I’ll be honest with you. Waking up to the news (actually we all got this late at night and so, I was going to sleep with it as I was consuming last nights miracle at Metlife) gave ME reasons to pause …

CNBC: Hasbro laying off 1,100 workers as weak toy sales persist into holiday season

… “We anticipated the first three quarters to be challenging, particularly in Toys, where the market is coming off historic, pandemic-driven highs,” CEO Chris Cocks said in the memo. “While we have made some important progress across our organization, the headwinds we saw through the first nine months of the year have continued into Holiday and are likely to persist into 2024 …

… Cutting ~20% of their workforce just 2wks before XMAS and on heels of ‘Black Friday’?

The most obvious reasons for concern are specifically what, if ANY message TO the markets and economy as well as the Fed are we to take ahead of this mornings CPI (which may be more impacted by yesterdays FRBNY inflation expectations (more in a minute) and this afternoons long bond auction …

… I had THOUGHT we’d be revisiting somewhat HIGHER yields but it would appear that a TLINE in place off the November ‘cheaps’ has continued to act as some sort of kryptonite. I’ll only say that this mornings CPI matters far more than whatever I might have thought, especially as it arrives well in advance of this afternoons 30yr auction and so, I’ll move along.

In as far as YESTERDAYS supply, well, exactly what did we THINK when we were going to get an auction double-header as desks continue to think out ahead of years last FOMC meeting and holiday travel season?

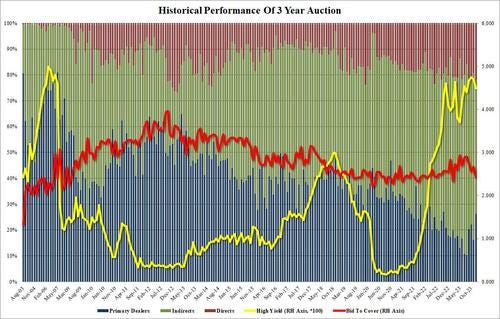

ZH: Ugly, Tailing 3Y Auction Sees Lowest Foreign Demand Since June 2022

… Then, moving to the internals, we go from bad to worse as buyside demand also collapsed and Indirects (i.e. foreign accounts) took down just 52.1%, a sharp drop from 64.6% last month (and the 63.9% six-auction average), and the lowest since June 2022; and with Directs awarded 21.7%, Dealers were left with a whopping 26.2%, a huge jump from last month's 16.3% and the six-auction average of 16.1%.

But WEIGHT … there’s MOAR …

ZH: Strong Buyside Demand For 10Y Auction Despite Big Tail

… AND for those (rate cute ‘istas — who still or are RE believers in TRANSITORY) in search of some GOODer news,

ZH: Year-Ahead Inflation Expectations Tumble To Lowest Since April 2021 In Latest NY Fed Survey

… AND click HERE for THE data from the horses mouth which I thought summed up best by this chart,

Please keep in mind this is a SENTIMENT survey and NOT actual inflation by any stretch of the imagination. Is it going in the right direction for the Fed? Sure. Does it mean anything in as far as rate CUTS? No. Not in the least…take the ‘data point’ for what it is. An OPINION … which I’m reminded … are like body parts which everyone has … HOPEFULLY no further commentary needed.

Moving along to some fresh bit of data in the form of this mornings NFIB

NFIB’s Small Business Optimism Index decreased 0.1 point in November to 90.6, which marks the 23rd consecutive month below the 50-year average of 98. Twenty-two percent of owners reported that inflation was their single most important problem in operating their business, unchanged from October but 10 points lower than this time last year.

“Job openings on Main Street remain elevated as the economy saw a strong third quarter,” said NFIB Chief Economist Bill Dunkelberg. “However, even with the growing economy, small business owners have not seen a strong wave of workers to fill their open positions. Inflation also continues to be an issue among small businesses.”

Key findings include:

Owners expecting better business conditions over the next six months increased one point from October to a net negative 42% seasonally adjusted.

A net negative 17% of all owners (seasonally adjusted) reported higher nominal sales in the past three months, unchanged from October and the lowest reading since July 2020.

Forty percent (seasonally adjusted) of owners reported job openings that were hard to fill, down three points.

Seasonally adjusted, a net 30% of owners plan to raise compensation in the next three months, up six points from October and the highest since December 2021.

The net percent of owners raising average selling prices decreased five points from October to a net 25% (seasonally adjusted).

The net percent of owners who expect real sales to be higher increased two points from October to a net negative 8% (seasonally adjusted).

Read THE REPORT for yourself and make of it whatever you will (rate CUTS and / or HIKES) and on that highlighted bit on comp just above, something from #FinTWIT

Don’t look now… but the NFIB survey points to a re-acceleration in small business’ compensation plans (which typically leads wage inflation by about 6 months). So is real income growth about to re-accelerate?

So to recap … TRANSITORIANS continue to be #Winning and so too are Tommy ‘Cutlets’ NYGs? OR your and my experienced inflation (not our OPINIONS and hopes) combined with small biz (the economic engine of the country) are perhaps more important?

Moving along and back TO Tommy ‘Cutlets’ for just a moment…

It is being said that Tommy ‘Cutlets’ agent (Sean Stellato) looks exactly as you’d expect Tommy ‘Cutlets’ agent to look …

I’m fairly confident Tommy DeVito’s agent tried to kill Hyman Roth back in the day … AND here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher with the curve bull-flattening after UK wage growth disappointed- which led to a sharp outperformance in Gilts versus Treasuries and Bunds this morning. A well-received JGB 5-year (-4.0bp) auction also gave a lift to Treasuries during Asian hours. DXY is lower (-0.35%) while front WTI futures are modestly lower (-0.3%). Asian stocks were mostly higher, EU and UK share markets are little changed while ES futures are UNCHD here at 6:45am. Our overnight US rates flows saw better real$ buying in intermediates and the long-end during Asian hours. The solid 5yr JGB auction plus word of shipping attacks off Yemen were cited by the desk as giving a lift to prices then. During London's AM hours, the 5bp drop in Tsy yields sparked some selling from real$ and fast$, mostly in intermediates. Back-end flows were subdued but saw better net buying earlier. Overnight Treasury volume was decent at ~120% of average with 3yrs (204%) seeing some relatively high average turnover (probably rolls?) overnight after yesterday's auction.

… This price-watcher was impressed by the Treasury market price action yesterday as markets bent, but did not break, under the weight of back-back, up-sized Treasury coupon auctions. Treasury 10yrs went into yesterday afternoon's sale locally 'overbought' and near range resistance at ~4.11%- as we show in today's first attachment. Despite all that, 10yr yields managed to close yesterday not far from the session's opening yield lows whilst extending yesterday afternoon's gains into this morning's NY open. As I mentioned to Ed yesterday afternoon, "If I was short rates, I'd be concerned." The reason for that comment was not just because of yesterday's price action but because of the unambiguously bullish set-ups in the longer-term charts that we've posted many times in recent weeks- including again this morning.

NOTED and also they note how much more constructive longer-term (ie MONTHLY) chart looks … and for some MORE of the news you can use » The Morning Hark - 12 Dec 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Here are the results of our 2024 Outlook Survey conducted during December 6th-8th 2023 with 540 market professionals from around the world taking part.

Some bullets:

A hard landing was seen as the biggest risk to market stability for 2024. This was helped by the fact that it's probably the most obvious observable risk. The US election was in second place. Geopolitics scored heavily but across various different potential flashpoints.

Participants thought that 69-76% of soft landing prospects were priced into Fed Funds, Credit and Equities.

The S&P is only expected to increase +1.7% in 2024 but the Magnificent 7 are expected to increase +12.7% albeit with a big range of answers.

10yr USTs and Bunds are expected to end 2024 at 3.8% and 2.4%, respectively.

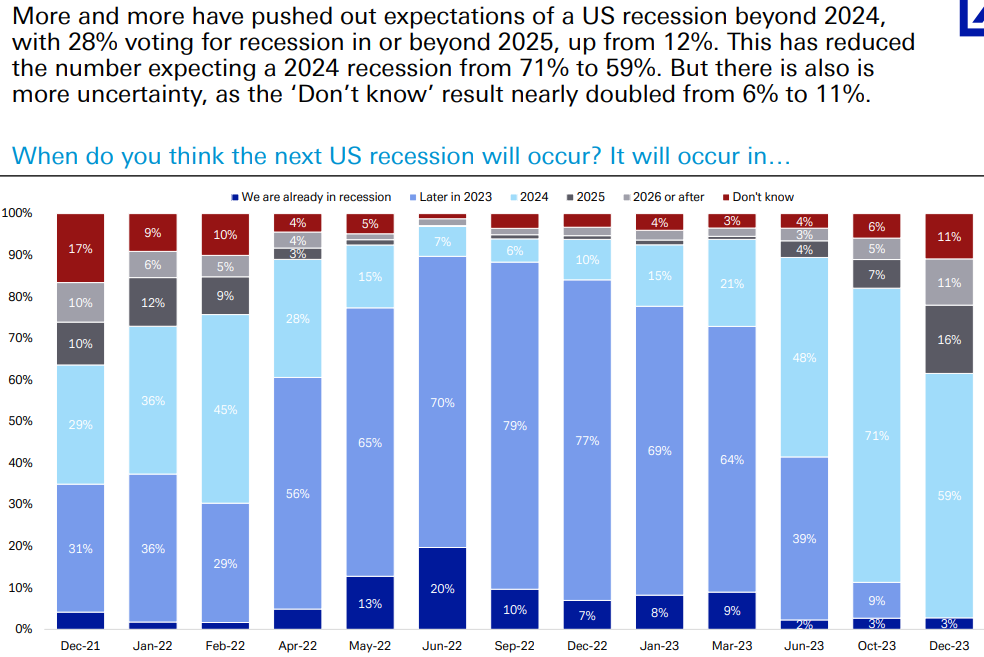

US recession risk for 2024 fell from 71% three months ago to 59%. With those saying a recession in 2025 or later increasing from 12% to 28%.

Inflation expectations are down to the lowest since Q4 '21 in the US and Q1 '22 in Europe.

ChatGPT adoption has now been steady since June after a spectacular rise in H1.

And your favourite Xmas song is....... click on the link to find out.

FirstTrust: Monday Morning Outlook - What Should the Fed Do? How About Nothing?

For the first time in roughly fifteen years, interest rates in the United States are about right. In economics, we call it the “neutral” or “natural” rate. The Taylor Rule says rates should be higher, and our model that uses nominal GDP growth (real GDP plus inflation) says the same thing. But both these models rely on data that is still distorted by COVID.

A simpler approach is to assume interest rates should be “Inflation Plus.” If we judge current inflation using an average of the Cleveland Median CPI (up 5.3% from a year ago) and overall total CPI (up 3.2% from a year ago) we get 4.2%. “Plus 1%” says rates should be roughly 5.2%. And that’s almost exactly where the federal funds rate is today.

This is a big change. Between 2008 and today, the Federal Reserve held the funds rate below inflation roughly 83% of the time. These excessively low rates have created problems…

… The bottom line is that those who think the Fed can just manage its way out this easily, cutting rates to offset the pain of recession (or avoid one entirely), may not be correct. Many seem to have submitted to “state-run capitalism.” But history shows it has never really worked. The Fed is likely to “do nothing” this week and holding that position in 2024 might not be a bad thing.

We expect a 0.27% increase in November core CPI (vs. 0.3% consensus), corresponding to a year-over-year rate of 3.99% (vs. 4.0% consensus). We expect a 0.03% increase in November headline CPI (vs. flat consensus), which corresponds to a year-over-year rate of 3.06% (vs. 3.1% consensus). Our forecast is consistent with a 0.37% increase in CPI core services excluding rent and owners’ equivalent rent and with a 0.16% increase in core PCE in November. We will update our core PCE forecast after the CPI and PPI are released.

We highlight three key component-level trends we expect to see in this month’s report. First, we expect used car prices to decline by 0.9% and new car prices to decline by 0.3%, reflecting rebounding promotional incentives and declining used car auction prices in November. Second, we expect airfares to increase by 4% this month, reflecting a seasonally adjusted increase in our airline team’s real-time measure of airfares ahead of the holidays. Third, we expect shelter inflation to run at a similar pace to last month’s (we forecast rent to increase by 0.46% and OER to increase by 0.42%), as the gap between rents for new and continuing leases continues to close and the OER-rent gap normalizes after last month’s decline.

Going forward, we expect monthly core CPI inflation to remain around 0.3% in the next three months. We see further disinflation in the pipeline in 2024 from rebalancing in the auto, housing rental, and labor markets, though we expect a small offset from a delayed acceleration in healthcare. We forecast year-over-year core CPI inflation of 2.7% in December 2024.

With the strong rally in government bonds since the end of October, we lay out what we see as the economic and market drivers for yields over the next three months. We also explore what US overnight repo rates staying elevated may mean.

Economics: Our expectation is for inflation and growth to moderate in DM over the next 12 months, but the path of disinflation will likely be bumpy. In both the US and Europe, while inflation drifts lower, the 6-month moving average will likely turn higher in the first part of next year before coming down again, arguing against Fed and ECB cutting in March.

US rates: We turn neutral on duration into year-end. Duration has rallied too far, too fast, there remains some upside risk to inflation as flagged by our economists, and markets appear fairly priced versus our view of the December FOMC dot plot…

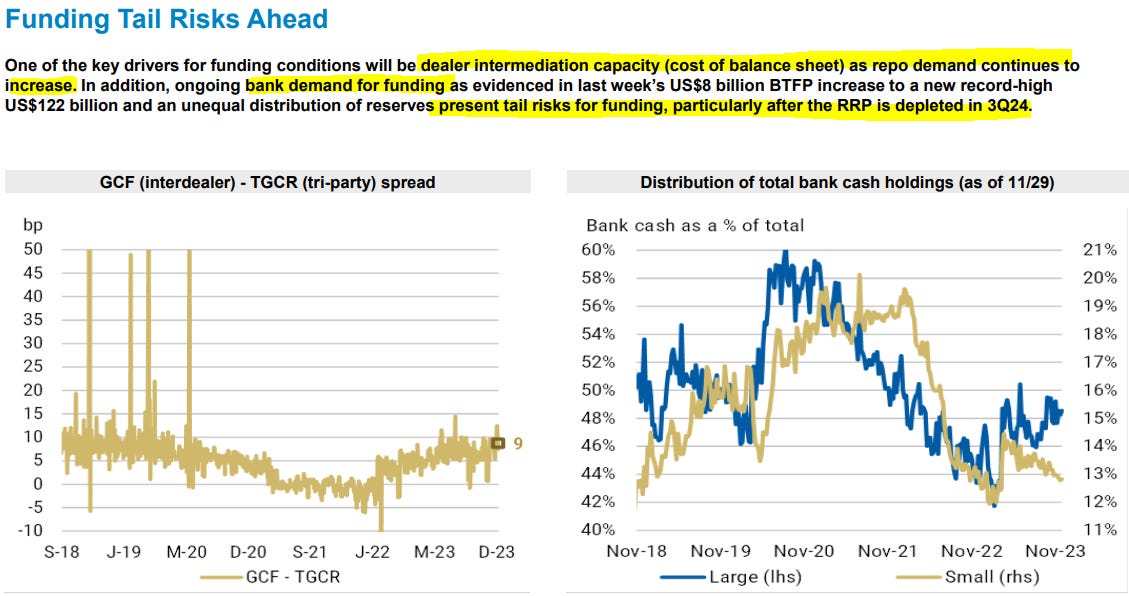

Short duration: The recent SOFR spike reflects balance sheet constraints, with dealer intermediation capacity and large UST net settlements coming into play this past month-end. We continue to see repo rates on a gradual path higher, with MMF cash in the RRP keeping funding markets orderly.

UBS (Donovan): US inflation; fantasy and fighting back

US November consumer price inflation is expected to be stable. Economists must act as second-hand car salespeople; used car prices are a volatile (probably declining) component. Record numbers of people were travelling for fun over Thanksgiving (assuming seeing family constitutes fun), which may have raised leisure travel prices. The fantasy of owners’ equivalent rent adds a lot to consumer prices but not to the cost of living.

Aside from the weirdness, the US is likely to follow the developed economy trend of slowing profit-led inflation. Consumers are increasingly fighting back against the creative excuses companies have been using to justify price increases. Profit-led inflation often ends quite suddenly; and because it is irrational and infrequent, mathematical models underestimate its impact…

Wells Fargo: The Fiscal Tailwinds Are Still Blowing

Summary

Government hiring and output have accelerated this year even as indicators of private sector economic activity have shown some signs of slowing. Nearly one-quarter of the 2.6 million jobs added to the U.S. economy year-to-date have been in government, with payrolls up 2.9% over the past year versus 1.6% in the private sector. The government component of GDP (you may recall the formula GDP = C + I + G + NX from an economics class back in the day; G is government output) was up 4.7% year-over-year in Q3, near the strongest growth rates of the past 30 years.

Some of this pick-up can be attributed to a delayed rebound from the pandemic. October 2023 marked the first month in which government employment was above its February 2020 level, a threshold private nonfarm employment eclipsed in April 2022.

Flush state and local (S&L) government coffers also explain some of the strength. The vast majority (nearly 90%) of public sector workers are employed by S&L governments, and the fiscal situation for many of these entities has been relatively healthy over the past couple years. Robust tax receipt growth, significant federal aid and generally strong balance sheets have bolstered S&L governments' fiscal flexibility.

At the federal level, new policy initiatives have helped to boost output and hiring growth. More spending has started to come online for veterans, national defense, infrastructure and other areas, contributing to an acceleration in government hiring and production.

How long can this boom continue? In the near term, we believe the solid growth in government hiring and output will persist. S&L governments are still playing catch-up on hiring from the pandemic hit, and this momentum should continue a little while longer. Although S&L tax revenues are not growing as fast as they once were, they are also not collapsing. Federal aid from the pandemic is dwindling much like excess savings are for households, but the evidence suggests that these funds are not yet fully spent. Infrastructure funding from the federal government is also still ramping up, and the impact on economic growth likely will not peak for another year or two.

However, we believe the tide is starting to turn. At the federal level, the willingness to expand the deficit seems to be waning. There have been no new major fiscal expansions in 2023, a sharp contrast to the numerous bills passed from 2020-2022. As we look to next year, it strikes us as unlikely that Congress will pass any new major fiscal initiatives in an election year. At the S&L level, tax receipt growth is unlikely to return to double-digit territory anytime soon, and eventually leftover federal aid from the pandemic will be exhausted.

More broadly, fiscal austerity as a political issue may be slowly coming back into vogue amid a period of high inflation, elevated federal debt levels and rising interest costs.

On balance, the fiscal tailwinds are still blowing, but they are not as strong as they once were, and we believe they will keep fading as we get closer to 2025 and beyond. Government hiring and output can serve as one of the pillars propping up economic growth and the labor market in the near term. That said, this boost will not last forever, and the headwinds from restrictive monetary policy are still exerting a drag on the U.S. economy. In order to achieve a “soft landing,” sooner or later a Federal Reserve pivot will be needed to keep this expansion going.

Wells Fargo: Is This Housing Market Truly Different? Part I

Summary For the first time since 2012, the S&P CoreLogic Case-Shiller National Home Price Index (HPI) notched a negative year-over-year print in April 2023. While the HPI flirted with decline earlier this year, it proved to be a temporary lapse, as prices have turned around and are steadily inching higher. Uncertainty surrounding the strength of economic growth next year, combined with market participants expecting the FOMC to keep the target fed funds rate above 4% throughout 2024, suggest home prices face challenges ahead.

In this two-report series, we present two analyses to shed light on regional home prices. We use S&P CoreLogic Case-Shiller regional HPIs to determine which markets have depicted a leading or lagging behavior over the past few decades, and we estimate the potential effect of a recession on home prices. This first installment employs dashboards to visualize regional HPI trends during the Great Recession and pandemic.

WisdomTree: Prof. Siegel: My Preview to This Week’s Fed Meeting

…This week we will have a lot to report on. Normally, the week after the employment report is pretty quiet, but because the employment data came in so late, this week we have both the Consumer Price Index (CPI), and Producer Price Index (PPI) inflation reports and the Fed meeting on Wednesday.

My quick preview: the CPI and PPI will have no impact on this week’s Fed decision as there will be no change in the Fed funds rate. I also do not see this week’s inflation data impacting the Dot Plots because the Fed members already will have submitted their forecasts. I expect the Dot Plot headlines to still readout as pretty hawkish. We know the Fed funds futures markets are implying three to four 25-bp cuts by the end of 2024. I expect that will not be confirmed in the Fed Dots. But one has to remember that three months ago the Federal Open Market Committee (FOMC) predicted a rise in rates by now, which will be proven wrong this week.

So, a cautionary tale: don't put any credence in the one-year-ahead forecast of the FOMC. Powell will want to keep optionality of raising rates, particularly if there is a hot inflation report. But the data—commodity prices, oil prices and everything else—do not look inflationary.

The primary risk to equities in the first half of 2024 is a Fed that remains too stubborn to see the downward inflation path.If Powell is overly stubborn, we could see up to a 10% correction in the first half of the year, but I expect 2024 to close fairly strong once the Fed finally gets it.

The technicals of the market currently look quite strong and I see December continuing these positive trends. I see the 10-year Treasury not going much below 4% and Fed funds rate down to 3.5% by year end. Given what I see for earnings, I think the equity market is poised to perform well, and while I expect the productivity trends from advances in technology to support real economic growth, there could be a broadening participation in equity markets beyond the Magnificent 7 tech stocks.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Best Bond Forecasters of 2023 Say the Rally Is Doomed to Fizzle (i was NOT consulted :) )

Goldman, RSM see 10-year yields rising to around 4.5% in 2024

They were among the few to call this year’s yield jump

… They now say traders are falling into the same trap they did heading into the last two years: underestimating the economy’s strength and the likely persistence of inflation pressures. Signs of a slowdown in both helped drive the US bond market last month to its biggest gain since the mid-1980s, with yields tumbling sharply on speculation the Fed will cut its benchmark rate by over a full percentage point in 2024, starting in the first half of the year.

“Markets are pricing too much policy easing too soon,” said Korapaty.

The calls aren’t particularly worrisome, given that they would mean the debt market would effectively steady after being hammered by losses in 2021, 2022 and most of this year. But they highlight the risk that markets are prematurely dismissing the chance the Fed will keep rates elevated until inflation is safely reined in. The average forecast of those surveyed by Bloomberg is that 10-year yields will slide to 3.9% by the end of 2024…

The week remained particularly weak for Brent Crude Oil. The commodity declined for the seventh week in a row as it lost yet another 3.85% on the weekly basis. From the most immediate swing high of $95.35, the Brent has come off over 20% from that point.

From a technical perspective, crude has tested the important support of 200-week MA which is placed at 74.04. This was the point from where the commodity showed a mild technical rebound before closing at $75.84.

2/ Short Term Expectations From Crude Oil

Undoubtedly, the 200-week MA which is currently at 74.04 can be expected to act as a strong support at Close for the Brent Crude unless of course meaningfully violated. The commodity can be expected to show some signs of stability and a technical rebound cannot be ruled out.

This technical rebound, if and when it occurs, is likely to stay capped and limited in its extent. The commodity may find stiff resistance in the confluence zone of 10-week MA and the 40-Week MA which exists between 83.87 and 82.12. The crossovers of 10-, and 40-Week Mas have always had their impact on the price trajectory of the commodity. With these MAs moving towards a negative crossover (this would happen when the 10-Week MA will cross below 40-Week MA), the upsides and technical rebounds may find strong resistance here. Any violation of the 200-Week MA will make the commodity incrementally weaker.

I'm really bummed to admit I passed out instead of turning on the tv first, DAMN! As a fellow Fedora wearer the agent's Fedora is the BOMB!

I'll read later...

How about those Giants !!!!!!!

https://www.dailymail.co.uk/sport/nfl/article-12853299/tommy-devito-family-celebrations-new-york-giants.html