sellside observations for the week ahead (3/20) - stuff to read before Crisis TV returns (Sunday afternoon, 4p?) with news of UBS deal to buy CSFB (?); annotated FF; message from curve

Good morning / afternoon / evening. Please choose whichever one fits best as you stumble through all the noise on the intertube (present company included) and are attempting to making your way from now until markets open Sunday evening … planning your trades and trading your plans.

The flow of news over the weekend continues and by the time I finish the next sentence, the previous one is likely to be out of date or not make sense SO I’ll be brief and anxiously look forward to earlier than normal CRISIS coverage which apparently now starts at 4pm NY tomorrow,

BAML: 60/40 may be starting ANOTHER lost decade … BNPon increasing financial risks, tighter credit conditions leading TO downgrades and defaults CSFBs updated FED CALL (pause THEN 2 more 25bps hikes) DBtakes liberty to update historical / annotated chart of FF — when the Fed tightens, something BREAKS

… AND MORE. Much, much more. Have at IT as you make your way through busted brackets, XFL and whatever ELSE you are doing to distract yourself from the intertubes before Sunday AFTERNOON … 4pm!!

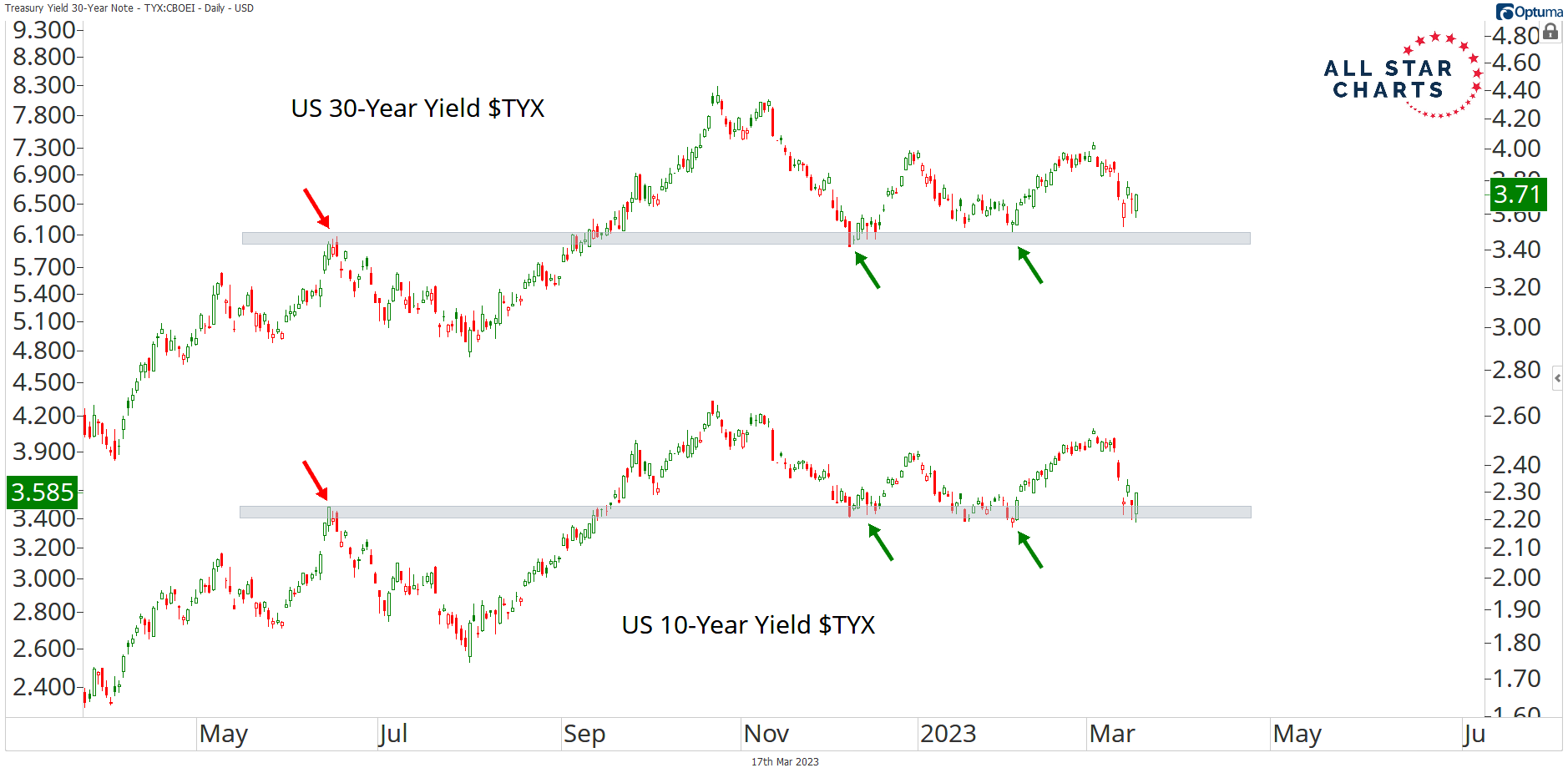

From Global Wall Street where narrativesalways follow price TO ‘fintwit’ and the intertubes … here are a few things I have seen which I felt were worth passing along as YOU attempt to decide for yourself … This first is a tweeted visual which speaks TO what the yield curve may / may NOT be screaming,

… We’re watching those pivot lows and June 2022 highs in the US 10-Year and 30-Year for confirmation.

A decisive violation of these critical levels would indicate the path of least resistance is now lower for interest rates.

And what does this all say for inflation?

Well, it looks like maybe the fed finally broke that, too.

Not only is the CRB Commodities Index making new 52-week lows, but the 5-Year Breakeven Inflation Rate just experienced its largest 5-day decline since early 2020.

We’re watching the pivot lows in this chart. If those break, you can kiss inflation goodbye.

Last but not least, here is a look at treasury spreads.

The 2s/10s spread just experienced its largest move since the early 1980s, snapping higher by about 60bps over the trailing five sessions.

Isn’t that a good thing, though? Inverted yield curves are leading indicators for recessions. Does this mean we’re in the clear now? Maybe the two quarters of negative GDP last year was the recession, and it’s behind us.

When we overlay the 2s/10s spread with the S&P 500, it paints a darker picture.

When the treasury spread reversed higher from negative territory in the past — 2001, 2007, and 2020 — historic bear markets were just getting started. In fact, the stock market literally crashed following the last three inversions and subsequent reversals in 2s/10s.

We’re not saying that has to be the case again this time. Surely, it’s a different interest rate environment today than it was back then…

I saw this Friday (and again over the weekend) and wanted to offer link and a quote from John Authers’ note Friday morning,

… For decades after the Fed under Paul Volcker slew inflation in the early 1980s, investors grew used to an environment of stable and low inflation, coupled with steadily declining long Treasury yields. The desperation tactics after the crisis, involving quantitative easing to hold yields lower, arguably extended this “Pax Volckeriana” for a decade longer than it should have lasted. But following Covid-19, the huge fiscal stimulus it brought, and the inflation and rising rates in its wake, the era of Volcker-induced peace is over.

This moment has been anxiously awaited for a long time. It’s quite possible that it will eventually bring about plenty of positive changes, after years in which capital may have been sent to the wrong places. But a degree of pain was inevitable. It would be greatest for those who had benefited from low rates and low inflation. Regional banks are near the top of the list.

In a simple long-term context, it’s not at all clear that monetary policy has tightened as much will be needed. Using a simple measure of subtracting the headline rate of inflation from the fed funds target to give a crude “real fed funds” rate, we see a record low a year ago. It remains negative. This dramatically demonstrates how far the Fed was behind the curve in responding to the inflation spike, and gives a sense of its urgency to tighten monetary policy:

Years of zero interest rates prompted investors to pay ever higher multiples for stocks…

Finally, this one caught my attention given the positive (?) developments with regards to UBS consuming CSFB (so, some resolution?) … WolfStreet

After Huge Plunge, Treasury Yields Are Due for a Big Bounce on Monday. Here’s Why

What we saw on Friday was large-scale fear of taking big uninsured deposits into a potentially gruesome FDIC weekend.

… Volatility in yields was breath-taking. On Monday, the two-year yield plunged 57 basis points, after having already plunged 30 basis points on Friday, March 10, when Silicon Valley Bank collapsed. On Tuesday, yields bounced. On Wednesday they plunged intraday and then undid some of the plunge intraday. On Thursday yields jumped 21 basis points, including an intraday recovery of 40 basis points. And then on Friday, there was such massive demand for two-year maturities that prices jumped and yields plunged 33 basis points – fear of a gruesome banking weekend.

The volatility last week in the two-year yield exceeds anything we’ve seen during the worst moments of the pandemic and during the Financial Crisis. This chart shows day-to-day changes in basis points of the two-year yield. Fear-driven panic buying:

And Monday? It’s now Saturday afternoon, and so far, so good, no collapse-announcement in the news, knock on wood. Some bank-buyout rumors in the news though about First Republic and Credit Suisse, and that would be a good thing. If this relative calm – or rather the absence of new chaos – continues, it’s going to be met with relief in the depositor and banking scene on Monday, and Treasury securities should sell off and yields should produce a circus-worthy bounce.

Food for thought as you attempt to digest UBS, BLK and CSFB news along with delightful BBG story on BUFFET being in contact with Biden on banking crisis!

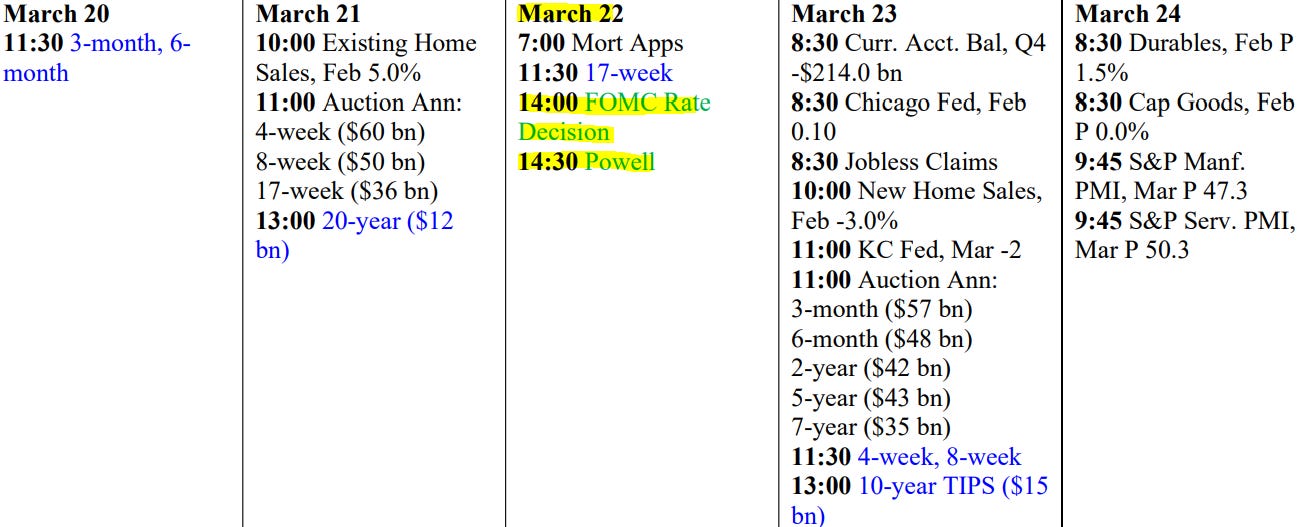

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, it would appear I’ve hit some sorta substack milestone which I didn’t really expect …

I’m grateful and at the same time, offer my apologies for any / all who’ve made it this far and are actually finding any of this funTERtaining or useful.

I’m simply trying to keep myself in ‘the game’ and up to speed with what institutional fixed income markets — and so, global MACRO — is thinking about and how to figure what MAY happen next.

I appreciate any and all feedback and will say that while I appreciate all the ‘pledges’ — that 'button’ was NOT my idea but was inserted automatically via Substack. Still, to those of you out there hittin’ it, THANK YOU but for now, there are NO plans to turn this into paid anything (like ZH premium … still trying to figure how THEY do it).

In any case, THAT is all for now. Enjoy whatever is left of YOUR weekend as I’m still soaking in all the turns of events here in the week just past and the several crucial hours just ahead for us all

In this swarm of narratives we'll, likely as not, never know which is the real Cassandra. Such a confused din suggests it may really all be, in one ERA and out with the other, after all is said and done.

In this swarm of narratives we'll, likely as not, never know which is the real Cassandra. Such a confused din suggests it may really all be, in one ERA and out with the other, after all is said and done.