ZH: Gold Spikes To Record High Over $2,130, Bitcoin Soars Above $40,000 As Market Calls Powell's Bluff

… and then there’s this bit of ‘news’ over weekend …

ZH: Grinch: Spotify Fires 17% Of Workforce Before Christmas

… and as much as it may seem LAST WEEKS bond market price action was about JPOW and Co talkin’ the talk and some select data points like Spotify, well, that all was then and this is now …

Bloomberg: Treasuries Fall as Gold Pares Gain, Stocks Mixed: Markets Wrap

Bitcoin climbs for fifth day to the highest since April 2022

Asian shares mixed; Australia stocks gain, Japan equities fall

AND with that in mind — bonds paring gains, 2yy dropped from 4.97 this time last week … to about 4.55% Friday and now, well …

… Plenty of room for rates to RISE ()TLINE at / about 4.88) and still be within downtrend and again, noting how overBOUGHT momentum (stochastics, bottom panel) is at this moment.

Be that as it may … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower along with stocks as 1-way(?) tactical positioning gets tested after a nice run for both markets. DXY is little changed while front WTI futures are -0.5%. Asian stocks were mostly lower, EU and UK share markets are mixed while ES futures are -0.3% here at 6:50am. Our overnight US rates flows saw a quick retrace of Friday's rally during Asian hours with the curve bear flattening on notably high volumes (5's and 10's especially). During London hours, selling in the belly from real$ was a feature but on much lighter volumes than seen during Asia's trade. Overnight Treasury volume was ~90% of average overall.

… Our first attachment was your author's main focus last week: the monthly chart of 5yr real yields (TIPS). This is a super bullish chart for two reasons: 1) long-term momentum confirmed a new bull signal at Thursday's close after being chronically 'oversold' since summer 2022 and 2) Thursday's close confirmed a rare (but typically reliable) Evening Star (circled) trend reversal described here Investopedia Our take is that 5yr reals may be headed toward the 1.16 area over the coming months, at least.

Interestingly, the monthly chart of Treasury 2yr yields looks the same with a now-confirmed, bullish long-term momentum signal and a confirmed Evening Star pattern (lower yields) too. It takes years to create these set-ups, and it's exciting to have watched them get confirmed while on the road talking about them.

Our next attachment looks at the medium-term, weekly chart of Treasury 30-year yields to show how 30yr yields are back in their old range <4.50% with weekly momentum (lower panel) still clearly guiding to lower rates.

… and for some MORE of the news you can use » The Morning Hark - 4 Dec 2023 (now a PAYWALLED site) and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use (this weekend’s note with an updated look at some WEEKLY observations) … here’s SOME of what Global Wall St is sayin’ …

The FAA’s monthly Business Jet Report provides a snapshot of trends in business jet activity, and the report from November 2023 shows continued strong demand for private jets, see chart below.

BNP: Sunday Tea with BNPP: The horse has left the barn

KEY MESSAGES

Markets are looking through Fed officials’ messaging that the next policy move can be a rate hike. Although we have rallied a long way, we believe that the front end of the US curve can rally even more if the economic data disappoint.

With the markets pricing in a more proactive Fed, we think that medium-term USD depreciation is upon us.

Short-dated implied vol in US equities has reached extremely low absolute levels. We like buying options ahead of the next major US data releases.

… four of the past five annualized m/m core PCE prints have come in near the Fed’s target now. And looking at the market-implied path for CPI for the next year, the market is expecting y/y rates to steadily move back toward 2% as well (Figure 1).

With the market already pricing in a benign inflation path, the reaction to Waller has been swift. There are now roughly 135bp of cuts priced for next year - a move of 45bp in a week. Does this mean that the rally is over for now? Not necessarily. While 135bp may seem like a lot, with the cycle turning, the market needs to price in both its modal outcome of cuts, plus a risk premium that cuts may come sooner or end up being deeper than believed in the base case. Notably, inflation has fallen despite growth being very strong for the past few months. Should the economy also show clearer signs of faltering, especially on the employment side, we think that the markets have scope to price additional cut risk premium into the curve…

A 100bps move lower is on the cards for US 2y yields, after breaking below the 55w MA (4.5785%) on a weekly basis, while also posting a bearish outside week.

Why it matters: We have now set up a 55-200w MA setup, which suggests extended downside. The next notable support is at 3.55-3.65% (May and March lows) which suggests a ~100bps move lower in yields.

Furthermore, with several bearish indicators at play, we expect this move lower to be swift.

US 10y yields: We posted a bearish outside week on US 10y yields, suggesting short term downside. Unlike US 2y yields, however, we do not expect a rapid move lower, with next support at 4.05-4.09% (September low and March high). Subsequently, we still have the crucial 55w MA at 3.92%

US 30y yields: Keep an eye on September lows at 4.18%. We expect this to be a significant support level, as this is close to the 55-200d MA setup’s indicated target (200d MA is currently at 4.15%).

Gold: Price is testing resistance at 2133 (ascending trendline) after breaking above 2020/21 highs. There are no more notable resistance levels above this…

… All roads this week point to payrolls on Friday with the usual build up via JOLTS (tomorrow) and ADP (Wednesday). Elsewhere in the US the Services ISM is out tomorrow (we will also watch the employment sub component ahead of payrolls), and the initial read on inflation expectations in the University of Michigan confidence sentiment release (Friday) will be of note after 5-10yr expectations ticked up to a decade high of 3.2% last month. Remember the Fed are now on a blackout period ahead of next week's FOMC so some of the big catalyst for moves of late, i.e. Fed speakers, won't be there …

… Digging a bit deeper into the US employment picture, our US economists expect headline and private payrolls to come in at +130k with consensus at +180k and +160k respectively. The returning post-strike autoworkers will boost the data by around +30k. Unemployment is expected to hold steady at 3.9% by DB and the consensus, although our economists see the risks tilted to a 3.8% print. One thing our economists look carefully at is the diffusion index that shows the breadth of job gains. It's currently at 52%, its lowest rate since the pandemic. They show that 70% of the private job gains in the last year come from only two sectors, namely leisure and hospitality and private education and healthcare. Outside of that job creation in the last 12 months is a very lowly 0.7% and just 0.2% over the last 6. Staying with US labour markets, the JOLTS data tomorrow is also important even if it's October data. As our economists point out, while the hiring and quits rates were at or below their 2019 averages in September, the layoffs and discharges rate remained near historical lows. So that gap is keeping labour markets tight for now. Our base case is that the demand for labour eases in the next few months …

MS: US Equity Strategy: Weekly Warm-up: How Low Can Rates Go? (clearly it’s worth pausing and reading an equity guys writeup when it’s centered around RATES — not earnings, profits, etc…)

The direction of equity markets continues to be influenced by the rate of change on bond yields which have been dictated recently by the bond market's perception of future rate cuts. With ~130bps of cuts now priced through YE '24, how much lower can rates go in the context of a soft landing?

How Low Can Rates Go?... After a 20% drawdown in many stocks between July and October, equities staged an impressive rebound in November thanks to the sharp reversal in interest rates. A good portion of this reversal was due to the pricing of a much more accommodative rate cut path over the next 12 months. Specifically, 130bps of cuts are now priced into Fed Funds futures through the end of next year—a dovish expectation in the context of stable economic growth in 2024. In today's note, we present analysis on index, industry and factor performance around Fed rate cuts. Interestingly, we find that large caps outperform small caps both before and after the initial cut is delivered. In our view, December may see some near term volatility in both rates and equities before more constructive seasonal trends for equities and market expectations of a potential 'January Effect' have an impact…

… Despite Jay Powell's comments that it was premature for markets to price in rate cuts so early next year, the bond market went ahead and priced in an even greater chance of a rate cut as early as March. In fact, one can attribute a good portion of the movement in 10-year Treasury yields over the last 6 months to changes in the bond market's view on what the Fed will do over the next year. From our perspective, the Fed hasn't really changed their guidance all that much over this period but the bond market's view is what matters. The net effect of this perceived pivot (both ways) hurt bonds and stocks between July and October and has helped considerably since then ( Exhibit 2 ).With 130bps of cuts now priced into the Fed Funds futures market through year end 2024, investors have set a high bar for cuts to be delivered.

MS: Sunday Start | What's Next in Global Macro: Decluttering the Closet: Status of the US Consumer

Is the US consumer breaking records this holiday? Or is spending disappointing? The media is offering simple narratives around this debate but, like most things in life, it's complicated. The signal through the noise, in our view, is that the US consumer remains resilient, but cautious and choosy, and with divergent trends beneath the surface regarding consumer categories and shopping channels. Taken together, this syncs with some of our core views for 2024: our economists’ expectations for the US to avoid recession, but with cooling growth over the course of 1H24, setting up policy rate cuts; and our strategists’ expectation of better total returns for high grade bonds as Treasury yields drift lower in sympathy with macro trends….

… Putting it all together, the US consumer is neither the juggernaut that some media headlines might lead you to believe nor the canary in the coal mine suggested by other headlines. This syncs with our economists’ view that the US avoids recession but still slows. The implication for Fed policy? Policy rates in most DMs will likely be on hold until the end of 1H24 before normalization begins and picks up in 2H24. We think that this should support bond returns, with Treasury yields tracking lower to reflect expectations of reduced policy rates, and high grade credit spreads holding steady along the way to reflect resilient fundamentals.

Wells Fargo: December Flashlight for the FOMC Blackout Period

Summary

We look for the FOMC to keep rates on hold at its December 13 meeting, an expectation that is universally shared. If realized, the third consecutive hold would suggest that, rather than the FOMC merely hiking at a slower pace, the fed funds rate probably has reached its terminal level of this cycle.

Both sides of the Fed's mandate are moving toward their longer-run estimated levels. The labor market is becoming less tight, and inflation continues to recede.

That said, inflation has not yet receded all the way back to 2%. Consequently, we expect the post-meeting statement will keep the door open to the possibility of additional tightening this cycle. However, while the statement likely will indicate that further tightening remains possible, we would not be surprised for it to hint that another rate hike is less probable.

A more benign inflation outlook is the key to what we believe will be a flat-to-modestly-lower "dot plot" in the Summary of Economic Projections released at the conclusion of the meeting on December 13. We expect that the median dot for year-end 2024 will shift down from 5.125% in the September SEP to 4.875%. For 2025 and beyond, we suspect the median dots will be more or less unchanged.

We look for the FOMC to maintain its current pace of balance sheet runoff (i.e., quantitative tightening).

… And from Global Wall Street inbox TO the WWW,

Bloomberg: 5 things to start your day (Asia with a fincon chart)

… Federal Reserve Chairman Jerome Powell pushed back against investor expectations for rapid 2024 rate cuts. The market pushed on with its assessment that policy easing is coming soon, signaling about 70% odds for a lowering in borrowing costs in the first quarter and fully pricing in five 25-basis-point reductions by the end of next year. The overwhelming consensus that the Fed will reverse rapidly is already helping to create looser conditions — a dynamic that could sow the seeds for some destructive pullbacks from the past month’s sizzling rallies. Financial conditions have swung rapidly toward stimulatory settings since late October. A Bloomberg gauge that tracks them is close to the highs touched in late July and mid-September.

Those peaks came around the times when Fed meetings delivered hawkish surprises — not in terms of action, but in the central bank’s rhetoric and outlook. The Fed’s July hike was forecast by all but four of 111 economists surveyed at the time, and the September hold was similarly anticipated. Each time, though, yields moved substantially higher within days as Fed speakers emphasized a willingness to hike again. That raises the potential for another hawkish shock for markets unless the Fed is convinced that inflation dangers have definitively cooled. Some officials cited the ramp up in yield in September and October as meaning the Fed may need to do less to tame inflation. It will be interesting to see if the return of financial conditions to the easier settings in place before that makes them consider the possibility they may need to do more.

Bloomberg: 5 things to start your day (EZ with a GOLD chart)

… Right after the starting bell in Asia this morning, spot gold punched its way to a record, coming out swinging as traders in Singapore and Tokyo were barely into their second cup of coffee. What’s more, this ascent looks set to extend into the new year.

The precious metal is well-placed as speculation that the Federal Reserve is fully done raising interest rates gathers momentum, even if Chair Jerome Powell wants to push the case that policymakers are in no hurry yet to ease.

Bullion’s fighting spirit has lifted its 14-RSI well into overbought territory, so at some stage there’ll be a pause, or minor retracement. But overall, this rally will build over December and into 2024 as buying interest picks up.

Bloomberg: 'Everything Rally' brings out the mealy-mouth in Powell (THE Authers OpED with some thoughts / a chart from BIANCO)

Attempt to rein in markets to again do the Fed’s job was blown off in a matter of minutes.

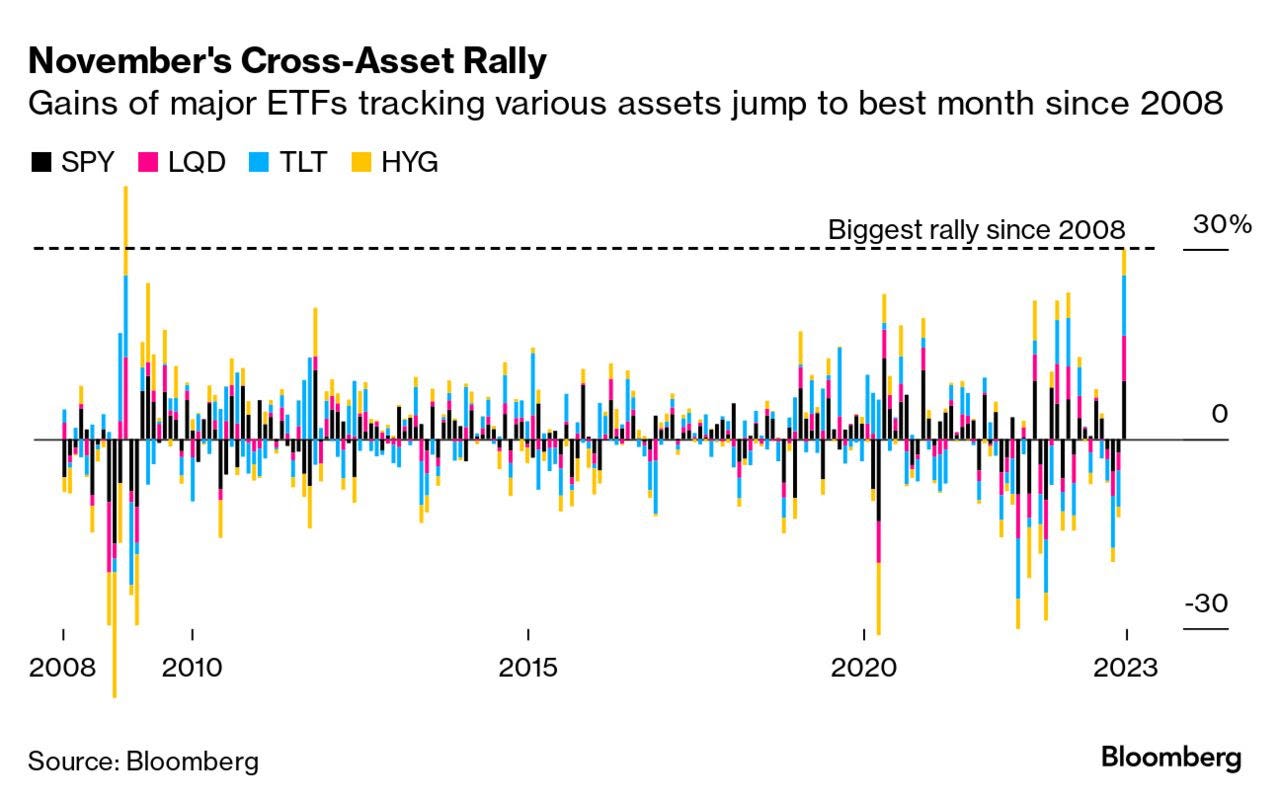

… And so it was that November’s “everything rally” extended for at least one more day into December. The rise in bond prices, and fall in their yields, has been in the driving seat, but more or less everything else has gained as a result, as demonstrated in this chart of monthly returns for exchange-traded funds covering US stocks, cash,long-term Treasuries and high-yield bonds. Add them together, and November was the biggest monthly rally since the chaos of the Global Financial Crisis in 2008:

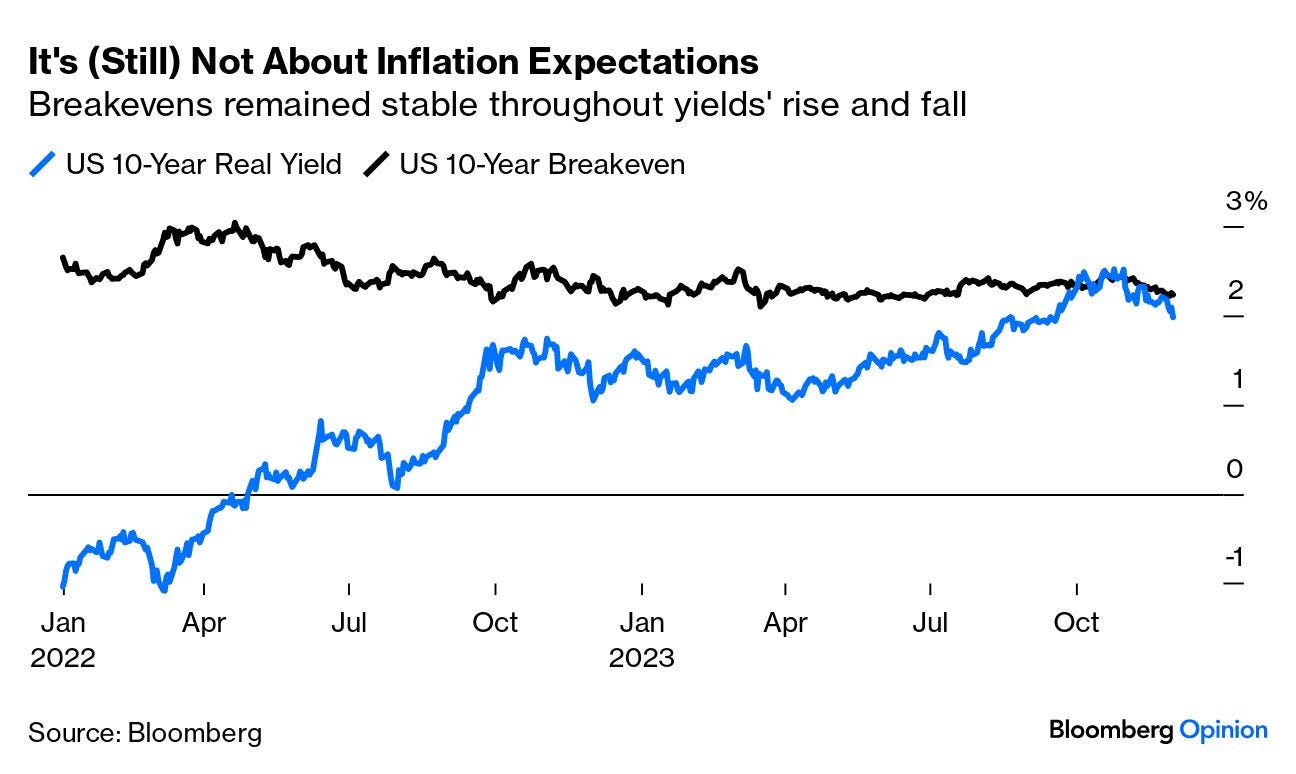

What lies behind the bond market’s change of mind? Despite appearances, it’s not really about what people expect for inflation. The 10-year yield can be split into two components — the real yield on Treasury Inflation Protected Securities, and the breakeven, or the rate of inflation that would be required for TIPS to deliver as much as the fixed-income bond. It’s the former that creates weaker or tighter conditions for financiers. And since the turn in the market at the beginning of 2022, the changes have been driven almost entirely by real yields. Very briefly, when “higher for longer” was at its peak, the real yield actually exceeded the breakeven. No more:

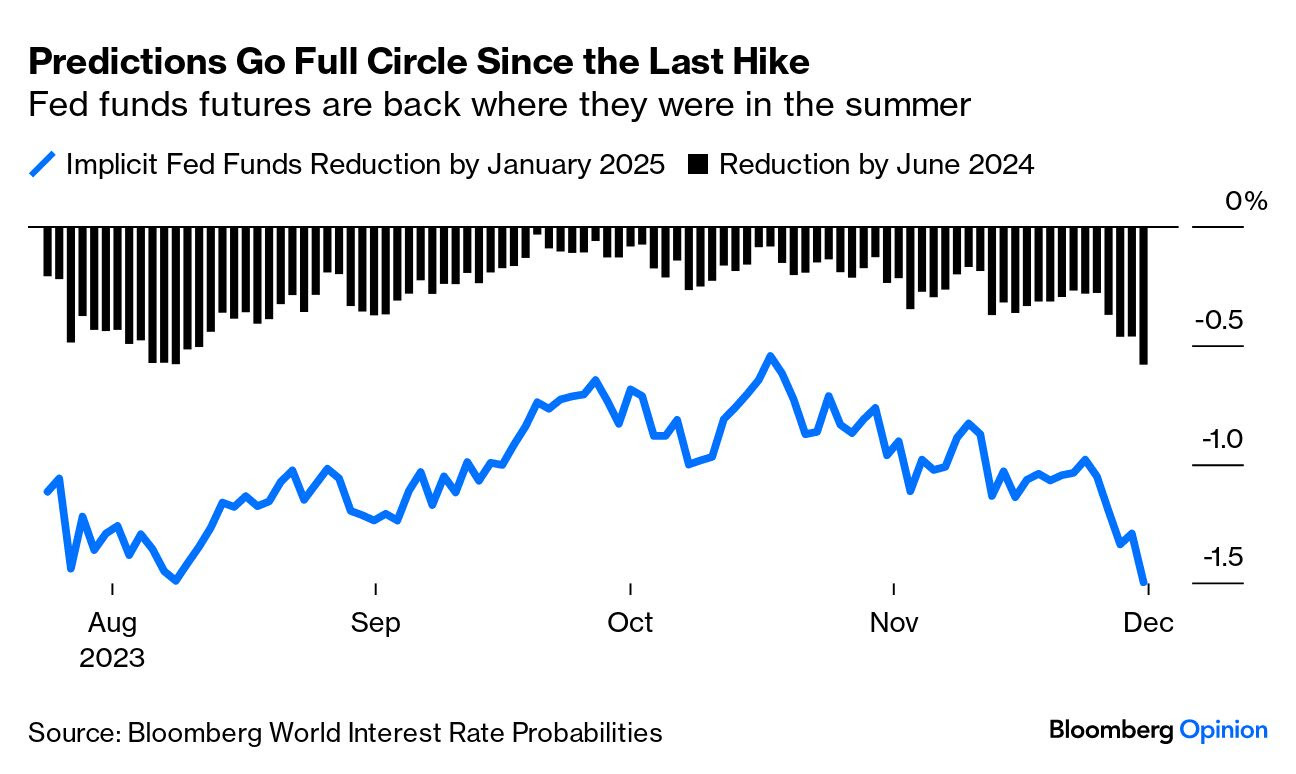

That primarily reflects a bet that the Fed will not, after all, be that aggressive. It’s been driven without substantive actions from the central bank. This is where the market forecasts have moved since the Fed last actually changed rates, in July:

Was the market right to change its mind? Neither the Fed nor the market is much good at predicting the fed funds rate. This chart from Jim Bianco or Bianco Research LLC shows the implied future course of the rate (derived from the futures market) at each meeting of the FOMC. They persistently predicted hikes throughout the post-GFC decade when rates stayed at or close to zero, and also persistently understated how far the Fed would go during the most recent cycle:

There’s no particular reason to believe that the market is right about its latest move, then…

JPMorgan: 4,200, $225 EPS (as of Nov. 29) “With a stepdown in economic growth next year (US growth to slow to 0.7% YoY by 4Q24 from 2.8% 4Q23), eroding household excess savings and liquidity, and tightening credit, we see 2024 consensus hockey-stick EPS growth of 11% as unrealistic… Negative corporate sentiment should be a catalyst for sharply lower estimates early next year.“

Morgan Stanley: 4,500, $229 EPS (as of Nov. 13) “Near-term uncertainty should give way to an earnings recovery... Our 2024 EPS estimate [of $229] is consistent with output from our leading earnings models, which show a recovery in growth next year as well as our economists' expectations for growth next year... 2025 represents a strong earnings growth environment (+16%Y) as positive operating leverage and tech-driven productivity growth (AI) lead to margin expansion. On the valuation front, we forecast a 17.0x forward P/E multiple at the end of next year (20-year average P/E is 15.6x; currently 18.1x).“

UBS: 4,600, $228 EPS (as of Nov. 8) “Our 2024 target is based on a YE 2024E multiple of 18.5x (a -0.7x multiple point contraction) applied to 2025E EPS of $249. While UBS anticipates a steep decline in yields over this period, higher equity risk premiums should offset this benefit.“

Wells Fargo: 4,625, $235 EPS (as of Nov. 27) “With VIX low, credit spreads tight, equities rallying, and cost of capital higher/volatile, it's time to downshift. Expect a volatile and ultimately flattish SPX in 2024 (4625), as valuation limits upside and rate uncertainty elevates downside risk.“

Goldman Sachs: 4,700, $237 EPS (as of Nov. 15) “Our baseline assumption during the next year is the U.S. economy continues to expand at a modest pace and avoids a recession, earnings rise by 5%, and the valuation of the equity market equals 18x, close to the current P/E level. Our forecast falls slightly below the typical 8% return during presidential election years.“

Societe Generale: 4,750, $230 EPS (as of Nov. 20) “The S&P 500 should be in ‘buy-the-dip’ territory, as leading indicators for profits continue to improve. Yet, the journey to the end of the year should be far from smooth, as we expect a mild recession in the middle of the year, a credit market sell-off in 2Q and ongoing quantitative tightening.“

Barclays: 4,800, $233 (as of Nov. 28) “Whether ‘new normal’ or ‘old,’ a roller coaster 2023 proved that this cycle is anything but. We expect US equities to deliver single-digit returns next year as easing inflation is offset by modest economic deceleration.“

Bank of America: 5,000, $235 EPS (as of Nov. 21) “The equity risk premium could fall further, especially ex-Tech: we are past maximum macro uncertainty. The market has absorbed significant geopolitical shocks already and the good news is we’re talking about the bad news. Macro signals are muddled, but idiosyncratic alpha increased this year. We’re bullish not because we expect the Fed to cut, but because of what the Fed has accomplished. Companies have adapted (as they are wont to do) to higher rates and inflation.“

RBC: 5,000, $232 EPS (as of Nov. 22) “While the November rally has likely pulled forward some of 2024’s gains, we remain constructive on the U.S. equity market in the year ahead. Our valuation and sentiment work are sending constructive signals, partially offset by headwinds from a sluggish economy and uncertainty around the 2024 Presidential election. Our work also suggests that the greater appeal of bonds may end up being a dampener of US equity market returns but not necessarily a derailer of them.“

Deutsche Bank: 5,100, $250 (as of Nov. 27) “Are valuations high? We don’t think so. If inflation returns to 2%, as economists forecast and is priced in across asset classes, while payout ratios remain elevated, fair value in our reading is 18x, with a range of 16x-20x, which they have been in for the last 2 years. If earnings growth continues to recover as we forecast, valuations will remain well supported.“

BMO: 5,100, $250 EPS (as of Nov. 27) “[W]e believe U.S. stocks will attain another year of positive returns in 2024, albeit while demonstrating more sanguine, broadly distributed, and fundamentally defined performance relative to the last decade or so. In other words, normal and typical.“

Capital Economics: 5,500 (as of Dec. 1) “Still time for the S&P 500 to party like it’s 1999 …it has come a long way lately, thanks both to a rise in its valuation and to an increase in expectations for future earnings. …This partly reflects investors’ enthusiasm about AI technology. …if AI enthusiasm is inflating a bubble in the S&P 500, it’s one that is still in its early stages. We think the index could therefore make further gains: our end-2024 forecast is 5,500, ~20% above its current level.“

Short (?) and sweet to start the week and the only good thing ‘bout FSU not making the playoffs is that I’ll get to see them vs Ohio State in The Orange Bowl?

Anyways … THAT is all for now. Off to the day job…

Excellent article.....

Been a long 3 years...

Can't blame people for getting enthusiastic about things....

Love to see 5000 S&P next year.....

I'll take the "over" on the NFP, JOLTS and ADP......

I feel bad for FSU......

Will the Bond retrace to 4.5% or higher ???

Lots of folks getting on the Rate Cut Bandwagon......