Good morning … Today is the anniversary OF Lehman bankruptcy declaration … this day always follows a very somber remembrance a few days earlier (#NeverForget). While I was not AT Lehman, thankfully I was not there when they went down (or were pushed, as it were…).

I was there when it was Shearson Lehman Brothers (joined there right from Bear Stearns … note the pattern, thankfully my partner retired on HIS terms and beware all where I am now :)).

Like many who work in finance, my life has come to have a fixed calendar: pre- and post-Lehman. When news broke 15 years ago today that Lehman Brothers had indeed gone bankrupt, with no willing buyer and no rescue from the government, things changed. We all knew that they would. The crisis had been brewing for at least 18 months at that point, and would not reach its nadir for another six months, but it was the collapse of Lehman that changed what was possible…

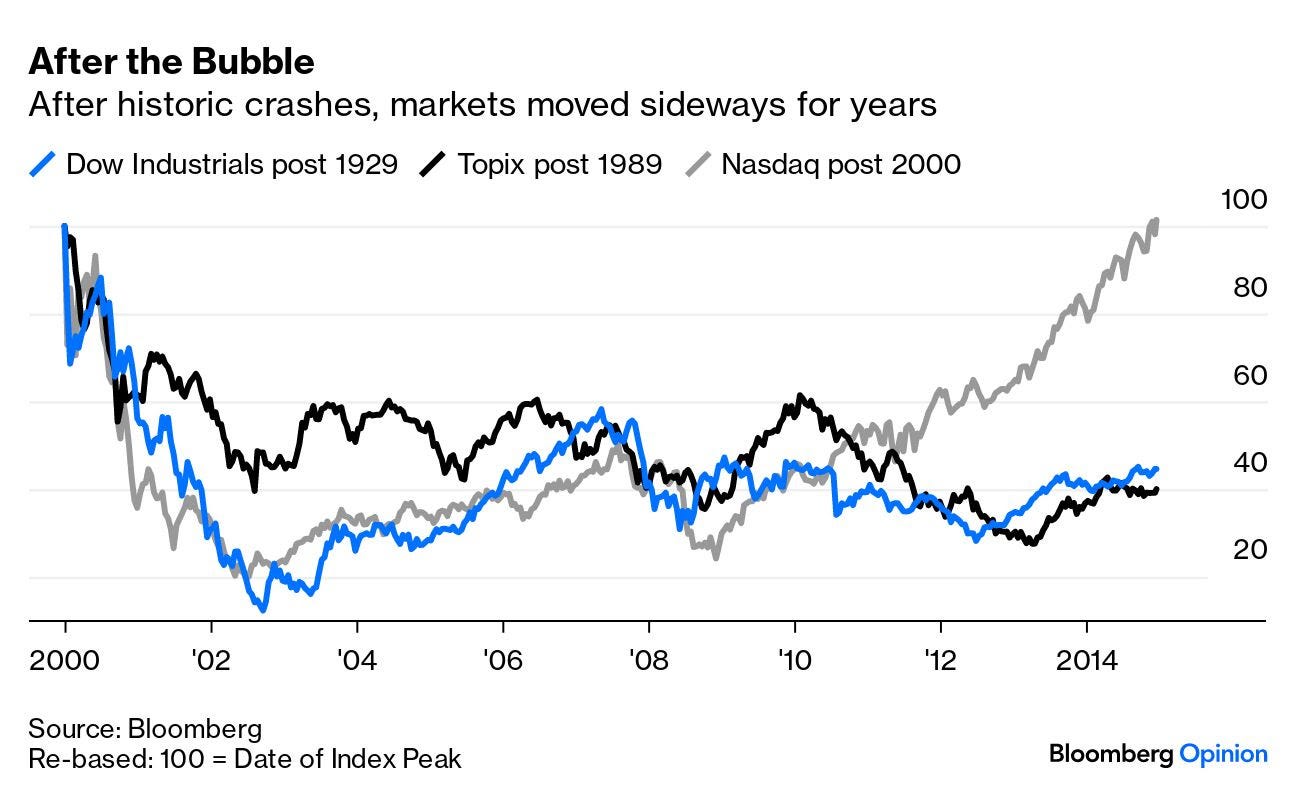

… This chart looks at the 15 years following the three most important equity bubbles before 2008: the Dow Jones Industrials after the Great Crash of 1929, the Topix after Japan’s bubble burst at the end of 1989, and the Nasdaq-100 after the dot-coms imploded in 2000. All are rebased to 100:

Nasdaq stocks staged a real recovery, after about a decade. Other than that, the pattern is clear. After the crash, markets hit a bottom and then move sideways for a long time, drifting within a range. That history left me (and many others) confident that the world should brace for crab-like markets for many years after Lehman. Value investing and skillful range-trading would be the name of the game…

I did / do have several friends and former colleagues who WERE there and so, on this day we’ll pause a moment to reflect on yet another ‘08 legacy and how it has forever changed the financial markets landscape … In whatever way / shape / form is important to you.

In overnight news, and via #FinTWIT, UAW has gone on strike … who cares? Well, we all might just be payin’ attention,

Awaiting further admin victory lapping here as it has seemed more than willing / ready / able to do with CPI, ReSale TALES and PPI … can’t WAIT To hear the SPIN as to how this isn’t a situation whereby ‘they’ (broad and VAGUE on purpose) are fighting the last war and in effort to force you and I to ‘go green’ …

At this point — early on in the season as it might be — I’d say i’m more likely to embrace Gang GREEN (J-E-T-S … JETS JETS JETS) than I am to be even ABLE to embrace the current desires … and so, off the soapbox I’ll step and move right along.

In OTHER overnight NEWS (thanks TO folks at Harkster), Chinese data dumped,

Industrial Production +4.5% vs exp +3.9% (prev +3.7%), Retail Sales +4.6% vs exp +3% (prev +2.5%). This unexpected strength has squeezed the bearish China complex and propelled USDCNH sub 7.26 and all of the correlated pairs stronger ... AUDUSD +50bps to 0.6465, NZDUSD +40bps 0.5930, etc etc. Is this data the first sign that China's small incremental initiatives will be enough to stimulate the economy and stabilise financial markets? One data set doesn't make a trend, but something to watch into year end…

FINALLY … are we celebrating today … for China data BEATS or on the day which Lehman filed? Likely NOT. A few reasons for that are, well, obvious and we can lean on the data dump HERE in the USofA just yesterday …

CalculatedRISK: Retail Sales Increased 0.6% in August ZH: Retail Sales Unexpectedly Soared In August, As Gasoline Costs Jumped ZH: Producer Prices Soar In August As Goods Inflation Reignites ZH: ECB "Surprises" With Tenth Consecutive Hike To A Record 4.00%

… serving to confuse / COMPLICATE markets a bit further.

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with EU and UK bond markets leading down after a long stretch of outperformance. The news we found is linked above. DXY is lower (-0.12%) while front WTI futures are modestly higher (+0.4%). Asian stocks were mostly higher (ex-China), EU and UK share markets are all higher (SX5E +1%) while ES futures are showing +0.15% here at 7am. Our US rates flows saw a grind higher during Asian hours on weak volumes and little flow apparently. During London hours, Asian strength was reversed in thin conditions with demand for 2's >5% and interest in steepeners persisting. Overnight Treasury volume was ~95% of average overall with 30yrs (125%) again seeing relatively elevated turnover this morning.

… and for some MORE of the news you can use » Morning Call Script - 15 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

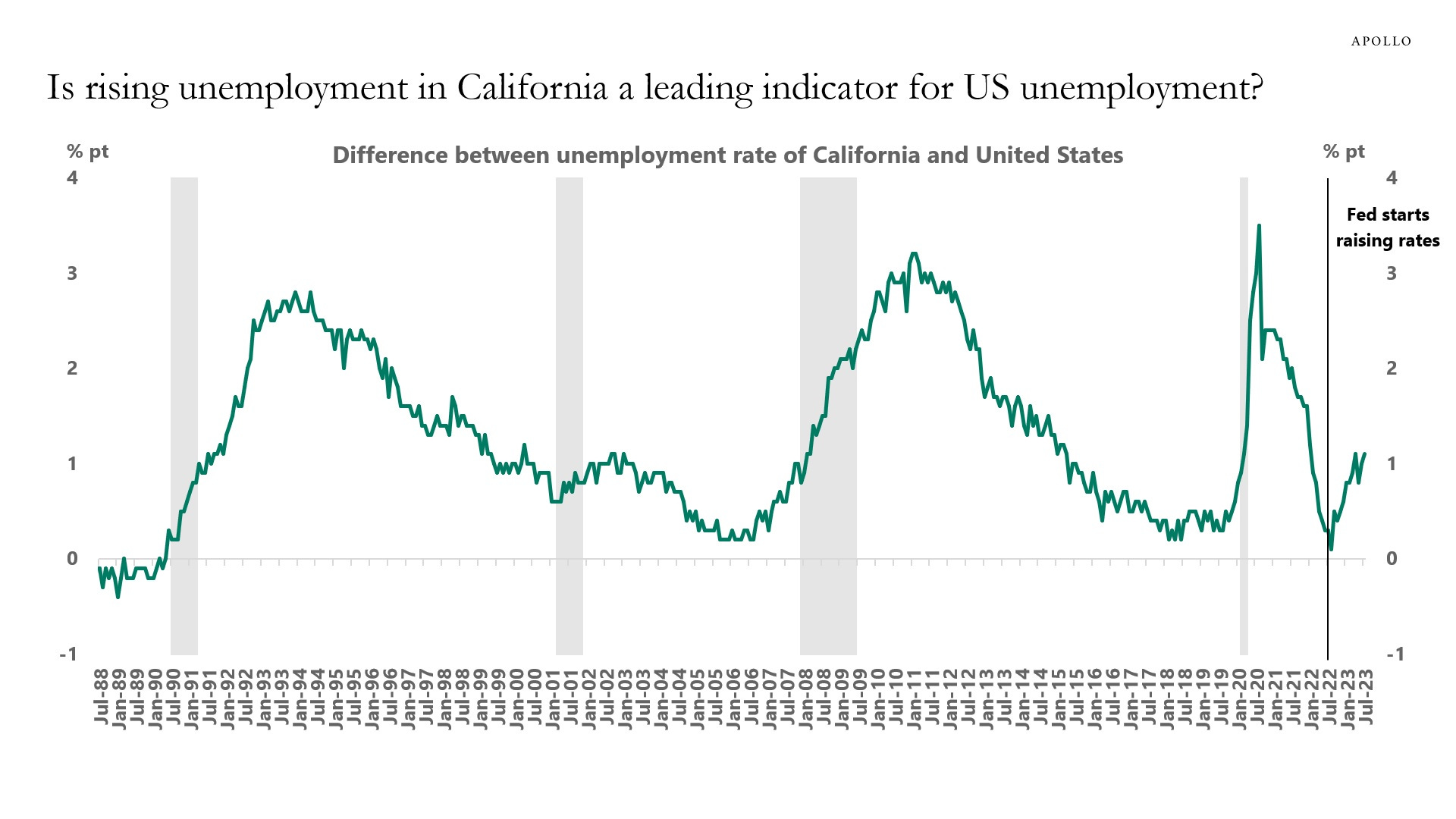

Apollo - Is Rising Unemployment in California a Leading Indicator for US Unemployment? (what happens in CA apparently does not STAY in CA)

Fed hikes have had a very negative effect on venture capital and tech firms because they have little or no cash flows and require financing that has become much more expensive.

This is likely the reason why the unemployment rate since the Fed started raising rates has increased more in California than in the rest of the country, see chart below.

High costs of financing slows down capital formation. That is how monetary policy works. With the Fed on hold for another nine months, the ongoing softening in the labor market continues.

Barcap - Retail sales: July's mountain becomes a hill (I thought we were supposed to make mountains outta mole hills … lets get to work then, sell side …)

Higher gas prices and a stronger-than-anticipated control group reading helped lift retail sales 0.6% m/m in August. However, July estimates were revised down considerably, implying less of a pull-forward effect on spending at the onset of Q3. On net, the numbers put consumer spending on similar footing, in our view.

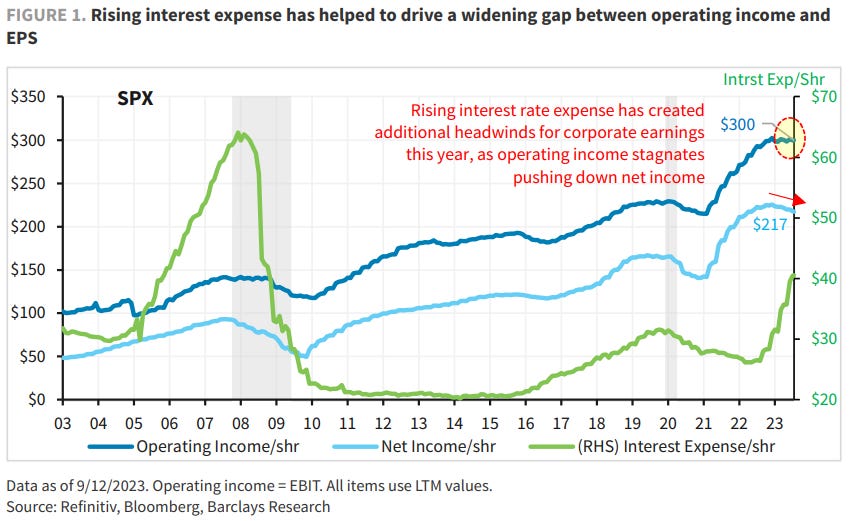

Barclays - U.S. Equity Strategy: Food for Thought: Interest Expense Takes a Bite Out of Earnings (so, higher yields ARE gonna matter, then, after all? laws of gravity haven’t yet been repealed?)

After climbing steadily throughout the Fed hiking cycle, interest expense within the S&P 500 has risen to levels not seen since the GFC and is contributing to a growing wedge between operating income and EPS. With rates set to stay higher for longer, rising interest expense poses another hurdle for '24 EPS growth.

BMO - Retail Sales Beats, PPI Stronger, Jobless Claims Still Low - UST selloff (3 strikes and we’re OUT…?)

Retail sales in August surprised on the upside at 0.6% MoM vs. 0.1% MoM expected and 0.7% MoM prior - a strong read despite the rumblings of a disappointment that were making the rounds before the number. The details were firmer as well with ex-auto and gas up 0.2% MoM vs. -0.1% MoM expected and most important for consumption estimates was the control group that rose 0.1% MoM vs. -0.1% MoM seen and last month's 1.0% MoM read. A strong spending print for August that will help Q3 growth estimates…

… The market found a bid following the ECB's 25 bp hike earlier this morning, and since the data has been released the curve has bear flattened with 2-year yields back above 5%, and 2s/10s dropping briefly back below -76 bp…

CSFB - CS House View - China Data: When the ocean is tumultuous (that ‘ole ancient proverb … when the tough gets going, PBoC cuts rates? no, that ain’t it … at least not exactly…)

We mentioned in a recent report that we might soon be above consensus with our 5.1% economic outlook for this year (link). Indeed, as of today, we are now modestly above market consensus for Q323 GDP growth given that so many economists have drastically reduced their forecasts for this year. (See Figure 1.) Yet, we have cautioned our audience against reading too much into the drastic changes to consensus forecast. Today’s above-consensus data releases out of China (IP, FAI, retail sales) are a perfect example of our caution. (See Figures 2, 3, 4 and 5.)

With the recent reduction to RRR materializing in line with our expectations, we believe that the PBoC will not reduce the RRR again before the end of the year. Despite the recent highlight of the structural challenges China’s economy has been facing, none of these issues should be news for close watchers, and hence should not be used as justifications to drastically reduce China’s outlook, let alone as justifications of an imminent collapse. Today’s data releases suggest that 2023 will most likely not go down in history as the year of China’s economic implosion.

Looking ahead, we expect China to continue its structural deceleration, as exemplified by our 4.4% GDP forecast for 2024, a forecast that we have maintained since the end of last year (link). We fully acknowledge the structural challenges and have not been shy to point out that the authorities do not have effective policy tools to reaccelerate household demand in a sustainable manner (link). The deleveraging trend by Chinese households will continue for years to come (link). We also worry about a significant correction to China’s house price in 2024 (link). Yet, we advise our readers to keep these challenges in perspective. For the foreseeable future, China will remain the factory of the world despite geopolitical tensions, placing a floor underneath China’s economic growth.

There is a famous saying in Chinese: “When the ocean is tumultuous, heroes show their true colors.”

FirstTrust - Retail Sales Rose 0.6% in August (NOT as good as it looked)

… Implications: You can't always judge a book by its cover. The headline increase of 0.6% in retail sales suggests the consumer is thriving, easily beating the consensus expected gain of 0.1%. However, factoring in revisions to previous months, retail sales only registered a modest 0.2% increase. Also, the August surge in sales was predominantly fueled by a substantial 5.2% spike at gasoline stations, as pump prices skyrocketed by 10.6%. In other words, higher sales were due to revisions and inflation and doesn’t reflect higher living standards…Our view remains that the tightening in monetary policy since last year will eventually deliver a recession. Expect more deterioration in real retail sales later this year. In employment news this morning, initial claims for jobless benefits inched up by 3,000 last week to reach 220,000, while continuing claims rose by 4,000 to 1.688 million. These figures suggest continued job growth in September.

FirstTrust- The Producer Price Index (PPI) Rose 0.7% in August

… Implications: Producer prices jumped 0.7% in August following a large rise in July, reminding the Fed that the inflation fight is still far from over…While modest core inflation readings are welcome, data from yesterday’s CPI report reiterates that the Fed hasn’t reached the finish line. When the Fed meets next week, they will most likely keep rates unchanged, but we expect they will make clear that a further hike remains on the table. The economy is in the grip of a battle between the ongoing impacts from the tsunami of money that hit the system in 2020-2021 and is still being absorbed, while at the same time starting to show signs of the riptide from the Fed and Treasury Department pulling money out of the system in the past year. Economic growth remains positive, but we still believe a recession is on the horizon. How the Fed will respond if/when a recession appears is very much an open question. The Fed’s failures in the 1970s should be a stark reminder of the painful results of easing before the battle against inflation is fully won.

BOTTOM LINE: August retail sales rose 0.6% and core retail sales edged up 0.1%—both above expectations and despite a high hurdle from Amazon Prime Day in July. However, spending was revised lower in prior months. We will update our GDP tracking estimates after the mid-morning data. Combining data from the latest retail sales and CPI reports, we estimate that real core retail sales were unchanged in August. The producer price index (PPI) increased by 0.7% in August, above consensus expectations. Core measures were roughly in line with consensus expectations, as the PPI excluding food and energy increased 0.2% and the PPI excluding food, energy, and trade services increased 0.3%. Based on details in the PPI and CPI reports, we estimate that the core PCE price index rose 0.14% in August, corresponding to a year-over-year rate of +3.81%. Both initial and continuing jobless claims edged slightly higher.

Wells Fargo - Upward Surprise in August Sales Overstates Consumer Resilience (the revisions…? nope … the SOURCE of surprise > the surprise itself..)

The upward surprise in retail sales can be traced to a few retailers—autos and gasoline —and is somewhat price related. Control group sales rose 0.1%, more in line with expectations, and when considering downward revisions, consumer spending is still tracking for a solid Q3 gain, albeit a bit weaker than we were previously expecting.

■ Headline retail sales rose +0.6% in August, continuing a string of 3 months of surprisingly strong consumer spending. ■ Unlike June and July, however, it looks like this month's retail sales numbers were boosted by gasoline station sales, fueled by a ~$0.40/gal jump in pump prices. Outside of gasoline, spending was much more modest in August. ■ Control group sales rose only 0.1% in August, after rising +0.7% in July. This is the smallest increase in control group sales since March. Q3 started off on strong footing, but we suspect the end of the quarter will be slower as the tailwind from summer travel and recreation spending dissipates. ■ The +0.1% increase in the control group suggests that nominal PCE will be up +0.4% in August, with real PCE unchanged. ■ If we assume no change to the level of PCE in September, this implies a +3.5% increase in real PCE for Q3, and a contribution of 2.3% for Q3 GDP. ■ Even though the August data shows some significant mean reversion from strength in June and July, we continue to expect that there will be more downside risk in September.

AND from the intertubes,

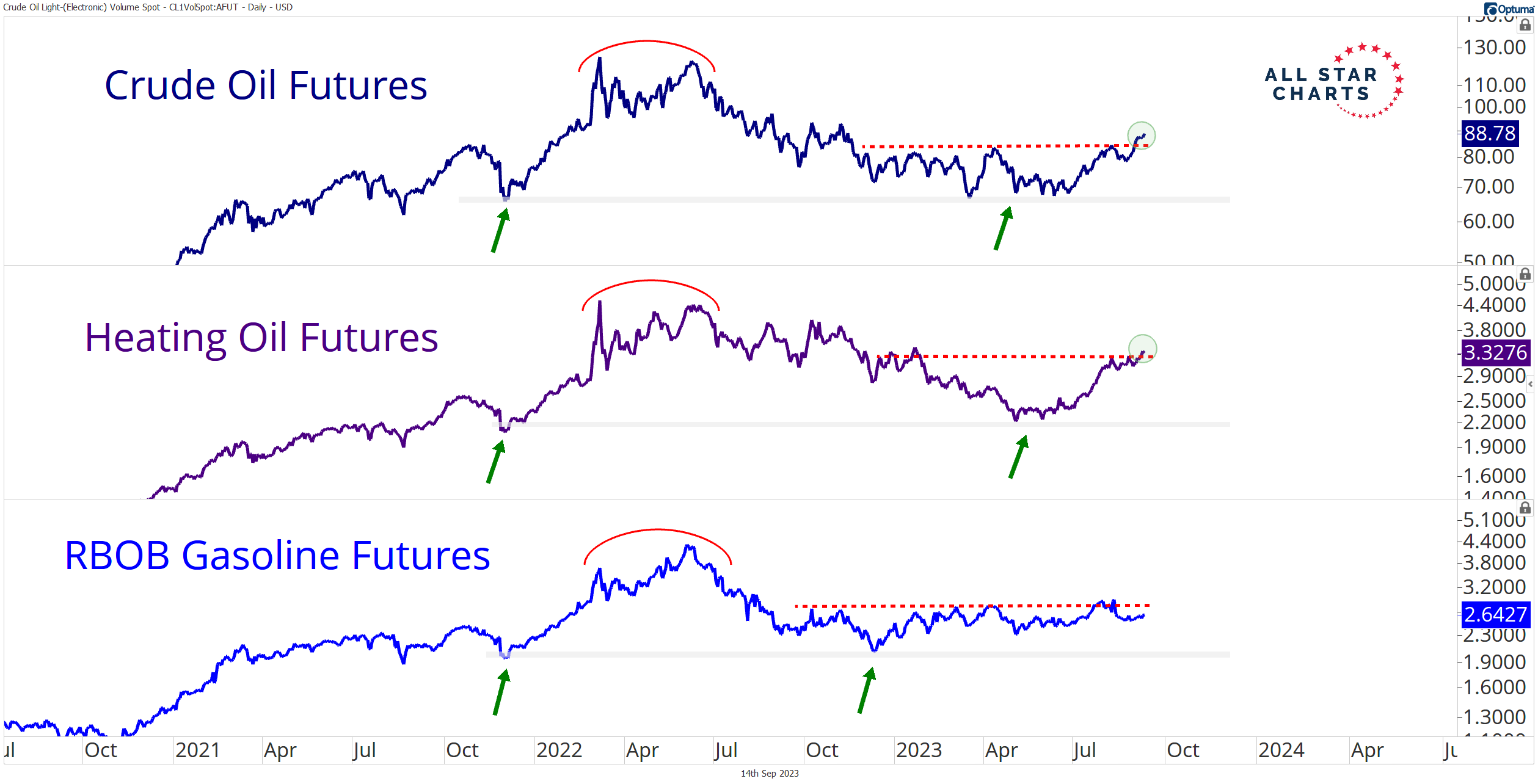

AllStarCharts- Here’s Why Gas Prices Are Heading Higher (NOW we know… and NOW they tell us….)

Energy stocks and commodities remain front and center.

Our equity plays are running toward our upside objectives. Natural gas is attracting a bid. And bulls are eyeing $100 crude.

With that as our backdrop, we reviewed the energy space on yesterday’s “What the FICC?” episode.

And it appears the next leg higher for crude and its crew has commenced…

Check out the triple-pane chart of crude oil, heating oil, and gasoline:

Gasoline stole the spotlight yesterday as the sole culprit for a higher-than-anticipated CPI print.

Yet crude and heating oil are exhibiting relative strength, eclipsing their summer highs – a feat gasoline futures have yet to accomplish.

It’s only a matter of time before gasoline joins the pack if the breakouts in crude and heating oil hold. If and when it does, we expect broadening participation among energy stocks…

BarChart TWEET (POSITIONS matter and for every seller there’s a buyer)

Kimble - Cap Weight vs Equal Weight Divergence, Sending Sell Signal Warning Signal? (some visual ‘food for thought’)

We often watch the performance of cap weighted indices versus the equal weight counterpart.

Why? Because divergences in performance often signal market turns.

Today is no different as we display the performances of the S&P 500 cap weight index versus the S&P 500 equal weight index.

And, as you can see, there is a wide divergence brewing.

The past 2 times that the cap weighted index was performing much stronger than the equal weighted index, stocks were near a short-term high. And shortly thereafter they declined sharply.

We are seeing the largest spread in the past 6 years between the two indices right now and the question we should be asking ourselves is: Will the result be different this time? …

Finally, ahead of the weekend that kicks off with holidays tonight (Happy New Year and Shanah Tovah), ‘posting’ here might be lighter than normal and I might NOT get an update out ahead of Sunday evenings futures … Friends, family and celebrations FIRST and so, thank you in advance for understanding.

SHOULD you require a partial refund for your free subscription, please reach out and we’ll make arrangements!

Thanks in advance and again, my apologies for ANY inconvenience AND … THAT is all for now. Off to the day job…

Excellent Summary!!!!!

Retail Sales details, in particular....

Treasury Market is fascinating.....Professionals betting against other Professionals..

Who is right ????

Risks are for Higher Rates......Too Much Supply, courtesy of the Biden Admin.

UAW............Suicide by Union

Thanks to the UAW, as a TSLA Shareholder, I sincerely appreciate it.....