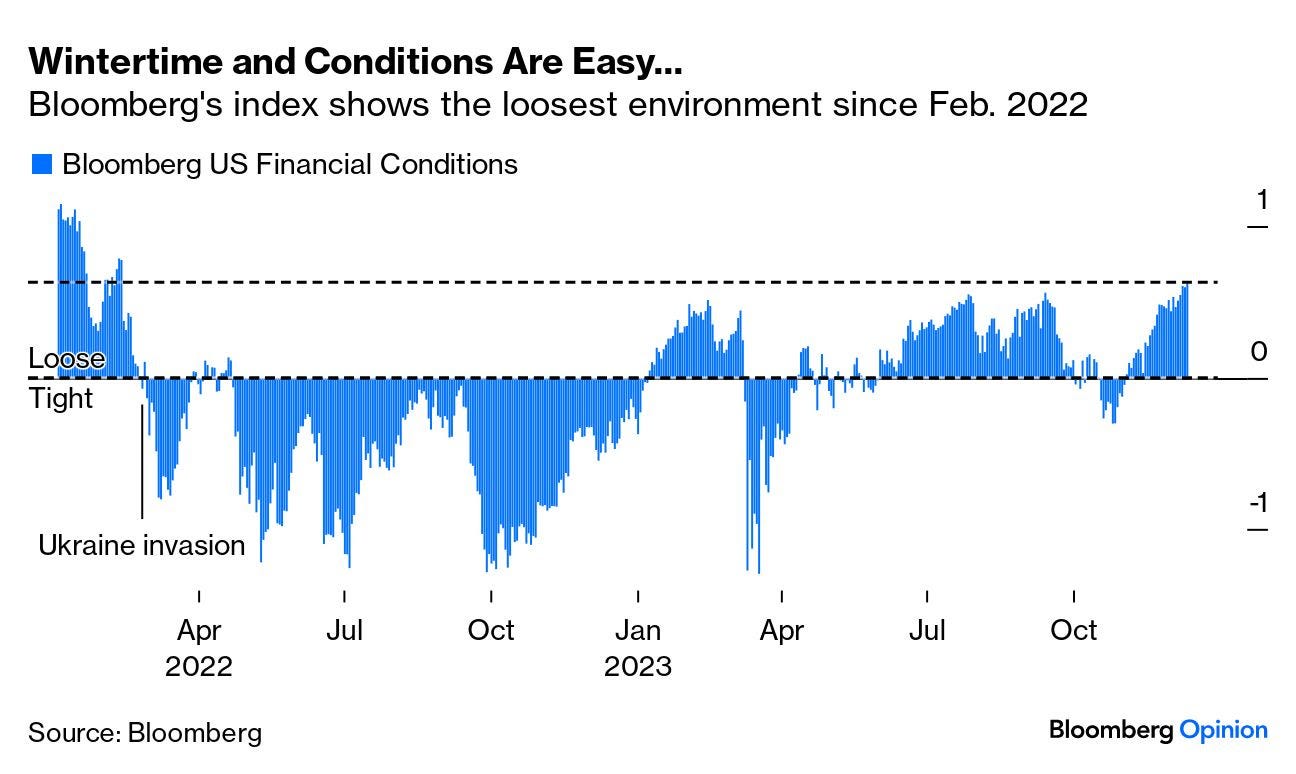

… The biggest problem at present is of the market’s own making. If Jerome Powell and friends are concerned about loose financial conditions, then rate cuts will be difficult. Powell made great play in recent months of the notion that when the market tightens financial conditions (by making it harder to raise equity or debt, or access cash), they are doing the Fed’s job. A couple of months ago, that was true. Now, the opposite is the case. There are different ways to measure this, but risk appetite by any yardstick is back in a big way, and that means that it’s getting easier to access finance. Bloomberg’s own index shows the easiest US financial conditionssince before the Ukraine invasion in February last year:

The FOMC won’t change rates this week, but it does get to revise the “dot plot” which shows its projected course of interest rates ahead. That would be a way to assure the market that rates are coming down swiftly, but for now the Fed could be reluctant to do anything that encourages more speculation. And after the dot plot, the press gets its last confrontation of the year with Powell at his press conference. If he wants to nudge bond yields back upward, and get the markets to tighten conditions again, he’s going to find it difficult.

Convexity Maven: "The 2024 Stocking Stuffers" (from the inventor of THE MOVE — bonds vol index — a few words of wisdom, highlights MINE…)

Come this time every year, I publish a list of “Investments” that I think will do well over the intermediate horizon – two to five years. These are NOT meant to be nips to blips RV trades, but rather longer-term notions that capitalize upon either my strongly held themes or the trembling hands of Sharpe Ratio focused portfolio managers.

Contrary to the past, this year I will offer investments suitable for widows and orphans - a buy and hold portfolio constructed for those who have a distant horizon with little desire to “trade”.

In preview, I am the Managing Partner at a firm I cannot mention, where I create and manage financial “strategies” whose tickers I cannot name. We utilize Professional investment products (Futures, Options, Total Return Swaps, etc.) to offer civilians access to the best-in-class construction at a modest fee.

That said, it will not take too much effort on your part to "connect the dots".

NOTE: Not mentioned here is an allocation to a diverse Equity Index, which should be 40% to 60%, with the remaining spread from the list as suits.

My Macro-view has not changed much this year: Higher for longer; the FED is not cutting rates before July, and certainly not five times in 2024…

AND again, OUT tomorrow (have yer girl call my girl if you require a rebate) and on heels of ALL this weeks UST supply (so far markets seem to have consumed largely without issue) in mind, an oldy but a goody …

AND … THAT is all for now. Off to the day job…back Friday!

Great detail on the CPI...

I agree with your Headline.....the market is ahead of itself

The inflation fight isn't quite over......

Have for in NYC.....

Thank you for your expertise....