Good morning … what a weekend and I’m NOT going to patronize you and suggest I’ve something to offer you’ve NOT yet heard. A few bulleted points of interest,

UBS agreed to buy Credit Suisse for CHF 3bn with the SNB providing a CHF 100bn “liquidity assistance loan” backed up by a guarantee of CHF 9bn from the Swiss Government.

FINMA demanded the Credit Suisse Additional Tier 1 (AT1) debt be written down to zero as part of the deal: The FINMA statement said “The extraordinary government support will trigger a complete write-down of the nominal value of all AT1 shares of Credit Suisse in the amount of around CHF 16 billion, and thus an increase in core capital”.

The Fed made joint announcement with BOE, ECB, BOC, BOJ and SNB to increase frequency of USD swap lines from weekly to daily.

Yellen and Powell issued joint statement that they welcomed “the announcements by the Swiss authorities…to support financial stability.”

I will NOT offer my opinion (although I will say I do agree with MSs Mike Wilson, “This Is Not QE” just below).

I cannot help but think there is also never just one cockroach (FRC shares down hard. again?) and this great deal by UBS has really yet to be ‘litigated’ by all of us as we’ve only been spoonfed SOME of the details of the deal we are to embrace.

Will there be continuation of a RELIEF RALLY? Today on into / through Wednesday’s FOMC? JPOW & Co. certainly hope so … For now, the Fed chimed in again Sunday night,

Feel better? … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly (for these days) higher and well off their earlier highs this morning after a giant Swiss bank agreed to a rescue deal for its once-giant rival. DXY is modestly lower (-0.1%) while front WTI futures are lower too (-1.8%, see attachments). Asian stocks were paced lower by the Hang Seng (-2.65%), EU and UK share markets are modestly higher while ES futures are showing +0.13% here at 6:55am. Our overnight US rates flows saw an active London morning session with decent 2-way flow, especially in the front-end. Overnight Treasury volume roughly matched the recent, elevated average.

… a March close in Treasury 2yrs below 4.032% (last month's low print) would itself confirm a bullish outside month and we discussed Friday morning that the last time this occurred at a move high was in November 2018.

… and for some MORE of the news you can use » IGMs Press Picks for today (20 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS. THIS PAST WEEKENDI offered more from the narrative creation machine (ie Sellside Observations for the week ahead HERE — MOST OF WHICH WAS WRITTEN BEFORE DETAILS OF THE UBS / CSFB DEAL). Where to next?

… This weekend felt like being transported back into 2007-2008 in many respects with a race-against-time deal between UBS and Credit Suisse being put together in full view of the market. The most remarkable thing about yesterday was the huge swings in Credit Suisse AT1s on a Sunday. Clips of the $17.3bn of outstanding CS AT1 bonds seemed to trade at both ends of a mid-20s to around 70c range as the outline of the UBS deal filtered through. It was eventually a shock that the AT1s were zeroed in the deal even as UBS eventually bought CS for $3.3bn, a firmly positive number. This was however less than half what they were worth at the close on Friday and down 99% from their peak pre-GFC. The decisions to wipe out AT1 bondholders is going to be the biggest issue medium and longer-term for the European banking sector, especially when the company was bought with a positive value yesterday…The good news at the macro level is that the CS situation has been dealt with and there are no obvious European next shoes to drop at this stage. CS had been decoupled from the rest of the continents' banking sector for months now and therefore was by far and away the weakest link when the US regional banking woes began less than 2 weeks ago. So the market has now got to balance the reduction of systemic risk with the likely higher cost of some forms of bank capital. There will also be nervousness as to how easy it was to change laws and market conventions in order to get this deal done. Some risk premium will surely be factored in to the cost of capital for the sector now.

Here are a couple things from the inbox AND intertubes to help distract (semi inform) and get you TO this evenings markets opening and whatever it is the authorities have decided and lined up.

First an economic WORLDview from the ivory tower and Seth Carpenter,

The Weekly Worldview: Financial Stability Meets Inflation Amid turmoil in markets, tightening monetary policy just enough – but not too much – got a lot harder to gauge.

… In the debate, the question arises if central banks will shift focus from inflation fighting to financial stability. This framing of the question, I think, misses the point; indeed, I see it as a false dichotomy. Inflation-fighting central banks are raising interest rates very intentionally to tighten financial conditions, and thereby slow economic growth. With slower growth, inflationary pressures should abate. The challenge is to tighten conditions enough to slow the economy, but not so much as to cause a deep recession. In that context, the current market volatility has the potential to tighten financial conditions and hurt economic growth. So if a central bank refrains from hiking, it is not a focus on financial stability at the expense of macroeconomic objectives, rather it is trying to calibrate whether more hikes will push conditions so far that the real side of the economy is hurt too much.

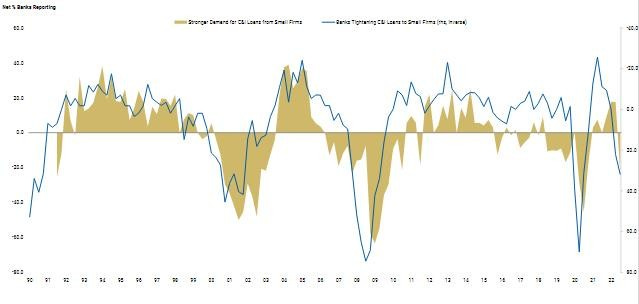

Even before last week, credit availability for C&I loans was falling

… For the Fed, our US team still thinks the Fed will hike 25bps at the March meeting. If the new measures have calmed funding markets, they can proceed with their intended hiking cycle. If not, they will have to assess how much the volatility will restrain the real economy. For example, will a higher cost of funding and reduced risk appetite lead to a reduction in bank lending? Rising rates and slower growth were already expected before the banking issues started, so the question is how much more slowing we get. Framed that way, it is perhaps clearer to see why the financial stability versus inflation dichotomy is a false one. More slowing will mean a lower path over time for policy, but as I noted above, so far, things seem to be more idiosyncratic than systemic.

But if liquidity in money markets remains impaired for an extended period, QT will have to be considered. The Fed has announced that it will at some point slow QT and eventually end QT. We do not think either is imminent, but if money markets deteriorate, the Fed will react. One interesting question to assess for the end of QT is whether banks now structurally will have a higher demand for deposits at the Fed (reserves) than before. If so, the so-called “scarcity” level of reserves has just moved up.

So where does all of the above leave us? For now, if lending can isolate the financial stability issues, then policy tightening will continue as expected. But to the degree that financial conditions are simply tighter than before, and slow the economy more than expected, policy will have to react. Moreover, the calibration of policy restraint just got harder, so tightening just enough, but not too much, certainly got harder to gauge.

Given the happenings over the weekend, and some recon from Twitter as well as Terminal, it is said that

…The events this past week correspond to a 1.5% increase in the Fed Funds rate. In other words, monetary policy has TIGHTENED to a degree which is associated with increased risks of sharper slowdown

Furthermore, according TO BBG economics (Anna Wong), the market induced tightening would be equivalent of 50bps HIKE every Fed meeting until the end of 2023,

Go ahead and discuss … AND for our inner stock jockey, this from MSs Mike Wilson

This Is Not QE; Focus on the Fundamentals With the back-stopping of bank deposits by the Fed/FDIC, many equity investors are asking if this is another form of QE and therefore "risk on." We argue it's not, and instead represents the beginning of the end of the bear market as falling credit availability squeezes growth out of the economy.

This Is Not QE...Once again, bond and stock markets seem to be diverging with their messaging on growth, with bonds seemingly pricing a hard landing and stocks still choosing a soft landing outcome. Part of this divergence is based on the view we hear from many that the Fed/FDIC back-stop of deposits equates to a form of QE and is therefore "risk on" for stocks. We disagree with that conclusion and think the focus should be on the more likely deterioration in growth due to the incrementally restrictive lending/credit environment that is now upon us. We also advise against the view that mega cap tech is immune to these growth concerns; we recommend positioning in defensive, low-beta sectors and stocks.

Why It's Not Prudent to Ignore the "Soft" Data...The main driver of our below consensus earnings forecast is our model that is based on soft data points like surveys and business cycle indicators. The pushback we have received to our forecast has consistently been that the "hard data is holding up" and "companies are not seeing the slowdown you are forecasting." However, now we have the elusive catalyst that should lead to a convergence of the hard data with the soft data...a reflection of growth risks that have been in place for months.

Breadth Is Deteriorating...We think it's worth noting that performance breadth measures are breaking down broadly. On this front, we flag the material relative underperformance of the S&P 500 Equal Weighted Index vs. the Cap Weighted Index. Further, the cumulative advance/decline series for the Nasdaq Composite Index has fallen significantly over the past several weeks, diverging from price. Ultimately, these are signs of unhealthy market internals, in our view.

… According to the Fed’s weekly release of its balance sheet on Wednesday, the Fed was lending depository institutions $308B, up $303B week over week. Of this, $153B was primary credit through the discount window, which is often viewed as temporary borrowing and unlikely to translate into new credit creation for the economy. $143B was a loan to the bridge banks the FDIC created for Silicon Valley Bank and Signature. Only $12B was lending through its new Bank Term Funding Program (BTFP), which is viewed as more permanent but also unlikely to end up converting into new loans in the near term. In short, none of these reserves will likely transmit to the economy as bank deposits normally do. Instead, we believe the overall velocity of money in the banking system is likely to fall sharply and more than offset any increase in reserves, especially given the temporary/emergency nature of these funds. Moody’s recent downgrade of the entire sector will likely contribute further to this deceleration. Herein lies the ultimate question for equity investors, in our view—will the Fed/FDIC backstop of deposits lead to a reversal in the plummeting M2 growth or will the concurrent fall in velocity of money from the credit crunch more than offset the increase in the Fed's balance sheet?

Exhibit 5: Money Supply (M2) Growth Is Already in Negative Territory...Will the Fed/FDIC Backstop Reverse This or Will It Fall Further as the Velocity of Money More than Offsets the Increase in the Fed's Balance Sheet

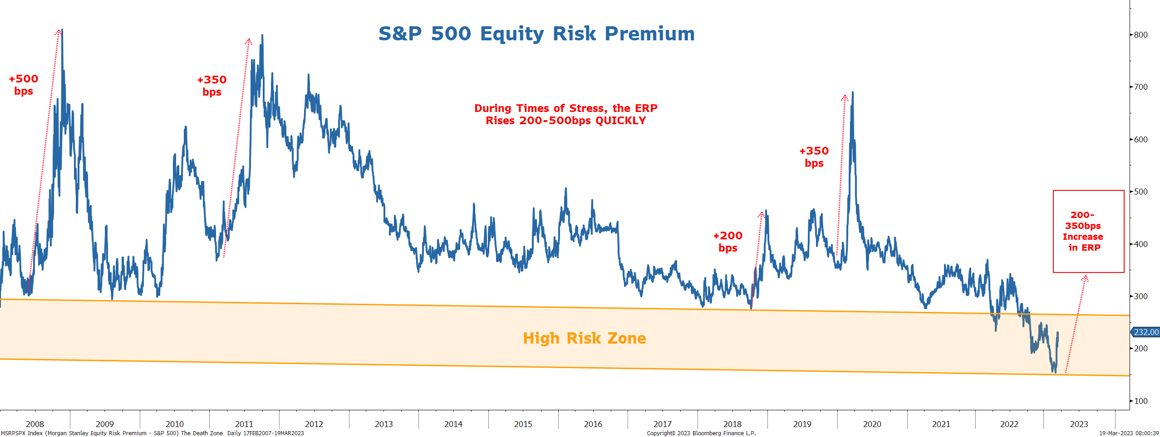

… From an equity market perspective, the events of the past week mean that credit availability is decreasing for a wide swath of the economy, which may be the catalyst that finally convinces market participants that earnings estimates are too high...which is another way of saying the equity risk premium (ERP) is way too low. We have been waiting patiently for this acknowledgment because with it comes the real buying opportunity. Just to remind readers, the S&P 500 ERP is currently 230bp. Given the risk to the earnings outlook, risk/reward in US equities remains unattractive until the ERP is at least 350-400bp, in our view. Assuming 10-year UST yields can fall a bit further as markets begin to worry about growth more than inflation, that translates into a P/E multiple of 14-15x, 15-20% below the current multiple.

Exhibit 10: The Equity Risk Premium Appears to be Finally Adjusting for the Earnings Risk We See

The bottom line is that we think this is exactly how bear markets end—an unforeseen catalyst that is obvious in hindsight forces market participants to acknowledge what has been right in front of them the entire time…

Facts are changing faster than I can keep up in my current seat … more later and nothing Wednesday due to travel … THAT is all for now. Off to the day job…